Soldering Iron and Station Market

Soldering Iron and Station Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704453 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Soldering Iron and Station Market Size

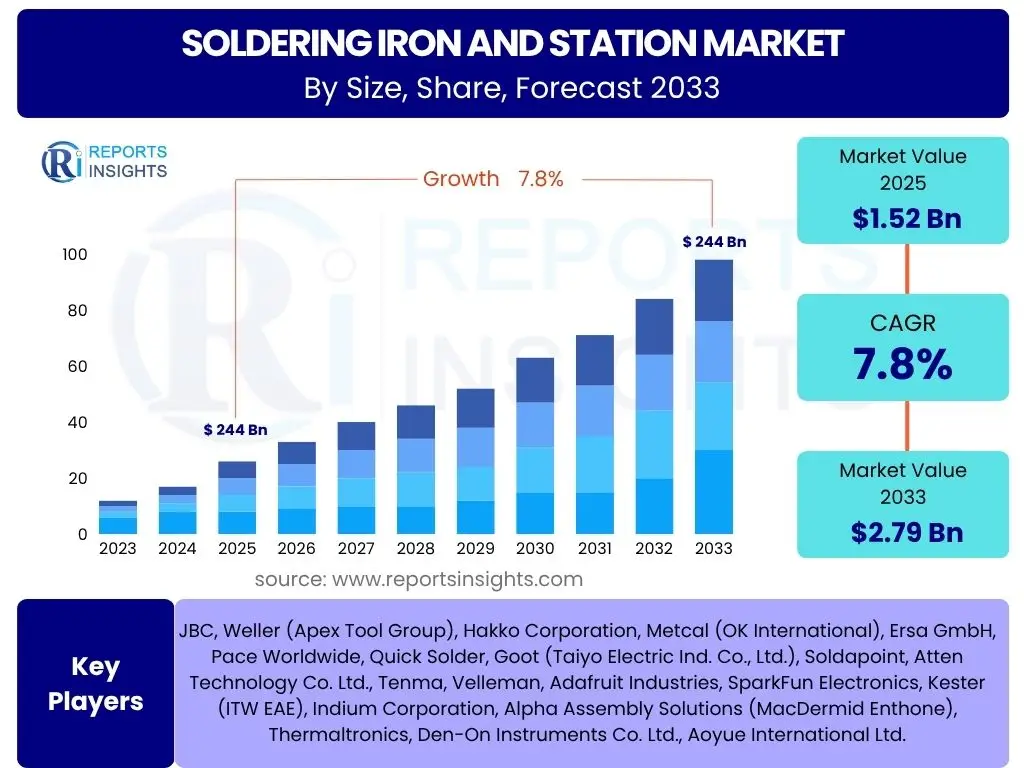

According to Reports Insights Consulting Pvt Ltd, The Soldering Iron and Station Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.52 Billion in 2025 and is projected to reach USD 2.79 Billion by the end of the forecast period in 2033.

Key Soldering Iron and Station Market Trends & Insights

User inquiries frequently focus on the evolving landscape of soldering technologies, specifically exploring how market dynamics are shifting in response to technological advancements and industry demands. A significant area of interest revolves around the increasing adoption of lead-free soldering solutions, driven by environmental regulations and a growing emphasis on sustainable manufacturing practices. Additionally, there is a clear demand for insights into automation and precision in soldering processes, particularly in high-volume electronics manufacturing.

Another prominent theme in user questions concerns the impact of miniaturization in electronic components on soldering equipment requirements. As devices become smaller and more complex, there is a critical need for soldering irons and stations that offer enhanced accuracy, thermal control, and adaptability for fine-pitch components. Furthermore, users are keen to understand the role of smart features, such as digital temperature control, data logging, and connectivity, in improving efficiency and quality control within soldering operations.

The market is increasingly influenced by the convergence of traditional soldering techniques with advanced manufacturing paradigms, including Industry 4.0 principles. This integration necessitates equipment capable of seamless data exchange and remote monitoring, enabling predictive maintenance and optimized production workflows. The demand for ergonomic designs and user-friendly interfaces also remains a consistent trend, reflecting the need for equipment that enhances operator comfort and reduces fatigue in intricate soldering tasks.

- Transition to Lead-Free Soldering: Driven by environmental regulations and health concerns.

- Miniaturization of Electronic Components: Demanding higher precision and finer tip sizes.

- Increased Automation and Robotic Soldering: Enhancing efficiency and consistency in manufacturing.

- Integration of Smart Features: Digital temperature control, connectivity, and data analytics.

- Demand for Ergonomic and User-Friendly Designs: Improving operator comfort and productivity.

- Focus on Thermal Stability and Control: Crucial for sensitive components and consistent quality.

- Rise of Rework and Repair Stations: Addressing complex repair needs for advanced electronics.

AI Impact Analysis on Soldering Iron and Station

User questions regarding AI's impact on soldering iron and station technology primarily revolve around its potential to revolutionize manufacturing precision, quality assurance, and operational efficiency. There is significant interest in how artificial intelligence can enable more sophisticated automated soldering processes, moving beyond simple programmed movements to adaptive, real-time adjustments based on complex variables. Users are keen to understand if AI can detect subtle defects during soldering, predict equipment maintenance needs, or even optimize thermal profiles for different solder joints.

Another key area of inquiry pertains to AI's role in improving quality control and reducing human error. Users are exploring the feasibility of AI-powered vision systems for post-soldering inspection, capable of identifying microscopic flaws that might be missed by human operators or conventional automated optical inspection (AOI) systems. The concept of AI-driven predictive analytics for soldering tip wear or flux degradation also garners attention, aiming to minimize downtime and ensure consistent performance throughout production cycles.

Ultimately, the overarching expectation is that AI integration will lead to more intelligent, self-optimizing soldering environments. This includes the potential for AI to learn from vast datasets of soldering parameters and outcomes, continuously refining process control and material utilization. While the direct integration of AI within a handheld soldering iron might be limited, its pervasive influence on robotic soldering stations, automated assembly lines, and comprehensive quality management systems is anticipated to significantly enhance precision, reliability, and cost-effectiveness across the electronics manufacturing sector.

- Enhanced Quality Control: AI-powered vision systems for defect detection and real-time inspection.

- Predictive Maintenance: AI algorithms analyzing equipment performance to anticipate failures and optimize upkeep.

- Process Optimization: AI-driven adjustments to soldering parameters (temperature, time, pressure) for optimal joint quality.

- Robotic Soldering Advancement: Enabling more adaptive, precise, and autonomous robotic soldering operations.

- Data Analytics and Insights: AI processing large datasets from soldering processes to identify trends and improve efficiency.

Key Takeaways Soldering Iron and Station Market Size & Forecast

User inquiries about the key takeaways from the soldering iron and station market size and forecast consistently highlight the market's robust growth trajectory, driven primarily by the relentless expansion of the global electronics industry. A significant insight is the sustained demand for advanced soldering solutions, moving beyond basic tools to sophisticated stations equipped with precise temperature control, digital interfaces, and enhanced safety features. This indicates a market maturation where quality, efficiency, and technological sophistication are becoming paramount considerations for purchasers across various sectors.

Another crucial takeaway frequently sought by users relates to the regional dynamics influencing market growth. The rapid industrialization and burgeoning electronics manufacturing hubs in Asia Pacific, particularly China, India, and Southeast Asian nations, are identified as major catalysts for market expansion. This regional dominance underscores the shift in global manufacturing paradigms and the increasing investment in advanced production capabilities within these economies. Concurrently, innovation in North America and Europe continues to drive demand for high-end, specialized soldering equipment for niche applications.

Furthermore, the market's resilience is notable, adaptable to challenges such as skilled labor shortages by fostering automation, and responding to environmental pressures through the adoption of lead-free technologies. The forecasted growth signifies not just an increase in unit sales, but a clear shift towards higher-value, more technologically integrated solutions that meet the evolving demands of intricate electronics assembly and repair. This forward momentum is expected to persist, reflecting the indispensable role of soldering in modern technological infrastructure.

- Steady Market Expansion: Consistent growth projected, driven by global electronics manufacturing.

- Technological Evolution: Increasing demand for advanced, precision-controlled, and smart soldering solutions.

- Regional Growth Hubs: Asia Pacific continues to be a primary growth engine due to robust manufacturing activities.

- Sustainability Focus: Accelerated adoption of lead-free and energy-efficient soldering practices.

- Industry Adaptation: Market responding to challenges like miniaturization and automation requirements.

Soldering Iron and Station Market Drivers Analysis

The global surge in electronics manufacturing stands as a paramount driver for the soldering iron and station market. The proliferation of consumer electronics, including smartphones, laptops, smart home devices, and wearables, necessitates high-volume production lines that rely heavily on efficient and precise soldering processes. Beyond consumer goods, the expanding sectors of automotive electronics, medical devices, and telecommunications infrastructure also fuel demand for advanced soldering equipment, as these industries increasingly integrate complex electronic components requiring reliable and durable connections.

Technological advancements in printed circuit board (PCB) design and component miniaturization are further propelling market growth. As electronic components become smaller and more densely packed, the need for soldering irons and stations capable of extremely precise, controlled, and localized heating becomes critical. This drives innovation in tip design, thermal management systems, and ergonomic features, pushing manufacturers to develop more sophisticated and specialized equipment to meet the stringent requirements of modern electronics assembly. The continuous innovation in soldering alloys and fluxes also demands compatible and optimized heating tools.

Moreover, the increasing adoption of automation and robotic solutions in manufacturing processes contributes significantly to market expansion. While automated soldering machines are a distinct category, the underlying need for high-quality, consistent solder joints necessitates advanced soldering stations for prototyping, rework, and specialized applications that complement automated lines. The demand for reliable and efficient repair and rework stations for complex and high-value electronic assemblies further strengthens the market, ensuring the longevity and functionality of advanced electronic products across various industries.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electronics Manufacturing | +2.5% | Global, particularly Asia Pacific | Short- to Long-Term |

| Miniaturization and Complex PCBs | +1.8% | Global, especially high-tech regions | Mid- to Long-Term |

| Increasing Automation in Production | +1.5% | North America, Europe, Asia Pacific | Mid- to Long-Term |

| Demand for Lead-Free Soldering | +1.0% | Europe, North America, Asia Pacific | Short- to Mid-Term |

| Expansion of Automotive Electronics | +0.7% | Europe, North America, Asia Pacific | Mid- to Long-Term |

Soldering Iron and Station Market Restraints Analysis

The primary restraint facing the soldering iron and station market is the high initial investment cost associated with advanced, high-precision soldering stations, particularly those designed for complex manufacturing or specialized applications. While basic soldering irons are relatively inexpensive, professional-grade stations with digital temperature control, multiple tip options, integrated fume extraction, and smart features represent a significant capital expenditure for small to medium-sized enterprises (SMEs) or individual hobbyists. This cost barrier can limit widespread adoption, especially in price-sensitive emerging markets, despite the long-term benefits of efficiency and quality.

Another significant restraint is the shortage of skilled labor proficient in intricate soldering techniques. Modern electronics assembly, particularly with surface-mount devices (SMD) and fine-pitch components, requires highly trained technicians. The dwindling availability of such expertise, coupled with the time and cost associated with training new personnel, can hinder the full utilization of advanced soldering equipment. This creates a bottleneck in production processes and may lead some manufacturers to seek alternative joining methods or outsource complex assembly, thereby dampening demand for new equipment.

Furthermore, the increasing adoption of alternative joining technologies, such as conductive adhesives, laser welding, and crimping, poses a competitive threat to traditional soldering. While soldering remains indispensable for many applications, these alternative methods offer advantages in specific scenarios, such as heat-sensitive components or applications requiring flexibility. Environmental regulations, particularly concerning lead content, also present challenges by necessitating costly transitions to new materials and processes, which can increase operational expenses and slow down equipment upgrades for companies hesitant to invest in new lead-free compatible stations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment for Advanced Systems | -1.2% | Global, particularly SMEs | Short- to Mid-Term |

| Shortage of Skilled Soldering Technicians | -0.9% | North America, Europe, parts of Asia | Mid- to Long-Term |

| Competition from Alternative Joining Technologies | -0.8% | Global, niche applications | Mid- to Long-Term |

| Volatile Raw Material Prices | -0.5% | Global | Short- to Mid-Term |

Soldering Iron and Station Market Opportunities Analysis

The expansion of smart manufacturing and Industry 4.0 initiatives presents a significant opportunity for the soldering iron and station market. The integration of soldering equipment into networked production environments, leveraging IoT capabilities for real-time monitoring, data analytics, and remote control, can significantly enhance efficiency and quality assurance. This trend encourages the development of "smart" soldering stations capable of seamless communication with other factory systems, enabling predictive maintenance, automated process adjustments, and comprehensive traceability of soldering operations, thereby offering value beyond basic functionality.

The burgeoning sectors of electric vehicles (EVs) and renewable energy technologies also offer substantial growth opportunities. The complex power electronics, battery management systems, and charging infrastructure within EVs, as well as the intricate components in solar inverters and wind turbine controls, all require robust and precise soldering connections. This demand for high-reliability solder joints in harsh environments drives the need for specialized, high-power soldering stations and advanced rework tools capable of handling larger components and higher thermal loads, fostering innovation in equipment design and capabilities.

Furthermore, the increasing complexity and value of modern electronic devices create a growing market for specialized rework and repair stations. As consumer and industrial electronics become more expensive and difficult to replace, there is a rising demand for tools that can accurately repair or replace individual components on densely populated PCBs without damaging surrounding circuitry. This segment offers opportunities for manufacturers to develop highly sophisticated rework stations with features like advanced optical alignment, localized heating, and precise temperature profiling, catering to professional repair centers and specialized industrial applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Smart Manufacturing & Industry 4.0 Integration | +1.7% | Global, particularly developed regions | Mid- to Long-Term |

| Growth in Electric Vehicles & Renewable Energy | +1.5% | Global | Mid- to Long-Term |

| Demand for Advanced Rework & Repair Solutions | +1.3% | Global, professional services | Short- to Mid-Term |

| Emergence of New Electronic Applications (e.g., 5G, IoT) | +1.0% | Global | Mid- to Long-Term |

Soldering Iron and Station Market Challenges Impact Analysis

One of the primary challenges for the soldering iron and station market is the rapid pace of technological obsolescence in the electronics industry. As new components, materials, and manufacturing processes emerge frequently, soldering equipment must constantly evolve to remain compatible and efficient. This requires significant research and development investment from manufacturers to keep their product lines updated, and it poses a challenge for end-users who face the need for frequent equipment upgrades, potentially impacting their return on investment and adoption rates of the latest soldering solutions. The short product lifecycles in consumer electronics, in particular, exacerbate this issue.

Another significant challenge stems from global supply chain disruptions and the volatility of raw material prices. The manufacturing of soldering irons and stations relies on various components, including specialized metals for tips, heating elements, and electronic circuitry. Geopolitical events, trade disputes, and natural disasters can disrupt the supply of these critical materials, leading to production delays and increased manufacturing costs. Fluctuating prices for key inputs directly impact the profitability of soldering equipment manufacturers and can translate into higher prices for end-users, potentially slowing market growth.

Furthermore, environmental regulations, especially those mandating the reduction or elimination of lead in soldering processes, present a continuous challenge. While driving the adoption of lead-free solutions, the transition requires significant investment in new equipment, training, and process optimization for manufacturers and end-users alike. The differences in thermal properties and joint characteristics of lead-free solders necessitate more precise temperature control and more robust equipment, which can be more complex to operate and maintain. Ensuring consistent quality and reliability with these newer materials remains an ongoing hurdle for the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -1.0% | Global | Short- to Mid-Term |

| Supply Chain Disruptions & Raw Material Volatility | -0.8% | Global | Short-Term |

| Adherence to Environmental Regulations (e.g., Lead-Free) | -0.7% | Europe, North America, Asia Pacific | Short- to Mid-Term |

| Intense Market Competition & Price Pressure | -0.5% | Global | Short- to Mid-Term |

Soldering Iron and Station Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global soldering iron and station market, offering detailed insights into its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges that shape the industry landscape, alongside a granular segmentation analysis across various types, technologies, applications, and regional markets. The report aims to furnish stakeholders with critical intelligence necessary for strategic decision-making and understanding competitive dynamics within this essential segment of the electronics manufacturing ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.52 Billion |

| Market Forecast in 2033 | USD 2.79 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | JBC, Weller (Apex Tool Group), Hakko Corporation, Metcal (OK International), Ersa GmbH, Pace Worldwide, Quick Solder, Goot (Taiyo Electric Ind. Co., Ltd.), Soldapoint, Atten Technology Co. Ltd., Tenma, Velleman, Adafruit Industries, SparkFun Electronics, Kester (ITW EAE), Indium Corporation, Alpha Assembly Solutions (MacDermid Enthone), Thermaltronics, Den-On Instruments Co. Ltd., Aoyue International Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The soldering iron and station market is extensively segmented to provide a nuanced understanding of its diverse landscape and the varied needs of its end-users. This segmentation allows for a detailed analysis of market dynamics across different product types, technologies, applications, and user categories, reflecting the specialized requirements inherent in modern electronics manufacturing and repair. Understanding these distinct segments is crucial for identifying specific growth pockets and developing targeted market strategies, given the wide range of precision, power, and functionality demanded by different industries and users.

Segmentation by product type typically differentiates between standalone soldering irons, comprehensive soldering stations, and highly specialized rework or desoldering stations. Each type caters to distinct operational needs, from basic assembly to intricate component replacement on multi-layered PCBs. Technology-based segmentation highlights the ongoing shift towards lead-free soldering solutions and the increasing adoption of digitally controlled and smart, IoT-enabled equipment, which offer enhanced precision, efficiency, and connectivity, signifying the market's technological progression.

Furthermore, the market is segmented by application, covering a broad spectrum of industries from high-volume consumer electronics and rapidly expanding automotive electronics to specialized fields like aerospace, medical devices, and telecommunications. This application-based analysis reveals the critical role of soldering in diverse manufacturing environments. Lastly, end-user segmentation distinguishes between Original Equipment Manufacturers (OEMs), Contract Manufacturers (CMs), repair and service centers, educational institutions, and individual hobbyists, each with unique purchasing patterns, volume requirements, and demands for specific features or capabilities from soldering equipment.

- By Product Type: Soldering Irons, Soldering Stations, Rework Stations, Desoldering Stations.

- By Technology: Lead-Free Soldering, Leaded Soldering, Temperature Controlled, Smart/IoT Enabled.

- By Application: Consumer Electronics, Automotive Electronics, Aerospace & Defense, Medical Devices, Telecommunications, Industrial Manufacturing, Research & Development, Hobbyists & DIY.

- By End-User: Original Equipment Manufacturers (OEMs), Contract Manufacturers (CMs), Repair & Service Centers, Educational Institutions, Individuals & Hobbyists.

Regional Highlights

- Asia Pacific (APAC): This region is anticipated to be the largest and fastest-growing market for soldering irons and stations due to its robust electronics manufacturing base, including countries like China, South Korea, Japan, Taiwan, and India. The increasing foreign direct investment in manufacturing facilities, coupled with a large workforce and a burgeoning domestic demand for electronic products, fuels significant adoption of both basic and advanced soldering equipment. Government initiatives supporting local manufacturing and the expansion of smart factories further contribute to its dominance.

- North America: The North American market is characterized by a strong emphasis on technological innovation, high-precision manufacturing, and specialized applications, particularly in aerospace, defense, medical devices, and advanced telecommunications (e.g., 5G infrastructure). While not as high-volume as APAC in terms of basic electronics, the demand for high-end, intelligent soldering stations for R&D, prototyping, and complex rework operations is substantial. The region also exhibits a growing trend towards automation in electronics assembly.

- Europe: Europe represents a mature market with a focus on quality, sustainability, and adherence to stringent environmental regulations, particularly concerning lead-free soldering. Countries like Germany, France, and the UK are leaders in industrial automation and advanced electronics manufacturing, driving demand for technologically sophisticated and energy-efficient soldering solutions. The automotive industry's push towards electric vehicles and autonomous driving also significantly contributes to the need for advanced soldering equipment for power electronics and control units.

- Latin America: The Latin American market for soldering irons and stations is emerging, driven by increasing industrialization and foreign investment in electronics assembly plants, particularly in Mexico and Brazil. Growth is propelled by expanding consumer electronics production and the automotive sector. While still smaller than developed regions, there is a growing demand for cost-effective yet reliable soldering solutions, and a gradual shift towards more automated processes is observed.

- Middle East and Africa (MEA): This region is in an early stage of growth but holds potential due to ongoing infrastructure development projects, increasing adoption of consumer electronics, and nascent manufacturing hubs. Investments in telecommunications, energy, and defense sectors are slowly creating demand for soldering equipment. The market here is largely dependent on imports, with a focus on essential and durable equipment for repair and basic assembly tasks, though specialized solutions are sought for high-value projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Soldering Iron and Station Market.- JBC

- Weller (Apex Tool Group)

- Hakko Corporation

- Metcal (OK International)

- Ersa GmbH

- Pace Worldwide

- Quick Solder

- Goot (Taiyo Electric Ind. Co., Ltd.)

- Soldapoint

- Atten Technology Co. Ltd.

- Tenma

- Velleman

- Adafruit Industries

- SparkFun Electronics

- Kester (ITW EAE)

- Indium Corporation

- Alpha Assembly Solutions (MacDermid Enthone)

- Thermaltronics

- Den-On Instruments Co. Ltd.

- Aoyue International Ltd.

Frequently Asked Questions

What is the current market size of the Soldering Iron and Station Market?

The Soldering Iron and Station Market is estimated at USD 1.52 Billion in 2025, demonstrating strong growth potential in the electronics manufacturing sector.

What are the key trends shaping the Soldering Iron and Station Market?

Key trends include the increasing adoption of lead-free soldering, demand for miniaturization and precision, integration of smart features, and greater automation in soldering processes.

How is AI impacting the Soldering Iron and Station Market?

AI is primarily impacting the market through enhanced quality control, predictive maintenance for equipment, and process optimization, especially in automated and robotic soldering systems.

What are the main drivers for the growth of the Soldering Iron and Station Market?

The primary drivers are the consistent growth in global electronics manufacturing, the ongoing miniaturization of electronic components, and the increasing adoption of automation in production lines.

Which region dominates the Soldering Iron and Station Market?

The Asia Pacific (APAC) region currently dominates the Soldering Iron and Station Market, driven by its expansive electronics manufacturing base and rapid industrialization.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted