Unfinished Paper Market

Unfinished Paper Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705421 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

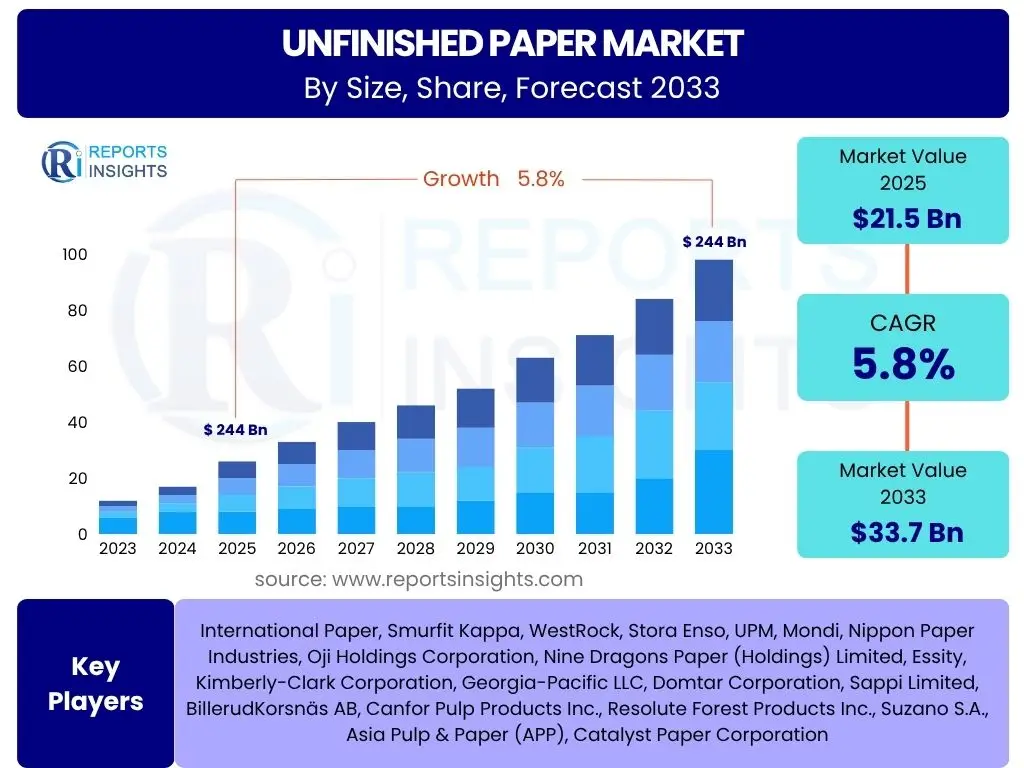

Unfinished Paper Market Size

According to Reports Insights Consulting Pvt Ltd, The Unfinished Paper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 21.5 Billion in 2025 and is projected to reach USD 33.7 Billion by the end of the forecast period in 2033.

Key Unfinished Paper Market Trends & Insights

The Unfinished Paper Market is undergoing significant transformations driven by evolving consumer preferences, technological advancements, and a heightened focus on sustainability. A primary trend involves the increasing demand for eco-friendly and recyclable paper products, which is influencing manufacturing processes and raw material sourcing. Manufacturers are investing in sustainable forestry practices and developing products with a reduced environmental footprint to meet regulatory requirements and consumer expectations. This shift is not merely a compliance issue but a strategic imperative for market differentiation and long-term viability.

Another crucial insight is the diversification of applications for unfinished paper. While traditional uses in packaging and printing remain significant, there is a notable expansion into specialty papers for medical, industrial, and innovative packaging solutions. This diversification helps mitigate risks associated with the decline in certain print media segments, opening new revenue streams. Furthermore, the market is experiencing consolidation, with major players acquiring smaller ones to enhance production capacities, expand geographic reach, and acquire specialized technologies, leading to a more concentrated competitive landscape.

- Growing emphasis on sustainable and recycled content in paper products.

- Expansion of unfinished paper applications into diverse specialty sectors.

- Increased adoption of advanced manufacturing technologies for efficiency and quality.

- Regional shifts in production and consumption, particularly towards Asia Pacific.

- Consolidation among key market players to optimize supply chains and market share.

AI Impact Analysis on Unfinished Paper

Artificial Intelligence (AI) is set to significantly reshape the Unfinished Paper Market by enhancing operational efficiency, optimizing supply chains, and improving product quality. In manufacturing, AI-powered predictive maintenance can monitor machinery in real-time, anticipating failures before they occur. This reduces downtime, extends equipment lifespan, and lowers operational costs, directly impacting the profitability of paper mills. AI algorithms can also optimize production parameters, such as pulp consistency and drying temperatures, leading to higher quality paper output with less waste and improved resource utilization.

Beyond the factory floor, AI is instrumental in demand forecasting and inventory management. By analyzing vast datasets including historical sales, economic indicators, and seasonal trends, AI can predict future demand for various types of unfinished paper with greater accuracy. This enables manufacturers to optimize production schedules, minimize excess inventory, and respond more agilely to market fluctuations, thereby reducing storage costs and preventing stockouts. Furthermore, AI can enhance supply chain transparency and efficiency by optimizing logistics, raw material procurement, and distribution networks, leading to a more resilient and responsive paper industry.

- Predictive maintenance for reduced machinery downtime and enhanced operational efficiency.

- Optimized production processes through AI-driven quality control and resource management.

- Enhanced demand forecasting and inventory management for improved supply chain resilience.

- Automated quality inspection systems for consistent product standards and reduced defects.

- AI-powered logistics and route optimization for cost-effective distribution of paper products.

Key Takeaways Unfinished Paper Market Size & Forecast

The Unfinished Paper Market is poised for steady growth through 2033, driven primarily by robust demand from the packaging sector, particularly fueled by the expansion of e-commerce. Despite the digital shift impacting print media, the indispensable nature of paper in various industrial and consumer applications ensures sustained market vitality. Stakeholders should recognize the critical role of sustainable practices, as environmental consciousness increasingly influences purchasing decisions and regulatory frameworks. Investment in eco-friendly production methods and recycled content will be pivotal for competitive advantage and long-term market relevance.

Furthermore, the market's trajectory is heavily influenced by regional economic growth and industrial development, with Asia Pacific expected to be a key growth engine due to its expanding manufacturing base and rising consumer disposable incomes. Companies seeking to capitalize on this growth must adopt flexible strategies that encompass technological advancements, supply chain optimization, and a keen understanding of diverse regional demands. Strategic collaborations and mergers will likely continue as companies seek to consolidate market share, streamline operations, and enhance their global footprint, making a proactive approach to partnerships essential for market participants.

- Consistent growth projected for the Unfinished Paper Market, driven by packaging and industrial demand.

- Sustainability and circular economy principles are critical for future market competitiveness.

- Asia Pacific is anticipated to be a primary region for market expansion and investment.

- Technological adoption and operational efficiency are key to navigating market dynamics.

- Strategic mergers and acquisitions are shaping the competitive landscape.

Unfinished Paper Market Drivers Analysis

The Unfinished Paper Market is significantly propelled by several key drivers that reinforce its foundational role in global industries. The burgeoning e-commerce sector, for instance, has created an unprecedented demand for protective packaging materials, a substantial portion of which is derived from unfinished paper. This surge in online retail directly translates into increased consumption of paperboard and corrugated materials. Concurrently, a heightened global awareness regarding environmental sustainability is driving a shift away from single-use plastics towards paper-based alternatives, particularly in the packaging and food service industries, thereby expanding the market's addressable opportunities.

Moreover, the steady growth in global population and urbanization, particularly in emerging economies, continues to fuel demand for consumer goods that require paper-based packaging, as well as for hygiene products like tissue paper. Industrial applications, ranging from construction materials to automotive components, also rely heavily on various forms of unfinished paper, contributing to a diversified demand base. Lastly, ongoing innovations in paper manufacturing, leading to enhanced strength, durability, and specialized properties, enable paper to compete effectively with alternative materials, further reinforcing its market position.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of E-commerce and Packaging Demand | +1.5% | Global, particularly North America, APAC, Europe | Short to Mid-term (2025-2030) |

| Increasing Demand for Sustainable Packaging Solutions | +1.2% | Europe, North America, Developing Economies | Mid to Long-term (2025-2033) |

| Population Growth and Urbanization | +0.8% | Asia Pacific, Latin America, MEA | Long-term (2028-2033) |

| Expansion of Industrial Applications | +0.7% | Global | Mid-term (2026-2031) |

Unfinished Paper Market Restraints Analysis

Despite robust growth drivers, the Unfinished Paper Market faces several significant restraints that could impede its expansion. The pervasive trend of digitalization and the increasing adoption of paperless technologies across various sectors, including office environments, education, and banking, directly reduce the demand for printing and writing paper. This shift, while environmentally beneficial, poses a continuous challenge to a substantial segment of the unfinished paper market. Furthermore, stringent environmental regulations concerning deforestation, industrial emissions, and water usage impose considerable compliance costs on manufacturers, which can affect production capacity and profitability, especially for mills in regions with strict environmental policies.

Another major restraint is the volatile pricing of raw materials, particularly wood pulp, which is influenced by global supply-demand dynamics, weather patterns, and trade policies. Fluctuations in pulp prices can significantly impact manufacturing costs and profit margins for paper producers. Additionally, intense competition from alternative packaging materials, such as plastics, glass, and metals, particularly in sectors where durability and specific barrier properties are paramount, continues to exert pressure on market share. While sustainability concerns are shifting preferences, the functional advantages and cost-effectiveness of these alternatives remain a competitive factor.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digitalization and Paperless Trends | -1.0% | Global, particularly Developed Economies | Continuous |

| Stringent Environmental Regulations | -0.7% | Europe, North America, China | Continuous |

| Volatile Raw Material Prices (Wood Pulp) | -0.5% | Global | Short to Mid-term (2025-2029) |

| Competition from Alternative Packaging Materials | -0.4% | Global | Continuous |

Unfinished Paper Market Opportunities Analysis

Significant opportunities are emerging within the Unfinished Paper Market, primarily driven by the expanding scope of sustainable solutions and innovative product development. The growing global emphasis on circular economy principles presents a substantial opportunity for increased recycling of paper and cardboard, reducing reliance on virgin pulp and lowering production costs. This includes advancements in de-inking technologies and the development of new uses for recycled fibers. Furthermore, the rising consumer preference for eco-friendly products creates a niche for specialized papers with enhanced biodegradability or compostability, opening new high-value segments for manufacturers.

Beyond recycling, the development of smart packaging solutions, integrating features like RFID tags, QR codes, or sensors into paper-based packaging, represents a frontier for innovation. This allows for enhanced traceability, anti-counterfeiting measures, and interactive consumer experiences, significantly adding value to traditional paper products. Moreover, the vast untapped potential in emerging markets, particularly in Southeast Asia, Africa, and Latin America, where industrialization and consumerism are rapidly advancing, offers significant growth avenues. As these regions develop infrastructure and increase manufacturing output, the demand for basic and specialized unfinished paper products is set to surge, providing opportunities for market expansion and investment.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Recycling and Circular Economy Initiatives | +1.0% | Europe, North America, Asia Pacific | Mid to Long-term (2026-2033) |

| Development of Sustainable and Biodegradable Paper Products | +0.9% | Global | Continuous |

| Innovation in Smart and Functional Packaging | +0.8% | Developed Economies | Mid-term (2027-2032) |

| Expansion into Untapped Emerging Markets | +0.7% | Asia Pacific, Latin America, MEA | Long-term (2028-2033) |

Unfinished Paper Market Challenges Impact Analysis

The Unfinished Paper Market faces several complex challenges that demand strategic responses from industry participants. Supply chain disruptions, often triggered by geopolitical tensions, natural disasters, or global health crises, can severely impact the availability and cost of raw materials and disrupt the timely delivery of finished products. Such disruptions create volatility and unpredictability, affecting production schedules and market stability. Furthermore, escalating energy costs, a significant component of paper manufacturing, pose a constant challenge to profitability. Energy-intensive processes, from pulping to drying, mean that fluctuations in electricity and fuel prices directly impact the operational viability of paper mills globally.

Another pressing challenge is effective waste management and environmental compliance. While sustainability presents opportunities, the increasing volume of paper waste and the strict regulations surrounding industrial effluents and emissions necessitate substantial investments in waste treatment and pollution control technologies. Labor shortages, particularly skilled labor for operating advanced machinery and maintaining complex production lines, represent an additional hurdle. This issue is exacerbated by an aging workforce in some regions and a lack of new talent entering the industry, potentially leading to increased labor costs or operational inefficiencies. Addressing these challenges requires sustained innovation, strategic partnerships, and adaptable business models to maintain competitiveness in a dynamic global market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Volatility | -0.8% | Global | Short to Mid-term (2025-2029) |

| Rising Energy Costs and Resource Scarcity | -0.6% | Global | Continuous |

| Waste Management and Environmental Compliance Burden | -0.5% | Europe, North America, Asia Pacific | Continuous |

| Labor Shortages and Workforce Skill Gaps | -0.4% | Developed Economies | Long-term (2027-2033) |

Unfinished Paper Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Unfinished Paper Market, offering a detailed analysis of its size, growth trajectory, and key influencing factors. It provides an in-depth examination of market segments, regional performance, and the competitive landscape, incorporating insights from primary and secondary research. The report aims to furnish stakeholders with actionable intelligence to make informed strategic decisions regarding market entry, product development, and geographic expansion within the unfinished paper sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.5 Billion |

| Market Forecast in 2033 | USD 33.7 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | International Paper, Smurfit Kappa, WestRock, Stora Enso, UPM, Mondi, Nippon Paper Industries, Oji Holdings Corporation, Nine Dragons Paper (Holdings) Limited, Essity, Kimberly-Clark Corporation, Georgia-Pacific LLC, Domtar Corporation, Sappi Limited, BillerudKorsnäs AB, Canfor Pulp Products Inc., Resolute Forest Products Inc., Suzano S.A., Asia Pulp & Paper (APP), Catalyst Paper Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Unfinished Paper Market is extensively segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a detailed analysis of demand patterns, supply chain intricacies, and competitive positioning across various product types and end-use applications. Understanding these distinct segments is crucial for identifying specific growth opportunities and tailoring strategies to meet the nuanced requirements of different industries.

The segmentation by type typically includes major categories such as pulp, paperboard, packaging paper, newsprint, and specialty paper, each serving unique purposes within the industrial and consumer landscape. Pulp, as the fundamental raw material, is further broken down into bleached and unbleached variants, reflecting different processing levels and end-product characteristics. Similarly, segmentation by application or end-use highlights the diverse sectors reliant on unfinished paper, ranging from the vast packaging industry to the specific demands of printing, hygiene, and various industrial uses, allowing for targeted market analysis and strategic planning by market participants.

- By Type:

- Pulp (Bleached Pulp, Unbleached Pulp)

- Paperboard

- Packaging Paper

- Newsprint

- Specialty Paper

- Others (e.g., Kraft Paper, Coated Paper)

- By Application/End-Use:

- Packaging (Corrugated Boxes, Folding Cartons, Flexible Packaging)

- Printing & Writing (Publishing, Office & Commercial)

- Tissue & Hygiene (Toilet Paper, Paper Towels, Facial Tissues, Napkins)

- Industrial (Construction, Automotive, Electrical & Electronics)

- Consumer Goods

- Other Applications

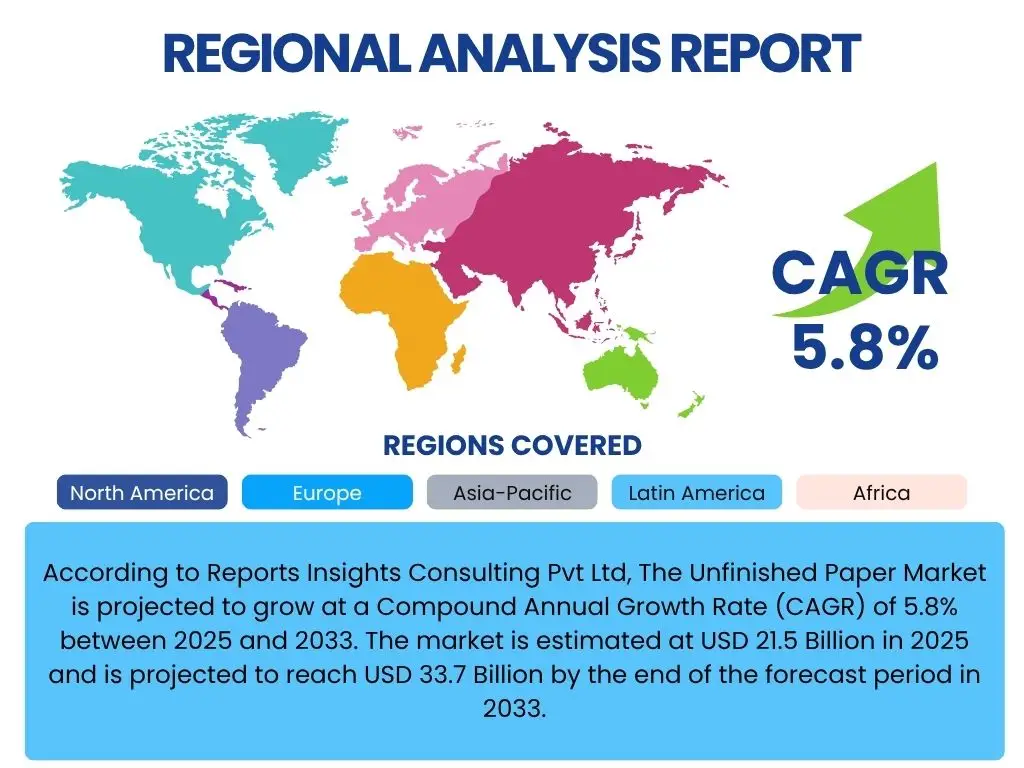

Regional Highlights

The Unfinished Paper Market exhibits distinct regional dynamics, influenced by varying economic conditions, consumer preferences, regulatory environments, and industrial development levels. Asia Pacific, particularly China and India, stands out as a primary growth engine. This region benefits from rapid urbanization, expanding manufacturing capabilities, a booming e-commerce sector, and a large consumer base, driving significant demand for packaging, tissue, and industrial papers. Investments in new capacities and technological upgrades are prevalent here to meet the escalating regional consumption.

North America and Europe represent mature markets characterized by a strong emphasis on sustainability, recycling, and high-value specialty papers. While traditional print media may see declining demand, the focus shifts to advanced packaging solutions, circular economy initiatives, and innovative paper products. These regions also lead in adopting advanced manufacturing technologies and adhering to stringent environmental standards. Latin America and the Middle East & Africa are emerging markets with considerable potential, driven by infrastructure development, rising disposable incomes, and increasing industrialization, offering opportunities for market expansion and the establishment of new production facilities.

- Asia Pacific: Dominant market share and highest growth, driven by China, India, and Southeast Asian economies due to massive manufacturing, e-commerce boom, and rising consumption of packaged goods and tissue products.

- North America: Mature market with stable demand, strong focus on sustainable and specialized paper products, significant consumption in packaging and hygiene sectors, and technological innovation.

- Europe: Emphasis on circular economy, high recycling rates, stringent environmental regulations, growing demand for sustainable packaging, and innovation in paper-based solutions across various applications.

- Latin America: Emerging market with increasing industrialization and consumer base, driven by growth in packaging and tissue sectors, and significant natural resource availability.

- Middle East & Africa (MEA): Developing market with increasing investments in infrastructure and manufacturing, growing demand for basic paper products and packaging, and reliance on imports for specialized grades.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Unfinished Paper Market.- International Paper

- Smurfit Kappa

- WestRock

- Stora Enso

- UPM

- Mondi

- Nippon Paper Industries

- Oji Holdings Corporation

- Nine Dragons Paper (Holdings) Limited

- Essity

- Kimberly-Clark Corporation

- Georgia-Pacific LLC

- Domtar Corporation

- Sappi Limited

- BillerudKorsnäs AB

- Canfor Pulp Products Inc.

- Resolute Forest Products Inc.

- Suzano S.A.

- Asia Pulp & Paper (APP)

- Catalyst Paper Corporation

Frequently Asked Questions

What is unfinished paper?

Unfinished paper refers to paper in its raw or intermediate state before undergoing final processing, coating, or conversion into consumer products. It includes various forms like pulp, paperboard, packaging paper, newsprint, and specialty base papers that serve as raw materials for a wide range of end-use applications.

What are the primary drivers of growth in the Unfinished Paper Market?

Key growth drivers include the booming e-commerce sector driving demand for packaging materials, increasing consumer preference for sustainable and eco-friendly packaging alternatives over plastics, global population growth, and the expansion of industrial applications that require various forms of paper and paperboard.

How is sustainability influencing the Unfinished Paper Market?

Sustainability is a major influence, driving manufacturers to adopt eco-friendly production processes, increase the use of recycled content, source from certified sustainable forests, and develop biodegradable paper products. This shift responds to both consumer demand and stringent environmental regulations, creating new market opportunities.

What impact does digitalization have on the Unfinished Paper Market?

Digitalization primarily impacts the printing and writing paper segments, leading to a decline in demand for office paper, newsprint, and publishing paper as more activities shift online. However, it simultaneously fuels demand for packaging paper due to the growth of e-commerce, creating a mixed effect on the overall market.

What is the market forecast for unfinished paper through 2033?

The Unfinished Paper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 33.7 Billion by the end of the forecast period. This growth is primarily driven by expanding packaging demand and increasing sustainability initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted