High Purity Phosphoric Acid for Semiconductor Market

High Purity Phosphoric Acid for Semiconductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703557 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

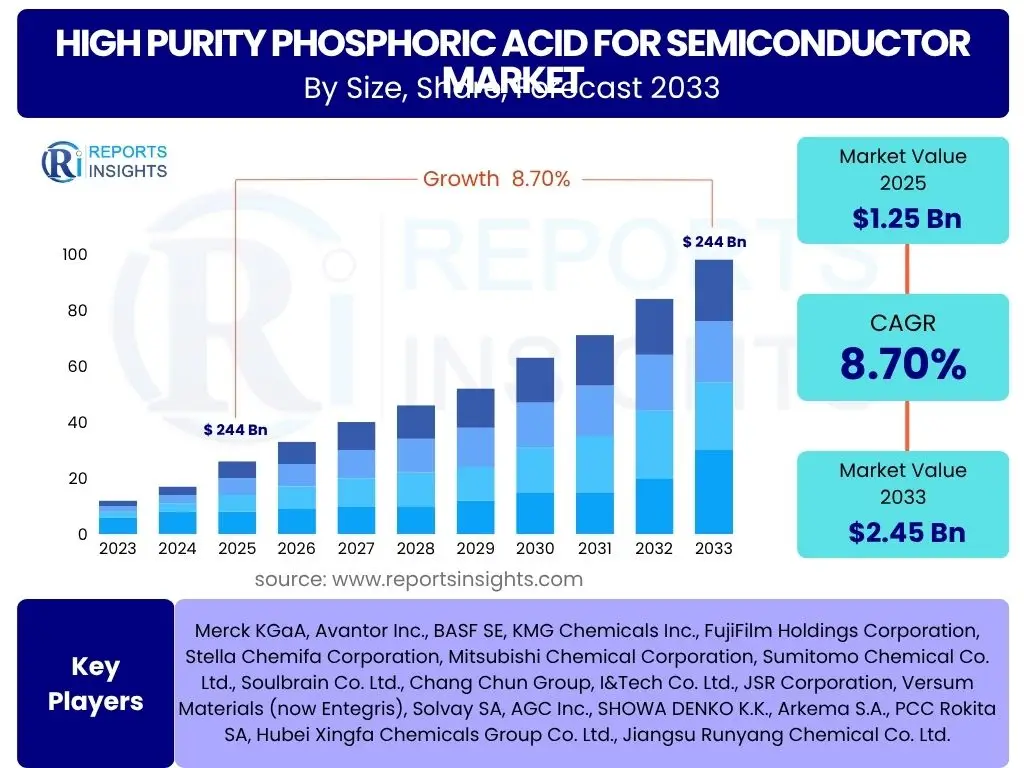

High Purity Phosphoric Acid for Semiconductor Market Size

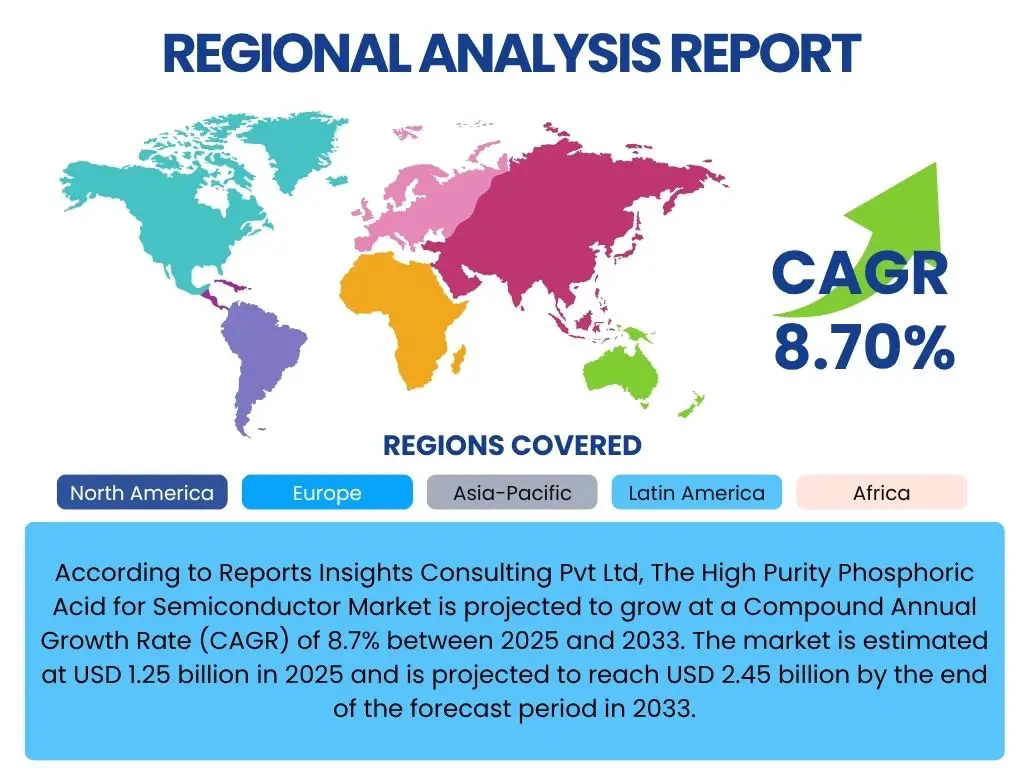

According to Reports Insights Consulting Pvt Ltd, The High Purity Phosphoric Acid for Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 1.25 billion in 2025 and is projected to reach USD 2.45 billion by the end of the forecast period in 2033.

Key High Purity Phosphoric Acid for Semiconductor Market Trends & Insights

The High Purity Phosphoric Acid for Semiconductor market is witnessing significant transformations driven by an escalating demand for advanced semiconductor devices and the continuous push for miniaturization. Users frequently inquire about the evolving purity standards, the impact of new manufacturing technologies, and the regional shifts in production and consumption. Key insights reveal a trend towards ultra-high purity grades (e.g., G5 and above) to support next-generation wafer fabrication processes, demanding tighter control over trace impurities.

Furthermore, the market is influenced by geopolitical factors and the drive for supply chain resilience, leading to diversification of sourcing and increased regional production capacities. Innovations in etching and cleaning processes, which are critical applications for phosphoric acid, are also shaping market dynamics. These advancements necessitate continuous research and development into more efficient and environmentally friendly production methods for high-purity chemicals, addressing user concerns about sustainability and operational efficiency.

The convergence of increasing data processing needs from AI, IoT, and 5G technologies directly correlates with the demand for more sophisticated and contaminant-free semiconductor components, thereby bolstering the high-purity phosphoric acid market. This intricate relationship underscores the criticality of this specialty chemical in enabling future technological progress and maintaining global competitive advantage in the semiconductor industry.

- Increasing demand for ultra-high purity grades (G5 and above) for advanced semiconductor manufacturing.

- Growth in silicon wafer production and expansion of fabrication plants globally.

- Emphasis on supply chain diversification and regionalization to enhance resilience.

- Technological advancements in etching and cleaning processes demanding specialized acid formulations.

- Rising adoption of 5G, AI, and IoT devices driving demand for high-performance chips.

AI Impact Analysis on High Purity Phosphoric Acid for Semiconductor

Common user questions regarding AI's impact on the High Purity Phosphoric Acid for Semiconductor market often revolve around its potential to optimize production, enhance quality control, and influence demand forecasting. AI and machine learning algorithms are increasingly being deployed in the chemical manufacturing sector to monitor and control complex purification processes. This leads to reduced waste, improved yield, and consistent achievement of ultra-high purity levels, directly benefiting the production of phosphoric acid for semiconductors where impurity levels are measured in parts per trillion.

Beyond process optimization, AI contributes significantly to predictive maintenance of manufacturing equipment, minimizing downtime and ensuring continuous supply. Furthermore, AI-driven analytics can process vast amounts of market data, including semiconductor industry growth rates, regional fab expansions, and technological shifts, to provide more accurate demand forecasts for high-purity chemicals. This allows manufacturers to better anticipate market needs, optimize inventory management, and make informed strategic investment decisions.

While the direct integration of AI into the chemical composition of phosphoric acid is not applicable, its indirect influence on the efficiency, quality assurance, and supply chain management of high-purity chemical production is substantial. This technological synergy helps meet the stringent demands of the semiconductor industry, ensuring the availability of critical materials with unparalleled consistency and purity.

- AI-driven optimization of chemical purification processes, leading to enhanced purity and yield.

- Improved quality control and defect detection through AI-powered inspection systems.

- More accurate demand forecasting for high-purity chemicals based on AI-powered market analysis.

- Predictive maintenance of manufacturing equipment reducing operational downtime.

- Automation of hazardous chemical handling procedures, improving safety and efficiency.

Key Takeaways High Purity Phosphoric Acid for Semiconductor Market Size & Forecast

The High Purity Phosphoric Acid for Semiconductor market is poised for robust growth, driven primarily by the relentless expansion of the global semiconductor industry. Users frequently seek concise insights into the market's long-term viability, key growth drivers, and potential investment opportunities. A key takeaway is the critical role of increasing purity demands; as semiconductor device geometries shrink and complexity rises, the need for G5 and higher-grade phosphoric acid becomes paramount, ensuring the market's sustained upward trajectory.

The forecast highlights significant opportunities for companies that can consistently meet stringent purity specifications and navigate complex global supply chains. Furthermore, the geographical concentration of semiconductor manufacturing in Asia-Pacific positions this region as the primary growth engine, albeit with emerging efforts in other regions to localize production. This suggests a nuanced approach to market entry and expansion, focusing on partnerships and strategic investments in high-growth fabrication hubs.

In essence, the market's future is intrinsically linked to technological advancements in semiconductors, making it a vital and resilient segment within the specialty chemicals industry. Companies capable of innovating purification processes, ensuring supply chain stability, and adhering to strict quality standards are well-positioned to capitalize on this expanding market.

- Market demonstrates robust growth, projected to nearly double by 2033, driven by semiconductor industry expansion.

- The imperative for ultra-high purity grades (G5+) is a central growth catalyst.

- Asia-Pacific remains the dominant region, while North America and Europe show strategic growth initiatives.

- Technological innovation in purification and supply chain resilience are critical for market success.

- Opportunities exist for investments in R&D and manufacturing capacity for specialized acid grades.

High Purity Phosphoric Acid for Semiconductor Market Drivers Analysis

The High Purity Phosphoric Acid for Semiconductor market is primarily propelled by the exponential growth of the semiconductor industry, which underpins virtually all modern electronic devices. As demand for smartphones, data centers, AI processors, and IoT devices continues to surge, the need for more advanced and smaller semiconductor chips intensifies. This directly translates into higher demand for ultra-pure specialty chemicals, including phosphoric acid, which is crucial for etching and cleaning processes during wafer fabrication. The continuous pursuit of miniaturization and higher performance in integrated circuits necessitates stricter purity levels for all input materials, driving innovation in phosphoric acid manufacturing.

Furthermore, the ongoing expansion of fabrication plant (fab) capacities globally, particularly in Asia-Pacific, North America, and Europe, serves as a significant market driver. Governments and private entities are investing heavily in new fab construction and upgrades to enhance domestic semiconductor production capabilities and reduce reliance on single regions. Each new fab, or expansion of an existing one, represents a substantial increase in the consumption of high-purity phosphoric acid. This capital expenditure on new manufacturing facilities ensures a sustained and growing demand for the specialized acid over the forecast period.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Exponential Growth of Semiconductor Industry | +2.5% | Global, especially APAC, North America, Europe | Long-term (2025-2033) |

| Increasing Demand for Advanced Purity Grades | +1.8% | Global, particularly advanced manufacturing hubs | Mid to Long-term (2025-2033) |

| Expansion of Global Wafer Fabrication Capacities | +1.5% | China, Taiwan, South Korea, US, Japan, EU | Mid-term (2025-2029) |

| Technological Advancements in Etching and Cleaning Processes | +0.9% | Leading semiconductor R&D countries | Continuous |

| Growth in End-use Applications (5G, AI, IoT, Automotive) | +1.2% | Global | Long-term (2025-2033) |

High Purity Phosphoric Acid for Semiconductor Market Restraints Analysis

The High Purity Phosphoric Acid for Semiconductor market faces several significant restraints that could temper its growth trajectory. One primary concern is the escalating cost of achieving and maintaining ultra-high purity levels. The purification processes for semiconductor-grade phosphoric acid are highly complex, energy-intensive, and require specialized equipment, leading to higher production costs compared to technical or food-grade phosphoric acid. These high costs can sometimes be a barrier, particularly for new entrants or smaller players, and can influence the final price of semiconductor components, potentially impacting demand if cost-effective alternatives emerge.

Another notable restraint is the stringent environmental regulations and disposal challenges associated with phosphoric acid production and usage. The manufacturing process generates by-products and waste streams that require careful management and disposal, often under strict environmental compliance. Adherence to these regulations adds to operational costs and can limit expansion opportunities in regions with very strict environmental protection policies. Additionally, the handling and transportation of corrosive chemicals like phosphoric acid pose logistical challenges and safety risks, requiring specialized infrastructure and expertise, which further contributes to operational complexities and costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Ultra-Purification Processes | -1.3% | Global | Long-term |

| Stringent Environmental Regulations and Waste Disposal | -1.0% | Europe, North America, China | Long-term |

| Supply Chain Vulnerabilities and Geopolitical Risks | -0.8% | Global, particularly dependent on specific regions for raw materials | Short to Mid-term (2025-2028) |

| Volatility in Raw Material Prices (Phosphate Rock) | -0.7% | Global | Mid-term |

| Competition from Alternative Etchants/Cleaning Agents | -0.5% | Global, R&D focused regions | Long-term |

High Purity Phosphoric Acid for Semiconductor Market Opportunities Analysis

The High Purity Phosphoric Acid for Semiconductor market presents several compelling opportunities for growth and innovation. A significant opportunity lies in the continuous advancement of semiconductor technology, particularly the development of smaller node sizes and 3D stacking architectures. These innovations demand even higher purity levels and precise etching characteristics, opening avenues for manufacturers to develop and commercialize next-generation ultra-high purity phosphoric acid grades (e.g., beyond G5). Companies capable of meeting these evolving, stringent specifications through advanced purification techniques will gain a competitive edge and unlock new revenue streams.

Furthermore, the ongoing trend of semiconductor manufacturing capacity expansion in regions like North America and Europe, driven by national security and supply chain diversification initiatives, presents a substantial opportunity. As these new fabs come online, they will require reliable and localized sources of high-purity chemicals. This creates an impetus for investment in new production facilities or partnerships within these regions, reducing reliance on traditional Asian supply hubs. The development of sustainable and circular economy practices in chemical manufacturing also offers an opportunity for companies to differentiate themselves by adopting greener production methods and waste recycling, aligning with global environmental objectives and potentially attracting environmentally conscious clients.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Next-Gen Ultra-High Purity Grades (e.g., G6, G7) | +1.5% | Global, R&D focused regions | Mid to Long-term (2027-2033) |

| Expansion of Semiconductor Fabs in New Geographies (e.g., US, EU) | +1.2% | North America, Europe, Japan, India | Mid-term (2025-2030) |

| Strategic Partnerships and Collaborations with Semiconductor Manufacturers | +0.9% | Global | Continuous |

| Focus on Sustainable Production and Recycling Technologies | +0.7% | Europe, North America, Japan | Long-term |

| Emerging Applications (Quantum Computing, Advanced Packaging) | +0.6% | Global | Long-term |

High Purity Phosphoric Acid for Semiconductor Market Challenges Impact Analysis

The High Purity Phosphoric Acid for Semiconductor market encounters several significant challenges that necessitate strategic navigation by industry players. One major challenge is maintaining the extremely high purity specifications required by semiconductor manufacturers, particularly as chip designs become more intricate and demanding. Any trace impurity can significantly compromise chip performance and yield, leading to substantial financial losses for foundries. This demands continuous investment in sophisticated purification technologies, rigorous quality control measures, and advanced analytical instrumentation, which can be capital-intensive and complex to implement.

Another critical challenge revolves around the stability and resilience of the global supply chain. The raw materials for phosphoric acid, primarily phosphate rock, are concentrated in a few geographic regions, making the supply vulnerable to geopolitical tensions, trade disputes, and natural disasters. Furthermore, the specialized nature of high-purity chemical manufacturing means that disruptions at any point in the supply chain can have ripple effects throughout the semiconductor industry, potentially leading to material shortages and production delays. Managing these risks requires diversification of sourcing, strategic inventory management, and potentially localized production capabilities, which adds to operational complexity and cost.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving and Maintaining Ultra-High Purity Standards | -1.2% | Global | Continuous |

| Supply Chain Disruptions and Geopolitical Volatility | -1.0% | Global | Short to Mid-term (2025-2028) |

| Intense Competition Among Key Players | -0.8% | Global, particularly APAC | Long-term |

| High Capital Investment and R&D Costs | -0.7% | Global | Long-term |

| Managing Hazardous Material Handling and Transportation | -0.6% | Global | Continuous |

High Purity Phosphoric Acid for Semiconductor Market - Updated Report Scope

This report provides an in-depth analysis of the High Purity Phosphoric Acid for Semiconductor Market, covering market size estimations, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It offers a comprehensive segmentation analysis by purity grade, application, and end-use, alongside a detailed regional outlook. The report also profiles leading market players, offering strategic insights for stakeholders to navigate the complex dynamics of this critical specialty chemicals market supporting the global semiconductor industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.45 Billion |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Merck KGaA, Avantor Inc., BASF SE, KMG Chemicals Inc., FujiFilm Holdings Corporation, Stella Chemifa Corporation, Mitsubishi Chemical Corporation, Sumitomo Chemical Co. Ltd., Soulbrain Co. Ltd., Chang Chun Group, I&Tech Co. Ltd., JSR Corporation, Versum Materials (now Entegris), Solvay SA, AGC Inc., SHOWA DENKO K.K., Arkema S.A., PCC Rokita SA, Hubei Xingfa Chemicals Group Co. Ltd., Jiangsu Runyang Chemical Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The High Purity Phosphoric Acid for Semiconductor market is rigorously segmented to provide granular insights into its diverse applications and purity requirements. Segmentation by purity grade is crucial, as the semiconductor industry increasingly demands ultra-high purity levels, categorized from G1 to G5 and beyond, with G5+ being critical for advanced node manufacturing. Each grade caters to specific stages of wafer processing, and understanding the demand shift across these grades is vital for manufacturers to align their production capabilities and R&D efforts.

Application-wise segmentation, including etching, cleaning, and wafer processing, highlights the primary uses of high-purity phosphoric acid. Etching processes, which involve precise removal of materials, represent a significant consumption segment due to the acid's ability to selectively etch silicon nitride and other films. Cleaning applications, critical for removing contaminants between processing steps, also account for substantial demand. Analyzing these segments helps identify specific technological shifts and their impact on demand for particular acid properties.

Furthermore, segmentation by end-use industry, such as memory devices, logic and microprocessor units, power devices, and optoelectronics, offers insights into which semiconductor sectors are driving demand. Different end-use devices have varying purity and volume requirements, providing a nuanced view of market opportunities and growth pockets. This comprehensive segmentation allows stakeholders to develop targeted strategies, optimize resource allocation, and foster innovation across the value chain, ensuring that the specialized needs of the evolving semiconductor landscape are met.

- By Purity Grade:

- G1

- G2

- G3

- G4

- G5 and Above

- By Application:

- Etching

- Cleaning

- Wafer Processing

- Others

- By End-Use Industry:

- Memory Devices (DRAM, NAND)

- Logic & Microprocessor Units (MPU)

- Power Devices

- Analog & Mixed-Signal ICs

- Optoelectronics

- MEMS

Regional Highlights

- Asia Pacific (APAC): The dominant region in the High Purity Phosphoric Acid for Semiconductor market, primarily due to the presence of major semiconductor manufacturing hubs in Taiwan, South Korea, China, and Japan. APAC accounts for the largest share of global semiconductor fabrication capacity, driving substantial demand for ultra-high purity phosphoric acid for wafer production, etching, and cleaning processes. The region continues to attract significant investments in new fabs and technology nodes, solidifying its leading position and projecting robust growth throughout the forecast period. Countries like China and India are also expanding their domestic semiconductor ecosystems, further contributing to regional market growth.

- North America: A significant market for high purity phosphoric acid, driven by substantial investments in semiconductor research and development, as well as new fab construction initiatives. The region's focus on advanced computing, AI chips, and specialized defense applications necessitates the highest purity grades of phosphoric acid. Government incentives and strategic initiatives to reshore semiconductor manufacturing are expected to boost demand for domestic sourcing of specialty chemicals, fostering growth and innovation in purification technologies.

- Europe: The European market is characterized by a strong emphasis on automotive semiconductors, industrial electronics, and R&D in advanced materials. While not as dominant in volume as APAC, Europe's stringent quality standards and focus on innovation drive demand for high-purity phosphoric acid for specialized applications. The EU Chips Act and similar regional initiatives are aimed at increasing domestic semiconductor production, which will consequently drive demand for critical input materials like high-purity phosphoric acid, emphasizing local supply chain resilience.

- Latin America: This region represents a smaller but emerging market, primarily driven by growing electronics assembly operations and expanding industrial sectors. While direct semiconductor fabrication is limited, increased demand for electronic components in automotive and consumer electronics industries contributes to a gradual rise in demand for specialty chemicals used in precursor manufacturing or local assembly processes. Future growth is contingent on further development of the regional electronics manufacturing ecosystem.

- Middle East and Africa (MEA): Currently, the MEA market for high purity phosphoric acid in semiconductors is nascent, with limited direct semiconductor manufacturing capabilities. Demand is largely influenced by general electronics assembly and maintenance activities. However, long-term opportunities may arise from diversification efforts in key economies and potential investments in technology infrastructure, which could indirectly stimulate demand for imported high-purity chemicals required for electronic components.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the High Purity Phosphoric Acid for Semiconductor Market.- Merck KGaA

- Avantor Inc.

- BASF SE

- KMG Chemicals Inc.

- FujiFilm Holdings Corporation

- Stella Chemifa Corporation

- Mitsubishi Chemical Corporation

- Sumitomo Chemical Co. Ltd.

- Soulbrain Co. Ltd.

- Chang Chun Group

- I&Tech Co. Ltd.

- JSR Corporation

- Versum Materials (now Entegris)

- Solvay SA

- AGC Inc.

- SHOWA DENKO K.K.

- Arkema S.A.

- PCC Rokita SA

- Hubei Xingfa Chemicals Group Co. Ltd.

- Jiangsu Runyang Chemical Co. Ltd.

Frequently Asked Questions

Analyze common user questions about the High Purity Phosphoric Acid for Semiconductor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is High Purity Phosphoric Acid for Semiconductors?

High Purity Phosphoric Acid for Semiconductors is an ultra-pure chemical extensively used in the fabrication of integrated circuits. It plays a crucial role in etching silicon nitride layers and cleaning silicon wafers during various stages of semiconductor manufacturing, ensuring the integrity and performance of microelectronic components by minimizing contamination.

What are the primary applications of High Purity Phosphoric Acid in the semiconductor industry?

The primary applications include selective etching of silicon nitride and other thin films, as well as critical cleaning processes for silicon wafers. These processes are essential for removing impurities and preparing wafer surfaces for subsequent fabrication steps, directly impacting chip yield and reliability.

How are purity grades determined for semiconductor-grade phosphoric acid?

Purity grades, such as G1 through G5 and beyond, are determined by the maximum allowable concentrations of trace metallic impurities and particulate matter. G5 and higher grades denote ultra-low impurity levels, often in parts per trillion (ppt), necessary for advanced semiconductor nodes and demanding etching applications.

What drives the growth of the High Purity Phosphoric Acid for Semiconductor Market?

Key growth drivers include the continuous expansion of the global semiconductor industry, increasing demand for advanced electronic devices (5G, AI, IoT), the ongoing miniaturization of chip architectures, and the construction of new wafer fabrication plants worldwide. The imperative for higher purity levels in etching and cleaning also fuels market growth.

Which regions are key consumers of High Purity Phosphoric Acid for Semiconductors?

Asia Pacific, particularly Taiwan, South Korea, China, and Japan, is the largest consumer due to its dominant semiconductor manufacturing capacity. North America and Europe are also significant markets, driven by R&D, advanced chip production, and strategic initiatives to enhance regional supply chain resilience.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted