Automotive Semiconductor Market

Automotive Semiconductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703496 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

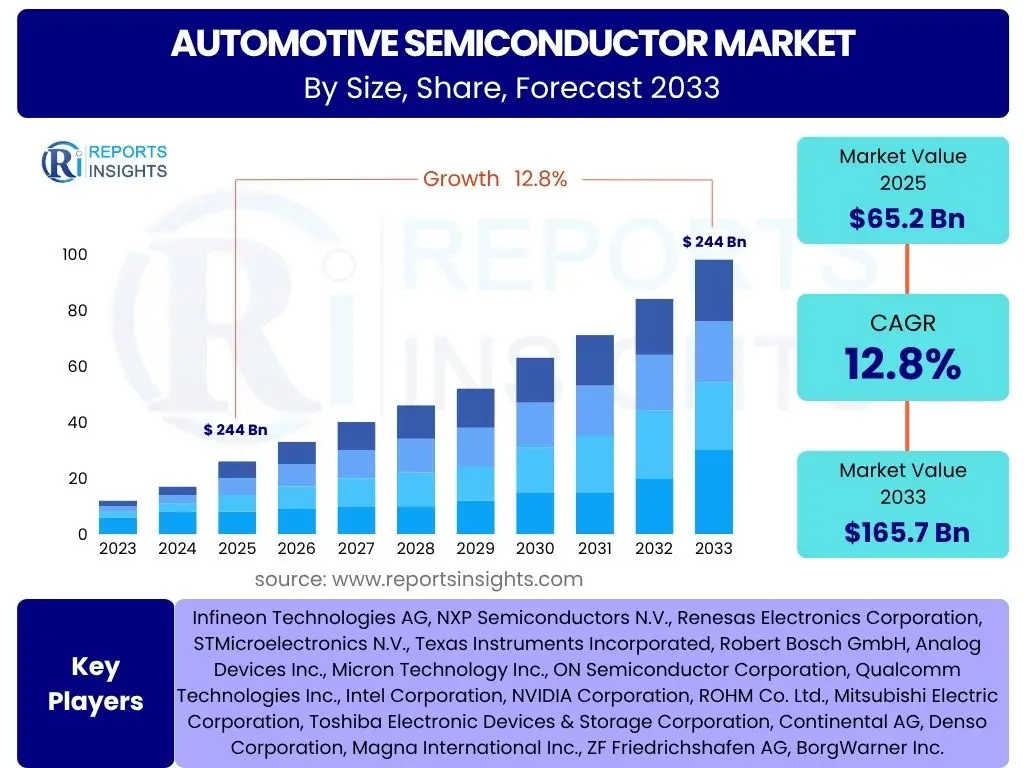

Automotive Semiconductor Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 65.2 billion in 2025 and is projected to reach USD 165.7 billion by the end of the forecast period in 2033.

Key Automotive Semiconductor Market Trends & Insights

Common user questions regarding automotive semiconductor trends frequently revolve around the impact of vehicle electrification, the progression of autonomous driving capabilities, and the pervasive integration of connectivity features. Users are keen to understand how these megatrends are reshaping demand for specific semiconductor types, driving innovation, and influencing market dynamics. The increasing complexity of automotive electronic architectures and the shift towards software-defined vehicles also generate significant interest, as these factors necessitate more advanced and powerful semiconductor solutions. Furthermore, questions often address the role of new material technologies like Silicon Carbide (SiC) and Gallium Nitride (GaN) in enhancing efficiency and performance.

A notable trend is the escalating demand for high-performance computing (HPC) units to manage the vast data processing requirements of ADAS and autonomous driving systems. This includes advanced microcontrollers (MCUs), microprocessors (MPUs), and specialized AI accelerators capable of real-time sensor fusion and decision-making. Simultaneously, the proliferation of electric vehicles (EVs) is fueling a surge in demand for power semiconductors, particularly SiC and GaN, which offer superior efficiency, reduced size, and lower weight compared to traditional silicon-based alternatives. These materials are critical for optimizing battery management systems, inverters, and onboard chargers, directly contributing to extended EV range and faster charging times.

Another significant trend is the increasing focus on software-defined vehicles (SDVs), where vehicle functions are increasingly controlled by software rather than purely hardware. This paradigm shift requires more sophisticated and flexible semiconductor architectures, capable of supporting over-the-air (OTA) updates, cloud connectivity, and advanced cybersecurity features. The integration of sensors for environmental perception, such as radar, lidar, and cameras, is also expanding rapidly, each demanding dedicated processing capabilities. Furthermore, connectivity solutions, including 5G, V2X (Vehicle-to-Everything) communication, and high-bandwidth in-car networking, are becoming standard, driving the need for robust communication chips and modules.

- Electrification of vehicles driving demand for power semiconductors (SiC, GaN).

- Increased adoption of Advanced Driver-Assistance Systems (ADAS) and autonomous driving requiring high-performance computing.

- Expansion of connected car technologies (5G, V2X) boosting communication chip demand.

- Shift towards software-defined vehicles (SDVs) necessitating flexible and powerful architectures.

- Integration of advanced sensors (Lidar, Radar, Cameras) for environmental perception.

- Growing emphasis on in-vehicle infotainment and digital cockpits.

AI Impact Analysis on Automotive Semiconductor

User inquiries concerning the impact of Artificial Intelligence (AI) on the automotive semiconductor market frequently explore how AI capabilities are being integrated into vehicle systems, the types of semiconductor technologies required to support these advancements, and the resulting performance demands. Key themes include the need for specialized AI accelerators for deep learning inference at the edge, the challenges of managing power consumption while maintaining high computational throughput, and the implications for data processing and security within the automotive environment. Users often seek to understand how AI is enabling new functionalities in autonomous driving, predictive maintenance, and intelligent cabin experiences.

The profound influence of AI on the automotive semiconductor sector is primarily evident in the escalating demand for highly specialized processing units capable of executing complex AI algorithms with low latency and high energy efficiency. These include dedicated AI accelerators, neural processing units (NPUs), and powerful GPUs optimized for parallel processing. These components are fundamental for enabling sophisticated AI functions such as real-time object recognition, path planning, driver monitoring, and predictive analysis critical for ADAS and fully autonomous driving systems. The integration of AI necessitates a shift towards heterogeneous computing architectures, combining traditional CPUs with these specialized AI engines to optimize performance for diverse workloads.

Furthermore, AI's role extends beyond core autonomous driving capabilities, influencing areas such as in-vehicle infotainment, human-machine interface (HMI), and predictive diagnostics. AI algorithms enhance voice recognition, gesture control, and personalized user experiences, requiring advanced application processors and memory solutions. The continuous learning and adaptation capabilities of AI also necessitate robust memory solutions and secure over-the-air (OTA) update mechanisms, driving innovations in non-volatile memory and embedded security hardware. The increasing volume of data generated by AI-powered vehicle sensors and systems also underscores the need for high-bandwidth communication interfaces and efficient data management solutions at the chip level.

- Increased demand for specialized AI accelerators (NPUs, GPUs) for edge computing in vehicles.

- Requirement for higher computational power and energy efficiency for AI workloads.

- Development of chip architectures optimized for real-time sensor fusion and decision-making.

- Integration of AI for advanced infotainment, personalized user experiences, and predictive maintenance.

- Enhanced focus on secure hardware for AI model protection and data integrity.

Key Takeaways Automotive Semiconductor Market Size & Forecast

Common user questions regarding key takeaways from the Automotive Semiconductor market size and forecast typically focus on identifying the most impactful growth segments, understanding the primary drivers of market expansion, and discerning the overall long-term viability and profitability of the sector. Users frequently inquire about the segments expected to experience the highest Compound Annual Growth Rate (CAGR), the resilience of the market against external economic shocks, and the strategic implications for industry stakeholders. They also often seek concise summaries of the market's trajectory and the core reasons behind its projected growth.

A central takeaway is the robust and sustained growth trajectory of the automotive semiconductor market, primarily propelled by the relentless innovation in electric vehicles (EVs), advanced driver-assistance systems (ADAS), and connected car technologies. These areas are not merely incremental improvements but represent fundamental shifts in automotive architecture, demanding significantly higher semiconductor content per vehicle. The market's expansion is characterized by a move towards more complex, higher-value chips, moving beyond basic components to sophisticated system-on-chips (SoCs), power management ICs, and advanced sensor arrays, which command premium pricing and drive overall market value.

Another crucial insight is the increasing strategic importance of semiconductor supply chain resilience within the automotive industry. Recent global events have highlighted vulnerabilities, prompting automakers and semiconductor manufacturers to forge stronger, more integrated partnerships to ensure a stable supply of critical components. This emphasizes a long-term trend towards more regionalized manufacturing and diversified sourcing strategies. Furthermore, the burgeoning demand for software-defined vehicles (SDVs) suggests that the market's future growth will increasingly depend on the seamless integration of hardware and software, creating new opportunities for semiconductor companies that can offer comprehensive, platform-level solutions.

- Market growth is robust and primarily driven by EV adoption and ADAS/autonomous driving advancements.

- Average semiconductor content per vehicle is rapidly increasing, especially in premium and electric segments.

- Focus on supply chain resilience and diversified manufacturing is a critical strategic imperative.

- Software-defined vehicle architectures are reshaping demand for advanced and flexible semiconductor solutions.

- Power semiconductors and high-performance computing chips are key segments for future growth.

Automotive Semiconductor Market Drivers Analysis

The automotive semiconductor market is experiencing significant growth driven by several powerful trends transforming the automotive industry. The global shift towards vehicle electrification, encompassing Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Fuel Cell Electric Vehicles (FCEVs), is a primary catalyst. Electric powertrains require a substantially higher number of power semiconductors, such as Silicon Carbide (SiC) and Gallium Nitride (GaN) devices, along with advanced microcontrollers and battery management integrated circuits (ICs), to efficiently manage power conversion, motor control, and battery charging, thereby boosting overall semiconductor demand per vehicle.

Concurrently, the rapid advancements in Advanced Driver-Assistance Systems (ADAS) and the progression towards fully autonomous driving capabilities are creating an insatiable demand for high-performance computing (HPC) solutions. These systems rely on an intricate network of sensors—including radar, lidar, cameras, and ultrasonic sensors—each requiring sophisticated processing units to interpret environmental data, perform real-time object detection, and execute complex decision-making algorithms. The need for faster data processing, lower latency, and higher computational power directly translates into increased chip complexity and volume within vehicles.

Moreover, the widespread integration of connectivity features, such as 5G, Vehicle-to-Everything (V2X) communication, and in-car Wi-Fi hotspots, is significantly expanding the market for communication modules, antenna tuners, and secure networking chips. These features enable cloud-based services, over-the-air (OTA) updates, and enhanced infotainment experiences, transforming vehicles into connected smart devices. The evolving landscape of software-defined vehicles (SDVs), where electronic architectures are becoming more centralized and software-centric, further necessitates adaptable and powerful semiconductors capable of supporting flexible functionalities and future upgrades, solidifying their role as indispensable components in modern automobiles.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Vehicle Electrification (EV Adoption) | +4.5% | Global, particularly China, Europe, North America | 2025-2033 |

| Advanced Driver-Assistance Systems (ADAS) & Autonomous Driving | +3.8% | Global, especially North America, Europe, Asia Pacific | 2025-2033 |

| Growing Demand for Connected Car Features & Infotainment | +2.1% | Global, strong in developed economies | 2025-2033 |

| Shift Towards Software-Defined Vehicles (SDVs) | +1.5% | Global | 2027-2033 |

Automotive Semiconductor Market Restraints Analysis

Despite robust growth drivers, the automotive semiconductor market faces several significant restraints that could temper its expansion. One prominent restraint is the inherent volatility and complexity of the global supply chain. Recent disruptions, such as the COVID-19 pandemic and geopolitical tensions, have exposed the fragility of semiconductor manufacturing and distribution networks, leading to widespread chip shortages. These shortages have directly impacted vehicle production, causing delays and lost revenue for automotive manufacturers, and highlighting the reliance on a limited number of specialized fabrication facilities, particularly for leading-edge processes.

Another considerable restraint is the high cost of research and development (R&D) and capital expenditure (CapEx) required for designing and manufacturing advanced automotive-grade semiconductors. Developing chips that meet the stringent reliability, safety, and longevity requirements of the automotive industry is a complex and expensive undertaking. The long product life cycles in automotive contrasted with faster cycles in consumer electronics, combined with the need for rigorous testing and certification, prolong the development process and increase upfront investment, making it challenging for new entrants and potentially limiting innovation speed.

Furthermore, the automotive industry's traditional business models and its cautious approach to technology adoption can act as a restraint. While innovation is embraced, the emphasis on safety and proven reliability means that new technologies often undergo lengthy validation periods before widespread integration. This conservative approach, coupled with intense cost pressure from original equipment manufacturers (OEMs), can lead to thinner profit margins for semiconductor suppliers, especially for high-volume, lower-value components. Additionally, the increasing geopolitical risks and trade tensions, particularly between major economic blocs, could further fragment supply chains and impose barriers to technology transfer, impacting market access and growth opportunities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Volatility and Geopolitical Risks | -1.2% | Global | 2025-2028 |

| High R&D Costs and Capital Expenditure | -0.8% | Global | 2025-2033 |

| Stringent Regulatory Compliance and Safety Standards | -0.5% | Europe, North America, Asia Pacific (e.g., China) | 2025-2033 |

| Complexity of Integrated Systems and Software Integration | -0.4% | Global | 2025-2033 |

Automotive Semiconductor Market Opportunities Analysis

The automotive semiconductor market presents numerous lucrative opportunities driven by technological evolution and paradigm shifts in vehicle design and functionality. One significant area of opportunity lies in the burgeoning market for Silicon Carbide (SiC) and Gallium Nitride (GaN) power semiconductors. As electric vehicles (EVs) become mainstream, the demand for more efficient, lighter, and compact power electronics is escalating. SiC and GaN offer superior performance in high-power, high-frequency, and high-temperature applications compared to traditional silicon, making them ideal for EV inverters, onboard chargers, and DC-DC converters, thereby opening up substantial growth avenues for manufacturers of these advanced materials.

Another major opportunity is the development of centralized computing architectures and domain/zone controllers within vehicles. As the industry moves towards software-defined vehicles and higher levels of autonomous driving, the traditional distributed Electronic Control Unit (ECU) architecture is being replaced by powerful central computers that integrate multiple functionalities. This shift creates a demand for highly integrated System-on-Chips (SoCs) and complex microprocessors capable of handling vast amounts of data from various sensors and systems, offering semiconductor companies the chance to provide more comprehensive, high-value solutions rather than individual components.

Furthermore, the increasing focus on in-car connectivity and cybersecurity represents a significant growth opportunity. With vehicles constantly connected to external networks, there is a heightened need for robust cybersecurity solutions embedded directly into semiconductor hardware to protect against cyber threats and ensure data integrity. This includes secure boot mechanisms, hardware-based encryption, and secure communication modules. Additionally, the development of advanced human-machine interfaces (HMIs) and immersive infotainment systems, leveraging AI and machine learning, offers avenues for innovation in display drivers, graphics processors, and specialized AI accelerators, enhancing the user experience and creating new revenue streams for semiconductor providers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Silicon Carbide (SiC) & Gallium Nitride (GaN) in EVs | +2.0% | Global | 2025-2033 |

| Development of Centralized & Domain Computing Architectures | +1.7% | Global | 2026-2033 |

| Growth in Vehicle Connectivity (5G, V2X) & Cybersecurity Solutions | +1.3% | Global | 2025-2033 |

| Advanced Infotainment Systems and Digital Cockpits | +1.0% | Global | 2025-2033 |

Automotive Semiconductor Market Challenges Impact Analysis

The automotive semiconductor market, while promising, grapples with several formidable challenges that demand strategic navigation from industry participants. One primary challenge is the inherent complexity of integrating diverse semiconductor technologies into increasingly sophisticated vehicle architectures. Modern vehicles require a seamless interplay between thousands of chips, from power management units to high-performance processors for autonomous driving, each with its own specific requirements for power, thermal management, and software compatibility. Ensuring interoperability and optimizing overall system performance across varied components poses a significant engineering hurdle and extends development cycles.

Another critical challenge is the intense pressure to balance innovation with cost-effectiveness. While automotive OEMs demand cutting-edge semiconductor solutions to enable advanced features, there is also continuous pressure to reduce overall vehicle costs. This creates a dilemma for semiconductor manufacturers, who must invest heavily in R&D for next-generation technologies while simultaneously optimizing production processes and material costs to remain competitive. The long design-in cycles and product lifespans typical in the automotive sector further complicate this, as initial investments must be amortized over a longer period, requiring foresight into future technological demands.

Furthermore, the rapid pace of technological obsolescence in the semiconductor industry presents a unique challenge for the automotive sector. While consumer electronics markets embrace rapid upgrades, automotive applications require chips with extended reliability and support over a vehicle's lifespan, often exceeding 10-15 years. This necessitates long-term supply agreements, robust obsolescence management strategies, and backward compatibility, which can strain resources and limit the adoption of the very latest chip technologies if not carefully planned. Additionally, the shortage of skilled talent in areas such as AI engineering, embedded software development, and specialized semiconductor manufacturing further exacerbates these challenges, impacting both design innovation and production capabilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of System Integration & Interoperability | -0.7% | Global | 2025-2033 |

| Balancing Innovation with Cost Pressure from OEMs | -0.6% | Global | 2025-2033 |

| Rapid Technological Obsolescence vs. Long Automotive Lifecycles | -0.5% | Global | 2025-2030 |

| Shortage of Skilled Talent and Expertise | -0.4% | Global | 2025-2033 |

Automotive Semiconductor Market - Updated Report Scope

This report provides a comprehensive analysis of the global Automotive Semiconductor Market, offering detailed insights into market size, growth drivers, restraints, opportunities, and competitive landscape. It covers market trends, technological advancements, and the impact of emerging areas like AI and software-defined vehicles across various segments and key regions, providing a strategic outlook from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.2 Billion |

| Market Forecast in 2033 | USD 165.7 Billion |

| Growth Rate | 12.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, NXP Semiconductors N.V., Renesas Electronics Corporation, STMicroelectronics N.V., Texas Instruments Incorporated, Robert Bosch GmbH, Analog Devices Inc., Micron Technology Inc., ON Semiconductor Corporation, Qualcomm Technologies Inc., Intel Corporation, NVIDIA Corporation, ROHM Co. Ltd., Mitsubishi Electric Corporation, Toshiba Electronic Devices & Storage Corporation, Continental AG, Denso Corporation, Magna International Inc., ZF Friedrichshafen AG, BorgWarner Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive semiconductor market is broadly segmented based on component type, vehicle application, vehicle type, and sales channel. This granular segmentation provides a detailed understanding of how different semiconductor technologies are consumed across various parts of the vehicle and types of automobiles, reflecting the diverse and evolving needs of the automotive industry. Each segment highlights specific growth drivers and technological advancements that are shaping market dynamics and investment priorities.

- By Component:

- Processors: Microcontrollers, Microprocessors, Digital Signal Processors (DSPs), Application-Specific Integrated Circuits (ASICs), Graphics Processing Units (GPUs), AI Accelerators

- Sensors: Image Sensors, Radar Sensors, Lidar Sensors, Ultrasonic Sensors, Pressure Sensors, Temperature Sensors, Position Sensors, Hall Effect Sensors

- Memory: Dynamic Random-Access Memory (DRAM), NAND Flash, NOR Flash, Magnetoresistive Random-Access Memory (MRAM), Phase-Change Memory (PCM)

- Power Semiconductors: Metal-Oxide-Semiconductor Field-Effect Transistors (MOSFETs), Insulated Gate Bipolar Transistors (IGBTs), Diodes, Rectifiers, Silicon Carbide (SiC), Gallium Nitride (GaN)

- Analog ICs: Amplifiers, Comparators, Voltage Regulators, Data Converters (ADCs, DACs)

- Others: LED Drivers, Transistors, Switches

- By Application:

- Powertrain: Engine Control, Transmission Control, Battery Management Systems, Motor Control

- Safety: Airbag Control, Anti-lock Braking System (ABS)/Electronic Stability Control (ESC), Advanced Driver-Assistance Systems (ADAS), Autonomous Driving, Security Gateways

- Body Electronics: Lighting Control, Power Windows, Seat Control, Heating, Ventilation, and Air Conditioning (HVAC)

- Chassis: Steering Systems, Braking Systems, Suspension Systems

- Infotainment: Navigation Systems, Audio Systems, Video Systems, Telematics Units

- Telematics & Connectivity: Vehicle-to-Everything (V2X), 5G Connectivity, Global Positioning System (GPS), Bluetooth, Wi-Fi

- By Vehicle Type:

- Passenger Vehicles: Sedans, Sports Utility Vehicles (SUVs), Hatchbacks

- Commercial Vehicles: Light Commercial Vehicles, Heavy Commercial Vehicles, Buses

- Electric Vehicles: Battery Electric Vehicles (BEV), Plug-in Hybrid Electric Vehicles (PHEV), Fuel Cell Electric Vehicles (FCEV)

- By Sales Channel:

- Original Equipment Manufacturer (OEM)

- Aftermarket

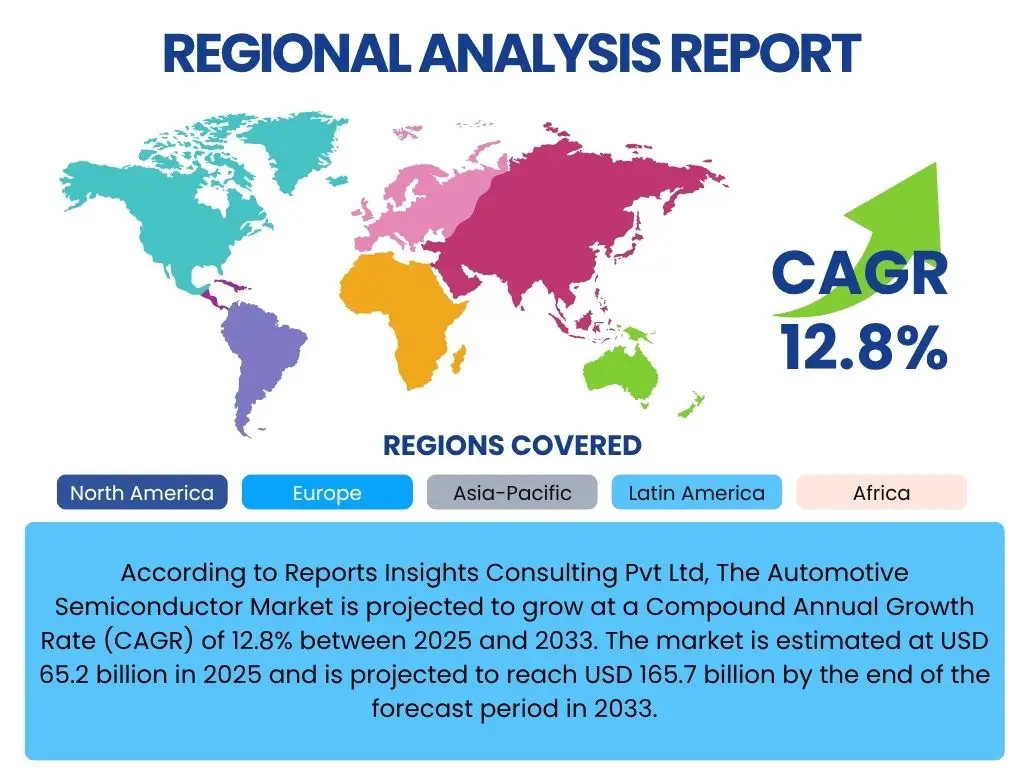

Regional Highlights

- Asia Pacific (APAC): The APAC region, especially China, Japan, and South Korea, is projected to dominate the automotive semiconductor market. This leadership is driven by the region's strong automotive manufacturing base, rapid adoption of electric vehicles, and significant investments in autonomous driving technologies. China stands out due to its massive EV market and government initiatives promoting advanced automotive technologies, leading to high demand for power semiconductors and AI-enabled chips. Japan and South Korea are key hubs for automotive electronics innovation and manufacturing, contributing significantly to sensor and memory development.

- North America: North America holds a substantial share in the automotive semiconductor market, fueled by robust research and development in autonomous driving, advanced ADAS, and growing electric vehicle adoption, particularly in the United States. The presence of leading technology companies and automotive OEMs investing heavily in next-generation vehicle architectures, including software-defined vehicles, drives demand for high-performance computing and secure connectivity solutions. Government support for EV infrastructure and domestic semiconductor manufacturing initiatives further bolsters market growth.

- Europe: Europe is a significant market for automotive semiconductors, characterized by stringent emission regulations driving EV adoption and a strong focus on automotive safety and quality standards. Countries like Germany, France, and the UK are at the forefront of automotive innovation, leading to high demand for advanced sensors, microcontrollers, and power semiconductors for powertrain and safety applications. The region's emphasis on vehicle connectivity and smart mobility solutions also contributes to the increased content of communication and security chips per vehicle.

- Latin America & Middle East and Africa (MEA): While smaller in market share compared to the developed regions, Latin America and MEA are emerging markets for automotive semiconductors, driven by increasing vehicle production, urbanization, and growing adoption of basic ADAS features and infotainment systems. Investments in local manufacturing capabilities and the gradual shift towards connected and electric vehicles are expected to contribute to a steady growth in these regions, albeit at a slower pace compared to the global average.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Semiconductor Market.- Infineon Technologies AG

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Robert Bosch GmbH

- Analog Devices Inc.

- Micron Technology Inc.

- ON Semiconductor Corporation

- Qualcomm Technologies Inc.

- Intel Corporation

- NVIDIA Corporation

- ROHM Co. Ltd.

- Mitsubishi Electric Corporation

- Toshiba Electronic Devices & Storage Corporation

- Continental AG

- Denso Corporation

- Magna International Inc.

- ZF Friedrichshafen AG

- BorgWarner Inc.

Frequently Asked Questions

Analyze common user questions about the Automotive Semiconductor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary drivers of growth in the automotive semiconductor market?

The primary drivers include the escalating adoption of electric vehicles (EVs), the rapid advancement and integration of Advanced Driver-Assistance Systems (ADAS) and autonomous driving technologies, and the increasing demand for connected car features and sophisticated in-vehicle infotainment systems. These trends collectively necessitate a higher semiconductor content per vehicle.

How is Artificial Intelligence (AI) impacting the automotive semiconductor sector?

AI significantly impacts the sector by driving demand for high-performance computing chips, specialized AI accelerators (e.g., NPUs, GPUs), and robust memory solutions. These components are essential for real-time data processing, sensor fusion, and decision-making in autonomous vehicles, as well as for enhanced in-cabin AI functionalities and predictive maintenance systems.

Which types of semiconductors are experiencing the highest growth in the automotive industry?

Power semiconductors, especially those based on Silicon Carbide (SiC) and Gallium Nitride (GaN), are seeing high growth due to EV electrification. Additionally, high-performance microcontrollers, microprocessors, and specialized AI accelerators are experiencing significant demand for ADAS, autonomous driving, and centralized computing architectures.

What are the main challenges faced by the automotive semiconductor market?

Key challenges include managing the volatility and complexity of the global supply chain, the high costs associated with R&D and capital expenditure for advanced automotive-grade chips, the intricate process of integrating diverse technologies into vehicle architectures, and balancing rapid technological innovation with the automotive industry's long product lifecycles and stringent safety standards.

Which regions are leading the market for automotive semiconductors?

The Asia Pacific (APAC) region, particularly China, Japan, and South Korea, currently leads the market due to its robust automotive manufacturing base and high EV adoption. North America and Europe also hold significant market shares, driven by strong R&D in autonomous technologies, advanced safety features, and a growing emphasis on connected and electric vehicles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted