Zirconium Tube Market

Zirconium Tube Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704024 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Zirconium Tube Market Size

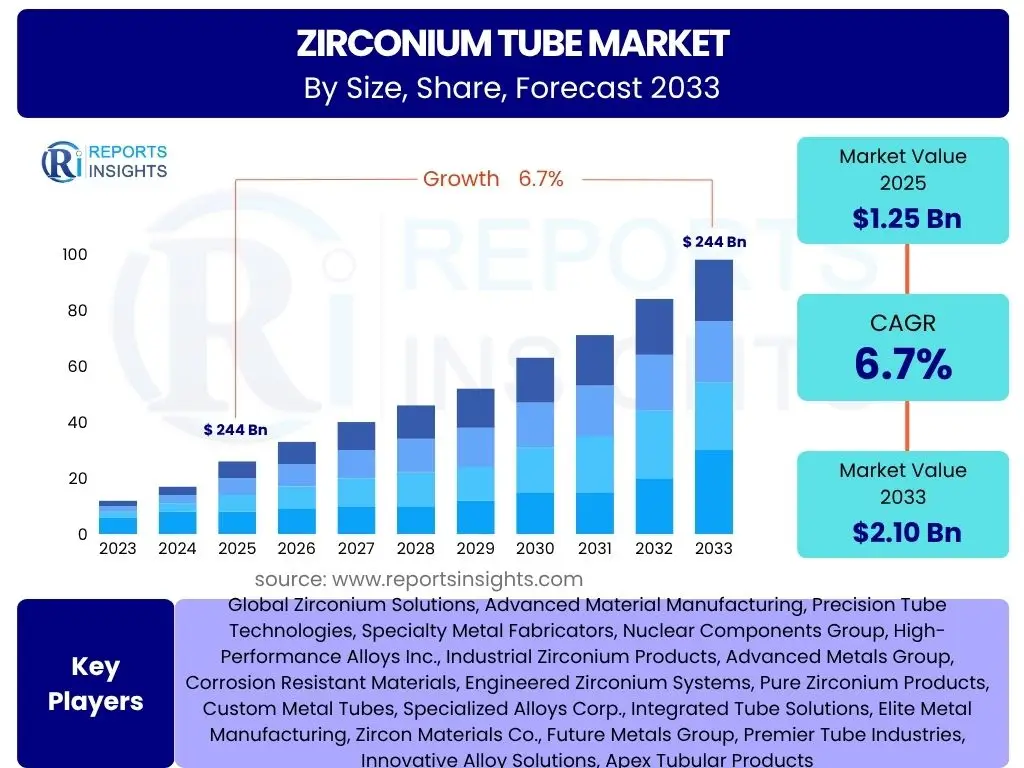

According to Reports Insights Consulting Pvt Ltd, The Zirconium Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.10 Billion by the end of the forecast period in 2033.

Key Zirconium Tube Market Trends & Insights

The Zirconium Tube market is experiencing significant evolution driven by advancements in nuclear energy, particularly the development of Small Modular Reactors (SMRs), and increasing demand from high-precision industries. User inquiries often highlight the shift towards enhanced material specifications for extreme environments and the growing emphasis on sustainable manufacturing practices. Key trends indicate a robust demand from sectors requiring superior corrosion resistance, high neutron transparency, and thermal stability.

Furthermore, there is a discernible trend towards custom fabrication and specialized alloys to meet the stringent requirements of advanced applications such as medical implants and sophisticated chemical processing units. The integration of advanced manufacturing techniques, including additive manufacturing for complex geometries, is also gaining traction, promising greater design flexibility and reduced material waste. This focus on high-performance materials and innovative production methods underscores the market's trajectory towards higher value-added applications and tailored solutions.

- Increasing demand from nuclear power generation, particularly for next-generation reactors and SMRs.

- Growing adoption in critical industrial applications requiring high corrosion resistance, such as chemical processing and pharmaceuticals.

- Development of specialized zirconium alloys for enhanced performance in extreme environments.

- Technological advancements in manufacturing processes leading to higher purity and more precise tube dimensions.

- Rising focus on material traceability and quality assurance across the supply chain.

- Expansion of medical and aerospace applications due to zirconium's biocompatibility and strength-to-weight ratio.

AI Impact Analysis on Zirconium Tube

Common user questions regarding AI's influence on the Zirconium Tube market typically revolve around optimizing manufacturing processes, enhancing quality control, and improving supply chain efficiency. Users are interested in how artificial intelligence can mitigate the complexities associated with producing high-purity, precision-engineered tubes and reduce operational costs. The primary expectation is that AI will introduce new levels of automation and predictive capabilities, ultimately leading to more consistent product quality and faster production cycles.

AI's role extends to predictive maintenance for manufacturing equipment, optimizing material usage, and improving defect detection through advanced image processing and machine learning algorithms. Furthermore, AI can aid in the discovery of new zirconium alloys by simulating material properties and performance under various conditions, significantly accelerating research and development cycles. This transformative potential positions AI as a crucial enabler for innovation and operational excellence within the specialized Zirconium Tube manufacturing sector.

- AI-driven optimization of melting, extrusion, and pilgering processes for improved efficiency and reduced waste.

- Enhanced quality control through machine learning algorithms for defect detection and material purity analysis.

- Predictive maintenance for manufacturing equipment, minimizing downtime and increasing production throughput.

- Supply chain optimization using AI for demand forecasting, inventory management, and logistics.

- Accelerated material research and development through AI-powered simulation and design of new zirconium alloys.

- Improved data analysis for performance monitoring and continuous improvement in Zirconium Tube production.

Key Takeaways Zirconium Tube Market Size & Forecast

The Zirconium Tube market is poised for steady growth, primarily fueled by the sustained global demand for nuclear energy and the expansion of specialized industrial applications. User inquiries often highlight the market's resilience in the face of economic fluctuations, driven by the indispensable nature of zirconium tubes in critical infrastructure and advanced technological sectors. The forecast indicates a stable increase in market valuation, reflecting ongoing investments in nuclear power plants and an escalating need for high-performance materials across diverse industries.

A significant takeaway is the market's trajectory towards increased complexity and customization, necessitating advanced manufacturing capabilities and stringent quality control. The projected growth underscores the strategic importance of zirconium tubes in energy security and technological innovation, cementing its status as a critical component in the global industrial landscape. The emphasis on long-term project lifecycles, particularly in nuclear and chemical processing, provides a foundational stability to the market's growth projections.

- The market is projected to achieve a CAGR of 6.7% from 2025 to 2033, indicating stable expansion.

- Nuclear power remains the primary growth driver, with significant investments in new reactor builds and SMRs.

- Diversification into chemical processing, medical, and aerospace industries contributes to market resilience.

- Technological advancements in manufacturing and material science are crucial for meeting evolving demands.

- Long-term contracts and stringent quality requirements characterize a mature yet expanding market.

- Regional demand disparities influence overall market dynamics, with Asia Pacific and North America leading.

Zirconium Tube Market Drivers Analysis

The global increase in nuclear power generation capacity stands as the foremost driver for the Zirconium Tube market. Zirconium alloys, particularly Zircaloy, are indispensable for fuel rod cladding due to their low neutron absorption cross-section, high corrosion resistance, and excellent mechanical properties under extreme reactor conditions. The ongoing construction of new nuclear power plants, alongside the modernization and life extension of existing facilities worldwide, directly translates to a consistent and growing demand for zirconium tubes. Furthermore, the development and deployment of Small Modular Reactors (SMRs) are anticipated to open new avenues for market expansion, offering a more flexible and scalable approach to nuclear energy deployment.

Beyond nuclear applications, the chemical processing industry represents another significant driver. Zirconium's exceptional resistance to various corrosive chemicals, including strong acids and alkalis, makes zirconium tubes ideal for heat exchangers, condensers, and piping systems in harsh chemical environments. Industries such as phosphoric acid production, acetic acid distillation, and urea synthesis heavily rely on zirconium components to ensure operational safety and longevity. This persistent demand from the chemical sector, driven by the need for durable and reliable equipment in highly corrosive settings, continues to bolster the Zirconium Tube market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Nuclear Power Expansion (New Builds & SMRs) | +2.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Increasing Demand from Chemical Processing Industry | +1.8% | Asia Pacific, Europe, Middle East | 2025-2033 |

| Technological Advancements in Zirconium Alloys | +1.2% | North America, Europe, Japan | 2027-2033 |

| Growing Applications in Medical & Aerospace Sectors | +0.8% | North America, Europe | 2026-2033 |

| Emphasis on Energy Security & Clean Energy | +0.4% | Global | 2025-2033 |

Zirconium Tube Market Restraints Analysis

The high cost associated with zirconium raw materials and the complex manufacturing processes involved in producing high-quality tubes pose a significant restraint on market growth. Zirconium is not as abundant as other industrial metals, and its extraction and purification are energy-intensive, leading to elevated material costs. Furthermore, the specialized manufacturing techniques required for zirconium tubes, such as vacuum melting, hot extrusion, cold pilgering, and extensive quality control measures, contribute to higher production expenses. These elevated costs can make zirconium tubes less competitive against alternative materials in applications where extreme conditions are not paramount, thereby limiting their broader adoption and potentially slowing market expansion, particularly in cost-sensitive segments.

Another critical restraint is the stringent regulatory environment governing the nuclear industry, which is a primary end-user for zirconium tubes. The highly regulated nature of nuclear power generation necessitates extensive testing, certification, and compliance with rigorous international safety standards. This not only adds to the manufacturing lead times and costs but also creates significant barriers to entry for new players, thus concentrating market power among a few established manufacturers. While essential for safety, these regulatory hurdles can impede innovation and rapid market response to evolving demands, acting as a decelerating factor for growth within the nuclear segment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Raw Materials & Manufacturing | -1.5% | Global | 2025-2033 |

| Strict Regulatory & Certification Requirements | -1.0% | Global, particularly Nuclear Nations | 2025-2033 |

| Availability of Alternative Materials (e.g., Titanium, Stainless Steel) | -0.7% | Global | 2025-2030 |

| Limited Number of Specialized Manufacturers | -0.5% | Global | 2025-2033 |

| Environmental Concerns & Waste Management | -0.3% | Developed Nations | 2028-2033 |

Zirconium Tube Market Opportunities Analysis

The increasing global emphasis on clean energy initiatives presents a significant opportunity for the Zirconium Tube market. As nations strive to reduce carbon emissions and transition away from fossil fuels, nuclear power is gaining renewed attention as a reliable, baseload, and low-carbon energy source. This resurgence includes not only the construction of new large-scale reactors but, more importantly, the accelerated development and deployment of Small Modular Reactors (SMRs) and advanced reactor designs. These next-generation technologies promise enhanced safety features, modular construction, and smaller footprints, potentially democratizing nuclear energy and expanding its global reach. The widespread adoption of SMRs would lead to a substantial and sustained demand for zirconium tubes for fuel cladding and other critical components, offering a long-term growth trajectory for the market.

Furthermore, the diversification of zirconium tube applications beyond the traditional nuclear sector represents a compelling opportunity. Industries such as hydrogen production, where zirconium tubes can serve in high-temperature electrolysis or storage systems due to their corrosion resistance and strength, are emerging as new demand centers. The medical sector is also exploring zirconium for advanced surgical instruments and biocompatible implants, leveraging its non-toxicity and durability. Similarly, the aerospace and defense industries are finding niche applications for zirconium tubes in high-performance systems where lightweight and robust materials are essential. These expanding application areas allow market players to mitigate reliance on a single sector and tap into new, high-growth segments, thereby enhancing market stability and potential for innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Small Modular Reactors (SMRs) & Advanced Reactors | +2.0% | North America, Europe, Asia Pacific | 2027-2033 |

| Expansion into New Industrial Applications (Hydrogen, Desalination) | +1.5% | Global | 2028-2033 |

| Demand for Zirconium in Medical Implants & Devices | +1.0% | North America, Europe | 2026-2033 |

| Focus on Material Innovation & Customization | +0.8% | Global | 2025-2033 |

| Increased Investment in Research & Development for Zirconium Alloys | +0.7% | Global | 2025-2033 |

Zirconium Tube Market Challenges Impact Analysis

One of the primary challenges confronting the Zirconium Tube market is the volatility in the supply chain for raw materials, particularly zirconium sponge. The production of high-purity zirconium is concentrated in a limited number of countries, making the supply vulnerable to geopolitical tensions, trade policies, and unexpected production disruptions. Any instability in the supply of raw zirconium can lead to price fluctuations, increased lead times, and potential shortages for manufacturers of zirconium tubes. This supply chain fragility can significantly impact production schedules and costs, posing a considerable risk to the stability and profitability of market players, especially given the long-term, critical nature of many zirconium tube applications.

Another significant challenge stems from the requirement for highly specialized manufacturing expertise and a skilled labor force. The production of zirconium tubes, especially for nuclear applications, involves intricate processes that demand a deep understanding of metallurgy, precise engineering, and rigorous quality control. There is a limited pool of experienced professionals proficient in these specialized manufacturing techniques, leading to potential labor shortages and increased training costs for companies. Moreover, attracting and retaining this specialized talent can be difficult, hindering production capacity expansion and the adoption of new technologies. This expertise gap represents a critical bottleneck that could impede the market's ability to scale effectively to meet future demand.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Volatility & Raw Material Price Fluctuations | -1.2% | Global | 2025-2030 |

| Requirement for Highly Specialized Manufacturing Expertise | -1.0% | Global | 2025-2033 |

| Intense Competition from Alternative Materials | -0.8% | Global | 2025-2033 |

| High Capital Investment for Production Facilities | -0.6% | Global | 2025-2030 |

| Disposal & Environmental Regulations for Nuclear Waste | -0.4% | Developed Nations | 2028-2033 |

Zirconium Tube Market - Updated Report Scope

This report provides a comprehensive analysis of the Zirconium Tube market, encompassing historical data, current market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The aim is to deliver actionable insights for stakeholders to make informed strategic decisions in this specialized industrial sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.10 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Zirconium Solutions, Advanced Material Manufacturing, Precision Tube Technologies, Specialty Metal Fabricators, Nuclear Components Group, High-Performance Alloys Inc., Industrial Zirconium Products, Advanced Metals Group, Corrosion Resistant Materials, Engineered Zirconium Systems, Pure Zirconium Products, Custom Metal Tubes, Specialized Alloys Corp., Integrated Tube Solutions, Elite Metal Manufacturing, Zircon Materials Co., Future Metals Group, Premier Tube Industries, Innovative Alloy Solutions, Apex Tubular Products |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Zirconium Tube market is comprehensively segmented based on various attributes to provide a granular understanding of its dynamics and opportunities. These segmentations are critical for identifying specific market niches, understanding demand patterns, and developing targeted strategies. The segmentation by type differentiates between seamless and welded tubes, each serving distinct application requirements based on structural integrity and cost-efficiency. Seamless tubes typically dominate high-pressure and critical applications due to their uniform strength and absence of weld seams, while welded tubes offer cost advantages for less demanding uses.

Further segmentation by application highlights the diverse utility of zirconium tubes across critical industries. Nuclear power generation remains the largest segment, driven by the essential role of zirconium in fuel cladding and reactor components. However, the growing adoption in chemical processing, medical, and aerospace sectors underscores the material's versatile properties, including exceptional corrosion resistance and biocompatibility. Analyzing these segments provides insights into industry-specific growth drivers and technological requirements, informing product development and market penetration strategies. The market also segments by purity, diameter, and wall thickness, which are crucial specifications dictating performance and suitability for highly specialized and demanding environments.

- By Type: Seamless, Welded

- By Application: Nuclear Power Generation, Chemical Processing, Medical, Aerospace & Defense, Other Industrial Applications

- By Purity: High Purity, Standard Purity

- By Diameter: Small Diameter, Medium Diameter, Large Diameter

- By Wall Thickness: Thin Wall, Medium Wall, Thick Wall

Regional Highlights

- North America: A major market driven by significant investments in nuclear power plant modernization and the development of SMRs. The region also exhibits strong demand from the chemical processing, aerospace, and advanced medical device sectors due to stringent regulatory standards and technological leadership. High R&D expenditure and a robust industrial base contribute to its market share.

- Europe: Characterized by a strong emphasis on clean energy and a mature nuclear industry, contributing to consistent demand. Countries like France, the UK, and Eastern European nations are significant consumers. The region also boasts a sophisticated chemical processing industry and a growing focus on high-performance materials for specialized applications. Environmental regulations often drive demand for corrosion-resistant materials.

- Asia Pacific (APAC): The fastest-growing region, primarily propelled by aggressive expansion in nuclear power capacity, especially in China, India, and South Korea. Rapid industrialization, increasing energy demand, and growing investments in chemical manufacturing and infrastructure development are key drivers. The region is emerging as a critical hub for both production and consumption of zirconium tubes.

- Latin America: Showing nascent growth in nuclear energy projects and an expanding chemical industry. While currently a smaller market, increasing industrialization and foreign investments in energy infrastructure are expected to drive future demand for specialized materials like zirconium tubes.

- Middle East and Africa (MEA): Growing interest in nuclear power for energy diversification and water desalination projects, particularly in countries like UAE and Saudi Arabia. Investments in chemical and petrochemical industries also contribute to the demand for corrosion-resistant materials, indicating potential for steady market expansion in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Zirconium Tube Market.- Global Zirconium Solutions

- Advanced Material Manufacturing

- Precision Tube Technologies

- Specialty Metal Fabricators

- Nuclear Components Group

- High-Performance Alloys Inc.

- Industrial Zirconium Products

- Advanced Metals Group

- Corrosion Resistant Materials

- Engineered Zirconium Systems

- Pure Zirconium Products

- Custom Metal Tubes

- Specialized Alloys Corp.

- Integrated Tube Solutions

- Elite Metal Manufacturing

- Zircon Materials Co.

- Future Metals Group

- Premier Tube Industries

- Innovative Alloy Solutions

- Apex Tubular Products

Frequently Asked Questions

What is the projected growth rate for the Zirconium Tube market?

The Zirconium Tube market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033, reaching an estimated value of USD 2.10 Billion by 2033.

Which industries primarily drive the demand for Zirconium Tubes?

The primary drivers for Zirconium Tube demand are the nuclear power generation industry (for fuel rod cladding and structural components) and the chemical processing industry (for corrosion-resistant heat exchangers and piping).

How do Small Modular Reactors (SMRs) impact the Zirconium Tube market?

SMRs are a significant opportunity, expected to drive future demand for zirconium tubes due to their role in next-generation nuclear energy solutions, offering flexible and scalable power generation.

What are the main challenges faced by the Zirconium Tube market?

Key challenges include high raw material costs, supply chain volatility, complex and specialized manufacturing processes, and stringent regulatory requirements, particularly within the nuclear sector.

In which regions is the Zirconium Tube market experiencing the most significant growth?

The Asia Pacific (APAC) region is experiencing the most significant growth, driven by extensive investments in new nuclear power plants and rapid industrial expansion in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted