Ductile Cast Iron Market

Ductile Cast Iron Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700584 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

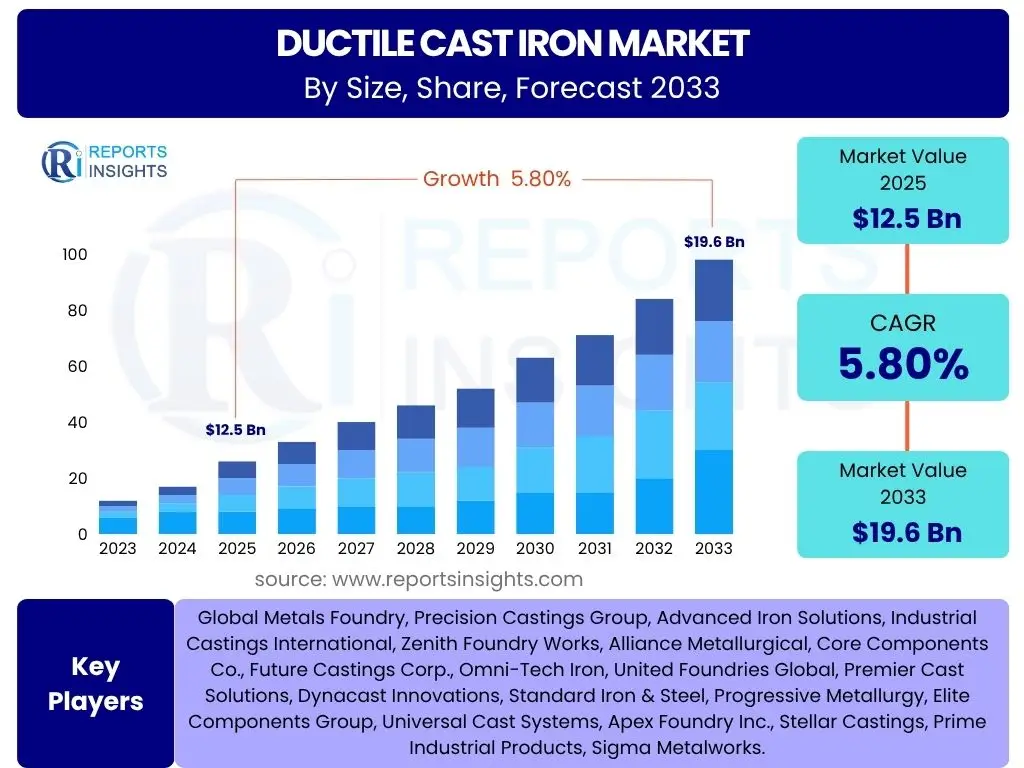

Ductile Cast Iron Market Size

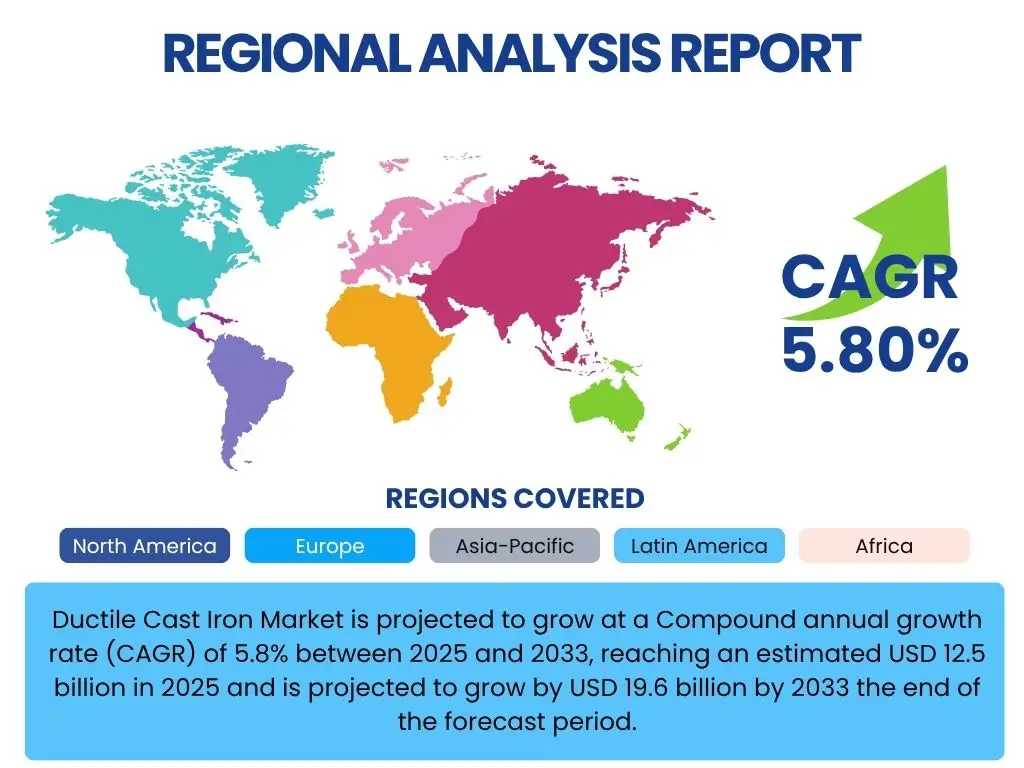

Ductile Cast Iron Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 12.5 billion in 2025 and is projected to grow by USD 19.6 billion by 2033 the end of the forecast period.

Key Ductile Cast Iron Market Trends & Insights

The ductile cast iron market is experiencing dynamic shifts driven by global economic developments, technological advancements in material science, and evolving industrial demands. Key trends include a growing emphasis on sustainable manufacturing practices, the adoption of advanced casting techniques for improved material properties, and increasing integration of digital technologies across the value chain. Furthermore, the market is witnessing a surge in demand from critical infrastructure projects and the automotive sector, alongside a strategic focus on expanding applications in renewable energy and specialized industrial machinery.

- Increasing adoption of high-strength and lightweight ductile iron grades.

- Technological advancements in casting processes enhancing material performance.

- Growing focus on circular economy principles and recycling of cast iron.

- Expansion of ductile iron pipe networks for water and wastewater infrastructure globally.

- Rising demand from the electric vehicle (EV) sector for specific components.

- Integration of smart manufacturing and automation in foundries.

- Shifting manufacturing hubs influencing regional demand patterns.

AI Impact Analysis on Ductile Cast Iron

Artificial Intelligence (AI) is progressively transforming the ductile cast iron market by optimizing production processes, enhancing material quality, and streamlining supply chain operations. AI-driven solutions are being deployed for predictive maintenance of foundry equipment, real-time quality control through sensor data analysis, and intelligent inventory management. This integration leads to significant reductions in operational costs, minimization of defects, and improvements in overall production efficiency, positioning AI as a crucial enabler for future growth and competitiveness in the industry.

- AI-powered predictive maintenance reduces equipment downtime in foundries.

- Machine learning algorithms optimize melting processes and material composition.

- Computer vision systems enhance quality control for defect detection.

- AI-driven supply chain optimization improves raw material procurement and logistics.

- Data analytics provide insights for market forecasting and demand prediction.

- Automated robotics guided by AI enhances precision in casting operations.

- Digital twins facilitate process simulation and new product development.

Key Takeaways Ductile Cast Iron Market Size & Forecast

- The global ductile cast iron market is poised for robust growth, projected at a CAGR of 5.8% from 2025 to 2033.

- Market valuation is expected to increase from USD 12.5 billion in 2025 to USD 19.6 billion by 2033.

- Infrastructure development, particularly in water and wastewater management, remains a primary growth driver.

- The automotive sector's demand, including the burgeoning EV segment, contributes significantly to market expansion.

- Technological innovations in casting and material science are enhancing ductile iron's properties and applications.

- Asia Pacific is anticipated to maintain its dominance due to rapid industrialization and urbanization.

- Sustainability initiatives and the adoption of advanced manufacturing techniques are shaping future market dynamics.

Ductile Cast Iron Market Drivers Analysis

The ductile cast iron market is fundamentally driven by robust demand from key industrial sectors worldwide, propelled by ongoing global infrastructure development and the increasing need for durable and cost-effective material solutions. The material's inherent strength, corrosion resistance, and versatility make it indispensable across diverse applications, from critical urban utilities to advanced manufacturing components. These drivers collectively contribute to the sustained expansion and innovation within the ductile cast iron industry, fostering both regional and global market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Urbanization and Infrastructure Development: Rapid urbanization, particularly in developing economies, necessitates massive investments in public infrastructure projects such as water supply and sewerage systems, road networks, and building construction. Ductile iron pipes are preferred for water and wastewater transportation due to their superior strength, durability, and corrosion resistance, ensuring long-term performance and minimal maintenance. Similarly, ductile iron components are crucial in structural applications and machinery utilized in construction. The continuous global push for modernizing and expanding urban centers directly fuels the demand for ductile cast iron products. | +1.5% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Growing Demand from Water and Wastewater Management: With increasing global population and industrial activities, the need for efficient and reliable water and wastewater management infrastructure is paramount. Ductile cast iron pipes are the material of choice for these critical applications due to their exceptional pressure bearing capacity, impact resistance, and longevity. Governments and municipalities worldwide are investing heavily in upgrading aging water systems and establishing new ones to ensure safe water supply and effective waste disposal, creating a sustained and significant demand for ductile iron pipes and fittings. | +1.2% | Global, particularly developing nations and aging infrastructure regions (North America, Europe) | Long-term (2025-2033) |

| Expansion of Automotive and Transportation Sector: The automotive industry relies heavily on ductile cast iron for various critical components such as engine blocks, crankshafts, brake parts, and suspension components due to its excellent strength-to-weight ratio, castability, and vibration damping properties. The global growth in vehicle production, including both internal combustion engine (ICE) vehicles and the burgeoning electric vehicle (EV) segment, continues to drive demand. As vehicle manufacturers increasingly focus on lightweighting for fuel efficiency and emissions reduction, advanced grades of ductile iron offer a compelling solution without compromising structural integrity or safety. | +0.9% | Asia Pacific (China, India, Japan), Europe (Germany, France), North America (USA, Mexico) | Medium-term (2025-2030) |

| Industrialization and Manufacturing Growth: As industrialization progresses across various regions, particularly in emerging economies, there is a corresponding rise in demand for industrial machinery, equipment, and components. Ductile cast iron is widely used in pumps, valves, compressors, agricultural machinery, and various heavy equipment due to its robustness, wear resistance, and ability to withstand high pressures and temperatures. The expansion of manufacturing bases and capital investments in new industrial facilities directly translate into increased consumption of ductile iron products, supporting diverse industrial applications. | +0.7% | Asia Pacific, Eastern Europe, Latin America | Long-term (2025-2033) |

| Energy Sector Expansion (Oil & Gas, Power Generation): The energy sector, encompassing both conventional oil and gas and renewable energy infrastructure, relies on ductile cast iron for various components. In oil and gas, it's used for pipelines, valves, and pump housings due to its ability to handle high pressures and corrosive environments. In power generation, including wind turbines, ductile iron components like hubs and frames are critical for structural integrity and durability. Global investments in new energy projects, particularly the rapid growth of wind energy and the ongoing exploration and production activities in oil and gas, consistently contribute to the demand for high-performance ductile iron castings. | +0.5% | Middle East, North America, Europe, China (for renewables) | Medium-to-Long-term (2025-2033) |

Ductile Cast Iron Market Restraints Analysis

While the ductile cast iron market exhibits significant growth potential, it is also subject to several restraining factors that can impede its expansion and profitability. These restraints primarily stem from the inherent characteristics of metal production, external economic pressures, and the evolving competitive landscape. Addressing these challenges requires strategic adaptation, technological innovation, and careful management of external market dynamics to maintain growth trajectories.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Iron Ore, Scrap, Magnesium): The production of ductile cast iron is heavily dependent on raw materials such as iron ore, ferrous scrap, and magnesium, among other alloying elements. The prices of these commodities are highly susceptible to global supply-demand dynamics, geopolitical events, and currency fluctuations. Sudden and significant increases in raw material costs can directly impact the production expenses for ductile iron manufacturers, leading to reduced profit margins or necessitate price increases for end-products, which can make ductile iron less competitive compared to alternative materials. This price volatility creates uncertainty and complicates long-term planning for manufacturers. | -0.8% | Global | Short-to-Medium-term (2025-2028) |

| Stringent Environmental Regulations and Production Costs: The manufacturing of cast iron involves high energy consumption and the potential generation of emissions and waste. Governments worldwide are increasingly implementing stringent environmental regulations regarding air quality, water discharge, and waste management in industrial processes. Compliance with these regulations often requires significant capital investments in pollution control technologies, energy-efficient equipment, and waste treatment facilities. These compliance costs add to the overall production expense for ductile iron foundries, potentially reducing their competitiveness and impacting market growth, especially for smaller players struggling with capital expenditure. | -0.6% | Europe, North America, China (developed regions) | Long-term (2025-2033) |

| Competition from Alternative Materials (Plastics, Steel, Composites): Ductile cast iron faces significant competition from a range of alternative materials, each offering specific advantages for certain applications. For instance, PVC and HDPE pipes are increasingly used in water and wastewater infrastructure due to their lighter weight, ease of installation, and perceived lower cost, challenging ductile iron's dominance. In the automotive and construction sectors, advanced steels, aluminum alloys, and composite materials provide lightweight and high-strength solutions. While ductile iron offers a unique combination of properties, the continuous development and marketing of these alternative materials can limit ductile iron's market share and application scope. | -0.7% | Global (application-specific) | Medium-to-Long-term (2025-2033) |

| Economic Slowdowns and Geopolitical Instability: The ductile cast iron market is highly sensitive to global economic conditions and geopolitical stability. Economic downturns or recessions can lead to reduced investments in infrastructure projects, a decline in automotive production, and a general slowdown in industrial activity, directly impacting the demand for ductile iron. Geopolitical tensions, trade disputes, and supply chain disruptions can further exacerbate these effects by hindering raw material supply, increasing logistics costs, and creating market uncertainty. Such external macroeconomic factors can significantly restrain market growth and profitability. | -0.5% | Global (interconnected economies) | Short-term (2025-2027) |

Ductile Cast Iron Market Opportunities Analysis

Despite existing challenges, the ductile cast iron market is ripe with opportunities for growth and innovation, driven by emerging technological advancements, shifting global economic landscapes, and a growing emphasis on sustainable practices. These opportunities enable manufacturers to diversify their product offerings, penetrate new markets, and enhance the overall value proposition of ductile cast iron, ensuring its continued relevance and expansion in the industrial materials sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Casting Technologies and Material Properties: Continuous research and development in casting techniques, such as advanced mold technologies, process automation, and precise metallurgical control, are enabling the production of ductile iron with enhanced mechanical properties and reduced defects. Innovations like thin-wall casting, compacted graphite iron (CGI), and austempered ductile iron (ADI) offer superior strength, ductility, and wear resistance, expanding ductile iron's application scope into more demanding sectors like high-performance automotive parts and specialized industrial machinery. These advancements create new market niches and reinforce ductile iron's competitive edge against alternative materials. | +1.0% | Global (focus on R&D hubs: Europe, North America, Japan) | Long-term (2025-2033) |

| Rising Demand in Emerging Economies: Countries in Asia Pacific, Latin America, and Africa are experiencing rapid economic growth, industrialization, and infrastructure development. This surge in development translates into a significant increase in demand for basic industrial materials, including ductile cast iron for construction, water infrastructure, automotive manufacturing, and general industrial applications. These regions offer vast untapped markets with considerable potential for new investments and expanded sales for ductile iron manufacturers, driven by population growth and modernization efforts. | +1.3% | Asia Pacific (India, Southeast Asia), Latin America, Africa | Long-term (2025-2033) |

| Focus on Sustainable and Recyclable Materials: With growing global awareness and regulatory pressure towards environmental sustainability, there is an increasing preference for materials that are recyclable and have a lower carbon footprint. Ductile cast iron is highly recyclable, and its production often utilizes a significant proportion of recycled scrap metal, reducing reliance on virgin materials and lowering energy consumption compared to some alternatives. This inherent sustainability characteristic presents a significant opportunity for ductile iron to gain preference in green building initiatives, sustainable infrastructure projects, and environmentally conscious manufacturing, aligning with global ESG (Environmental, Social, and Governance) goals. | +0.8% | Europe, North America, Japan (regions with strong sustainability focus) | Medium-to-Long-term (2025-2033) |

| Development of Lightweight and High-Strength Grades: The continuous push across industries, particularly automotive and aerospace, for lightweighting to improve fuel efficiency and performance, presents a strong opportunity for ductile iron. Innovations in metallurgy and casting processes are leading to the development of new ductile iron grades that offer superior strength-to-weight ratios. These advanced grades can replace heavier traditional materials or less durable alternatives, allowing for component downsizing without compromising structural integrity. This trend opens new design possibilities and expands ductile iron’s addressable market in applications where weight reduction is a critical design parameter. | +0.6% | Global (focused on automotive, machinery, aerospace R&D) | Medium-term (2025-2030) |

Ductile Cast Iron Market Challenges Impact Analysis

The ductile cast iron market faces a range of challenges that can hinder its growth and operational efficiency. These challenges span from complex supply chain dynamics and intense market competition to the availability of skilled labor and high operational costs. Successfully navigating these hurdles requires robust strategic planning, continuous technological investment, and adaptive business models to ensure market resilience and sustained profitability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Logistics Complexities: The ductile cast iron industry relies on a global supply chain for raw materials such as iron ore, ferrous scrap, and various alloying elements, as well as for the distribution of finished products. Geopolitical events, natural disasters, pandemics, and trade policy changes can lead to significant disruptions in this supply chain, causing material shortages, price spikes, and delays in delivery. Managing complex logistics across different regions and ensuring the timely availability of materials and dispatch of products adds considerable operational complexity and cost, potentially impacting production schedules and profitability. | -0.7% | Global, particularly regions with less diversified supply sources | Short-to-Medium-term (2025-2028) |

| Intense Competition and Price Pressures: The ductile cast iron market is characterized by a significant number of domestic and international players, leading to intense competition. This competitive landscape often results in considerable price pressures, forcing manufacturers to operate on thin margins. The need to balance competitive pricing with rising raw material costs, labor expenses, and environmental compliance costs poses a significant challenge. Furthermore, the availability of alternative materials like plastics, steel, and composites adds to the competitive intensity, demanding continuous innovation and efficiency improvements from ductile iron producers. | -0.5% | Global, particularly mature markets (Europe, North America) | Long-term (2025-2033) |

| Skilled Labor Shortages and Workforce Training Needs: The ductile cast iron industry, particularly foundries, requires a specialized workforce with expertise in metallurgy, casting processes, quality control, and advanced machinery operation. There is a growing concern about the shortage of skilled labor, as younger generations may not be attracted to traditional manufacturing roles. Additionally, rapid technological advancements in foundry operations necessitate continuous training and upskilling of the existing workforce. The inability to attract and retain skilled personnel can lead to production inefficiencies, quality issues, and increased labor costs, posing a significant operational challenge for manufacturers. | -0.4% | Developed economies (Europe, North America, Japan) | Long-term (2025-2033) |

| High Energy Consumption in Manufacturing: The production of ductile cast iron, especially the melting and heat treatment processes in foundries, is highly energy-intensive. Fluctuations in energy prices, driven by global supply dynamics, geopolitical events, and environmental policies, directly impact the operational costs of manufacturers. High energy consumption also contributes to the industry's carbon footprint, drawing increased scrutiny from environmental regulators and sustainability advocates. Companies face the challenge of investing in energy-efficient technologies and exploring renewable energy sources to mitigate these costs and meet evolving environmental targets, which often requires substantial upfront capital. | -0.6% | Global (affected by energy market volatility) | Medium-to-Long-term (2025-2033) |

Ductile Cast Iron Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global ductile cast iron market, offering critical insights into its current status, historical performance, and future growth trajectory. The scope covers detailed market segmentation, competitive landscape assessment, regional dynamics, and the impact of key market influencers such as drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 19.6 Billion |

| Growth Rate | 5.8% CAGR from 2025 to 2033 |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Metals Foundry, Precision Castings Group, Advanced Iron Solutions, Industrial Castings International, Zenith Foundry Works, Alliance Metallurgical, Core Components Co., Future Castings Corp., Omni-Tech Iron, United Foundries Global, Premier Cast Solutions, Dynacast Innovations, Standard Iron & Steel, Progressive Metallurgy, Elite Components Group, Universal Cast Systems, Apex Foundry Inc., Stellar Castings, Prime Industrial Products, Sigma Metalworks. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global ductile cast iron market is comprehensively segmented to provide a detailed understanding of its diverse applications, end-use industries, and material grades. This granular segmentation allows for precise market sizing, trend identification, and strategic planning, catering to the varied needs of stakeholders across the value chain. Each segment represents distinct market dynamics and growth opportunities within the broader ductile cast iron landscape.

- By Application: This segment analyzes the various uses of ductile cast iron across different sectors.

- Pipes & Fittings: Primarily used for water supply and sewerage systems due to their durability, high pressure resistance, and corrosion properties. These are essential for urban and rural infrastructure development.

- Automotive Components: Includes critical parts like engine blocks, crankshafts, camshafts, brake calipers, and suspension components, valued for their strength, vibration damping, and castability.

- Industrial Machinery: Covers components for pumps, valves, compressors, agricultural machinery, and heavy equipment, where robust and wear-resistant materials are essential.

- Wind Power: Encompasses large structural components such as turbine hubs, main frames, and gearbox housings, requiring high strength and fatigue resistance.

- Other: Includes miscellaneous applications in construction equipment (e.g., counterweights), railway components, and various other general industrial uses.

- By End-Use Industry: This segment categorizes the market based on the major industries consuming ductile cast iron products.

- Construction: Encompasses residential, commercial, and infrastructure construction, primarily for pipes, fittings, and structural components.

- Automotive & Transportation: Includes passenger vehicles, commercial vehicles, and railway systems utilizing ductile iron for powertrain, chassis, and brake systems.

- Water & Wastewater Management: Dedicated to the infrastructure for water distribution, sewage collection, and treatment plants.

- Energy & Power: Covers conventional power generation, oil & gas, and renewable energy sectors like wind and solar.

- Manufacturing & General Industrial: Broad category including general manufacturing, foundries, and various industrial equipment production.

- By Grade: This segment differentiates ductile cast iron based on its metallurgical composition and resulting mechanical properties.

- Ferritic Ductile Iron: Known for its excellent ductility and toughness, often used for components requiring good machinability and impact resistance.

- Pearlitic Ductile Iron: Offers higher strength and hardness than ferritic grades, suitable for applications requiring wear resistance and higher tensile strength.

- Austenitic Ductile Iron: Contains nickel to enhance corrosion resistance and non-magnetic properties, ideal for specialized chemical and low-temperature applications.

- Austempered Ductile Iron (ADI): A heat-treated ductile iron with superior strength, toughness, and wear resistance, often used in gears, crankshafts, and heavy-duty components.

- Silicon-Molybdenum Ductile Iron: A specialized grade offering improved high-temperature strength and oxidation resistance, suitable for exhaust manifolds and turbocharger components.

- By Region: This segment provides a geographical breakdown of the market, identifying key regional demand and supply dynamics.

- North America: Covers the United States, Canada, and Mexico.

- Europe: Includes Germany, France, United Kingdom, Italy, Spain, and Rest of Europe.

- Asia Pacific (APAC): Encompasses China, India, Japan, South Korea, Southeast Asia, and Rest of APAC.

- Latin America: Includes Brazil, Argentina, and Rest of Latin America.

- Middle East, and Africa (MEA): Comprises UAE, Saudi Arabia, South Africa, and Rest of MEA.

Regional Highlights

The global ductile cast iron market exhibits distinct regional dynamics, driven by varying levels of industrialization, infrastructure investments, and regulatory environments. Understanding these regional highlights is crucial for market participants to tailor their strategies and capitalize on localized growth opportunities, leveraging specific economic and industrial trends.

- Asia Pacific (APAC) Dominance: Asia Pacific is projected to be the largest and fastest-growing market for ductile cast iron. This dominance is primarily attributed to rapid urbanization, extensive infrastructure development projects in countries like China and India, and the flourishing automotive and manufacturing sectors across the region. Significant investments in water and wastewater management systems, coupled with increasing industrial production, particularly in Southeast Asian nations, fuel the demand. The region also benefits from a robust base of ductile iron foundries and manufacturing capabilities.

- Europe's Steady Growth: Europe represents a mature but stable market for ductile cast iron. The demand is primarily driven by the ongoing replacement and upgrading of aging water infrastructure, stringent environmental regulations promoting durable and sustainable materials, and a strong automotive industry, particularly in Germany and France. The region also focuses on advanced manufacturing techniques and developing high-performance ductile iron grades, contributing to sustained, albeit moderate, growth.

- North America's Resilient Market: North America demonstrates a resilient market for ductile cast iron, supported by substantial investments in public works and utility infrastructure, particularly in the United States and Canada. The automotive sector, including the increasing production of light trucks and SUVs, continues to be a significant consumer. While infrastructure needs are critical, the market also faces challenges from competition by alternative materials and high labor costs, prompting a focus on efficiency and advanced products.

- Latin America's Emerging Potential: Latin America is an emerging market with significant growth potential, driven by urbanization and infrastructure development in countries like Brazil and Mexico. The expansion of water and sanitation services and a growing automotive manufacturing base contribute to the demand for ductile cast iron. Economic stability and foreign investments will be key factors influencing the pace of market expansion in this region.

- Middle East and Africa (MEA) Expansion: The MEA region is witnessing growth in ductile cast iron demand, largely due to ongoing large-scale construction projects, investments in oil and gas infrastructure, and initiatives to improve water supply and sanitation. Countries in the Gulf Cooperation Council (GCC) are particularly active in infrastructure development. While still smaller than other regions, the long-term growth prospects are positive, contingent on continued economic diversification and infrastructure spending.

Top Key Players:

The market research report covers the analysis of key stake holders of the Ductile Cast Iron Market. Some of the leading players profiled in the report include -- Global Metals Foundry

- Precision Castings Group

- Advanced Iron Solutions

- Industrial Castings International

- Zenith Foundry Works

- Alliance Metallurgical

- Core Components Co.

- Future Castings Corp.

- Omni-Tech Iron

- United Foundries Global

- Premier Cast Solutions

- Dynacast Innovations

- Standard Iron & Steel

- Progressive Metallurgy

- Elite Components Group

- Universal Cast Systems

- Apex Foundry Inc.

- Stellar Castings

- Prime Industrial Products

- Sigma Metalworks

Frequently Asked Questions:

What is Ductile Cast Iron?

Ductile cast iron, also known as nodular cast iron or spheroidal graphite cast iron, is a type of cast iron alloy distinguished by its graphite inclusions being spheroidal or nodular in shape, rather than the flake-like form found in gray cast iron. This unique microstructure, achieved by adding a small amount of magnesium or cerium to the molten iron, gives ductile iron significantly enhanced ductility, strength, and impact resistance compared to other cast irons. It combines the advantages of cast iron (excellent castability, machinability, and vibration damping) with properties closer to steel (high strength and toughness), making it a versatile material for a wide range of engineering applications.

What are the primary applications of Ductile Cast Iron?

Ductile cast iron is widely used across various industries due to its robust mechanical properties. Its primary applications include water and wastewater pipes and fittings, which benefit from its high strength and corrosion resistance for long-term infrastructure. In the automotive sector, it's utilized for critical components like engine blocks, crankshafts, and brake parts. Other significant applications involve industrial machinery components such as pumps, valves, and compressors, as well as structural parts in wind turbines and various construction equipment, highlighting its versatility and reliability in demanding environments.

What is the projected growth rate (CAGR) of the Ductile Cast Iron Market?

The Ductile Cast Iron Market is projected to exhibit a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. This consistent growth indicates a stable expansion trajectory, driven by ongoing demand from key end-use industries such as infrastructure, automotive, and industrial machinery, alongside technological advancements in material properties and manufacturing processes. This growth rate underscores the material's sustained relevance and increasing adoption in diverse global markets over the forecast period.

What factors are driving the demand for Ductile Cast Iron?

The demand for ductile cast iron is primarily driven by several key factors. Global urbanization and extensive infrastructure development, particularly in emerging economies, fuel the need for durable water and wastewater management systems where ductile iron pipes are preferred. The continuous expansion of the automotive sector, including advancements in electric vehicles requiring high-strength and lightweight components, also contributes significantly. Furthermore, sustained growth in industrialization, manufacturing, and the energy sector (oil & gas, renewables) worldwide necessitates robust and reliable materials, further propelling the market for ductile cast iron.

What are the emerging trends in the Ductile Cast Iron Market?

Emerging trends in the Ductile Cast Iron Market include a strong emphasis on sustainability and the circular economy, leading to increased recycling efforts and adoption of eco-friendlier production methods. There's a growing focus on developing advanced grades with enhanced properties like higher strength-to-weight ratios and improved wear resistance to meet evolving industry demands. The integration of digital technologies, such as Artificial Intelligence (AI) and automation, is also becoming prevalent in foundry operations, optimizing production efficiency and quality control. Lastly, geographical shifts in manufacturing and demand, especially towards Asia Pacific, continue to shape market dynamics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted