Pyrogen Testing Market

Pyrogen Testing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703552 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

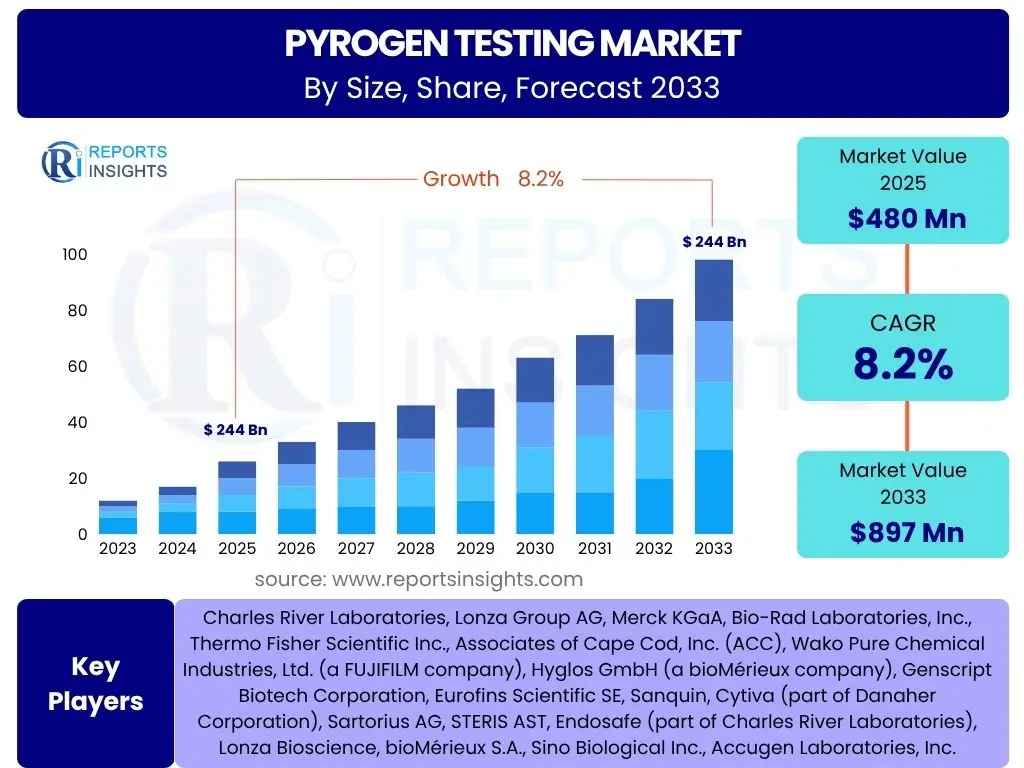

Pyrogen Testing Market Size

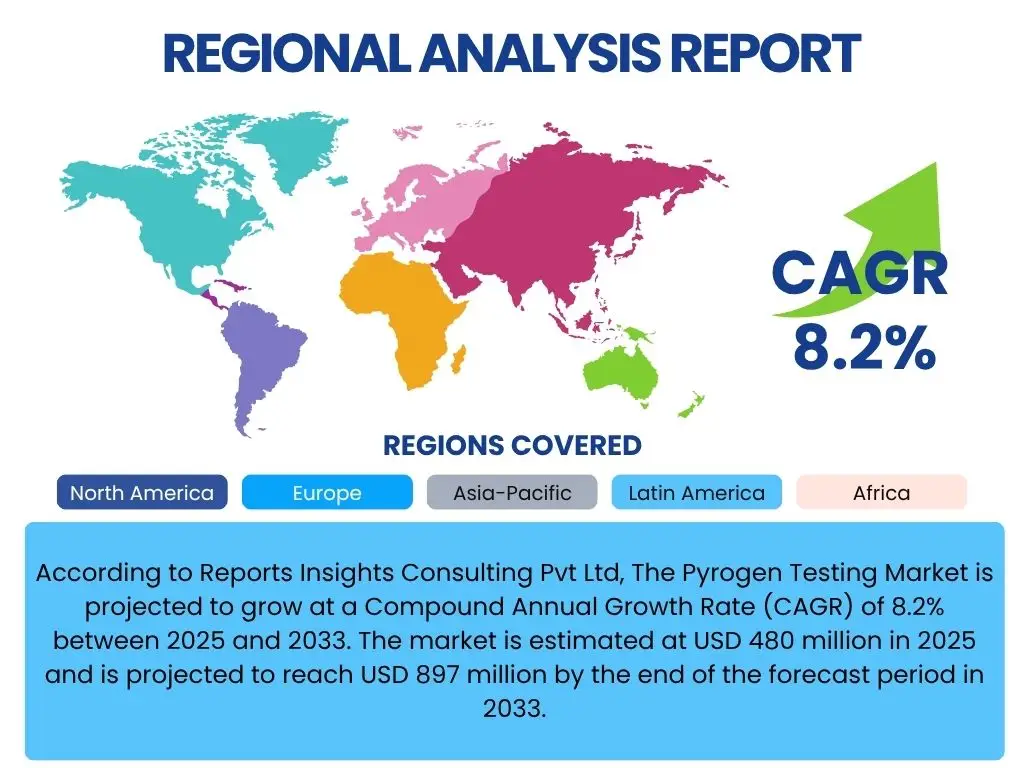

According to Reports Insights Consulting Pvt Ltd, The Pyrogen Testing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 480 million in 2025 and is projected to reach USD 897 million by the end of the forecast period in 2033.

Key Pyrogen Testing Market Trends & Insights

The pyrogen testing market is significantly influenced by a confluence of evolving regulatory landscapes, advancements in testing methodologies, and increasing demand from the pharmaceutical and biotechnology sectors. Users frequently inquire about the shift from traditional Limulus Amebocyte Lysate (LAL) tests to more ethical and high-throughput alternative methods, such as Monocyte Activation Tests (MAT) and recombinant Factor C (rFC) assays. The emphasis on rapid, accurate, and automated testing solutions is a prominent theme, driven by the need for quicker drug development cycles and enhanced product safety.

Another key area of interest revolves around the globalization of pharmaceutical manufacturing and the harmonization of regulatory standards across different regions. This necessitates adaptable and widely accepted pyrogen testing protocols. Furthermore, the rising investment in biopharmaceutical research and development, particularly for complex biological drugs and vaccines, amplifies the demand for sophisticated and highly sensitive pyrogen detection methods. The integration of digital solutions for data management and analysis in testing laboratories is also gaining traction, streamlining workflows and improving data integrity.

The market also observes a trend towards outsourcing pyrogen testing services to Contract Research Organizations (CROs) and Contract Manufacturing Organizations (CMOs), particularly among smaller pharmaceutical companies lacking in-house capabilities or seeking to optimize operational costs. This trend not only facilitates access to specialized expertise and advanced instrumentation but also enables companies to focus on their core competencies. The push for sustainability and reduction of animal use in research further accelerates the adoption of in vitro and non-animal pyrogen testing methods, reshaping the market's technological trajectory and regulatory acceptance.

- Shift from animal-derived LAL to synthetic and in vitro alternatives (rFC, MAT).

- Increasing adoption of high-throughput and automated pyrogen testing systems.

- Growing demand for pyrogen testing in biopharmaceutical and vaccine production.

- Harmonization of global regulatory guidelines for product safety and quality.

- Expansion of outsourcing pyrogen testing services to CROs and CMOs.

AI Impact Analysis on Pyrogen Testing

The integration of Artificial Intelligence (AI) within the pyrogen testing domain is a subject of growing interest, with common user questions focusing on how AI can enhance efficiency, accuracy, and data interpretation. AI's primary impact is anticipated in optimizing experimental design, analyzing complex data sets generated by advanced in vitro assays, and predicting potential pyrogen contamination risks based on historical data and material characteristics. This predictive capability could significantly reduce the need for extensive physical testing in certain stages, accelerating product development timelines.

AI algorithms can facilitate the identification of novel pyrogens or pyrogen-like substances by analyzing molecular structures and biological interactions, moving beyond traditional endotoxin-centric detection. Furthermore, AI-powered systems can enable advanced automation in laboratory settings, from robotic handling of samples to intelligent process control for automated testing instruments. This level of automation promises to minimize human error, increase throughput, and ensure greater consistency in testing outcomes, addressing critical concerns regarding reproducibility and scalability in pyrogen detection.

While the full extent of AI's transformative potential is still unfolding, its application in areas such as predictive maintenance for testing equipment, robust quality control, and streamlined regulatory reporting through intelligent data synthesis is highly anticipated. Concerns, however, revolve around the validation of AI models in highly regulated environments, the need for large, high-quality datasets for training, and the ethical implications of AI-driven decision-making in critical safety assessments. Despite these challenges, AI is poised to revolutionize the pyrogen testing landscape by enabling more intelligent, efficient, and robust safety evaluations.

- Enhanced data analysis and interpretation for complex assay results.

- Predictive modeling for identifying potential pyrogen contamination risks.

- Optimization of experimental design and automation in testing workflows.

- Facilitating the discovery and characterization of novel pyrogens.

- Improved quality control and streamlined regulatory documentation through intelligent systems.

Key Takeaways Pyrogen Testing Market Size & Forecast

Analysis of user inquiries concerning the Pyrogen Testing Market's size and forecast reveals a strong interest in understanding the underlying growth drivers, the longevity of traditional methods versus emerging alternatives, and the regional disparities in market development. A key takeaway is the consistent, robust growth projected for the market, primarily fueled by the expanding pharmaceutical and biotechnology sectors, which necessitates stringent quality control for parenteral drugs, vaccines, and medical devices. This growth is not uniform across all segments, with in vitro and rapid testing methods expected to gain significant market share over conventional tests.

The forecast indicates a sustained shift towards more ethical, sensitive, and high-throughput testing solutions. This transition is not merely a technological evolution but also a response to increasing regulatory pressure to reduce animal testing and enhance patient safety. Stakeholders are particularly keen on understanding how these technological advancements will influence operational costs, turnaround times, and overall compliance in their respective industries. The competitive landscape is evolving, with both established players and innovative startups vying for market leadership through new product development and strategic collaborations.

Ultimately, the market forecast underscores a dynamic environment where regulatory mandates, technological innovation, and evolving industry demands collectively shape the future of pyrogen testing. Companies that invest in advanced, compliant, and efficient testing methodologies, particularly those that reduce reliance on animal models, are poised for significant growth. Furthermore, regional market dynamics suggest that while mature markets in North America and Europe continue to dominate, emerging economies in Asia Pacific are rapidly accelerating their adoption of advanced pyrogen testing, presenting substantial opportunities for market expansion and diversification.

- Significant market growth driven by biopharmaceutical expansion and regulatory stringency.

- Accelerated adoption of advanced in vitro and non-animal pyrogen testing methods.

- Increasing investment in automated and high-throughput testing solutions.

- North America and Europe to maintain strong market positions; Asia Pacific to show rapid growth.

- Focus on cost-efficiency, faster turnaround times, and enhanced safety in testing processes.

Pyrogen Testing Market Drivers Analysis

The pyrogen testing market is primarily driven by the escalating demand for parenteral drugs, medical devices, and other sterile products, necessitating rigorous quality and safety checks. The rapid expansion of the biopharmaceutical industry, particularly in the development of complex biologics, vaccines, and advanced therapies, significantly contributes to this demand. These products require meticulous pyrogen detection to ensure patient safety and regulatory compliance, thereby propelling the adoption of advanced testing methodologies. Furthermore, the global rise in chronic diseases and infectious outbreaks continually fuels pharmaceutical research and development, indirectly boosting the pyrogen testing market.

Stringent regulatory guidelines imposed by global health authorities such as the FDA, EMA, and pharmacopoeias worldwide are a fundamental driver. These regulations mandate comprehensive pyrogen testing for all injectable drugs and medical devices, pushing manufacturers to invest in compliant and validated testing solutions. The continuous updates and harmonization of these guidelines globally further ensure a baseline requirement for pyrogen detection. The increasing awareness among consumers and healthcare professionals regarding product safety and quality also pressures manufacturers to adopt robust testing protocols, enhancing market demand for reliable pyrogen testing services and products.

Technological advancements in pyrogen testing methods, particularly the development of more sensitive, specific, and ethical alternatives to animal testing, serve as a significant market driver. The shift towards in vitro methods like the Monocyte Activation Test (MAT) and recombinant Factor C (rFC) assays addresses concerns about animal welfare and offers higher throughput and reproducibility. These innovations attract greater adoption by pharmaceutical and biotechnology companies looking for efficient and modern testing solutions. The growing trend of outsourcing testing services to specialized Contract Research Organizations (CROs) and Contract Development and Manufacturing Organizations (CDMOs) further facilitates market growth by providing access to advanced testing infrastructure and expertise.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing R&D in Biopharmaceuticals | +2.1% | Global, particularly North America, Europe, APAC | 2025-2033 (Long-term) |

| Stringent Regulatory Guidelines | +1.8% | Global, highly impactful in regulated markets | 2025-2033 (Ongoing) |

| Technological Advancements (e.g., in vitro methods) | +1.5% | Global | 2025-2033 (Medium-to-Long term) |

| Growing Demand for Sterile Products | +1.3% | Global | 2025-2033 (Long-term) |

| Outsourcing of Testing Services | +0.8% | North America, Europe, APAC | 2025-2033 (Medium-term) |

Pyrogen Testing Market Restraints Analysis

Despite robust growth prospects, the pyrogen testing market faces several significant restraints. One primary challenge is the high cost associated with advanced pyrogen testing methodologies, including reagents, instruments, and the need for highly skilled personnel. The initial capital investment for setting up in-house advanced testing laboratories can be substantial, particularly for smaller and medium-sized enterprises. This financial barrier often limits the widespread adoption of newer, more sophisticated methods, particularly in developing regions where budget constraints are more pronounced.

Another major restraint involves the complex and sometimes disparate regulatory approval processes across different countries and regions. While there is a push for harmonization, significant variations still exist in specific test requirements and validation criteria. This can create complexities for global manufacturers who must navigate multiple regulatory landscapes, potentially delaying product approval and increasing compliance costs. The validation and acceptance of alternative non-animal methods also present a hurdle, as these methods require extensive data and regulatory endorsement before they can fully replace traditional tests.

Furthermore, the scarcity of trained professionals capable of performing and interpreting advanced pyrogen tests poses a significant limitation. The highly specialized nature of these assays demands specific expertise in microbiology, immunology, and analytical chemistry. This talent gap can lead to bottlenecks in testing workflows, compromise test accuracy, and increase operational costs due to the need for specialized training or outsourcing. Ethical concerns and the ongoing debate surrounding animal welfare, particularly concerning the Rabbit Pyrogen Test (RPT), while driving innovation, also present a restraint as companies navigate the transition away from animal testing amidst established regulatory frameworks.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Testing Methods | -1.2% | Global, higher impact in developing regions | 2025-2030 (Medium-term) |

| Complex & Varied Regulatory Approval Processes | -0.9% | Global | 2025-2033 (Ongoing) |

| Lack of Skilled Professionals | -0.7% | Global | 2025-2033 (Long-term) |

| Ethical Concerns with Animal Testing | -0.5% | North America, Europe | 2025-2030 (Medium-term) |

Pyrogen Testing Market Opportunities Analysis

The pyrogen testing market is presented with substantial growth opportunities driven by continuous technological innovation and expanding applications. A significant opportunity lies in the ongoing development and broader acceptance of novel in vitro pyrogen testing methods, such as cell-based assays (e.g., MAT) and recombinant proteins (e.g., rFC). These methods offer advantages like higher specificity, sensitivity, reduced batch-to-batch variability, and, critically, eliminate the ethical concerns associated with animal testing. As regulatory bodies increasingly endorse these alternatives, their adoption is expected to accelerate, opening new revenue streams for innovators in this space.

The burgeoning biopharmaceutical industry, particularly in areas like gene therapies, cell therapies, and personalized medicine, represents another colossal opportunity. These advanced therapeutic modalities often involve complex manufacturing processes and unique product characteristics that necessitate highly specialized and sensitive pyrogen detection methods. The growth in contract manufacturing and research organizations (CMOs/CROs) also offers a lucrative avenue, as these entities can invest in sophisticated testing platforms and offer comprehensive services to a wide range of clients, including small biotech startups and large pharmaceutical companies seeking to outsource non-core activities.

Geographical expansion into emerging markets such as Asia Pacific, Latin America, and parts of Africa presents considerable untapped potential. These regions are experiencing rapid growth in their healthcare infrastructure, increasing pharmaceutical manufacturing capabilities, and evolving regulatory frameworks. Companies that strategically establish their presence, offer cost-effective solutions, and adapt to local market needs can capitalize on this growth. Furthermore, the integration of automation, robotics, and digital solutions for data management and analysis in pyrogen testing laboratories offers opportunities to enhance efficiency, reduce costs, and improve data integrity, appealing to a broader range of end-users.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Alternative In Vitro Methods | +2.0% | Global | 2025-2033 (Long-term) |

| Growth of Biologics and Advanced Therapies | +1.7% | Global | 2025-2033 (Long-term) |

| Expansion in Emerging Markets | +1.5% | APAC, Latin America, MEA | 2025-2033 (Medium-to-Long term) |

| Increasing Demand for Outsourced Services | +1.0% | North America, Europe, APAC | 2025-2033 (Medium-term) |

Pyrogen Testing Market Challenges Impact Analysis

The pyrogen testing market faces several critical challenges that can impede its growth and widespread adoption of innovative solutions. One significant challenge is the ongoing need for extensive validation and regulatory acceptance of new, non-animal pyrogen testing methods. Despite their scientific advantages and ethical benefits, gaining full regulatory endorsement from agencies worldwide often involves lengthy and costly processes. This slow acceptance can delay the market penetration of advanced assays and maintain reliance on traditional, sometimes less efficient, methods, especially for legacy products and established markets.

Another major challenge is maintaining the high sensitivity and specificity required for pyrogen detection across a diverse range of pharmaceutical products, including complex biologics, vaccines, and cell therapies. These products can have unique matrices that interfere with standard assays or may contain non-endotoxin pyrogens that are difficult to detect with conventional methods. Developing universal or highly adaptable testing solutions that can accurately identify all types of pyrogens in varied sample types remains a significant technical hurdle, requiring continuous research and development investment.

Furthermore, supply chain complexities and ensuring the availability of high-quality, consistent reagents and specialized equipment pose logistical challenges. The global nature of pharmaceutical manufacturing means that disruptions in the supply chain for critical testing components can impact production schedules and product release. Additionally, the need for highly trained personnel to operate sophisticated instruments and interpret complex assay results adds to operational challenges, particularly in regions with limited skilled labor. Cybersecurity threats and data integrity concerns for digitalized testing platforms also present evolving challenges that require robust solutions to maintain trust and compliance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Acceptance & Validation of New Methods | -1.5% | Global | 2025-2030 (Medium-term) |

| Ensuring Sensitivity & Specificity for Diverse Products | -1.0% | Global | 2025-2033 (Long-term) |

| Supply Chain Vulnerabilities for Reagents/Equipment | -0.8% | Global | 2025-2028 (Short-term) |

| Shortage of Highly Skilled Professionals | -0.6% | Global | 2025-2033 (Long-term) |

Pyrogen Testing Market - Updated Report Scope

This comprehensive report delves into the Pyrogen Testing Market, providing an in-depth analysis of its current landscape, historical performance, and future growth trajectory. It encompasses detailed segmentation by product, test type, application, and end-user, offering granular insights into market dynamics. The report also features a thorough regional analysis, identifying key growth pockets and competitive strategies of prominent industry players. Our updated scope ensures coverage of emerging trends, technological advancements, and the impact of evolving regulatory frameworks, providing a holistic view for stakeholders and decision-makers in the pharmaceutical, biotechnology, and medical device industries.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 480 million |

| Market Forecast in 2033 | USD 897 million |

| Growth Rate | 8.2% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Charles River Laboratories, Lonza Group AG, Merck KGaA, Bio-Rad Laboratories, Inc., Thermo Fisher Scientific Inc., Associates of Cape Cod, Inc. (ACC), Wako Pure Chemical Industries, Ltd. (a FUJIFILM company), Hyglos GmbH (a bioMérieux company), Genscript Biotech Corporation, Eurofins Scientific SE, Sanquin, Cytiva (part of Danaher Corporation), Sartorius AG, STERIS AST, Endosafe (part of Charles River Laboratories), Lonza Bioscience, bioMérieux S.A., Sino Biological Inc., Accugen Laboratories, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The pyrogen testing market is extensively segmented to provide granular insights into its diverse components and drivers. These segmentations are critical for understanding market dynamics, identifying high-growth areas, and strategizing effectively across various product types, test methodologies, application areas, and end-user categories. Each segment reflects specific trends and demands, offering a comprehensive view of the market landscape and its evolving requirements for safety and quality assurance in sensitive products.

The categorization by product type differentiates between the consumables (reagents and kits), the machinery (instruments), and the outsourced support services, each catering to different operational needs within a testing workflow. Test type segmentation highlights the shift from traditional, animal-based methods to innovative, in vitro alternatives, reflecting regulatory and ethical pressures. Application-based segmentation provides insights into the primary industries driving demand for pyrogen testing, such as pharmaceuticals, medical devices, and even food and cosmetics, underscoring the broad applicability of these safety assessments. Lastly, end-user segmentation distinguishes between in-house testing capabilities of large companies and the growing reliance on specialized third-party providers, illustrating the evolving service landscape in the market.

- By Product Type:

- Reagents and Kits

- Instruments

- Services

- By Test Type:

- Limulus Amebocyte Lysate (LAL) Test

- Chromogenic LAL Test

- Turbidimetric LAL Test

- Gel Clot LAL Test

- Monocyte Activation Test (MAT)

- Rabbit Pyrogen Test (RPT)

- Recombinant Factor C (rFC) Assay

- Others

- Limulus Amebocyte Lysate (LAL) Test

- By Application:

- Pharmaceutical and Biotechnology

- Medical Devices

- Food and Beverage

- Cosmetics

- Others

- By End User:

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic and Research Institutes

- Medical Device Companies

Regional Highlights

- North America: This region is expected to maintain its dominant position in the pyrogen testing market, primarily due to the presence of a well-established pharmaceutical and biotechnology industry, coupled with stringent regulatory frameworks from bodies like the FDA. High R&D investments, advanced healthcare infrastructure, and early adoption of innovative testing technologies further contribute to its leading share.

- Europe: Europe is a significant market, driven by robust pharmaceutical manufacturing, a strong focus on biopharmaceutical research, and increasing adoption of alternative pyrogen testing methods owing to strict animal welfare regulations. Countries like Germany, France, and the UK are key contributors to market growth, emphasizing advanced analytical techniques and regulatory compliance.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate during the forecast period. This growth is attributable to the rapidly expanding pharmaceutical and biotechnology sectors, increasing healthcare expenditure, a growing number of contract manufacturing organizations (CMOs), and rising awareness regarding drug safety and quality. Emerging economies such as China, India, and Japan are at the forefront of this regional expansion.

- Latin America: This region is experiencing steady growth in the pyrogen testing market, fueled by improving healthcare infrastructure, increasing foreign direct investment in the pharmaceutical sector, and growing demand for quality drugs and medical devices. Brazil and Mexico are leading countries in terms of market development and adoption of modern testing methods.

- Middle East and Africa (MEA): The MEA region is expected to show gradual growth, driven by increasing government initiatives to develop the healthcare sector, rising incidence of infectious and chronic diseases, and a growing focus on pharmaceutical production. Investments in healthcare infrastructure and adoption of international quality standards are key drivers in this emerging market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pyrogen Testing Market.- Charles River Laboratories

- Lonza Group AG

- Merck KGaA

- Bio-Rad Laboratories, Inc.

- Thermo Fisher Scientific Inc.

- Associates of Cape Cod, Inc. (ACC)

- Wako Pure Chemical Industries, Ltd. (a FUJIFILM company)

- Hyglos GmbH (a bioMérieux company)

- Genscript Biotech Corporation

- Eurofins Scientific SE

- Sanquin

- Cytiva (part of Danaher Corporation)

- Sartorius AG

- STERIS AST

- Endosafe (part of Charles River Laboratories)

- Lonza Bioscience

- bioMérieux S.A.

- Sino Biological Inc.

- Accugen Laboratories, Inc.

Frequently Asked Questions

Analyze common user questions about the Pyrogen Testing market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is pyrogen testing and why is it important?

Pyrogen testing is a critical quality control procedure used to detect the presence of fever-inducing substances (pyrogens) in injectable drugs, medical devices, and other sterile products. It is vital to ensure patient safety, as pyrogens can cause adverse reactions, including fever, inflammation, and potentially life-threatening conditions, upon administration. Compliance with pyrogen testing regulations is mandatory for product release in the pharmaceutical and medical device industries.

What are the primary types of pyrogen tests used today?

The primary types include the Limulus Amebocyte Lysate (LAL) test, which detects bacterial endotoxins; the Rabbit Pyrogen Test (RPT), an in vivo animal-based test; and emerging in vitro methods like the Monocyte Activation Test (MAT) and Recombinant Factor C (rFC) assay. LAL is widely used for endotoxin detection, while MAT and rFC offer alternatives to animal testing and can detect both endotoxin and non-endotoxin pyrogens.

How are new, non-animal pyrogen testing methods impacting the market?

New non-animal methods such as MAT and rFC are significantly impacting the market by offering more ethical, sensitive, and high-throughput alternatives to traditional animal testing. They are gaining increasing regulatory acceptance due to their ability to reduce animal use, provide faster results, and often offer broader pyrogen detection capabilities. This shift is driving innovation and adoption of advanced instrumentation and reagents in the market.

What role do regulatory bodies play in the pyrogen testing market?

Regulatory bodies, such as the FDA, EMA, and various national pharmacopoeias, play a crucial role by setting stringent guidelines and standards for pyrogen testing of pharmaceutical products and medical devices. They mandate the types of tests required, their validation, and the acceptable limits for pyrogen contamination. Their continuous updates and approval of new methodologies directly influence market trends and adoption rates of pyrogen testing technologies.

Which regions are leading the pyrogen testing market, and why?

North America and Europe currently lead the pyrogen testing market due to their well-established pharmaceutical and biotechnology industries, robust R&D investments, and strict regulatory enforcement. These regions have a high demand for advanced testing solutions and a strong focus on patient safety and quality control. The Asia Pacific region is projected for rapid growth driven by expanding healthcare infrastructure and increasing pharmaceutical manufacturing activities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted