Spinal Implant and Surgical Device Market

Spinal Implant and Surgical Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705034 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Spinal Implant and Surgical Device Market Size

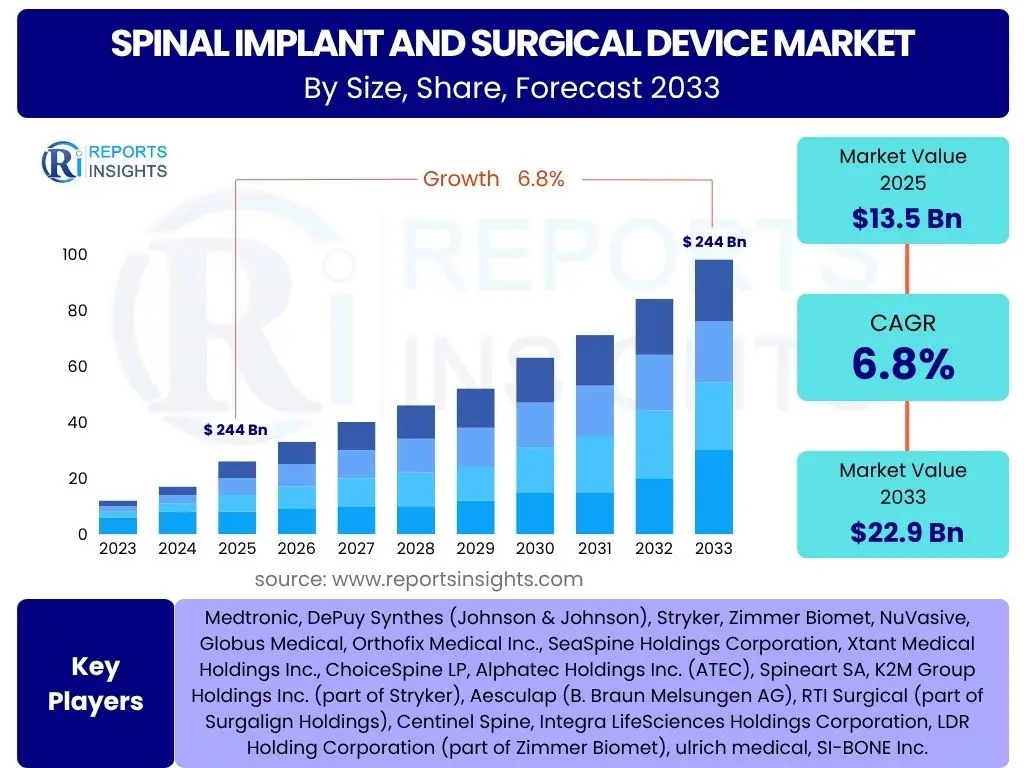

According to Reports Insights Consulting Pvt Ltd, The Spinal Implant and Surgical Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 13.5 billion in 2025 and is projected to reach USD 22.9 billion by the end of the forecast period in 2033.

Key Spinal Implant and Surgical Device Market Trends & Insights

The Spinal Implant and Surgical Device market is currently experiencing a transformative phase, driven by a confluence of technological advancements and shifting demographic patterns. A dominant trend is the increasing adoption of minimally invasive surgical (MIS) techniques, which reduce patient recovery times, hospital stays, and overall healthcare costs. This shift is fueling demand for specialized MIS-compatible implants and instrumentation, designed for smaller incisions and enhanced precision.

Another significant insight revolves around the evolution of implant materials and designs. The industry is moving towards more biocompatible materials like PEEK and advanced titanium alloys, offering improved integration and reduced risk of adverse reactions. Furthermore, the personalization of implants through 3D printing technology is gaining traction, allowing for patient-specific solutions that enhance surgical outcomes and anatomical fit. This customization capability represents a major leap forward from traditional off-the-shelf devices.

Beyond surgical techniques and materials, the market is also influenced by the integration of digital technologies. Robotics and navigation systems are becoming increasingly commonplace in spinal surgeries, offering unparalleled precision and consistency. The aging global population, coupled with a rising incidence of degenerative spinal conditions, also forms a foundational driver for sustained market growth, necessitating a continuous supply of innovative and effective spinal solutions.

- Growing adoption of Minimally Invasive Surgical (MIS) techniques.

- Advancements in biomaterials and implant design, including PEEK and advanced titanium.

- Increasing personalization of implants via 3D printing technology.

- Integration of robotics and navigation systems for enhanced surgical precision.

- Rising prevalence of degenerative spinal disorders among an aging global demographic.

- Emphasis on expedited patient recovery and reduced hospital stays.

- Expansion of outpatient surgical settings for less complex spinal procedures.

AI Impact Analysis on Spinal Implant and Surgical Device

The integration of Artificial Intelligence (AI) is poised to revolutionize the Spinal Implant and Surgical Device market, addressing common user questions related to precision, efficiency, and patient outcomes. AI algorithms are increasingly being employed in pre-operative planning, enabling surgeons to visualize complex spinal anatomies in 3D, predict surgical outcomes, and plan implant placement with unprecedented accuracy. This leads to reduced intraoperative complications and optimized surgical strategies, directly improving patient safety and efficacy.

Furthermore, AI plays a crucial role in enhancing intraoperative guidance and robotic assistance. AI-powered navigation systems can provide real-time feedback during surgery, adjusting for patient movement and ensuring precise instrument and implant positioning. This minimizes human error and allows for more consistent procedural execution, which is a significant concern for both surgeons seeking reliable tools and patients desiring optimal results. The data generated from these AI-assisted surgeries also feeds back into learning models, perpetually refining diagnostic capabilities and treatment protocols.

Beyond the operating room, AI's impact extends to research and development, accelerating the design and testing of new implant technologies. Predictive analytics can identify patient cohorts most likely to benefit from specific implants, personalize rehabilitation protocols, and even anticipate post-operative complications. While concerns exist regarding data privacy and the ethical implications of autonomous systems, the overarching expectation is that AI will drive significant advancements in spinal care, leading to more personalized, efficient, and successful interventions across the entire patient journey.

- Enhanced pre-operative planning and 3D anatomical modeling using AI.

- Real-time intraoperative guidance and robotic assistance for precision.

- Accelerated research and development of new implant designs and materials.

- Predictive analytics for personalized treatment plans and outcome forecasting.

- Optimization of surgical workflows and reduction of procedural variations.

- Improved diagnostic accuracy and identification of spinal pathologies.

Key Takeaways Spinal Implant and Surgical Device Market Size & Forecast

The Spinal Implant and Surgical Device market is on a robust growth trajectory, driven primarily by an aging global population and the increasing prevalence of spinal disorders, which are common user inquiries related to market expansion. The shift towards less invasive surgical techniques and the continuous introduction of advanced materials and personalized implants are fundamental pillars supporting this growth. These innovations address patient demands for quicker recovery, reduced pain, and improved long-term outcomes, thereby fueling market demand.

Furthermore, technological integration, particularly the burgeoning role of artificial intelligence and robotics, is transforming surgical precision and planning, making complex spinal procedures safer and more effective. This technological adoption, while initially cost-intensive, is expected to yield significant long-term benefits in terms of patient care efficiency and resource utilization. The market's future will be heavily influenced by regulatory frameworks, reimbursement policies, and the ability of manufacturers to innovate while maintaining competitive pricing.

Regional dynamics also play a crucial role, with developed economies in North America and Europe leading in technological adoption and market share due to established healthcare infrastructures. However, emerging economies in Asia Pacific are poised for rapid growth, driven by increasing healthcare expenditure, medical tourism, and a growing awareness of advanced spinal treatments. The overall forecast indicates a sustained and significant expansion of the market, offering substantial opportunities for innovation and market penetration for stakeholders.

- Sustained market growth driven by demographic shifts and rising spinal disorder incidence.

- Minimally invasive techniques and personalized implants are key innovation drivers.

- Technological advancements, including AI and robotics, are enhancing surgical precision.

- North America and Europe currently dominate, with Asia Pacific showing significant growth potential.

- Healthcare expenditure and regulatory landscapes are critical factors influencing market evolution.

- The market is expanding to address the growing demand for effective and less invasive spinal care solutions.

Spinal Implant and Surgical Device Market Drivers Analysis

The Spinal Implant and Surgical Device market is propelled by several potent drivers, primarily the escalating global geriatric population, which is inherently more susceptible to degenerative spinal conditions such as osteoarthritis, disc degeneration, and spinal stenosis. This demographic shift significantly increases the pool of patients requiring surgical intervention. Concurrently, a heightened awareness of spinal health and the availability of advanced diagnostic tools contribute to earlier and more accurate diagnoses, leading to a greater demand for effective treatment solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Global Population & Degenerative Conditions | +2.1% | Global, particularly North America, Europe, Japan | Long-term (2025-2033) |

| Technological Advancements in MIS & Robotics | +1.8% | North America, Europe, Asia Pacific (Tier-1 cities) | Mid to Long-term (2025-2033) |

| Increasing Prevalence of Spinal Deformities | +1.5% | Global, especially emerging economies | Mid to Long-term (2025-2033) |

| Rising Healthcare Expenditure & Reimbursement Policies | +1.2% | Developed economies (US, Germany, UK), gradually emerging markets | Mid-term (2025-2030) |

| Growing Adoption of Personalized Implants (3D Printing) | +0.9% | North America, Europe | Mid to Long-term (2027-2033) |

Spinal Implant and Surgical Device Market Restraints Analysis

Despite the robust growth, the Spinal Implant and Surgical Device market faces several significant restraints that could impede its full potential. The high cost associated with advanced spinal implants and the complex surgical procedures often poses a barrier to adoption, particularly in developing regions with limited healthcare budgets or inadequate insurance coverage. This financial burden can restrict access for a large segment of the patient population, thereby slowing market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Implants & Surgical Procedures | -1.5% | Global, more pronounced in emerging markets | Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -1.0% | North America (FDA), Europe (CE Mark) | Mid to Long-term (2025-2033) |

| Risks of Post-operative Complications & Product Recalls | -0.8% | Global | Ongoing |

| Limited Reimbursement Coverage in Certain Regions | -0.7% | Developing economies, some European countries | Long-term (2025-2033) |

| Preference for Non-Surgical Treatments | -0.5% | Global | Ongoing |

Spinal Implant and Surgical Device Market Opportunities Analysis

Significant opportunities exist within the Spinal Implant and Surgical Device market, driven by unmet medical needs and evolving technological landscapes. The development of bio-resorbable implants, which naturally degrade and are absorbed by the body after serving their purpose, presents a compelling opportunity. These implants eliminate the need for secondary surgeries for removal and may reduce long-term complications, representing a major advancement that can capture a new segment of demand.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-resorbable and Smart Implants | +1.9% | Global, R&D focused regions (NA, EU) | Long-term (2028-2033) |

| Expansion in Emerging Markets (APAC, LATAM) | +1.7% | China, India, Brazil, Southeast Asia | Mid to Long-term (2025-2033) |

| Increasing Adoption of Outpatient Spinal Surgeries | +1.4% | North America, Europe | Mid-term (2025-2030) |

| Strategic Collaborations & Acquisitions by Key Players | +1.1% | Global | Ongoing |

| Growth in Medical Tourism for Spinal Procedures | +0.8% | Asia (India, Thailand), Latin America (Mexico, Costa Rica) | Mid to Long-term (2025-2033) |

Spinal Implant and Surgical Device Market Challenges Impact Analysis

The Spinal Implant and Surgical Device market faces several persistent challenges that demand strategic navigation from industry players. Intense competition among a growing number of manufacturers, coupled with pricing pressures from healthcare providers and payers, represents a significant hurdle. This competitive landscape can drive down profit margins and necessitate continuous innovation to maintain market share, posing a financial strain on companies, particularly smaller enterprises.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition & Pricing Pressures | -1.2% | Global | Ongoing |

| High Entry Barriers for New Players (R&D, Regulatory) | -1.0% | Global | Long-term (2025-2033) |

| Risk of Product Failures & Malpractice Litigation | -0.9% | Global | Ongoing |

| Shortage of Skilled Spinal Surgeons & Support Staff | -0.7% | Global, more pronounced in developing regions | Long-term (2025-2033) |

| Supply Chain Disruptions and Raw Material Volatility | -0.6% | Global | Short to Mid-term (2025-2027) |

Spinal Implant and Surgical Device Market - Updated Report Scope

This report provides a comprehensive analysis of the global Spinal Implant and Surgical Device market, detailing market size, growth drivers, restraints, opportunities, and challenges. It segments the market by product type, material, surgery type, end user, and region, offering a granular view of market dynamics. The report incorporates the impact of emerging technologies like AI and robotics, and profiles key industry players to provide a holistic understanding of the competitive landscape and future outlook.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.5 Billion |

| Market Forecast in 2033 | USD 22.9 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, DePuy Synthes (Johnson & Johnson), Stryker, Zimmer Biomet, NuVasive, Globus Medical, Orthofix Medical Inc., SeaSpine Holdings Corporation, Xtant Medical Holdings Inc., ChoiceSpine LP, Alphatec Holdings Inc. (ATEC), Spineart SA, K2M Group Holdings Inc. (part of Stryker), Aesculap (B. Braun Melsungen AG), RTI Surgical (part of Surgalign Holdings), Centinel Spine, Integra LifeSciences Holdings Corporation, LDR Holding Corporation (part of Zimmer Biomet), ulrich medical, SI-BONE Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Spinal Implant and Surgical Device market is extensively segmented to provide a granular understanding of its diverse components and their respective growth trajectories. These segments are primarily defined by the type of product, the materials used in implant manufacturing, the surgical approach employed, and the end-user facilities where procedures are performed. Each segment exhibits unique demand drivers and market dynamics, reflecting the varied needs within spinal care.

Product segmentation differentiates between spinal fusion devices, which aim to permanently join vertebrae, and non-fusion devices, designed to preserve motion. Within fusion, sub-segments include thoracolumbar and cervical fixation devices, interbody fusion cages, and a broad category of spinal biologics critical for bone regeneration. Non-fusion devices encompass dynamic stabilization systems, artificial discs, and instruments for vertebral compression fracture treatment, catering to different pathological conditions and patient requirements. Surgical navigation and robotics systems, alongside spinal orthotics, represent crucial supportive technologies within the market, enhancing precision and post-operative recovery.

Material-wise, titanium and PEEK continue to dominate due to their excellent biocompatibility and mechanical properties, but bioabsorbable materials are emerging as a promising alternative. The split between open and minimally invasive surgery reflects the ongoing shift towards less traumatic procedures, a key driver for specific device innovation. Finally, end-user segmentation highlights the significance of hospitals as primary hubs for complex spinal surgeries, alongside the growing role of ambulatory surgical centers and specialty clinics for less invasive procedures, emphasizing the evolving landscape of healthcare delivery for spinal conditions.

- By Product Type:

- Spinal Fusion Devices

- Thoracolumbar Devices

- Cervical Fixation Devices

- Interbody Fusion Devices

- Spinal Biologics

- Non-Fusion Devices

- Dynamic Stabilization Devices

- Artificial Discs

- Spinal Cord Stimulation Devices

- Vertebral Compression Fracture (VCF) Devices

- Spinal Bone Stimulators

- Surgical Navigation & Robotics Systems

- Spinal Orthotics and Bracing

- Spinal Fusion Devices

- By Material:

- Titanium and Titanium Alloys

- Polyetheretherketone (PEEK)

- Stainless Steel

- Bioabsorbable Materials

- Bone Grafts

- By Surgery Type:

- Open Surgery

- Minimally Invasive Surgery (MIS)

- By End User:

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

- Research Institutes

Regional Highlights

- North America: Dominates the global Spinal Implant and Surgical Device market due to high prevalence of spinal disorders, well-established healthcare infrastructure, high adoption of advanced technologies (MIS, robotics, 3D printing), substantial healthcare expenditure, and favorable reimbursement policies. The United States is the largest market within this region, driving innovation and market growth.

- Europe: Represents the second largest market, characterized by an aging population and a strong focus on research and development in spinal care. Countries like Germany, France, and the UK are key contributors, benefiting from advanced medical facilities and a robust regulatory environment. However, variations in healthcare systems and reimbursement across countries can influence market dynamics.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate during the forecast period. This growth is attributed to a rapidly expanding patient pool, improving healthcare infrastructure, rising disposable incomes, increasing medical tourism, and growing awareness of advanced spinal treatments. China, Japan, and India are the leading countries in this region, driven by large populations and expanding access to modern medical technologies.

- Latin America: An emerging market for spinal implants and surgical devices, characterized by increasing healthcare investments, growing awareness, and improving economic conditions. Brazil and Mexico are key markets in this region, with a rising demand for both traditional and minimally invasive spinal procedures.

- Middle East and Africa (MEA): Shows gradual growth, primarily driven by increasing healthcare expenditure, development of medical tourism hubs (e.g., UAE, Saudi Arabia), and a rising incidence of lifestyle-related spinal conditions. However, market penetration remains lower compared to developed regions due to varying healthcare access and economic disparities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Spinal Implant and Surgical Device Market.- Medtronic

- DePuy Synthes (Johnson & Johnson)

- Stryker

- Zimmer Biomet

- NuVasive

- Globus Medical

- Orthofix Medical Inc.

- SeaSpine Holdings Corporation

- Xtant Medical Holdings Inc.

- ChoiceSpine LP

- Alphatec Holdings Inc. (ATEC)

- Spineart SA

- K2M Group Holdings Inc. (part of Stryker)

- Aesculap (B. Braun Melsungen AG)

- RTI Surgical (part of Surgalign Holdings)

- Centinel Spine

- Integra LifeSciences Holdings Corporation

- LDR Holding Corporation (part of Zimmer Biomet)

- ulrich medical

- SI-BONE Inc.

Frequently Asked Questions

What is the projected growth rate of the Spinal Implant and Surgical Device Market?

The Spinal Implant and Surgical Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 22.9 billion by 2033.

Which key trends are shaping the Spinal Implant and Surgical Device market?

Key trends include the increasing adoption of minimally invasive surgical (MIS) techniques, advancements in biomaterials and personalized 3D-printed implants, and the integration of robotics and artificial intelligence (AI) for enhanced surgical precision.

How is Artificial Intelligence impacting spinal surgery and implant development?

AI is transforming spinal surgery by improving pre-operative planning, providing real-time intraoperative guidance, and accelerating research and development of new implant designs through predictive analytics. This enhances precision and patient outcomes.

What are the primary drivers for growth in the Spinal Implant and Surgical Device market?

Primary growth drivers include the rising global aging population, increasing prevalence of degenerative spinal disorders, continuous technological advancements in surgical techniques and implant materials, and growing healthcare expenditure.

Which geographical region is expected to lead market growth?

North America currently holds the largest market share, but the Asia Pacific region is anticipated to exhibit the highest growth rate during the forecast period due to expanding healthcare infrastructure and a large patient base.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted