Airless Tire Market

Airless Tire Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705420 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Airless Tire Market Size

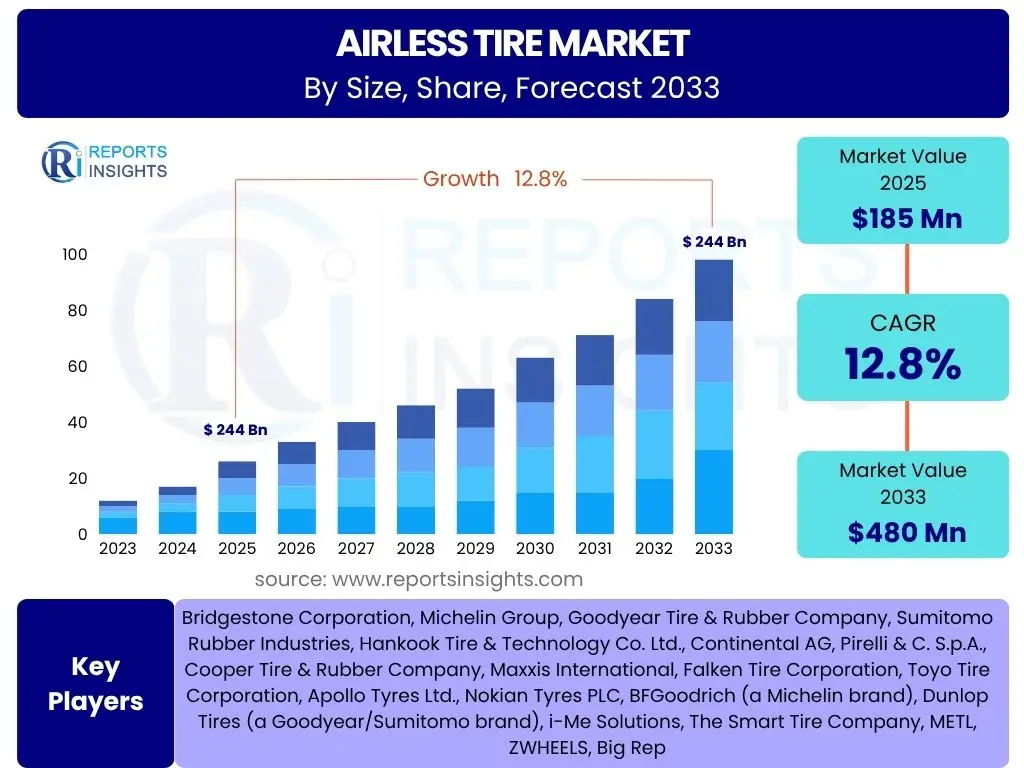

According to Reports Insights Consulting Pvt Ltd, The Airless Tire Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 185 Million in 2025 and is projected to reach USD 480 Million by the end of the forecast period in 2033.

Key Airless Tire Market Trends & Insights

User inquiries about airless tire market trends frequently highlight the shift towards sustainable mobility solutions and the demand for enhanced vehicle performance and safety. A significant trend is the growing interest from major automotive Original Equipment Manufacturers (OEMs) in integrating airless tire technology into their next-generation vehicles, particularly for electric and autonomous platforms. This reflects a strategic move to differentiate products, reduce maintenance, and improve overall vehicle uptime.

Another prominent trend observed is the continuous advancement in material science and manufacturing processes. Researchers and manufacturers are actively developing innovative polymers, composites, and structural designs that address previous limitations such as heat dissipation, ride comfort, and manufacturing complexity. This ongoing material innovation is critical for overcoming technical hurdles and expanding the applicability of airless tires beyond niche markets into mainstream consumer and commercial vehicle segments.

Furthermore, the focus on last-mile delivery and shared mobility services is driving demand for robust, maintenance-free tire solutions. Companies operating large fleets are exploring airless tires to minimize downtime associated with punctures and routine pressure checks, thereby improving operational efficiency. This application-specific adoption is paving the way for broader market acceptance and demonstrating the practical benefits of the technology in high-utilization environments.

- Advancements in material science and structural design, improving performance and durability.

- Increasing integration and testing by major automotive OEMs for future vehicle platforms, especially electric and autonomous.

- Growing adoption in niche applications such as last-mile delivery, shared mobility, and off-road vehicles due to puncture resistance and reduced maintenance.

- Emphasis on sustainability and reduced waste in tire manufacturing and disposal processes.

- Development of smart airless tire solutions incorporating sensors for real-time performance monitoring.

AI Impact Analysis on Airless Tire

Common user questions regarding AI's impact on airless tires revolve around how artificial intelligence can accelerate development, optimize performance, and streamline manufacturing. AI is poised to revolutionize the design phase through generative design and simulation, allowing engineers to rapidly explore thousands of structural configurations and material compositions to achieve optimal strength, flexibility, and heat dissipation properties. This significantly reduces the time and cost associated with traditional iterative prototyping, leading to faster innovation cycles and more efficient product development.

In manufacturing, AI-powered systems can enhance precision and consistency. Machine learning algorithms analyze data from production lines to detect anomalies, predict equipment failures, and optimize parameters for molding, curing, and assembly, thereby minimizing defects and maximizing output. This level of process control is crucial for mass-producing complex airless tire structures with consistent quality, addressing one of the key challenges of scalability.

Furthermore, AI will play a vital role in predictive maintenance and performance monitoring of airless tires once deployed. Integrated sensors within the tires, combined with AI analytics, can provide real-time data on wear, stress, and structural integrity. This allows for proactive maintenance scheduling, extends tire lifespan, and enhances overall vehicle safety by predicting potential issues before they escalate. Such capabilities are particularly appealing for fleet operators and autonomous vehicles, where maximizing uptime and minimizing human intervention are paramount.

- Generative design and simulation powered by AI for optimal structural and material engineering, accelerating R&D.

- AI-driven manufacturing process optimization to enhance precision, consistency, and reduce defects in production.

- Predictive maintenance and real-time performance monitoring through AI analysis of sensor data embedded within airless tires.

- Integration with autonomous vehicle systems for adaptive tire performance and enhanced safety protocols.

- Supply chain optimization and demand forecasting for airless tire components using AI algorithms.

Key Takeaways Airless Tire Market Size & Forecast

User inquiries about key takeaways from the airless tire market forecast consistently highlight the significant growth potential and the drivers underpinning this expansion. The market is positioned for substantial expansion, driven primarily by the pursuit of maintenance-free, puncture-proof, and environmentally sustainable tire solutions across various vehicle segments. The projected double-digit CAGR indicates a strong industry belief in the eventual commercial viability and widespread adoption of this technology, moving it beyond conceptual stages into practical application.

A crucial insight is that initial market penetration is expected to be led by niche and commercial applications where the benefits of airless tires, such as reduced downtime and enhanced safety, offer compelling economic advantages. Sectors like last-mile delivery, off-road vehicles, and autonomous shuttles are serving as crucial proving grounds, building confidence and demonstrating performance in real-world scenarios. This phased adoption strategy is vital for refining the technology and overcoming initial market hesitations before broader consumer market penetration.

The long-term outlook suggests that sustained investment in R&D, coupled with increasing environmental regulations and the ongoing evolution of vehicle technology (especially electric and autonomous vehicles), will continue to fuel market growth. Addressing challenges related to cost parity, performance at high speeds, and consumer perception will be critical for unlocking the full market potential. The market’s trajectory is therefore a testament to the industry’s commitment to innovation and sustainability within the tire sector.

- The Airless Tire Market is poised for significant growth, projected to reach nearly half a billion USD by 2033, indicating strong confidence in its future viability.

- Initial market expansion is largely driven by commercial and specialized applications benefiting from puncture resistance and reduced maintenance requirements.

- Technological advancements in materials and manufacturing processes are critical enablers for market scalability and performance improvement.

- Sustainability initiatives and the growing fleet of electric and autonomous vehicles are key long-term growth accelerators for airless tire adoption.

- Strategic partnerships between tire manufacturers and automotive OEMs are fundamental to bringing airless tire technology to the mainstream market.

Airless Tire Market Drivers Analysis

The airless tire market is being propelled forward by several compelling factors, primarily focusing on enhanced performance, safety, and environmental benefits. The inherent puncture-proof nature of airless tires addresses a common and costly issue for both individual drivers and commercial fleets, significantly reducing downtime and maintenance expenses. This reliability is particularly appealing in high-usage scenarios such as last-mile delivery, public transportation, and industrial operations, where uninterrupted service is paramount.

Furthermore, the growing emphasis on sustainability and circular economy principles is providing a strong tailwind for airless tire development. By eliminating the need for inflation and offering potential for longer lifespans and easier recyclability due to simplified material structures, airless tires align with global efforts to reduce waste and environmental impact. This environmental advantage resonates with eco-conscious consumers and corporations seeking greener operational practices.

Technological advancements in material science, particularly in the development of advanced polymers and composite structures, are overcoming previous limitations related to ride comfort, heat dissipation, and manufacturing complexity. These innovations are making airless tires more viable for a broader range of applications, including passenger vehicles, which demand specific performance characteristics. Simultaneously, the rise of electric and autonomous vehicles, which require durable, low-maintenance, and sensor-integrable components, presents a natural fit for airless tire technology, further accelerating its adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Demand for Puncture-Proof & Low Maintenance Tires | +3.5% | Global, particularly Commercial Fleets (North America, Europe, APAC) | Short to Mid-term (2025-2029) |

| Growing Emphasis on Sustainability & Environmental Benefits | +2.8% | Europe, North America, Japan | Mid to Long-term (2027-2033) |

| Advancements in Material Science & Manufacturing Technologies | +2.3% | Global, particularly R&D Hubs (USA, Germany, Japan) | Ongoing (2025-2033) |

| Rising Adoption in Electric & Autonomous Vehicle Segments | +2.5% | North America, Europe, China | Mid to Long-term (2028-2033) |

| Improved Safety & Reduced Downtime for Commercial Fleets | +1.7% | Global, especially logistics & last-mile delivery markets | Short to Mid-term (2025-2030) |

Airless Tire Market Restraints Analysis

Despite the promising outlook, the airless tire market faces significant restraints that could impede its growth trajectory. One of the primary barriers is the high initial manufacturing cost and complexity compared to traditional pneumatic tires. The intricate designs, specialized materials, and unique production processes required for airless tires often result in higher unit costs, which can deter widespread adoption, especially in price-sensitive consumer markets. Achieving cost parity or a compelling value proposition will be crucial for broader market penetration.

Another major restraint involves performance limitations, particularly concerning heat dissipation, ride comfort, and noise levels at higher speeds. Pneumatic tires excel at absorbing road imperfections and dissipating heat through their air chamber, characteristics that airless tires struggle to replicate without significant design compromises. While progress is being made, ensuring comparable performance across diverse driving conditions, especially for high-speed passenger vehicles, remains a technical challenge that can limit application scope and consumer acceptance.

Furthermore, the absence of standardized testing protocols and regulatory frameworks for airless tires poses a significant hurdle. Unlike pneumatic tires, which have established safety and performance standards globally, airless tires require new benchmarks for evaluation. This lack of standardization can prolong development cycles, complicate certification processes, and create uncertainty for manufacturers and consumers alike. Overcoming these regulatory and technical challenges will be critical for unlocking the full potential of the airless tire market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost & Production Complexity | -2.0% | Global | Short to Mid-term (2025-2030) |

| Performance Limitations (Heat Dissipation, Ride Comfort, Noise) | -1.8% | Global, especially Passenger Vehicle Markets | Mid-term (2026-2031) |

| Lack of Standardized Testing & Regulatory Frameworks | -1.5% | Global, particularly Developed Economies (EU, USA) | Mid to Long-term (2027-2033) |

| Consumer Skepticism & Awareness Barriers | -1.2% | Global Consumer Markets | Short to Mid-term (2025-2029) |

| Challenges in Recycling & End-of-Life Management | -0.8% | Europe, North America | Long-term (2029-2033) |

Airless Tire Market Opportunities Analysis

The airless tire market presents several compelling opportunities for growth and innovation, driven by evolving industry needs and technological advancements. One significant area of opportunity lies in the expanding segments of electric vehicles (EVs) and autonomous vehicles (AVs). EVs benefit from the potential for reduced rolling resistance, which can extend range, while AVs require robust, maintenance-free components to ensure continuous operation without human intervention. Airless tires, with their inherent durability and ability to integrate smart sensor technology, are a natural fit for these emerging mobility solutions, offering a distinct advantage over conventional pneumatic tires.

Furthermore, the growth of the last-mile delivery and shared mobility sectors represents a substantial opportunity. Fleets operating in these segments prioritize uptime and minimal maintenance to maximize profitability. Airless tires, by eliminating the risk of punctures and the need for pressure checks, can significantly reduce operational costs and improve efficiency for these high-utilization vehicles. This application-specific demand is expected to drive early adoption and create a strong foundation for market expansion.

Innovation in material science and manufacturing processes continues to open new avenues for airless tire development. Advancements in polymer composites, additive manufacturing (3D printing), and smart materials allow for the creation of more resilient, lighter, and customizable tire structures. These technological leaps can address current limitations, such as heat management and ride comfort, while also enabling the integration of advanced features like embedded sensors for real-time performance monitoring. Such innovations not only enhance product appeal but also facilitate cost reduction and scalability, paving the way for broader market acceptance.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Potential in Electric & Autonomous Vehicles | +3.0% | North America, Europe, Asia Pacific (China, South Korea) | Mid to Long-term (2027-2033) |

| Expansion into Commercial & Specialized Off-road Applications | +2.5% | Global, particularly developing economies and industrial sectors | Short to Mid-term (2025-2030) |

| Integration of Smart Tire Technologies & Sensors | +2.2% | Global | Mid-term (2026-2031) |

| Development of Cost-Effective Manufacturing Processes | +1.9% | Global, particularly manufacturing hubs | Long-term (2029-2033) |

| Growth in Aftermarket Replacement Segment for Niche Vehicles | +1.5% | Global | Short to Mid-term (2025-2028) |

Airless Tire Market Challenges Impact Analysis

The airless tire market faces several significant challenges that require substantial innovation and strategic effort to overcome. A primary challenge is achieving mass production scalability while simultaneously reducing manufacturing costs to be competitive with conventional pneumatic tires. The complex geometries and specialized materials often used in airless tire construction necessitate advanced manufacturing techniques, which can be expensive and difficult to scale efficiently. Without significant cost reductions, widespread consumer adoption, especially in the cost-sensitive passenger vehicle segment, will remain constrained.

Another critical challenge involves overcoming performance gaps and ensuring consistent reliability across diverse operating conditions. Airless tires must match or exceed the performance of pneumatic tires in areas such as ride comfort, noise reduction, and especially heat dissipation at high speeds. Unlike pneumatic tires that use air to dissipate heat, airless designs require novel structural and material solutions to manage thermal buildup, which is crucial for safety and longevity. Addressing these performance intricacies for various vehicle types and environments is essential for market acceptance.

Furthermore, consumer perception and regulatory hurdles present considerable obstacles. Consumers are accustomed to the feel and maintenance routines of pneumatic tires, and shifting this deeply ingrained perception requires extensive education and demonstrated reliability. Simultaneously, new regulatory frameworks and safety standards need to be established globally for airless tires, a process that can be lengthy and complex. Harmonizing these standards across different regions is vital for manufacturers to confidently enter and expand within various markets.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Mass Production Scalability & Cost Parity with Pneumatic Tires | -2.5% | Global | Short to Mid-term (2025-2030) |

| Achieving Optimal Performance Across All Driving Conditions | -2.0% | Global, particularly high-speed markets | Mid-term (2026-2031) |

| Establishing Industry Standards & Regulatory Approvals | -1.8% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Overcoming Consumer Acceptance & Awareness Barriers | -1.5% | Global Consumer Markets | Short to Mid-term (2025-2029) |

| Integration Challenges with Existing Vehicle Architectures | -1.0% | Global OEMs | Mid-term (2026-2031) |

Airless Tire Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Airless Tire Market, covering historical trends from 2019 to 2023, current market dynamics for 2024, and detailed forecasts from 2025 to 2033. The scope includes an assessment of market size, growth drivers, restraints, opportunities, and challenges influencing industry expansion. It also provides a thorough segmentation analysis by material type, application, vehicle type, and distribution channel, coupled with regional insights across key geographies. The report further examines the competitive landscape, profiling leading companies and their strategic initiatives, alongside an impact analysis of AI on the market. This structure ensures a holistic view for stakeholders seeking strategic insights into the evolving airless tire industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 185 Million |

| Market Forecast in 2033 | USD 480 Million |

| Growth Rate | 12.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bridgestone Corporation, Michelin Group, Goodyear Tire & Rubber Company, Sumitomo Rubber Industries, Hankook Tire & Technology Co. Ltd., Continental AG, Pirelli & C. S.p.A., Cooper Tire & Rubber Company, Maxxis International, Falken Tire Corporation, Toyo Tire Corporation, Apollo Tyres Ltd., Nokian Tyres PLC, BFGoodrich (a Michelin brand), Dunlop Tires (a Goodyear/Sumitomo brand), i-Me Solutions, The Smart Tire Company, METL, ZWHEELS, Big Rep |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Airless Tire Market is comprehensively segmented to provide granular insights into its diverse applications, material compositions, and distribution channels. This segmentation allows for a detailed understanding of where growth opportunities lie and how different market dynamics influence specific sub-segments. By examining the market through these various lenses, stakeholders can identify key areas for investment, product development, and strategic partnerships, tailoring their approaches to specific industry needs and consumer demands.

The segmentation by material highlights the evolving landscape of advanced polymers and composite materials crucial for developing durable, flexible, and high-performance airless tire structures. Application-based segmentation underscores the primary end-use industries driving adoption, from various commercial and passenger vehicles to specialized off-road and recreational segments. This differentiation helps in assessing the market's current focus and potential future expansion into new areas.

Further segmentation by vehicle type and distribution channel provides clarity on whether the market is primarily driven by original equipment manufacturers integrating airless tires into new vehicles or by the aftermarket for replacement and retrofit solutions. Understanding these channels is essential for sales strategies, supply chain management, and partnership development within the airless tire ecosystem. Each segment is characterized by unique technical requirements, regulatory considerations, and market adoption rates, which collectively shape the overall market trajectory.

- By Material:

- Polyurethane: Widely used for its flexibility, durability, and ease of molding.

- Composites: Incorporating various fibers (e.g., carbon fiber, fiberglass) for enhanced strength-to-weight ratio and structural integrity.

- Rubber: Traditional rubber compounds adapted for airless structures, often blended with other materials.

- Others: Including novel elastomers, advanced thermoplastics, and hybrid material combinations.

- By Application:

- Commercial Vehicles:

- Light Commercial Vehicles: For urban logistics and delivery.

- Heavy Commercial Vehicles: For trucking, freight, and public transport.

- Passenger Vehicles: Cars, SUVs, and other personal mobility vehicles.

- Off-Road Vehicles:

- Construction Equipment: Excavators, loaders, dozers.

- Mining Vehicles: Heavy-duty mining trucks and equipment.

- Agricultural Machinery: Tractors, harvesters, farming equipment.

- ATVs/UTVs: All-Terrain Vehicles and Utility Terrain Vehicles.

- Bicycles: Both recreational and professional cycling.

- Others: Robotics, Mobility Scooters, Wheelchairs, Golf Carts, Forklifts, Military Vehicles.

- Commercial Vehicles:

- By Vehicle Type:

- OEM (Original Equipment Manufacturer): Tires fitted on new vehicles directly from the factory.

- Aftermarket: Replacement tires purchased for existing vehicles.

- By Distribution Channel:

- Original Equipment Manufacturers (OEMs): Direct supply to vehicle manufacturers.

- Aftermarket:

- Wholesalers & Distributors: Supplying to retailers and service centers.

- Retailers: Tire shops, auto parts stores, and general merchandise retailers.

- Online: E-commerce platforms and direct-to-consumer sales.

Regional Highlights

- North America: This region is a significant hub for airless tire research and development, driven by substantial investment in automotive innovation, especially in electric and autonomous vehicle technologies. The presence of major tire manufacturers and automotive OEMs, coupled with a strong focus on fleet management efficiency in the logistics sector, makes North America a key early adopter. Consumer awareness and acceptance, particularly in specialized vehicle segments like ATVs and construction equipment, are also contributing to market growth. Stringent safety regulations and the demand for high-performance, durable solutions further bolster the market here.

- Europe: Europe is characterized by a strong emphasis on sustainability, stringent environmental regulations, and a robust automotive industry, all of which are favorable for airless tire adoption. Countries like Germany and France are at the forefront of automotive innovation, with significant R&D activities in tire technology. The push for electric vehicles and circular economy initiatives across the European Union encourages the development and commercialization of eco-friendly and long-lasting tire solutions. Early adoption in niche applications such as urban mobility and light commercial vehicles is notable.

- Asia Pacific (APAC): The APAC region is poised for rapid growth in the airless tire market, driven by its massive automotive production base, increasing vehicle parc, and growing demand for advanced mobility solutions, especially in countries like China, Japan, and South Korea. Rapid urbanization and the expansion of logistics and e-commerce sectors are fueling the demand for maintenance-free and efficient tires. Furthermore, significant investments in smart city infrastructure and autonomous vehicle testing provide fertile ground for the integration of airless tire technology. Government support for electric vehicle adoption also plays a crucial role in accelerating market expansion.

- Latin America: While currently a smaller market, Latin America presents significant long-term growth potential due to increasing industrialization, expanding commercial vehicle fleets, and rising disposable incomes leading to higher passenger vehicle sales. The region's diverse terrain and often challenging road conditions make puncture-proof solutions particularly appealing for both commercial and personal use. As economic development continues and awareness of advanced tire technologies grows, the adoption of airless tires is expected to gradually increase, especially in sectors prioritizing durability and reduced operational costs.

- Middle East and Africa (MEA): The MEA region is experiencing growth in infrastructure development, mining, and logistics, creating a demand for robust and reliable tire solutions. Countries in the Gulf Cooperation Council (GCC) are investing heavily in smart cities and diversified economies, which could eventually integrate advanced vehicle technologies, including airless tires. Extreme climatic conditions and challenging terrains in parts of Africa and the Middle East highlight the need for puncture-resistant tires, offering a niche but growing market for airless solutions in industrial and off-road applications. Economic diversification and foreign investments are expected to slowly pave the way for broader adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Airless Tire Market.- Bridgestone Corporation

- Michelin Group

- Goodyear Tire & Rubber Company

- Sumitomo Rubber Industries

- Hankook Tire & Technology Co. Ltd.

- Continental AG

- Pirelli & C. S.p.A.

- Cooper Tire & Rubber Company

- Maxxis International

- Falken Tire Corporation

- Toyo Tire Corporation

- Apollo Tyres Ltd.

- Nokian Tyres PLC

- BFGoodrich (a Michelin brand)

- Dunlop Tires (a Goodyear/Sumitomo brand)

- i-Me Solutions

- The Smart Tire Company

- METL

- ZWHEELS

- Big Rep

Frequently Asked Questions

Analyze common user questions about the Airless Tire market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are airless tires?

Airless tires are innovative vehicle tires designed to operate without compressed air, eliminating the risk of punctures and maintaining structural integrity through a unique spoke or web design. They consist of a rigid hub, a shear band, and an outer tread, providing support and cushioning without the need for inflation.

What are the main benefits of airless tires?

The primary benefits of airless tires include their puncture-proof nature, which enhances safety and eliminates downtime due to flats. They also offer reduced maintenance requirements, potential for longer lifespan, and contribute to sustainability by reducing material waste and enabling easier recycling. Their consistent performance also improves vehicle uptime for fleets.

What are the challenges in adopting airless tires?

Key challenges for airless tire adoption involve high manufacturing costs and production complexity, which impact affordability. Performance limitations at high speeds, particularly concerning heat dissipation, ride comfort, and noise, are also significant. Additionally, the lack of standardized testing protocols and consumer skepticism pose hurdles to widespread market acceptance.

What vehicles are currently using or testing airless tires?

Airless tires are currently being tested and adopted in various niche and commercial applications. These include off-road vehicles like construction and agricultural machinery, ATVs/UTVs, golf carts, and some last-mile delivery vehicles. Major automotive OEMs are also actively testing them for integration into future electric and autonomous passenger vehicles.

When will airless tires be widely available for consumer vehicles?

While airless tires are already available for select specialized applications, their widespread availability for mainstream consumer vehicles is anticipated within the next 5-10 years. This timeline depends on continued advancements in manufacturing processes to reduce costs, improvements in high-speed performance, the establishment of global regulatory standards, and increased consumer acceptance through successful pilot programs and education.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted