Semiconductor Testing Board Market

Semiconductor Testing Board Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702203 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

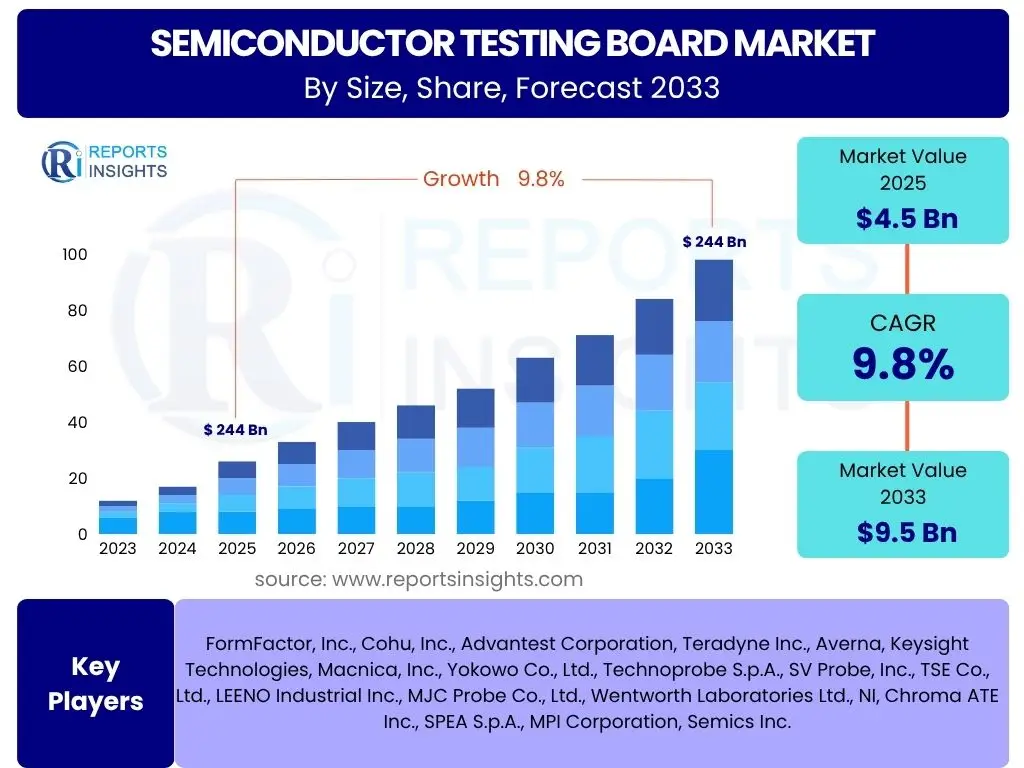

Semiconductor Testing Board Market Size

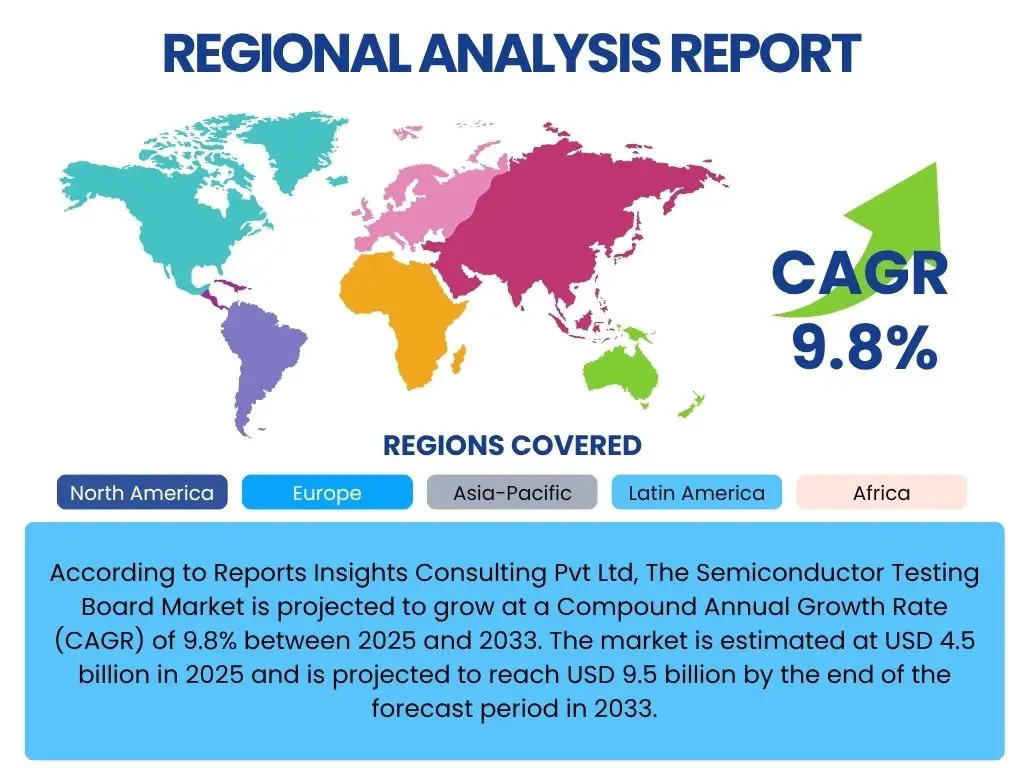

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Testing Board Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 4.5 billion in 2025 and is projected to reach USD 9.5 billion by the end of the forecast period in 2033.

Key Semiconductor Testing Board Market Trends & Insights

Current market discourse frequently revolves around the escalating demand for advanced semiconductor devices, which inherently necessitates more sophisticated testing solutions. Users commonly inquire about how the increasing complexity of integrated circuits, driven by advancements in artificial intelligence, 5G connectivity, and autonomous vehicles, translates into requirements for testing boards. There is significant interest in the transition from traditional manual testing to automated, high-throughput systems, as well as the adoption of innovative materials and design methodologies for testing boards themselves.

Another prominent area of user interest concerns the miniaturization of components and the increasing integration density of chips, which pose significant challenges for precise and reliable testing. Users also seek information on the shift towards heterogeneous integration and advanced packaging techniques (e.g., 3D ICs, chiplets), which require novel testing approaches capable of handling multi-die systems. Furthermore, the industry's drive towards sustainability and energy efficiency in manufacturing processes is prompting inquiries into eco-friendlier testing board solutions and methodologies that reduce power consumption during testing cycles.

- Miniaturization and increasing complexity of integrated circuits (ICs) driving demand for high-density, multi-functional testing boards.

- Rising adoption of advanced packaging technologies, such as 3D ICs and chiplets, necessitating specialized interface and probe solutions.

- Integration of high-speed data transfer protocols (e.g., PCIe Gen5/6, DDR5/6) into semiconductor devices, demanding higher frequency and integrity in testing board designs.

- Growing focus on test automation and robotic handling systems to enhance throughput and reduce human intervention in testing processes.

- Development of innovative materials and fabrication techniques for improved signal integrity and thermal management in testing boards.

AI Impact Analysis on Semiconductor Testing Board

Common user questions regarding AI's impact on semiconductor testing boards often center on how artificial intelligence and machine learning can optimize the testing process itself. Users are keen to understand if AI can predict potential failures, generate more efficient test patterns, or reduce the overall test time. There is a strong curiosity about AI's role in analyzing vast amounts of test data to identify anomalies and improve yields, thereby impacting the design and utilization of testing boards. Furthermore, the burgeoning market for AI-specific semiconductors, designed for complex computations, directly influences the demand for testing boards capable of validating these intricate architectures.

The application of AI in test and measurement is extending beyond mere data analysis to real-time adaptive testing, where test parameters can be dynamically adjusted based on the DUT's (Device Under Test) response, enhancing test coverage and efficiency. This necessitates testing boards that are highly configurable and integrated with intelligent control systems. Users also express interest in how AI can facilitate predictive maintenance for test equipment, including testing boards, thereby minimizing downtime and extending the lifespan of valuable assets. The drive towards 'smart factories' in semiconductor manufacturing inherently includes the intelligent management of testing infrastructure, positioning AI as a critical enabler for future advancements in test board technology and deployment.

- AI-driven test pattern generation and optimization reducing test time and improving fault coverage on testing boards.

- Machine learning algorithms enhancing defect detection and yield management through advanced data analysis of test results.

- Predictive maintenance for testing board infrastructure, leveraging AI to minimize downtime and extend equipment lifespan.

- Development of specialized testing boards for AI accelerators and neuromorphic chips, requiring validation of complex, parallel architectures.

- Integration of AI for adaptive testing methodologies, allowing testing boards to dynamically adjust parameters for optimized efficiency.

Key Takeaways Semiconductor Testing Board Market Size & Forecast

Analysis of common user questions regarding the Semiconductor Testing Board market size and forecast reveals a primary interest in understanding the underlying growth drivers and the long-term sustainability of market expansion. Users frequently inquire about which specific segments within the semiconductor industry, such as automotive, 5G, or AI, are contributing most significantly to the demand for testing boards. There is also considerable interest in regional market dynamics, particularly the dominance of Asia Pacific due to its robust semiconductor manufacturing ecosystem.

Another key area of inquiry focuses on the technological advancements required to support the projected market growth, including the need for higher frequency capabilities, improved signal integrity, and the development of testing boards for advanced packaging. Users also seek insights into the competitive landscape, asking about major players and potential new entrants that might shape future market trends. The overall sentiment suggests a market poised for substantial expansion, driven by continuous innovation in semiconductor technology and the increasing criticality of comprehensive quality assurance throughout the chip manufacturing lifecycle.

- The market is poised for robust growth, primarily fueled by the proliferation of advanced semiconductors in diverse end-use applications.

- Asia Pacific remains the dominant and fastest-growing region, driven by extensive semiconductor manufacturing and packaging activities.

- Technological advancements in testing boards, such as high-frequency capabilities and precision for complex ICs, are critical for market expansion.

- Increased R&D investments by market players and strategic collaborations are crucial for addressing evolving testing challenges.

- The automotive and telecommunications sectors are significant contributors to the escalating demand for high-reliability testing boards.

Semiconductor Testing Board Market Drivers Analysis

The increasing complexity and integration density of semiconductor devices serve as a fundamental driver for the semiconductor testing board market. As chip designs incorporate more transistors, advanced packaging techniques, and diverse functionalities onto a single die or package, the need for highly sophisticated and precise testing boards intensifies. These boards must be capable of handling high-speed signals, managing thermal dissipation, and providing accurate electrical interfaces to ensure the integrity and performance of cutting-edge semiconductors.

Furthermore, the rapid expansion of emerging technologies such as Artificial Intelligence (AI), 5G communication, Internet of Things (IoT), and autonomous vehicles is significantly propelling market growth. Each of these sectors relies heavily on advanced semiconductor components, which require rigorous and specialized testing to meet stringent performance and reliability standards. The proliferation of these applications drives continuous innovation in testing board design and manufacturing, creating sustained demand for advanced solutions across various end-use industries.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for advanced semiconductors in AI, 5G, and IoT | +2.5% | Global, particularly APAC and North America | 2025-2033 |

| Increasing complexity and miniaturization of ICs | +1.8% | Global | 2025-2033 |

| Shift towards advanced packaging technologies (e.g., 3D ICs, chiplets) | +1.5% | APAC, North America | 2025-2033 |

| Rising focus on quality, reliability, and yield optimization | +1.2% | Global | 2025-2033 |

Semiconductor Testing Board Market Restraints Analysis

One significant restraint impacting the semiconductor testing board market is the substantial capital investment required for developing and acquiring advanced testing equipment and associated boards. The complexity of modern semiconductor architectures necessitates highly specialized and costly testing solutions, which can be a barrier for smaller manufacturers or those operating with limited budgets. This high initial investment can slow down the adoption of newer testing technologies, particularly in regions with less mature semiconductor ecosystems.

Another challenge stems from the rapid technological obsolescence inherent in the semiconductor industry. As new chip designs and manufacturing processes emerge frequently, testing boards designed for previous generations can quickly become outdated. This short product lifecycle for testing boards necessitates continuous R&D investment and frequent upgrades, which adds to operational costs and can strain manufacturers' resources, potentially limiting market growth by discouraging long-term commitments to specific testing methodologies or equipment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High capital expenditure for advanced test solutions | -1.0% | Global | 2025-2030 |

| Rapid technological obsolescence of test equipment | -0.8% | Global | 2025-2033 |

| Complex supply chain and material sourcing challenges | -0.5% | Global | 2025-2028 |

| Strict regulatory compliance and environmental standards | -0.3% | Europe, North America | 2025-2033 |

Semiconductor Testing Board Market Opportunities Analysis

The burgeoning trend of Outsourced Semiconductor Assembly and Test (OSAT) services presents a significant opportunity for the semiconductor testing board market. As semiconductor companies increasingly focus on core design and research, they often outsource assembly, packaging, and testing to specialized OSAT providers. This trend drives demand for high-volume, standardized, and versatile testing boards, as OSAT companies require robust solutions capable of handling diverse chip architectures from multiple clients efficiently. Partnerships between testing board manufacturers and OSAT providers can unlock new revenue streams and foster innovation.

Furthermore, the development of new materials and advanced manufacturing techniques for testing boards themselves offers a substantial opportunity. Innovations in substrate materials, interconnect technologies, and thermal management solutions can significantly enhance the performance, longevity, and cost-effectiveness of testing boards. Opportunities also exist in developing eco-friendly and energy-efficient testing solutions, aligning with global sustainability goals and attracting companies looking to reduce their environmental footprint while maintaining high testing standards.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Outsourced Semiconductor Assembly and Test (OSAT) services | +1.5% | APAC | 2025-2033 |

| Development of new materials and advanced manufacturing techniques for boards | +1.2% | Global | 2025-2033 |

| Emergence of specialized testing needs for new technologies (e.g., quantum computing) | +0.9% | North America, Europe | 2028-2033 |

| Increasing adoption of smart manufacturing and Industry 4.0 principles | +0.7% | Global | 2025-2033 |

Semiconductor Testing Board Market Challenges Impact Analysis

One significant challenge confronting the semiconductor testing board market is the increasing difficulty in ensuring comprehensive test coverage for highly complex System-on-Chips (SoCs). Modern SoCs integrate multiple functions, often including analog, digital, RF, and memory components, onto a single chip, making it incredibly challenging to design a single testing board that can effectively test all functionalities without compromising speed or accuracy. This challenge is compounded by the need to balance test coverage with cost-effectiveness and test time, creating a perpetual engineering dilemma for manufacturers.

Another critical challenge is the shortage of skilled engineers and technicians proficient in advanced semiconductor test methodologies. The design, development, and maintenance of sophisticated testing boards and equipment require specialized expertise in electrical engineering, materials science, and software development. The global scarcity of such talent can impede innovation, delay product development, and increase operational costs, ultimately impacting the market's ability to keep pace with the rapid advancements in semiconductor technology and meet growing demand.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Difficulty in achieving comprehensive test coverage for complex SoCs | -0.9% | Global | 2025-2033 |

| Shortage of skilled workforce in test engineering | -0.7% | Global | 2025-2033 |

| High research and development costs for advanced solutions | -0.6% | Global | 2025-2030 |

| Maintaining signal integrity at ever-increasing frequencies | -0.4% | Global | 2025-2033 |

Semiconductor Testing Board Market - Updated Report Scope

This report provides an in-depth analysis of the Semiconductor Testing Board market, offering a comprehensive overview of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It incorporates detailed insights into the impact of emerging technologies like Artificial Intelligence and highlights key takeaways for stakeholders. The scope also includes a detailed competitive landscape, profiling major market players and their strategic initiatives, to provide a holistic understanding of the market dynamics from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 billion |

| Market Forecast in 2033 | USD 9.5 billion |

| Growth Rate | 9.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | FormFactor, Inc., Cohu, Inc., Advantest Corporation, Teradyne Inc., Averna, Keysight Technologies, Macnica, Inc., Yokowo Co., Ltd., Technoprobe S.p.A., SV Probe, Inc., TSE Co., Ltd., LEENO Industrial Inc., MJC Probe Co., Ltd., Wentworth Laboratories Ltd., NI, Chroma ATE Inc., SPEA S.p.A., MPI Corporation, Semics Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Testing Board market is broadly segmented across several key dimensions to provide granular insights into its diverse applications and technological requirements. These segmentations are critical for understanding specific market dynamics, identifying high-growth areas, and tailoring solutions to meet varied industry demands. Analyzing the market through these lenses allows for a detailed assessment of product adoption, application-specific needs, and the influence of different end-use sectors on overall market trajectory.

- By Product Type: This segment includes Wafer Probe Cards, Load Boards, Burn-in Boards, Interface Boards, and other specialized board types. Wafer probe cards are crucial for testing semiconductor dies at the wafer level, ensuring early defect detection. Load boards are essential for final testing of packaged integrated circuits, while burn-in boards are used for reliability testing under extreme conditions. Interface boards provide the necessary electrical and mechanical connections between the device under test and the test equipment.

- By Application: This segmentation covers the specific types of devices being tested, such as Memory Devices (DRAM, NAND, NOR), Logic Devices (CPUs, GPUs, ASICs), Mixed-Signal Devices, Radio Frequency (RF) Devices, Power Management ICs (PMICs), and Micro-electromechanical Systems (MEMS). Each application demands unique testing board specifications due to varying signal characteristics, power requirements, and functional complexities.

- By End-Use Industry: The market is further analyzed by the industries that utilize semiconductor devices, including Consumer Electronics, Automotive, Telecommunications, Industrial, Medical Devices, and Aerospace & Defense. The stringent reliability and performance requirements across these industries significantly influence the design and demand for specific types of testing boards, with automotive and aerospace sectors demanding the highest levels of robustness and precision.

- By Test Type: This segment differentiates the market based on the stage of testing, encompassing Wafer Probing, Final Test, Burn-in Test, and Functional Test. Each test type employs distinct testing methodologies and requires specialized testing boards designed for specific environments and measurement parameters, ensuring comprehensive quality assurance throughout the semiconductor manufacturing process.

Regional Highlights

- Asia Pacific (APAC): Dominates the global semiconductor testing board market due to the presence of major semiconductor manufacturing hubs in countries like Taiwan, South Korea, China, and Japan. High investments in semiconductor foundries and outsourced semiconductor assembly and test (OSAT) services, coupled with robust consumer electronics manufacturing, drive significant demand. The region is anticipated to maintain its lead and exhibit the highest growth rate during the forecast period.

- North America: A significant market driven by technological innovation, substantial R&D investments, and the presence of leading semiconductor design and equipment manufacturers. The region's focus on advanced computing, AI, and automotive electronics necessitates cutting-edge testing solutions.

- Europe: Characterized by a strong automotive sector and growing investment in industrial automation and communication technologies. Demand for high-reliability semiconductor components and testing boards is consistent, with a focus on precision engineering and stringent quality standards.

- Latin America & Middle East and Africa (MEA): Emerging markets with nascent but growing semiconductor industries. Investments in telecommunications infrastructure and localized electronics manufacturing are expected to foster gradual growth in these regions, albeit from a lower base compared to established markets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Testing Board Market.- FormFactor, Inc.

- Cohu, Inc.

- Advantest Corporation

- Teradyne Inc.

- Averna

- Keysight Technologies

- Macnica, Inc.

- Yokowo Co., Ltd.

- Technoprobe S.p.A.

- SV Probe, Inc.

- TSE Co., Ltd.

- LEENO Industrial Inc.

- MJC Probe Co., Ltd.

- Wentworth Laboratories Ltd.

- NI

- Chroma ATE Inc.

- SPEA S.p.A.

- MPI Corporation

- Semics Inc.

Frequently Asked Questions

Analyze common user questions about the Semiconductor Testing Board market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a semiconductor testing board?

A semiconductor testing board is a critical interface used in the semiconductor manufacturing process to connect a device under test (DUT) to automated test equipment (ATE). These boards facilitate the electrical and mechanical contact necessary to perform various functional, performance, and reliability tests on integrated circuits (ICs) at different stages of production, including wafer probing, final testing, and burn-in.

What are the primary drivers of growth in the Semiconductor Testing Board market?

The key drivers for market growth include the increasing complexity and miniaturization of semiconductor devices, the surging demand for advanced chips in emerging technologies like AI, 5G, IoT, and automotive electronics, and the rising focus on ensuring product quality and reliability through rigorous testing processes across the global supply chain.

How does AI impact the Semiconductor Testing Board industry?

AI significantly impacts the industry by enabling more efficient test pattern generation, optimizing test flows, and enhancing defect detection through advanced data analysis. AI also facilitates predictive maintenance for test equipment, extends product lifespan, and drives the development of specialized testing boards for AI-specific processors, making testing smarter and more efficient.

What are the main types of semiconductor testing boards?

The main types of semiconductor testing boards include wafer probe cards, used for testing dies on a silicon wafer; load boards, for final testing of packaged ICs; and burn-in boards, which perform reliability tests by subjecting devices to extreme temperature and voltage conditions over extended periods.

Which regions are most significant for the Semiconductor Testing Board market?

Asia Pacific is the most significant region, largely due to its dominant position in semiconductor manufacturing, particularly in countries like Taiwan, South Korea, China, and Japan. North America and Europe also hold substantial market shares, driven by advanced technological innovation and the presence of leading semiconductor design and equipment manufacturers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted