Bimetallic Tube Market

Bimetallic Tube Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703320 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

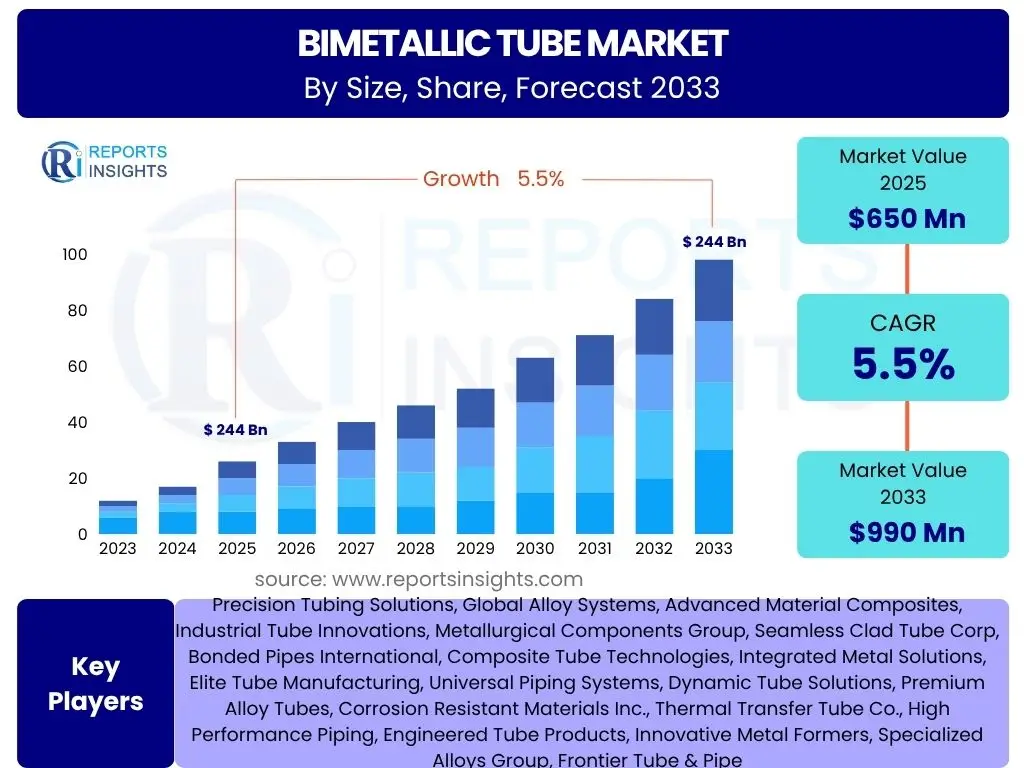

Bimetallic Tube Market Size

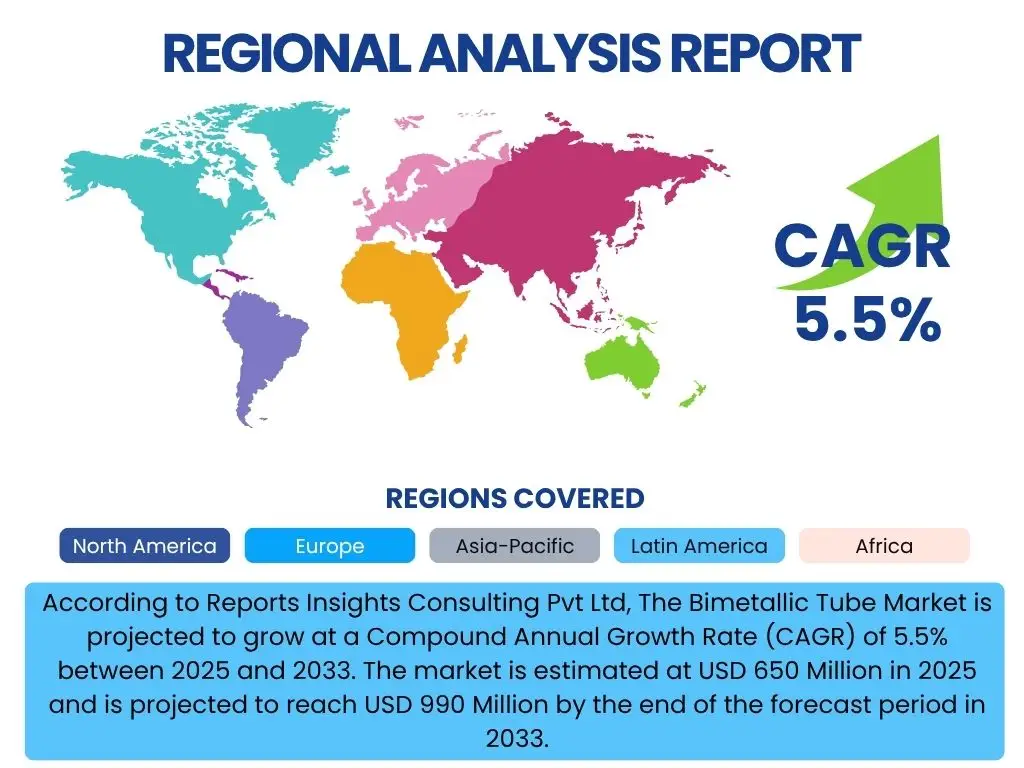

According to Reports Insights Consulting Pvt Ltd, The Bimetallic Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 650 Million in 2025 and is projected to reach USD 990 Million by the end of the forecast period in 2033.

Key Bimetallic Tube Market Trends & Insights

The bimetallic tube market is experiencing significant evolution driven by industrial demands for enhanced material performance and longevity in corrosive or high-temperature environments. A prominent trend is the increasing adoption of these tubes in critical infrastructure projects, particularly within the energy and chemical processing sectors. Innovations in manufacturing techniques, such as advanced co-extrusion and explosion bonding, are enabling the production of tubes with superior metallurgical bonds and tighter tolerances, expanding their applicability to more demanding conditions. Furthermore, there is a growing emphasis on sustainable manufacturing practices and the development of bimetallic solutions that offer longer service life, thereby reducing material consumption and waste over time.

Another key insight is the expanding material combination portfolio, moving beyond traditional carbon steel/stainless steel pairings to include more exotic alloys like titanium, nickel, and super duplex steels as liners. This diversification addresses highly specific corrosive media and extreme thermal loads encountered in specialized applications like hydrogen production, advanced nuclear reactors, and deep-sea oil and gas exploration. The market is also witnessing a trend towards customization, where bimetallic tubes are engineered to meet precise performance specifications for individual projects, rather than relying solely on standard sizes and compositions. This shift is fueled by the need for optimized solutions that balance performance, cost, and lifespan for critical industrial assets.

- Increasing demand from burgeoning energy sectors, including renewables and hydrogen infrastructure.

- Technological advancements in co-extrusion and explosion bonding enhancing bond integrity and performance.

- Diversification of material combinations to address increasingly severe operating environments.

- Growing focus on life cycle cost reduction through extended service life and reduced maintenance.

- Rise in demand for customized bimetallic solutions tailored to specific project requirements.

AI Impact Analysis on Bimetallic Tube

Artificial Intelligence (AI) is poised to significantly transform various facets of the bimetallic tube market, from design and manufacturing to quality control and predictive maintenance. Users are increasingly curious about how AI can optimize material selection and geometric configurations, enabling the development of bimetallic tubes with superior performance characteristics for specific applications. AI algorithms can analyze vast datasets of material properties, performance under stress, and failure modes to recommend optimal material pairings and bond interfaces, accelerating the R&D cycle and reducing the need for extensive physical prototyping. This data-driven approach promises to unlock new material combinations and design efficiencies previously unattainable through traditional methods.

In the manufacturing domain, AI is expected to revolutionize process control and quality assurance. Integrating AI-powered vision systems and sensor arrays on production lines can enable real-time defect detection, precise control over bonding parameters, and optimization of processing temperatures and pressures. This leads to higher production yields, reduced scrap rates, and improved consistency in the metallurgical bond between layers. Furthermore, AI's capability in predictive analytics will play a crucial role in the operational phase of bimetallic tubes, predicting potential failures based on operational data, temperature fluctuations, and corrosive exposure. This allows for proactive maintenance, minimizing downtime, and extending the operational lifespan of critical equipment, thereby enhancing safety and operational efficiency across industries.

- Enhanced material selection and design optimization through AI-driven simulations.

- Real-time quality control and defect detection during manufacturing processes.

- Predictive maintenance for installed bimetallic tubes, extending operational life.

- Optimization of manufacturing parameters for improved yield and efficiency.

- Advanced supply chain management and demand forecasting for raw materials.

Key Takeaways Bimetallic Tube Market Size & Forecast

The bimetallic tube market is positioned for substantial growth through 2033, driven by the escalating global demand for durable and corrosion-resistant materials across critical industrial sectors. The forecast indicates a steady expansion, primarily fueled by significant investments in energy infrastructure, including traditional oil and gas, as well as emerging sectors such as hydrogen and carbon capture technologies. This growth underscores the essential role bimetallic tubes play in mitigating material degradation in harsh operating environments, offering a cost-effective alternative to solid alloy solutions while ensuring operational integrity and extended asset lifespan. The market's trajectory reflects a broader industrial shift towards optimized material performance and resource efficiency.

A significant takeaway is the market's resilience and adaptability, particularly in responding to evolving industrial requirements for high-performance components. The projected increase in market value highlights the confidence in bimetallic tube technology as a long-term solution for demanding applications, ranging from heat exchangers in chemical plants to critical piping in offshore platforms. Key growth areas include the Asia Pacific region, driven by rapid industrialization and infrastructure development, and North America, bolstered by renewed investments in energy and processing facilities. This sustained growth trajectory emphasizes the ongoing importance of material science innovation in supporting global industrial expansion and infrastructure modernization.

- Market projected for robust growth, reaching USD 990 Million by 2033.

- Crucial for industries facing severe corrosion and high temperatures.

- Significant demand from oil and gas, chemical, and power generation sectors.

- Cost-effective alternative to expensive solid alloy materials.

- Innovation in manufacturing and material combinations driving market expansion.

Bimetallic Tube Market Drivers Analysis

The bimetallic tube market is primarily driven by the increasing demand for high-performance materials capable of withstanding harsh operating conditions across various industries. Industries such as oil and gas, chemical processing, and power generation constantly seek materials that offer superior corrosion resistance, enhanced thermal conductivity, and mechanical strength to ensure operational safety and longevity of equipment. Bimetallic tubes provide a cost-effective solution by combining the desirable properties of two different metals, allowing for specialized resistance to specific corrosive agents on the inside while maintaining structural integrity and affordability with a different material on the outside. This dual-metal approach extends the lifespan of critical components, reducing maintenance costs and downtime.

Furthermore, global investments in new infrastructure projects and the modernization of existing facilities are significant market drivers. Rapid industrialization in emerging economies, coupled with a focus on energy efficiency and environmental regulations worldwide, necessitates the use of advanced materials. Bimetallic tubes, with their tailored properties, are increasingly specified in heat exchangers, condensers, and process piping systems to improve efficiency and comply with stringent safety and environmental standards. The growing complexity of industrial processes and the need for reliable, long-lasting solutions in challenging environments continue to fuel the adoption of bimetallic tubes, making them a crucial component in high-value industrial applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Energy Sectors (Oil & Gas, Power Generation) | +0.5% | Global, particularly Middle East, Asia Pacific, North America | Long-term (2025-2033) |

| Growing Need for Corrosion Resistance in Harsh Environments | +0.4% | Global, especially Coastal & Offshore Regions | Long-term (2025-2033) |

| Cost-Effectiveness Compared to Expensive Solid Alloys | +0.3% | Global, all industrial economies | Medium-term (2025-2029) |

| Expansion and Modernization of Chemical & Petrochemical Industries | +0.3% | Asia Pacific, North America, Europe | Long-term (2025-2033) |

Bimetallic Tube Market Restraints Analysis

Despite the significant advantages, the bimetallic tube market faces several restraints that could impede its growth trajectory. One primary constraint is the higher initial manufacturing cost and complexity associated with producing bimetallic tubes compared to conventional single-material tubes. The precise bonding of two dissimilar metals requires specialized equipment, skilled labor, and stringent quality control processes, all of which contribute to higher production expenses. This can deter price-sensitive end-users, especially for projects with limited budgets or when less demanding applications can suffice with standard materials. The technical challenges involved in ensuring a perfect metallurgical bond and preventing inter-diffusion or delamination under operational stress also pose significant hurdles to widespread adoption.

Another restraint stems from the volatility in raw material prices. Bimetallic tubes often incorporate high-value alloys such as nickel, titanium, or specific grades of stainless steel, whose prices can fluctuate significantly due to global supply and demand dynamics, geopolitical factors, or mining output. Such price instability makes long-term project planning and cost estimation challenging for manufacturers and end-users alike, potentially impacting investment decisions. Additionally, the availability of alternative high-performance single-metal alloys or advanced coatings, while often less effective or more expensive in specific extreme conditions, can still present competition, particularly in less critical applications where the full benefits of bimetallic solutions may not justify the higher upfront investment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Manufacturing Costs and Complexity | -0.3% | Global, especially emerging markets | Long-term (2025-2033) |

| Volatile Raw Material Prices | -0.2% | Global | Medium-term (2025-2029) |

| Availability of Alternative Materials and Technologies | -0.1% | Global, specific niche applications | Medium-term (2025-2029) |

Bimetallic Tube Market Opportunities Analysis

Significant opportunities exist for the bimetallic tube market, particularly in emerging industrial sectors and the increasing global focus on sustainable energy. The burgeoning hydrogen economy, with its need for corrosion-resistant materials capable of handling hydrogen embrittlement and high pressures, presents a substantial growth avenue. Similarly, the expansion of carbon capture, utilization, and storage (CCUS) projects, offshore wind energy, and advanced nuclear power generation facilities demand specialized materials for heat exchange and fluid transfer under extreme conditions. Bimetallic tubes, offering tailored material properties, are ideally suited for these evolving applications, providing a performance advantage over traditional materials and fostering new market segments.

Furthermore, ongoing research and development in material science and manufacturing processes offer continuous opportunities for market expansion. Innovations in bonding techniques, such as laser welding and additive manufacturing, could further enhance the integrity and reduce the cost of bimetallic tubes, making them accessible for a broader range of applications. Exploring new alloy combinations, including those with enhanced thermal conductivity or higher resistance to specific forms of corrosion (e.g., microbial corrosion), will open up new markets in industries like wastewater treatment or specialized chemical synthesis. The growing trend of replacing aging infrastructure globally also presents a substantial demand for durable and efficient bimetallic solutions, ensuring long-term market stability and growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Hydrogen Economy and CCUS | +0.6% | Global, particularly Europe, North America, Asia Pacific | Long-term (2027-2033) |

| R&D in New Material Combinations and Manufacturing Techniques | +0.4% | Global | Medium to Long-term (2026-2033) |

| Market Expansion in Developing Economies and Industrialization | +0.3% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Replacement Demand for Aging Industrial Infrastructure | +0.2% | North America, Europe | Long-term (2025-2033) |

Bimetallic Tube Market Challenges Impact Analysis

The bimetallic tube market faces several significant challenges that can influence its growth trajectory. One major challenge is ensuring consistent quality and maintaining bond integrity between the two dissimilar metals, especially under extreme operating conditions involving high temperatures, pressures, and corrosive media. Any defect in the metallurgical bond can lead to delamination, reduced performance, or catastrophic failure, making stringent quality control and advanced inspection techniques critical and costly. This challenge is exacerbated when dealing with novel material combinations or complex tube geometries, requiring continuous innovation in manufacturing and testing protocols.

Another prominent challenge is the intense competition from alternative materials and manufacturing technologies. While bimetallic tubes offer unique advantages, the market for high-performance industrial materials is diverse, including highly corrosion-resistant solid alloys, advanced coatings, and composite materials. Manufacturers must constantly demonstrate the superior life cycle cost, performance benefits, and reliability of bimetallic solutions to justify their adoption over competitive alternatives. Furthermore, the specialized knowledge and capital investment required for bimetallic tube production can limit the number of market participants, potentially leading to supply chain concentration and vulnerability to disruptions, thereby posing risks to market stability and growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Consistent Quality and Bond Integrity | -0.2% | Global | Long-term (2025-2033) |

| Competition from Alternative Materials and Technologies | -0.1% | Global, particularly for less critical applications | Medium-term (2025-2029) |

| Supply Chain Disruptions and Raw Material Scarcity | -0.1% | Global | Short to Medium-term (2025-2027) |

Bimetallic Tube Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the bimetallic tube market, offering critical insights into its current size, historical performance, and future growth projections. The scope encompasses detailed segmentation by material type, manufacturing process, end-use industry, and application, providing a granular view of market dynamics. Furthermore, the report presents a thorough regional analysis, identifying key growth hubs and their contributions to the overall market landscape. Strategic insights into market drivers, restraints, opportunities, and challenges are provided, alongside an assessment of the competitive landscape, featuring profiles of leading market participants and their strategic initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650 Million |

| Market Forecast in 2033 | USD 990 Million |

| Growth Rate | 5.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Precision Tubing Solutions, Global Alloy Systems, Advanced Material Composites, Industrial Tube Innovations, Metallurgical Components Group, Seamless Clad Tube Corp, Bonded Pipes International, Composite Tube Technologies, Integrated Metal Solutions, Elite Tube Manufacturing, Universal Piping Systems, Dynamic Tube Solutions, Premium Alloy Tubes, Corrosion Resistant Materials Inc., Thermal Transfer Tube Co., High Performance Piping, Engineered Tube Products, Innovative Metal Formers, Specialized Alloys Group, Frontier Tube & Pipe |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The bimetallic tube market is comprehensively segmented to provide a detailed understanding of its varied applications and demand drivers across different industrial verticals. This segmentation allows for precise market sizing and forecasting, highlighting the specific material combinations and manufacturing processes that are gaining prominence. The primary segmentation categories include material type, which differentiates between the outer and inner layer compositions, crucial for addressing diverse corrosive environments and operational temperatures. Manufacturing process segmentation identifies the dominant methods used to produce these specialized tubes, influencing cost, quality, and production scalability. Furthermore, end-use industry and application segments illustrate the breadth of industries reliant on bimetallic tubes for their critical infrastructure and equipment.

- By Material Type (Clad/Liner): Carbon Steel/Stainless Steel, Carbon Steel/Copper Alloys, Alloy Steel/Stainless Steel, Nickel Alloys/Stainless Steel, Duplex/Super Duplex Steel, Titanium/Stainless Steel, Aluminum/Stainless Steel.

- By Manufacturing Process: Co-extrusion, Hydraulic Expansion, Drawn Over Mandrel (DOM), Explosive Bonding, Roll Forming & Welding.

- By End-Use Industry: Oil & Gas, Chemical & Petrochemical, Power Generation (Thermal, Nuclear, Renewable), HVAC & Refrigeration, Marine & Shipbuilding, Desalination Plants, Food & Beverage, Pulp & Paper, Pharmaceutical, Others.

- By Application: Heat Exchangers, Condensers, Boilers, Furnaces, Process Piping, Evaporators, Heaters, Reactors, Structural Components.

Regional Highlights

- North America: This region is a significant market due to the extensive presence of oil and gas exploration and refining activities, robust chemical processing industries, and ongoing infrastructure modernization projects. The demand for bimetallic tubes is driven by the need for corrosion-resistant materials in aging energy infrastructure and new investments in petrochemical facilities.

- Europe: Driven by stringent environmental regulations, a focus on industrial efficiency, and significant investments in renewable energy and carbon capture technologies, Europe presents a strong market for bimetallic tubes. Germany, the UK, and France are key contributors, particularly in the chemical, power generation, and marine sectors.

- Asia Pacific (APAC): The APAC region represents the largest and fastest-growing market, propelled by rapid industrialization, massive investments in infrastructure development, and expanding chemical, petrochemical, and power generation capacities, especially in China, India, and Southeast Asian countries. The escalating demand for energy and the need for durable industrial components are major drivers.

- Latin America: This region shows promising growth, particularly influenced by the oil and gas sector in countries like Brazil and Mexico, alongside growing investments in mining and chemical industries. The need for advanced materials to enhance operational efficiency and reduce maintenance in harsh environments fuels demand.

- Middle East and Africa (MEA): The MEA region is a critical market, predominantly due to its vast oil and gas reserves and significant investments in desalination plants and petrochemical complexes. The extremely corrosive environments and high temperatures necessitate the use of bimetallic tubes for prolonged equipment life and operational safety.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bimetallic Tube Market.- Precision Tubing Solutions

- Global Alloy Systems

- Advanced Material Composites

- Industrial Tube Innovations

- Metallurgical Components Group

- Seamless Clad Tube Corp

- Bonded Pipes International

- Composite Tube Technologies

- Integrated Metal Solutions

- Elite Tube Manufacturing

- Universal Piping Systems

- Dynamic Tube Solutions

- Premium Alloy Tubes

- Corrosion Resistant Materials Inc.

- Thermal Transfer Tube Co.

- High Performance Piping

- Engineered Tube Products

- Innovative Metal Formers

- Specialized Alloys Group

- Frontier Tube & Pipe

Frequently Asked Questions

Analyze common user questions about the Bimetallic Tube market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are bimetallic tubes?

Bimetallic tubes are composite tubes made from two different metals or alloys concentrically bonded together, typically for enhanced performance in specific industrial applications. The outer layer provides structural integrity or specific external resistance, while the inner layer offers superior corrosion resistance or other specialized properties for the internal medium.

Why are bimetallic tubes used in industrial applications?

Bimetallic tubes are preferred for their ability to combine the benefits of two distinct metals, offering superior corrosion resistance, enhanced thermal conductivity, or improved mechanical strength at a potentially lower cost than using a solid tube of an expensive high-performance alloy. This optimizes material use for challenging operating environments.

What industries commonly use bimetallic tubes?

Key industries include oil and gas, chemical and petrochemical processing, power generation (thermal, nuclear, and renewable), marine and shipbuilding, and desalination plants. They are primarily used in heat exchangers, condensers, boilers, and process piping where severe corrosive conditions or extreme temperatures are present.

What are the primary manufacturing processes for bimetallic tubes?

Common manufacturing processes include co-extrusion, where two billets are simultaneously extruded to form a bonded tube; hydraulic expansion, which bonds an inner tube to an outer tube through pressure; drawn-over-mandrel (DOM) methods; and explosive bonding, which uses an explosive force to create a metallurgical bond.

What are the main advantages of bimetallic tubes over single-material tubes?

The key advantages include superior resistance to specific forms of corrosion or wear on the interior surface, combined with the cost-effectiveness and structural strength of a different material on the exterior. This leads to extended service life, reduced maintenance, and optimized performance in demanding environments, often providing a more economical solution than a monolithic high-alloy alternative.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted