Bioethanol Market

Bioethanol Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704510 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Bioethanol Market Size

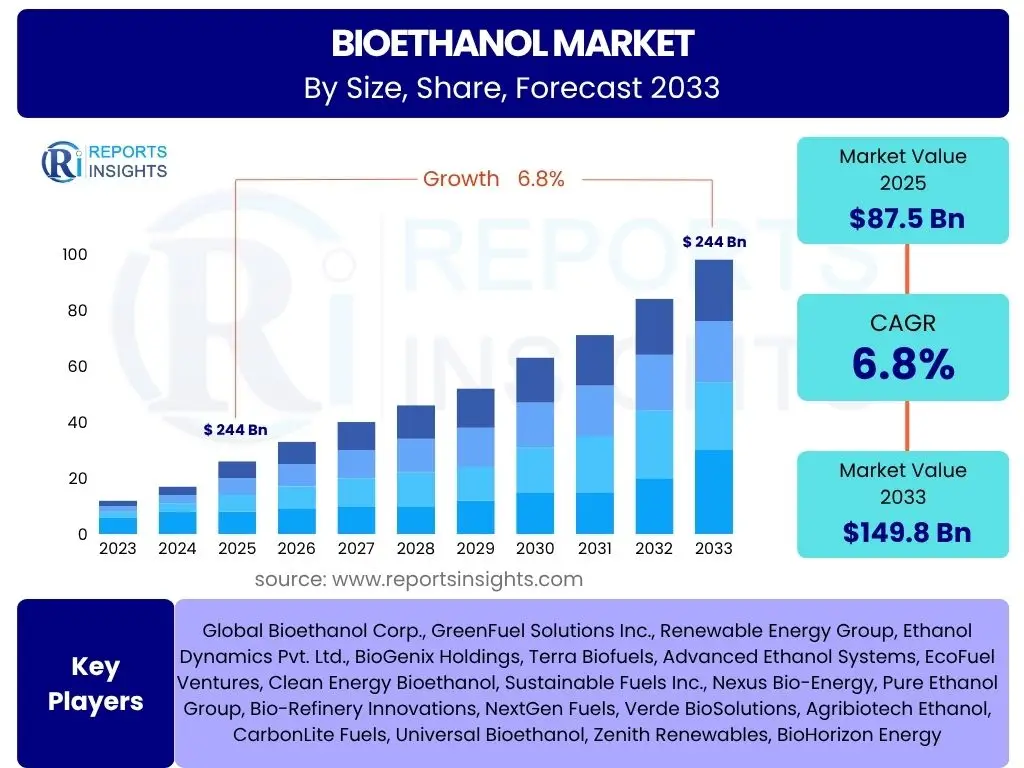

According to Reports Insights Consulting Pvt Ltd, The Bioethanol Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 87.5 Billion in 2025 and is projected to reach USD 149.8 Billion by the end of the forecast period in 2033.

The consistent growth trajectory of the global bioethanol market is primarily driven by an increasing global emphasis on sustainable energy solutions and the imperative to reduce greenhouse gas emissions. Bioethanol, as a renewable fuel, offers a compelling alternative to traditional fossil fuels, particularly in the transportation sector. The estimated market size for 2025 reflects robust current adoption and ongoing policy support in various regions, indicating a strong foundation for future expansion. This foundational demand, coupled with technological advancements in production and diversified feedstock options, underpins the market's current valuation.

The projected substantial increase in market value by 2033 underscores the anticipated acceleration of bioethanol's integration into global energy matrices. This growth is expected to be fueled by stringent environmental regulations, growing investments in advanced biofuel technologies, and expanding flex-fuel vehicle fleets in key economies. Furthermore, the diversification of bioethanol's applications beyond just fuel, into industrial solvents and biochemicals, will contribute significantly to its market expansion, ensuring a broad and resilient growth pathway over the forecast period.

Key Bioethanol Market Trends & Insights

Analysis of common user questions reveals a strong interest in the evolving landscape of the bioethanol market, specifically concerning shifts in feedstock utilization, technological advancements in production efficiency, and the influence of environmental policies. Users are keen to understand which types of bioethanol are gaining traction, how sustainability concerns are being addressed, and the role of innovation in driving market growth. There is also significant curiosity about the integration of bioethanol into broader energy transition strategies and its competitiveness against other renewable and conventional fuels.

The market is witnessing a notable pivot towards second and third-generation bioethanol production, driven by concerns over food security and land-use change associated with first-generation biofuels. This shift is fostering innovation in utilizing lignocellulosic biomass, agricultural residues, and even algae as sustainable feedstocks, promising a lower carbon footprint and reduced competition with food crops. Concurrently, advancements in fermentation technologies, enzyme development, and process optimization are enhancing conversion efficiencies and lowering production costs, making bioethanol a more economically viable and environmentally attractive option. Policy support, in the form of blending mandates and incentives for sustainable biofuels, continues to be a critical determinant of market direction, ensuring sustained demand and investment in the sector.

- Shift towards advanced second and third-generation bioethanol production from non-food feedstocks.

- Increasing research and development in optimizing fermentation processes and enzyme technologies for higher yields.

- Growing adoption of bioethanol as a blending component in aviation fuels (Sustainable Aviation Fuel - SAF).

- Expansion of flex-fuel vehicle fleets and infrastructure in emerging economies.

- Integration of carbon capture and utilization (CCU) technologies in bioethanol production facilities to further reduce carbon intensity.

AI Impact Analysis on Bioethanol

User inquiries regarding the impact of Artificial Intelligence (AI) on the bioethanol sector predominantly center on its potential to revolutionize production efficiency, optimize feedstock management, and accelerate research and development. Common questions revolve around how AI can enhance yield, reduce operational costs, and improve the sustainability profile of bioethanol. There's also an interest in AI's role in predicting market trends and managing supply chain complexities, highlighting expectations for AI to drive both technical and commercial advancements within the industry.

Artificial Intelligence is poised to significantly transform the bioethanol industry by enabling more precise and efficient operations across the entire value chain. In feedstock management, AI algorithms can analyze vast datasets, including soil conditions, weather patterns, and crop yields, to optimize cultivation practices and predict feedstock availability, thereby ensuring a consistent and cost-effective supply. Within the production process, AI-driven solutions can monitor and control fermentation parameters in real-time, leading to optimized reaction conditions, increased ethanol yields, and reduced energy consumption. Predictive maintenance for machinery also becomes possible, minimizing downtime and operational inefficiencies.

Furthermore, AI accelerates research and development by facilitating the discovery of new enzymes, microorganisms, and conversion pathways through advanced computational modeling and simulation. This drastically reduces the time and cost associated with laboratory experimentation. AI can also be applied to supply chain optimization, predicting demand fluctuations and optimizing logistics for feedstock transport and bioethanol distribution. The integration of AI tools is expected to lead to more economically competitive and environmentally sustainable bioethanol production, unlocking new levels of efficiency and innovation in the sector.

- AI-driven optimization of feedstock cultivation, harvest, and logistics for enhanced efficiency and reduced waste.

- Real-time process monitoring and control in biorefineries using AI for maximized yield and reduced energy consumption.

- Predictive analytics for equipment maintenance, minimizing downtime and improving operational reliability.

- Accelerated discovery of novel enzymes and microbial strains for improved bioethanol conversion through AI-powered bioinformatics.

- Enhanced supply chain management and market forecasting for bioethanol distribution using machine learning algorithms.

Key Takeaways Bioethanol Market Size & Forecast

Analysis of common user questions regarding the Bioethanol market's size and forecast reveals a strong desire for concise, actionable insights into its future trajectory and underlying drivers. Users are primarily concerned with understanding the market's long-term viability, the most influential growth factors, and potential challenges that could alter the projected expansion. There is also significant interest in identifying key investment areas and regions that are expected to demonstrate the most significant growth.

The market is poised for substantial and sustained growth, driven by an escalating global commitment to decarbonization and renewable energy sources. The Compound Annual Growth Rate (CAGR) indicates a healthy expansion, signifying increasing adoption rates and supportive policy frameworks worldwide. This growth is not merely volumetric but also qualitative, reflecting a shift towards more sustainable and technologically advanced production methods that mitigate environmental concerns and enhance economic competitiveness. The projected market value by 2033 underscores bioethanol's critical role in the future energy mix, particularly in the transportation sector, and its growing importance in bio-based industrial applications.

- The bioethanol market is set for robust growth, projected to reach USD 149.8 Billion by 2033, driven by sustainability mandates.

- Strong governmental support and blending mandates are critical catalysts for market expansion.

- Technological advancements in second and third-generation bioethanol production are enhancing cost-effectiveness and environmental benefits.

- Diversification of applications beyond fuel, including industrial solvents and biochemicals, is opening new revenue streams.

- The market's long-term outlook is positive, underpinned by increasing demand for renewable fuels and the push for reduced carbon emissions globally.

Bioethanol Market Drivers Analysis

The bioethanol market's significant growth is primarily propelled by a convergence of environmental imperatives, energy security concerns, and supportive governmental policies. Governments worldwide are increasingly implementing stringent regulations and mandates aimed at reducing greenhouse gas emissions and diversifying energy sources away from fossil fuels. This commitment to climate goals directly translates into higher demand for biofuels like bioethanol, which offer a readily available renewable alternative, particularly for the transportation sector. The increasing focus on energy independence and reducing reliance on volatile oil markets also positions bioethanol as a strategic component of national energy strategies, further stimulating its production and consumption. Furthermore, the automotive industry's continuous innovation in flex-fuel vehicle technologies supports higher blending ratios, expanding the market's absorption capacity.

Consumer awareness and corporate sustainability initiatives also play a crucial role in driving demand. As environmental consciousness grows, both individual consumers and large corporations are seeking greener alternatives, which includes cleaner-burning fuels. This aligns with the broader corporate social responsibility goals and contributes to the market's expansion. Additionally, the increasing availability of diverse and sustainable feedstocks, coupled with ongoing technological advancements that improve conversion efficiency and reduce production costs, makes bioethanol a more competitive and attractive option. The synergistic effect of these drivers creates a positive feedback loop, encouraging further investment and innovation in the bioethanol value chain.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Government Mandates & Policies (e.g., RFS, RED) | +2.0% | North America, Europe, Brazil, India | Long-term (2025-2033) |

| Growing Environmental Concerns & Decarbonization Goals | +1.5% | Global | Long-term (2025-2033) |

| Energy Security & Diversification of Energy Sources | +1.0% | Europe, Asia Pacific, Emerging Economies | Medium-term (2025-2029) |

| Increasing Demand for Cleaner Fuels in Transportation | +1.3% | Global, particularly developing nations | Long-term (2025-2033) |

| Technological Advancements in Production Efficiency | +1.0% | Global | Medium-term to Long-term (2025-2033) |

Bioethanol Market Restraints Analysis

Despite the strong growth drivers, the bioethanol market faces several significant restraints that could impede its full potential. A prominent concern is the ongoing "food versus fuel" debate, particularly in regions heavily reliant on first-generation bioethanol from food crops like corn or sugarcane. This debate raises ethical questions about diverting food resources for fuel production, especially in the context of global food security and fluctuating commodity prices. Such concerns can lead to public backlash, policy adjustments, and increased scrutiny, potentially limiting expansion in certain markets or feedstock choices. Furthermore, the substantial land and water resources required for large-scale feedstock cultivation raise environmental sustainability questions, including deforestation and water stress, which can create opposition to market growth.

Another critical restraint is the economic competitiveness of bioethanol compared to conventional fossil fuels and emerging alternatives like electric vehicles (EVs). Fluctuations in crude oil prices can directly impact bioethanol's profitability; when oil prices are low, the economic incentive to use bioethanol diminishes. Additionally, the capital-intensive nature of establishing and operating bioethanol production facilities, especially for advanced biofuels, poses a barrier to entry and expansion. The nascent but rapid rise of electric vehicles also presents a long-term challenge to the demand for liquid transportation fuels, including bioethanol, as the world transitions towards electrification. Policy instability and the unpredictable nature of government incentives can also create an uncertain investment climate, hindering long-term planning and large-scale project development in the bioethanol sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Food vs. Fuel Debate & Land Use Concerns | -0.8% | Global, especially food-deficit regions | Long-term (2025-2033) |

| Competition from Electric Vehicles (EVs) | -1.2% | North America, Europe, China | Long-term (2027-2033) |

| Volatility in Feedstock Prices & Availability | -0.7% | Global | Medium-term (2025-2029) |

| High Production Costs (especially for advanced biofuels) | -0.6% | Global | Medium-term (2025-2029) |

| Uncertainty in Government Policies & Subsidies | -0.5% | Certain Developed Markets | Short-term to Medium-term (2025-2027) |

Bioethanol Market Opportunities Analysis

The bioethanol market is characterized by several significant opportunities that are poised to accelerate its growth and diversification. One of the most promising avenues lies in the continued development and commercialization of advanced biofuels, particularly second and third-generation bioethanol. These technologies, which utilize non-food feedstocks such as agricultural residues, woody biomass, or algae, address the "food versus fuel" concerns and offer a more sustainable and potentially scalable production pathway. Investment in research and development for these advanced methods is unlocking higher conversion efficiencies and reducing the overall carbon footprint, making bioethanol a more attractive option for governments and industries aiming for aggressive decarbonization targets.

Beyond traditional fuel blending, the expansion into new end-use applications presents another substantial opportunity. Bioethanol serves as a versatile building block for various bio-based chemicals, plastics, and other industrial products, offering a sustainable alternative to petrochemicals. The growing demand for sustainable aviation fuels (SAF) also represents a nascent but high-potential market segment for bioethanol derivatives. Furthermore, emerging economies, particularly in Asia Pacific and Latin America, offer immense growth potential due to rising energy demands, increasing environmental awareness, and developing policy frameworks supportive of biofuels. These regions are actively seeking diverse and sustainable energy solutions, providing fertile ground for bioethanol market expansion, alongside opportunities for technological transfer and infrastructure development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced (2nd & 3rd Gen) Bioethanol | +1.5% | Global | Long-term (2026-2033) |

| Growth in Sustainable Aviation Fuel (SAF) Market | +1.0% | North America, Europe, Asia Pacific | Long-term (2027-2033) |

| Diversification into Bio-based Chemicals & Solvents | +0.8% | Global | Medium-term (2025-2029) |

| Untapped Potential in Emerging Economies | +0.9% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Carbon Capture, Utilization & Storage (CCUS) Integration | +0.7% | North America, Europe | Medium-term to Long-term (2026-2033) |

Bioethanol Market Challenges Impact Analysis

The bioethanol market, while promising, grapples with several formidable challenges that can influence its growth trajectory. One significant hurdle is the debate surrounding the true environmental impact of bioethanol, particularly first-generation biofuels. Concerns over indirect land-use change (ILUC), deforestation, and the environmental footprint of cultivation practices, including water usage and fertilizer runoff, can undermine the sustainability credentials of bioethanol. Addressing these concerns requires transparent lifecycle assessments and the adoption of more sustainable feedstock sourcing and production methods. Furthermore, the extensive infrastructure required for higher ethanol blends, especially for distribution and vehicle compatibility, poses a considerable financial and logistical challenge in many regions.

Another key challenge pertains to the economic viability and price competitiveness of bioethanol against conventional petroleum fuels. The profitability of bioethanol producers is often sensitive to fluctuations in crude oil prices, feedstock costs, and the level of government subsidies. Without consistent policy support or a significant carbon price, bioethanol may struggle to compete purely on price in a volatile energy market. Technological scalability for advanced bioethanol, though a significant opportunity, also presents a challenge, as transitioning from laboratory-scale innovations to commercial, industrial-scale production often involves high capital expenditure, complex engineering, and overcoming unforeseen operational hurdles. Public perception, often influenced by the food versus fuel debate and perceived environmental trade-offs, can also serve as a barrier, impacting consumer acceptance and policy support.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Sustainability Concerns (ILUC, Water Use) | -0.9% | Global, especially developed markets | Long-term (2025-2033) |

| Inadequate Infrastructure for Higher Blends | -0.7% | Asia Pacific, Africa, Parts of Europe | Medium-term (2025-2029) |

| Price Volatility of Crude Oil and Feedstocks | -0.8% | Global | Short-term to Medium-term (2025-2028) |

| Technological Scaling for Advanced Biofuels | -0.6% | Global | Medium-term (2025-2029) |

| Competition from Other Renewable Energy Sources | -0.5% | Global | Long-term (2027-2033) |

Bioethanol Market - Updated Report Scope

This market research report provides a comprehensive analysis of the global bioethanol market, encompassing its historical performance, current dynamics, and future projections. The scope includes an in-depth examination of market size and growth, key trends, drivers, restraints, and opportunities influencing the industry landscape. The report segments the market by feedstock type, end-use application, and generation type, offering detailed insights into each segment's contribution and growth potential. Furthermore, a thorough regional analysis is presented, highlighting the market's performance and key country-level dynamics across major geographical regions. The competitive landscape section profiles leading companies, assessing their strategies, product portfolios, and market positioning. This structured approach aims to provide stakeholders with actionable intelligence for strategic decision-making and investment planning within the bioethanol sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 87.5 Billion |

| Market Forecast in 2033 | USD 149.8 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Bioethanol Corp., GreenFuel Solutions Inc., Renewable Energy Group, Ethanol Dynamics Pvt. Ltd., BioGenix Holdings, Terra Biofuels, Advanced Ethanol Systems, EcoFuel Ventures, Clean Energy Bioethanol, Sustainable Fuels Inc., Nexus Bio-Energy, Pure Ethanol Group, Bio-Refinery Innovations, NextGen Fuels, Verde BioSolutions, Agribiotech Ethanol, CarbonLite Fuels, Universal Bioethanol, Zenith Renewables, BioHorizon Energy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The bioethanol market is meticulously segmented to provide a granular view of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper understanding of market drivers, restraints, and opportunities specific to different production methods, feedstock sources, and end-use applications. Analyzing these segments helps stakeholders identify high-growth areas, assess competitive landscapes, and formulate targeted strategies that align with specific market needs and technological advancements. The interplay between these segments also sheds light on the evolving preferences for sustainable and efficient bioethanol production pathways, reflecting the industry's shift towards more environmentally benign practices.

The segmentation by feedstock reveals the dominance of corn and sugarcane in first-generation production, while highlighting the accelerating growth and investment in cellulosic and other advanced feedstocks due to sustainability imperatives. End-use segmentation illustrates bioethanol's expanding utility beyond fuel blending, showcasing its significant role in industrial applications, beverages, cosmetics, and pharmaceuticals. Finally, the generation type segmentation provides a clear distinction between conventional and advanced bioethanol forms, indicating the industry's progression towards more sustainable and technologically sophisticated production methods. Each segment's performance and projected growth are crucial for comprehensive market assessment and strategic planning.

- By Feedstock: Corn, Sugarcane, Cellulosic (Agricultural Residues, Forest Residues, Energy Crops, Municipal Solid Waste), Others (Algae, Sweet Sorghum)

- By End-Use: Fuel & Blending, Industrial Solvents, Alcoholic Beverages, Cosmetics, Pharmaceuticals

- By Generation Type: First Generation, Second Generation, Third Generation, Fourth Generation

Regional Highlights

- North America: Dominates the bioethanol market, primarily driven by robust government mandates such as the Renewable Fuel Standard (RFS) in the U.S. and ample corn feedstock availability. The region also leads in research and development for advanced biofuels.

- Europe: Characterized by strong policy support, including the Renewable Energy Directive (RED), focusing on reducing greenhouse gas emissions and promoting advanced biofuels. Strict sustainability criteria influence feedstock choices, driving innovation in cellulosic ethanol.

- Asia Pacific (APAC): Emerging as a significant growth region due to increasing energy demand, growing environmental awareness, and developing biofuel policies in countries like China and India. The region offers immense potential for sugarcane and cellulosic ethanol production.

- Latin America: Led by Brazil, a global pioneer in sugarcane-based bioethanol production, with high blending mandates and a well-established flex-fuel vehicle fleet. Other countries in the region are also exploring bioethanol expansion.

- Middle East and Africa (MEA): A nascent but growing market, driven by rising energy consumption and increasing interest in diversifying energy sources. Investments in sustainable agriculture and renewable energy projects are expected to foster bioethanol adoption in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bioethanol Market.- Global Bioethanol Corp.

- GreenFuel Solutions Inc.

- Renewable Energy Group

- Ethanol Dynamics Pvt. Ltd.

- BioGenix Holdings

- Terra Biofuels

- Advanced Ethanol Systems

- EcoFuel Ventures

- Clean Energy Bioethanol

- Sustainable Fuels Inc.

- Nexus Bio-Energy

- Pure Ethanol Group

- Bio-Refinery Innovations

- NextGen Fuels

- Verde BioSolutions

- Agribiotech Ethanol

- CarbonLite Fuels

- Universal Bioethanol

- Zenith Renewables

- BioHorizon Energy

Frequently Asked Questions

What is bioethanol and why is it important?

Bioethanol is a renewable fuel produced through the fermentation of biomass, primarily starches and sugars from plants like corn, sugarcane, or cellulosic materials. It is crucial for reducing greenhouse gas emissions, enhancing energy security, and diversifying the global energy mix, particularly as a cleaner-burning alternative to gasoline in transportation.

What are the primary drivers for the bioethanol market's growth?

The key drivers include stringent government mandates and policies promoting renewable fuels, increasing global focus on decarbonization and environmental sustainability, growing demand for cleaner transportation fuels, and the pursuit of energy independence by various nations. Technological advancements in production also play a significant role.

What challenges does the bioethanol industry face?

Major challenges include the "food versus fuel" debate, concerns over indirect land-use change and water consumption, volatility in feedstock prices, the significant infrastructure investment required for higher blend usage, and growing competition from electric vehicles in the long term.

How are advancements in feedstock impacting bioethanol production?

Advancements are shifting production towards second and third-generation bioethanol, utilizing non-food feedstocks like agricultural residues, woody biomass, and algae. This reduces competition with food crops, improves sustainability, and expands the potential for bioethanol production by leveraging diverse and abundant biomass resources.

What role do government policies play in the bioethanol market?

Government policies are pivotal, providing the regulatory framework and incentives, such as blending mandates (e.g., RFS, RED), tax credits, and subsidies, that drive demand and investment in the bioethanol sector. These policies are critical for creating a stable market environment and promoting the adoption of renewable fuels.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted