Iron and Steel Casting Market

Iron and Steel Casting Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703632 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

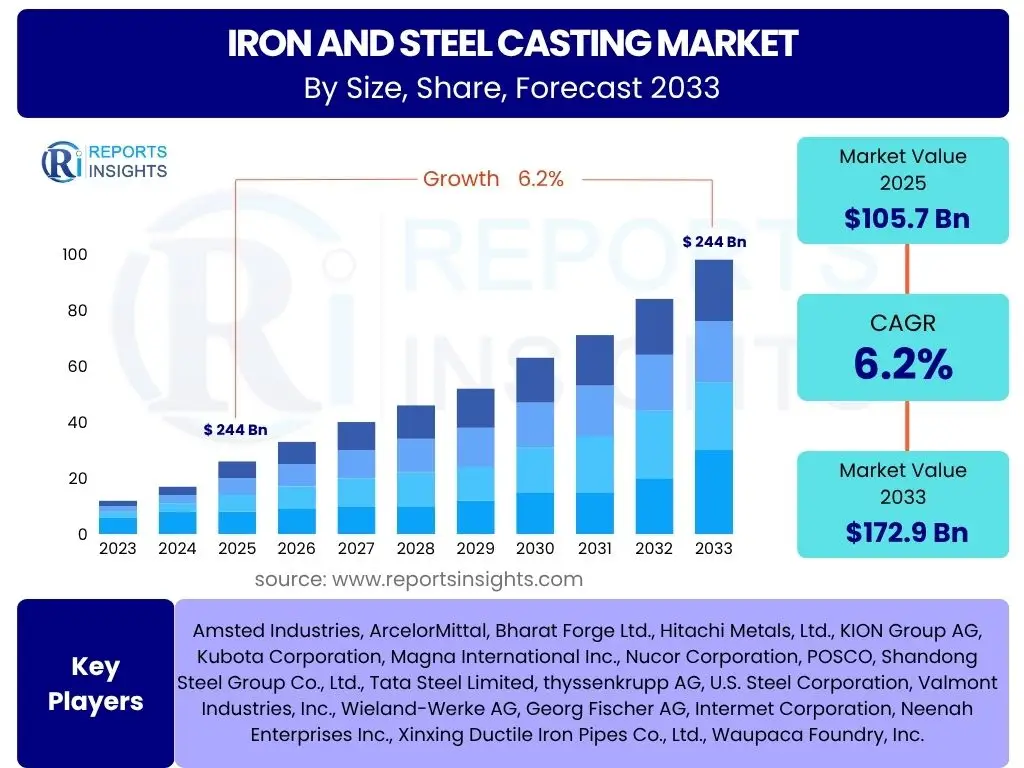

Iron and Steel Casting Market Size

According to Reports Insights Consulting Pvt Ltd, The Iron and Steel Casting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 105.7 Billion in 2025 and is projected to reach USD 172.9 Billion by the end of the forecast period in 2033.

Key Iron and Steel Casting Market Trends & Insights

The iron and steel casting market is undergoing significant transformation driven by evolving industrial demands, technological advancements, and increasing emphasis on sustainability. Users frequently inquire about the shift towards lightweight materials, the adoption of advanced manufacturing processes, and the impact of automation on production efficiency. There is also considerable interest in how global supply chain dynamics and the push for higher quality standards are influencing market trends. The industry is witnessing a strategic pivot towards specialized castings that offer superior performance characteristics and meet stringent environmental regulations across various end-use sectors.

Key insights reveal a growing demand for high-strength, low-weight castings, particularly from the automotive and aerospace industries seeking to improve fuel efficiency and reduce emissions. Furthermore, the integration of digital technologies, such as IoT and real-time monitoring, is optimizing casting processes, leading to reduced defects and enhanced productivity. The market is also experiencing a surge in demand for custom casting solutions, as industries require components tailored to unique specifications, driving innovation in design and material science. This adaptability is crucial for meeting the diverse and complex needs of modern manufacturing.

- Adoption of advanced casting technologies like 3D printing for rapid prototyping and complex geometries.

- Increasing demand for lightweight and high-strength castings in automotive and aerospace sectors.

- Integration of automation and robotics for enhanced precision and operational efficiency.

- Growing focus on sustainable production practices, including recycling and energy efficiency.

- Shift towards specialized and customized casting solutions for niche industrial applications.

AI Impact Analysis on Iron and Steel Casting

User inquiries concerning the impact of Artificial Intelligence (AI) on the iron and steel casting industry primarily revolve around its potential to revolutionize operational efficiency, quality control, and predictive maintenance. Stakeholders are keen to understand how AI can optimize complex casting processes, reduce material waste, and enhance safety standards. Specific concerns often include the initial investment required for AI integration, the need for skilled personnel to manage these systems, and the implications for job roles within foundries. There is a general expectation that AI will lead to more intelligent manufacturing environments, capable of self-optimization and proactive issue resolution.

The analysis indicates that AI's influence extends across multiple facets of casting operations, from raw material inspection to final product quality assessment. AI-driven models can predict potential defects based on real-time process parameters, allowing for immediate adjustments and significantly reducing scrap rates. Furthermore, AI algorithms can optimize energy consumption by controlling furnace temperatures and machinery operation, contributing to both cost savings and environmental sustainability. The adoption of AI is also fostering a data-driven culture, enabling better decision-making processes and paving the way for fully autonomous casting facilities in the long term. This transformative potential positions AI as a critical enabler for future industry growth and competitiveness.

- Enhanced quality control through AI-driven defect detection and prediction.

- Optimization of casting parameters for improved material utilization and energy efficiency.

- Implementation of predictive maintenance for machinery, reducing downtime and operational costs.

- AI-assisted design and simulation for novel casting geometries and material compositions.

- Automation of repetitive tasks, improving workplace safety and enabling more complex human roles.

Key Takeaways Iron and Steel Casting Market Size & Forecast

Common user questions regarding key takeaways from the iron and steel casting market size and forecast consistently highlight the drivers of growth, potential barriers, and the regions poised for significant expansion. Users seek clarity on how macroeconomic factors, technological advancements, and shifting industrial demands will shape the market's trajectory over the next decade. There is particular interest in understanding the long-term viability of traditional casting methods versus emerging technologies and the strategic implications for industry participants.

The primary insights underscore a robust growth outlook for the iron and steel casting market, primarily propelled by continued demand from the automotive, construction, and industrial machinery sectors. Despite challenges such as raw material price volatility and stringent environmental regulations, technological innovation, particularly in automation and material science, is expected to mitigate these pressures and unlock new opportunities. The market's future will be characterized by a strong emphasis on efficiency, sustainability, and the production of highly specialized components, driving consolidation and strategic partnerships among key players. This dynamic environment necessitates continuous adaptation and investment in advanced capabilities.

- The market is set for sustained growth, driven by expansion in end-use industries like automotive and construction.

- Technological advancements, including automation and digitalization, are critical for overcoming operational challenges and enhancing competitiveness.

- Sustainability initiatives and the adoption of eco-friendly practices will increasingly influence market dynamics and investment decisions.

- Emerging economies, particularly in Asia Pacific, are anticipated to be significant growth engines due to rapid industrialization and infrastructure development.

- Strategic partnerships and mergers & acquisitions are likely to increase as companies seek to consolidate market share and leverage specialized expertise.

Iron and Steel Casting Market Drivers Analysis

The global iron and steel casting market is significantly driven by robust demand from key end-use industries, particularly the automotive sector. As the automotive industry continues to evolve with a focus on lighter, more efficient, and structurally sound vehicles, the demand for advanced iron and steel castings for engine blocks, chassis components, and transmission parts remains strong. This driver is further amplified by the ongoing shift towards electric vehicles, which, despite differing component needs, still require various high-strength cast parts for structural integrity and battery housing. Manufacturers are continually innovating to provide castings that meet stringent performance and weight specifications for both traditional and electric powertrains.

Infrastructure development and industrial machinery manufacturing also represent substantial drivers for the market. Governments worldwide are investing heavily in infrastructure projects, including roads, bridges, railways, and urban development, all of which require significant quantities of cast iron and steel components for structural elements, pipes, and fittings. Similarly, the continuous need for new and replacement machinery in agriculture, construction, mining, and manufacturing industries fuels the demand for durable and precise cast parts. These sectors rely on castings for their strength, durability, and ability to withstand harsh operating conditions, making them indispensable components in heavy-duty applications. The global urbanization trend and industrial expansion across developing economies further bolster this demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Automotive Sector Growth | +1.8% | Global, particularly Asia Pacific, Europe, North America | Short to Medium-term (2025-2030) |

| Infrastructure Development | +1.5% | Asia Pacific, Middle East & Africa, Latin America | Medium to Long-term (2027-2033) |

| Industrial Machinery Demand | +1.2% | North America, Europe, China, India | Short to Medium-term (2025-2030) |

| Energy Sector Expansion | +0.9% | Global, particularly emerging economies | Medium to Long-term (2027-2033) |

| Technological Advancements in Casting | +0.8% | Global | Ongoing (2025-2033) |

Iron and Steel Casting Market Restraints Analysis

The iron and steel casting market faces significant restraints, primarily stemming from the volatility of raw material prices. The primary inputs, such as scrap steel, pig iron, and various alloying elements, are subject to global supply and demand fluctuations, geopolitical tensions, and trade policies. These price swings directly impact production costs, making it challenging for foundries to maintain consistent profit margins and competitive pricing. The uncertainty in raw material costs also hinders long-term strategic planning and investment in advanced technologies, as companies must prioritize managing immediate operational expenses over future growth initiatives. This volatility is a constant pressure point for the industry, often leading to delayed projects or reduced production volumes.

Environmental regulations and high energy consumption also pose substantial restraints on market growth. Foundries are energy-intensive operations, relying heavily on electricity and natural gas for melting and heat treatment processes. Rising energy costs, coupled with increasingly stringent environmental standards related to emissions, waste disposal, and water usage, necessitate significant investments in pollution control technologies and energy-efficient equipment. These compliance costs can be prohibitive for smaller foundries, leading to consolidation or market exit. Furthermore, the industry faces pressure to adopt more sustainable practices, which often requires a fundamental shift in traditional manufacturing processes, adding complexity and financial burden to operations. The balance between profitability and environmental responsibility remains a critical challenge for the sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -1.5% | Global | Short to Medium-term (2025-2030) |

| Environmental Regulations & Compliance Costs | -1.2% | Europe, North America, Japan, China | Ongoing (2025-2033) |

| High Energy Consumption & Costs | -1.0% | Global | Short to Medium-term (2025-2030) |

| Intense Competition from Alternative Materials | -0.8% | Global | Medium to Long-term (2027-2033) |

| Shortage of Skilled Labor | -0.7% | North America, Europe, Japan | Long-term (2028-2033) |

Iron and Steel Casting Market Opportunities Analysis

Significant opportunities in the iron and steel casting market are emerging from the growing demand for lightweight and advanced alloy castings. Industries such as automotive, aerospace, and defense are continuously seeking ways to reduce the overall weight of components without compromising strength or durability, driven by fuel efficiency standards and performance requirements. This trend opens avenues for foundries to invest in research and development of new high-strength steel alloys, ductile iron variations, and composite castings that offer superior strength-to-weight ratios. The ability to produce complex geometries and thin-walled components using innovative casting techniques further enhances these opportunities, catering to the evolving design needs of modern engineering applications.

Another major opportunity lies in the integration of additive manufacturing and the adoption of Industry 4.0 principles within casting operations. While not a direct replacement for traditional casting, additive manufacturing (3D printing) offers possibilities for rapid prototyping of molds and cores, reducing lead times and facilitating design iterations. Furthermore, the broader implementation of Industry 4.0 technologies, including IoT, AI, and Big Data analytics, can transform traditional foundries into smart factories. This digital transformation enables real-time monitoring of production processes, predictive maintenance of machinery, optimized energy usage, and improved quality control. Such advancements not only enhance operational efficiency and reduce costs but also position foundries to offer more value-added services and faster turnaround times, addressing contemporary industrial demands.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lightweighting and Advanced Alloys | +1.7% | Global, especially North America, Europe, APAC | Medium to Long-term (2027-2033) |

| Additive Manufacturing Integration (for molds/cores) | +1.3% | Global (developed economies) | Medium-term (2026-2031) |

| Recycling and Circular Economy Initiatives | +1.1% | Europe, North America, Japan | Ongoing (2025-2033) |

| Expansion in Emerging Markets | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2028-2033) |

| Digitalization and Industry 4.0 Adoption | +0.8% | Global | Ongoing (2025-2033) |

Iron and Steel Casting Market Challenges Impact Analysis

The iron and steel casting market is confronted by significant challenges, notably global supply chain disruptions. Events such as the COVID-19 pandemic, geopolitical conflicts, and natural disasters have highlighted the fragility of intricate global supply networks. These disruptions can lead to delays in raw material procurement, extended lead times for equipment, and increased transportation costs, directly impacting production schedules and profitability. Foundries often rely on a global network for specialized inputs and machinery, making them vulnerable to localized disruptions that can ripple across the entire production process. Managing these uncertainties requires robust risk mitigation strategies and potentially a shift towards more localized sourcing, which can, in turn, affect cost structures.

Another prominent challenge is the capital-intensive nature of the industry and the continuous need for investment in advanced technology. Setting up and operating a modern foundry requires substantial upfront capital for furnaces, molding equipment, robotic systems, and quality control instruments. Furthermore, to remain competitive and meet evolving industry standards, foundries must continuously invest in upgrading their technology and adopting automation and digitalization. This ongoing need for capital expenditure can be a barrier to entry for new players and a financial strain for existing ones, particularly small and medium-sized enterprises. The high investment threshold, combined with fluctuating market demands, makes long-term financial planning and securing funding a persistent hurdle for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions | -1.3% | Global | Short to Medium-term (2025-2028) |

| Capital Intensive Investment & High Overhead | -1.0% | Global | Long-term (2025-2033) |

| Maintaining Consistent Quality Control & Defects | -0.9% | Global | Ongoing (2025-2033) |

| Sustainability Pressures & Decarbonization | -0.8% | Europe, North America, Japan | Medium to Long-term (2027-2033) |

| Market Fragmentation & Price Competition | -0.7% | Global, particularly Asia Pacific | Ongoing (2025-2033) |

Iron and Steel Casting Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Iron and Steel Casting Market, offering a granular analysis of market size, trends, drivers, restraints, opportunities, and challenges. It provides detailed segmentation analysis across material types, processes, and end-use industries, alongside an in-depth regional assessment. The scope also includes an impact analysis of AI integration and a forecast through 2033, serving as a vital resource for strategic planning and informed decision-making within the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 105.7 Billion |

| Market Forecast in 2033 | USD 172.9 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amsted Industries, ArcelorMittal, Bharat Forge Ltd., Hitachi Metals, Ltd., KION Group AG, Kubota Corporation, Magna International Inc., Nucor Corporation, POSCO, Shandong Steel Group Co., Ltd., Tata Steel Limited, thyssenkrupp AG, U.S. Steel Corporation, Valmont Industries, Inc., Wieland-Werke AG, Georg Fischer AG, Intermet Corporation, Neenah Enterprises Inc., Xinxing Ductile Iron Pipes Co., Ltd., Waupaca Foundry, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The iron and steel casting market is comprehensively segmented based on material type, manufacturing process, and diverse end-use industries. This granular segmentation provides a detailed understanding of market dynamics within each category, highlighting specific growth pockets and evolving demand patterns. Analyzing these segments is crucial for identifying targeted opportunities, assessing competitive landscapes, and developing tailored strategies to meet the specific requirements of various industrial applications globally.

The material type segmentation distinguishes between gray iron, ductile iron, and various steel castings, each offering unique properties suitable for different applications. Process segmentation details common casting methods like sand casting, die casting, and investment casting, reflecting the technological capabilities and production efficiencies of the industry. Furthermore, the end-use industry segmentation provides insights into the primary sectors driving demand, ranging from the automotive and construction industries to industrial machinery, energy, and aerospace, allowing for a precise understanding of market dependencies and growth trajectories in key economic areas.

- By Material Type: Gray Iron Castings, Ductile Iron Castings, Steel Castings (Carbon Steel, Alloy Steel,200/300/400 Series Stainless Steel)

- By Process: Sand Casting, Die Casting, Investment Casting, Shell Mold Casting, Centrifugal Casting, Permanent Mold Casting, Lost Foam Casting, Others

- By End-Use Industry: Automotive (Passenger Vehicles, Commercial Vehicles, Electric Vehicles), Industrial Machinery (Agricultural Machinery, Construction Equipment, Mining Machinery, Textile Machinery), Construction (Structural Components, Pipes & Fittings), Energy (Oil & Gas, Power Generation, Renewable Energy), Railways, Aerospace & Defense, Marine, General Manufacturing, Others

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to rapid industrialization, extensive infrastructure development projects, and a flourishing automotive manufacturing sector, particularly in China and India. The region benefits from abundant raw material availability and lower labor costs, attracting significant investment in new foundry capacities.

- Europe: A mature market characterized by strong innovation in advanced casting technologies and stringent environmental regulations. Demand is driven by the robust automotive, industrial machinery, and renewable energy sectors, with a focus on high-performance and specialized castings. Germany, Italy, and France are key contributors.

- North America: Exhibits steady growth, propelled by the automotive industry's focus on lightweighting, significant investments in infrastructure upgrades, and a growing demand for industrial equipment. The region is also a leader in adopting automation and digital technologies in foundries.

- Middle East and Africa (MEA): Emerging as a growth region, primarily due to expanding oil & gas operations, infrastructure development, and diversification efforts in industrial sectors. Demand for pipes, fittings, and structural components is particularly notable.

- Latin America: Expected to show moderate growth driven by infrastructure projects, growth in the automotive sector (especially in Mexico and Brazil), and the expansion of the mining and agricultural machinery industries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Iron and Steel Casting Market.- Amsted Industries

- ArcelorMittal

- Bharat Forge Ltd.

- Hitachi Metals, Ltd.

- KION Group AG

- Kubota Corporation

- Magna International Inc.

- Nucor Corporation

- POSCO

- Shandong Steel Group Co., Ltd.

- Tata Steel Limited

- thyssenkrupp AG

- U.S. Steel Corporation

- Valmont Industries, Inc.

- Wieland-Werke AG

- Georg Fischer AG

- Intermet Corporation

- Neenah Enterprises Inc.

- Xinxing Ductile Iron Pipes Co., Ltd.

- Waupaca Foundry, Inc.

Frequently Asked Questions

What is the current market size and projected growth rate for iron and steel casting?

The Iron and Steel Casting Market is estimated at USD 105.7 Billion in 2025 and is projected to reach USD 172.9 Billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 6.2% during the forecast period.

Which end-use industries primarily drive the demand for iron and steel castings?

The automotive, industrial machinery, and construction sectors are the primary drivers of demand for iron and steel castings. These industries rely heavily on cast components for their durability, strength, and versatility in various applications.

What are the key technological trends influencing the iron and steel casting market?

Key technological trends include the adoption of automation and robotics, digitalization through Industry 4.0 principles, the development of lightweight and advanced alloy castings, and the integration of AI for quality control and process optimization.

How do environmental regulations impact the iron and steel casting industry?

Environmental regulations impose significant compliance costs on foundries, necessitating investments in pollution control technologies and energy-efficient processes. These regulations drive the industry towards more sustainable production practices, including waste reduction and increased recycling.

Which regions are expected to exhibit the most significant growth in the iron and steel casting market?

Asia Pacific is expected to exhibit the most significant growth, driven by rapid industrialization and infrastructure development in countries like China and India. North America and Europe also show steady growth due to technological advancements and strong automotive and industrial sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted