Iron Ore Pellet Market

Iron Ore Pellet Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705528 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

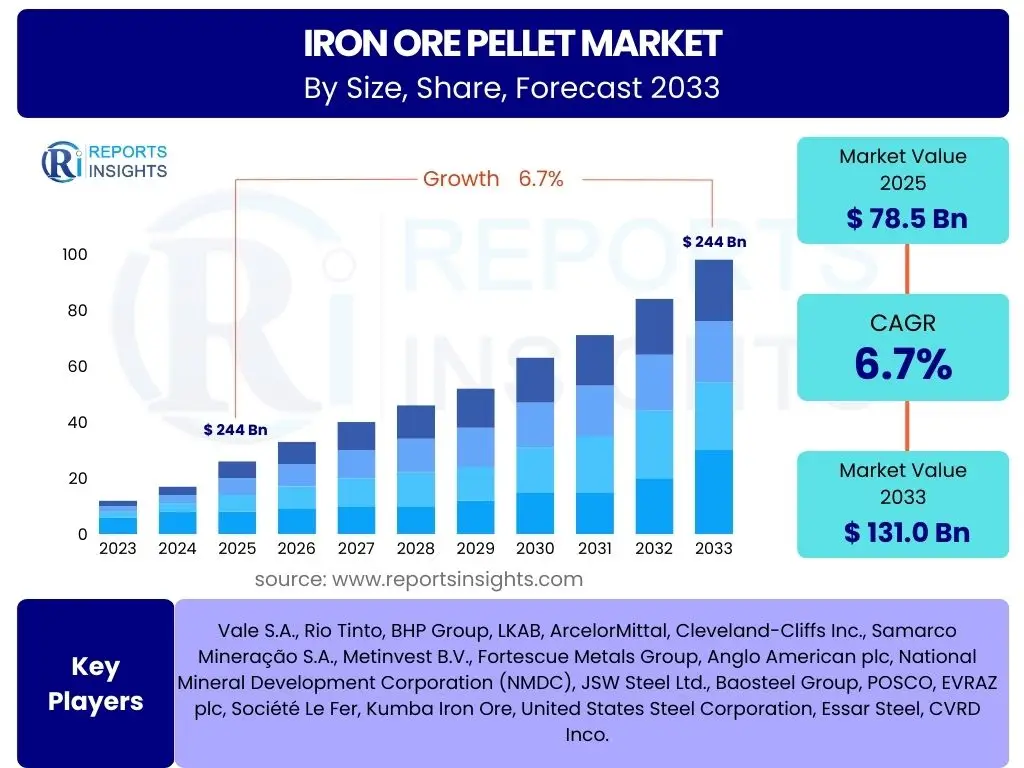

Iron Ore Pellet Market Size

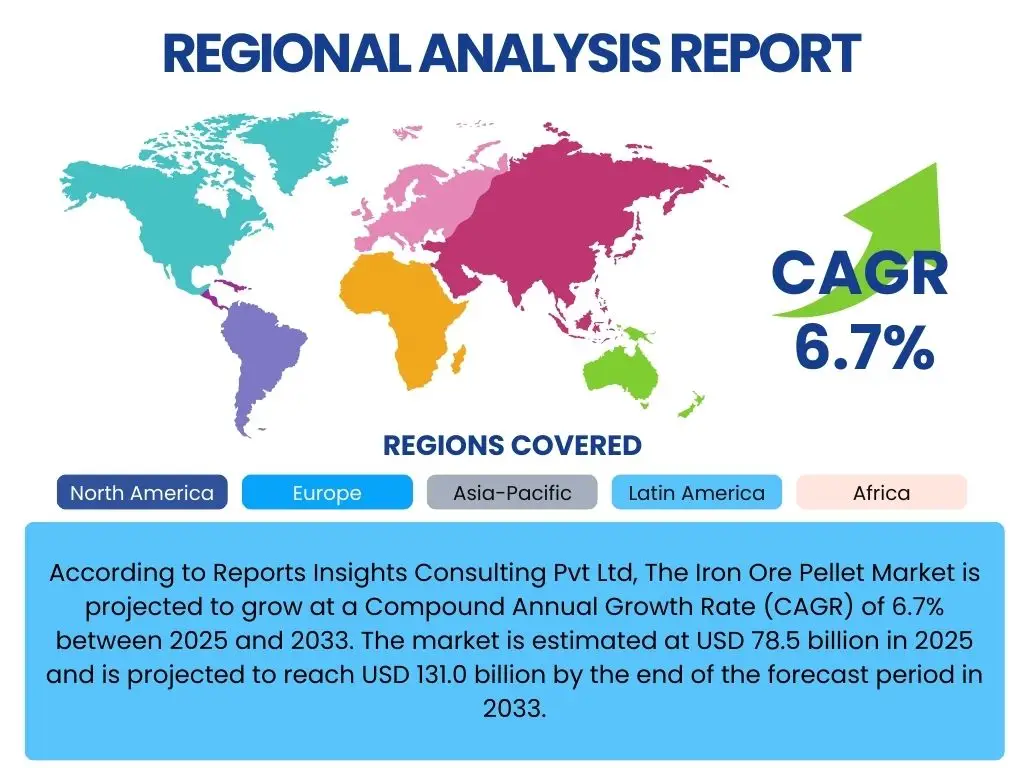

According to Reports Insights Consulting Pvt Ltd, The Iron Ore Pellet Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 78.5 billion in 2025 and is projected to reach USD 131.0 billion by the end of the forecast period in 2033.

Key Iron Ore Pellet Market Trends & Insights

The iron ore pellet market is undergoing significant transformations driven by evolving steelmaking practices and an increased focus on environmental sustainability. A prominent trend is the rising demand for high-grade iron ore pellets, particularly Direct Reduced (DR) grade pellets, as steelmakers increasingly adopt greener production methods like Direct Reduced Iron (DRI) and Electric Arc Furnaces (EAFs) to reduce carbon emissions. This shift is prompted by stringent global environmental regulations and a growing industry commitment to decarbonization, moving away from traditional blast furnace steel production that relies heavily on sinter and lump ore.

Technological advancements in pelletization processes are also shaping the market. Innovations are focused on improving efficiency, reducing energy consumption, and enhancing the quality of pellets to meet the specific requirements of modern steel plants. Furthermore, the market is observing a trend towards greater integration across the steel value chain, with some major steel producers investing in their own pelletizing facilities to ensure a stable supply of high-quality raw materials and optimize operational costs. Supply chain resilience, following recent global disruptions, is also a key area of focus, leading to diversification of sourcing strategies and emphasis on regional supply security.

- Increasing adoption of Direct Reduced Iron (DRI) and Electric Arc Furnaces (EAFs) for steel production.

- Growing demand for high-grade and ultra-low impurity iron ore pellets.

- Stringent environmental regulations driving demand for cleaner steelmaking inputs.

- Technological advancements in pelletization for energy efficiency and quality enhancement.

- Emphasis on supply chain resilience and diversification of raw material sources.

AI Impact Analysis on Iron Ore Pellet

Artificial intelligence is poised to significantly impact the iron ore pellet industry by revolutionizing various stages from mining and beneficiation to pelletization and logistics. Users are keen to understand how AI can enhance operational efficiency and resource optimization. AI-powered predictive maintenance, for instance, can prevent equipment breakdowns in pelletizing plants, minimizing downtime and optimizing production schedules. Furthermore, AI algorithms can analyze vast datasets from ore processing to optimize the blend of raw materials, improving pellet quality and consistency while reducing energy consumption during the induration process.

The application of AI extends to supply chain management, where it can provide real-time insights into logistics, inventory levels, and demand forecasting, leading to more efficient transportation and reduced holding costs for pellets. Quality control is another area where AI can make substantial improvements; AI-driven vision systems can inspect pellets for defects, ensuring that only high-quality products reach the market, thereby enhancing customer satisfaction and reducing waste. While the initial investment in AI infrastructure can be substantial, the long-term benefits in terms of cost reduction, operational efficiency, and improved product quality are expected to drive its widespread adoption within the iron ore pellet sector.

- Optimized raw material blending and quality control through AI-driven analytics.

- Enhanced predictive maintenance for pelletizing equipment, reducing downtime.

- Improved supply chain efficiency and logistics management using AI for forecasting and routing.

- Automated process control in pellet plants leading to energy savings and increased yield.

- Better resource utilization and environmental monitoring through AI data interpretation.

Key Takeaways Iron Ore Pellet Market Size & Forecast

The iron ore pellet market is set for robust growth over the forecast period, primarily driven by the global steel industry's ongoing shift towards more sustainable and cleaner production methods. This transformation is creating a persistent demand for high-quality iron ore inputs, particularly pellets, which offer superior characteristics for modern steelmaking technologies like DRI and EAF. The market's expansion is not merely quantitative but also qualitative, reflecting a pivot towards premium grades that support lower carbon footprints in steel production.

Geographically, emerging economies, particularly in Asia Pacific, will continue to be significant demand centers due to rapid industrialization and urbanization. However, developed regions will also contribute to growth through their commitment to green steel initiatives and technological upgrades in existing facilities. The future trajectory of the market will be significantly influenced by continuous innovation in pelletizing technology, effective management of raw material price volatility, and the industry's collective efforts to meet increasingly stringent environmental mandates, all contributing to a dynamic yet promising outlook for iron ore pellets.

- Consistent growth propelled by the global shift towards green steel technologies.

- Increasing preference for high-grade DR pellets over traditional iron ore forms.

- Asia Pacific remains a dominant and growing market due to strong industrial development.

- Technological advancements and environmental compliance are critical factors influencing market direction.

- The market is adapting to sustainability demands, driving innovation and new investment.

Iron Ore Pellet Market Drivers Analysis

The iron ore pellet market is primarily propelled by the burgeoning global demand for steel, particularly from industries undergoing rapid infrastructure development and urbanization. As countries continue to invest in construction, automotive, and manufacturing sectors, the need for steel, and consequently, its primary raw material, iron ore pellets, escalates. This fundamental demand is further amplified by the global steel industry's strategic shift towards cleaner production technologies. The push for decarbonization and the adoption of Direct Reduced Iron (DRI) and Electric Arc Furnace (EAF) processes, which rely heavily on high-quality iron ore pellets, are significant market drivers.

Moreover, the superior characteristics of iron ore pellets, such as their uniform size, high iron content, and low impurities, make them an ideal feedstock for these modern steelmaking methods. This preference over traditional forms like lump ore or sinter contributes to the sustained demand for pellets. Technological advancements in pelletization processes, aimed at improving energy efficiency and environmental performance, also act as drivers by making pellet production more economically viable and environmentally compliant, encouraging further market penetration.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Steel Demand & Infrastructure Development | +1.5% | Asia Pacific (China, India), Latin America, Middle East | Long-term (5+ years) |

| Shift Towards Green Steel Production (DRI/EAF) | +1.2% | Europe, North America, Japan, South Korea | Mid-term to Long-term (3-7 years) |

| Superior Quality & Efficiency of Pellets in Steelmaking | +0.8% | Global | Continuous |

| Technological Advancements in Pelletization | +0.7% | Global | Mid-term (3-5 years) |

| Favorable Environmental Regulations (Lower Emissions) | +0.9% | Europe, China, India | Mid-term to Long-term (4-8 years) |

Iron Ore Pellet Market Restraints Analysis

Despite robust growth prospects, the iron ore pellet market faces several significant restraints that could impede its expansion. One primary concern is the volatility in raw material prices, particularly iron ore fines and coal, which are essential inputs for pellet production. Fluctuations in these commodity prices directly impact production costs, affecting profit margins for pellet manufacturers and potentially leading to higher end-product prices for steelmakers, which can dampen demand. The capital-intensive nature of setting up and operating pelletizing plants also acts as a substantial barrier to entry for new players, limiting market competition and potentially slowing innovation.

Furthermore, stringent environmental regulations, while simultaneously driving demand for cleaner steelmaking, also pose a challenge for pellet producers. Compliance with emission standards, waste management protocols, and water usage limits requires significant investment in pollution control technologies and operational adjustments, increasing overall production costs. Logistical challenges, including transportation costs and infrastructure limitations, particularly in landlocked regions or developing economies, can also restrain market growth by increasing the cost of delivering pellets to end-users and limiting access to certain markets. Geopolitical instability and trade disputes can further disrupt supply chains, creating uncertainty and impacting market stability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Iron Ore Fines, Coal) | -0.8% | Global | Short-term to Mid-term (2-5 years) |

| High Energy Costs for Pelletization | -0.7% | Europe, Asia Pacific (Energy Import Dependent) | Mid-term (3-5 years) |

| Stringent Environmental Regulations on Production | -0.6% | Europe, China, India | Long-term (5+ years) |

| High Capital Expenditure for Plant Setup | -0.5% | Global (New Entrants) | Long-term (5+ years) |

| Logistical Challenges & Transportation Costs | -0.4% | Developing Regions, Remote Mining Locations | Continuous |

Iron Ore Pellet Market Opportunities Analysis

The iron ore pellet market is presented with significant opportunities arising from the global imperative for steel industry decarbonization. The growing adoption of green steel technologies, particularly Direct Reduced Iron (DRI) production paired with Electric Arc Furnaces (EAFs), creates a sustained and increasing demand for high-quality, low-impurity iron ore pellets. This shift offers manufacturers an opportunity to specialize in premium DR-grade pellets, which command higher prices and cater to environmentally conscious steel producers seeking to reduce their carbon footprint. The development of innovative pelletizing technologies that offer enhanced energy efficiency and lower emissions during production further opens avenues for competitive advantage and market expansion.

Emerging economies, particularly in Southeast Asia, Africa, and parts of Latin America, represent untapped potential as their industrialization and infrastructure development accelerate. These regions are expected to drive new demand for steel, and consequently for iron ore pellets, as they build out their industrial capacities. Furthermore, the potential for using alternative energy sources (such as biomass or hydrogen) in pellet induration processes presents a long-term opportunity for manufacturers to further reduce their carbon footprint and appeal to a broader market segment focused on sustainability. Investments in expanding existing pelletizing capacities and establishing new facilities in proximity to growing demand centers or iron ore reserves can capitalize on these market dynamics.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for DR-Grade Pellets in Green Steel Production | +1.3% | Europe, North America, Japan, South Korea, China | Long-term (5+ years) |

| Emerging Markets Industrialization & Urbanization | +1.0% | Southeast Asia, India, Africa, Latin America | Long-term (5+ years) |

| Development of Energy-Efficient & Sustainable Pelletizing Technologies | +0.9% | Global | Mid-term (3-6 years) |

| Adoption of Alternative Fuels (e.g., Hydrogen, Biomass) in Production | +0.8% | Europe, North America | Long-term (7+ years) |

| Strategic Partnerships & Vertical Integration in Supply Chain | +0.7% | Global | Mid-term to Long-term (4-8 years) |

Iron Ore Pellet Market Challenges Impact Analysis

The iron ore pellet market faces a range of challenges that necessitate strategic responses from industry participants. One significant challenge is the volatile nature of global iron ore prices, which directly affects the cost of raw materials for pellet production. Unpredictable price swings can erode profit margins and complicate long-term investment planning for pellet manufacturers. Furthermore, ensuring a stable and reliable supply of high-quality iron ore fines, the primary input for pellets, can be challenging due to geological complexities, operational disruptions at mines, or geopolitical factors impacting supply chains. This supply uncertainty can lead to production bottlenecks and affect market stability.

Meeting increasingly stringent environmental regulations while maintaining cost-effectiveness is another prominent challenge. Pelletizing plants are energy-intensive and have environmental footprints that require continuous investment in advanced pollution control technologies and sustainable practices. The high capital expenditure required for facility upgrades and new plant construction, coupled with long payback periods, poses a barrier to entry and expansion. Additionally, securing a skilled workforce capable of operating and maintaining complex pelletizing machinery, as well as managing advanced process controls, presents an ongoing human resource challenge for the industry. Navigating these complexities requires robust risk management strategies and a commitment to technological innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Global Iron Ore Prices & Supply Uncertainty | -0.9% | Global | Short-term to Mid-term (2-5 years) |

| Stringent Environmental & Emissions Regulations Compliance | -0.7% | Europe, China, India, North America | Long-term (5+ years) |

| High Operational Costs (Energy & Logistics) | -0.6% | Global | Continuous |

| Technological Obsolescence & Need for Continuous Innovation | -0.5% | Global | Mid-term (3-7 years) |

| Skilled Labor Shortages & Workforce Development | -0.4% | Global | Long-term (5+ years) |

Iron Ore Pellet Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global iron ore pellet market, offering detailed insights into its size, growth trajectory, key trends, and influencing factors. It covers a historical period of market performance and provides robust forecasts, segmenting the market by various parameters including grade, application, and process type. The report meticulously identifies and evaluates the market's drivers, restraints, opportunities, and challenges, providing a holistic view of the industry landscape. Furthermore, it features a thorough regional analysis and profiles of key industry players, offering strategic intelligence for stakeholders. The scope also includes an assessment of the impact of emerging technologies such as AI on the market's future.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 78.5 Billion |

| Market Forecast in 2033 | USD 131.0 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Vale S.A., Rio Tinto, BHP Group, LKAB, ArcelorMittal, Cleveland-Cliffs Inc., Samarco Mineração S.A., Metinvest B.V., Fortescue Metals Group, Anglo American plc, National Mineral Development Corporation (NMDC), JSW Steel Ltd., Baosteel Group, POSCO, EVRAZ plc, Société Le Fer, Kumba Iron Ore, United States Steel Corporation, Essar Steel, CVRD Inco. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global iron ore pellet market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segmentations are critical for identifying specific market niches, understanding demand patterns, and assessing competitive landscapes. The primary segmentation is by grade, differentiating between Blast Furnace (BF) grade pellets, primarily used in traditional blast furnace steelmaking, and Direct Reduction (DR) grade pellets, which are crucial for the rapidly growing direct reduced iron production route that supports greener steel initiatives. The increasing preference for DR-grade pellets reflects the industry's shift towards sustainable practices.

Further segmentation by application highlights the dominant role of steel production, broken down by specific furnace types such as blast furnaces and DRI-EAF combinations, showcasing the evolving consumption patterns. End-user segmentation provides insight into the primary consumers of pellets, distinguishing between integrated steel plants and dedicated DRI/EAF facilities. Finally, segmentation by process type, including Grate-Kiln, Straight Grate, and Shaft Furnace methods, reveals the technological preferences and efficiencies within the pelletization industry. Each segment contributes uniquely to the market dynamics, influenced by regional steel production trends, technological adoption rates, and environmental regulations.

- By Grade:

- Blast Furnace (BF) Grade

- Direct Reduction (DR) Grade

- By Application:

- Steel Production

- Blast Furnace

- DRI-EAF

- Other Metallurgical Applications

- Steel Production

- By End-User:

- Integrated Steel Plants

- Direct Reduced Iron (DRI) Plants

- Electric Arc Furnaces (EAF)

- By Process:

- Grate-Kiln

- Straight Grate

- Shaft Furnace

- Others

Regional Highlights

- Asia Pacific (APAC): Dominates the global iron ore pellet market, driven by robust steel production in China and India. Rapid industrialization, extensive infrastructure development, and a growing emphasis on greener steel production methods are fueling demand for high-grade pellets. Countries like Japan and South Korea also contribute significantly due to their advanced steel industries and focus on DRI technology.

- Europe: A significant market characterized by stringent environmental regulations and a strong push towards decarbonization in the steel industry. This region is a leading adopter of green steel technologies, driving the demand for DR-grade pellets. Countries like Germany, Sweden, and Russia (as a key producer and consumer) are pivotal.

- North America: Experiencing stable growth, particularly with the modernization of its steel industry and increasing adoption of Electric Arc Furnaces (EAFs) and Direct Reduced Iron (DRI) plants. The focus on domestic supply chains and premium quality steel production contributes to the demand for high-quality iron ore pellets.

- Latin America: A major producer and exporter of iron ore fines and pellets, notably Brazil. The region's market dynamics are influenced by global steel demand and internal infrastructure projects. While a significant supply hub, domestic consumption also contributes to regional market growth.

- Middle East and Africa (MEA): Emerging as a crucial region for DRI production, especially in the Middle East, due to abundant natural gas reserves, which is a key reductant for DRI. This drives substantial demand for DR-grade iron ore pellets. Africa, with its vast iron ore reserves, holds long-term potential for both production and consumption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Iron Ore Pellet Market.- Vale S.A.

- Rio Tinto

- BHP Group

- LKAB

- ArcelorMittal

- Cleveland-Cliffs Inc.

- Samarco Mineração S.A.

- Metinvest B.V.

- Fortescue Metals Group

- Anglo American plc

- National Mineral Development Corporation (NMDC)

- JSW Steel Ltd.

- Baosteel Group

- POSCO

- EVRAZ plc

- Société Le Fer

- Kumba Iron Ore

- United States Steel Corporation

- Essar Steel

- CVRD Inco

Frequently Asked Questions

What is an iron ore pellet and how is it used?

Iron ore pellets are small, spherical agglomerates of iron ore fines, typically 8-18 mm in diameter, produced through a process called pelletization. They are a crucial raw material in steelmaking, particularly favored for their uniform size, high iron content, and low impurity levels, making them ideal for blast furnaces and especially for Direct Reduced Iron (DRI) plants, which are key to greener steel production.

Why is the demand for iron ore pellets increasing?

The increasing demand for iron ore pellets is primarily driven by the global steel industry's shift towards sustainable and low-carbon production methods, such as Direct Reduced Iron (DRI) and Electric Arc Furnaces (EAFs). These technologies require high-quality, uniform raw materials, which pellets efficiently provide. Additionally, global infrastructure development and urbanization continue to fuel overall steel demand.

What are the key drivers of the Iron Ore Pellet Market?

Key drivers include the rising global demand for steel, particularly from construction and automotive sectors; the steel industry's transition to greener production technologies like DRI and EAF; the superior quality and efficiency of pellets in steelmaking processes; and continuous technological advancements in pelletization that improve efficiency and reduce environmental impact.

How do environmental regulations impact the Iron Ore Pellet Market?

Environmental regulations significantly impact the market by both presenting challenges and creating opportunities. While stringent emission standards and waste management protocols increase production costs for pellet manufacturers, they also drive the demand for high-quality, low-impurity pellets that enable steelmakers to comply with stricter environmental mandates and reduce their carbon footprint.

What is the future outlook for the Iron Ore Pellet Market?

The future outlook for the iron ore pellet market is robust and positive. It is expected to grow steadily, propelled by the persistent global demand for steel and the accelerating adoption of sustainable steelmaking technologies. Innovation in pelletization processes, focus on supply chain resilience, and growth in emerging economies will further shape and expand the market.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted