Stainless Steel Welded Tube Market

Stainless Steel Welded Tube Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702822 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

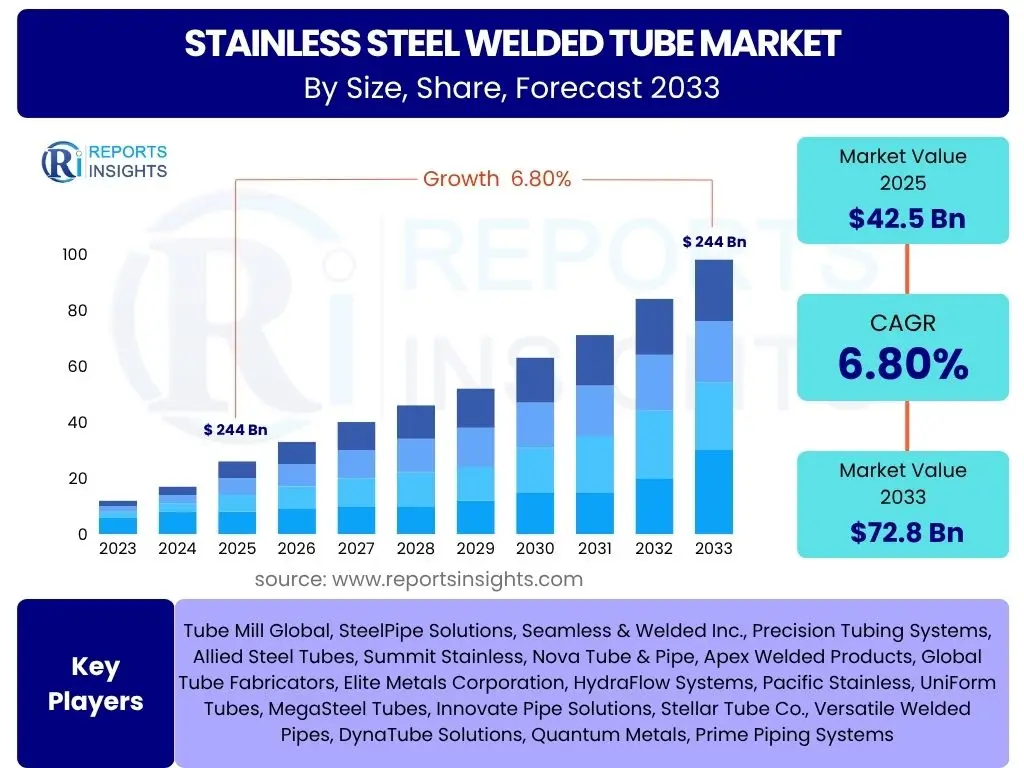

Stainless Steel Welded Tube Market Size

According to Reports Insights Consulting Pvt Ltd, The Stainless Steel Welded Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 42.5 billion in 2025 and is projected to reach USD 72.8 billion by the end of the forecast period in 2033.

Key Stainless Steel Welded Tube Market Trends & Insights

User queries frequently highlight an interest in understanding the evolving landscape of the stainless steel welded tube market, particularly concerning innovation in manufacturing processes, the adoption of advanced materials, and shifts in demand patterns across key end-use industries. There is a clear emphasis on how sustainability and efficiency are influencing market dynamics. Furthermore, questions arise about regional growth disparities and the impact of global supply chain considerations on market trends.

The market is experiencing a significant push towards higher-grade stainless steel alloys, driven by the need for enhanced corrosion resistance and strength in demanding environments such as chemical processing and offshore oil and gas. There's also a noticeable trend in the adoption of automated and precision welding technologies to improve product consistency and reduce manufacturing costs. Sustainability initiatives are increasingly impacting production methods, with a focus on energy efficiency and waste reduction throughout the manufacturing lifecycle.

- Growing demand for high-performance alloys (e.g., Duplex, Super Duplex) for critical applications.

- Increased adoption of advanced welding techniques such as laser welding and orbital welding for superior seam integrity.

- Rising focus on energy-efficient manufacturing processes and sustainable production practices.

- Expansion of applications in renewable energy sectors, particularly solar and hydrogen infrastructure.

- Shift towards customized and lightweight tube solutions to meet specific industry requirements.

AI Impact Analysis on Stainless Steel Welded Tube

Common user questions regarding AI's influence on the stainless steel welded tube sector center on its potential to revolutionize manufacturing efficiency, quality control, and supply chain management. Stakeholders are keen to understand how AI can optimize production parameters, predict equipment failures, and enhance material traceability. There is also an interest in AI's role in driving predictive maintenance and improving overall operational intelligence within tube manufacturing facilities.

The integration of Artificial Intelligence (AI) in the stainless steel welded tube industry is poised to bring transformative changes, primarily by optimizing production workflows and enhancing product quality. AI algorithms can analyze vast datasets from manufacturing lines, identifying patterns that lead to improved welding parameters, reduced scrap rates, and more efficient resource utilization. This analytical capability extends to predictive maintenance, where AI can forecast equipment failures, minimizing downtime and maintenance costs. Furthermore, AI-driven solutions are being explored for supply chain optimization, demand forecasting, and inventory management, leading to more resilient and responsive operations.

- Manufacturing Optimization: AI-driven process control for welding parameters, reducing defects and improving output consistency.

- Predictive Maintenance: AI algorithms analyze sensor data from machinery to predict failures, extending equipment lifespan and minimizing downtime.

- Quality Control: AI-powered vision systems for automated defect detection and classification, ensuring higher product quality.

- Supply Chain Efficiency: AI for demand forecasting, inventory management, and logistics optimization, leading to reduced costs and improved responsiveness.

- Material Innovation: AI-driven simulations and data analysis to accelerate the development of new alloy compositions and tube designs.

Key Takeaways Stainless Steel Welded Tube Market Size & Forecast

Common user queries concerning key takeaways from the market size and forecast often focus on identifying the most promising growth segments, understanding the primary drivers of expansion, and discerning the regions poised for significant development. Users also seek clarity on the long-term sustainability of growth trends and the competitive landscape. The core interest lies in actionable insights derived from the market's quantitative projections.

The Stainless Steel Welded Tube Market is set for robust growth, primarily fueled by expanding applications in critical industries such as automotive, oil and gas, and construction, alongside increasing demand from emerging sectors like renewable energy and hydrogen infrastructure. Asia Pacific is anticipated to remain the dominant and fastest-growing region, driven by rapid industrialization and urbanization. The forecast indicates a sustained focus on technological advancements and higher-grade materials, shaping the market's future trajectory.

- The market exhibits strong growth potential, driven by global industrialization and infrastructure development.

- Asia Pacific is expected to maintain its leadership, offering significant opportunities due to high investment in manufacturing and construction.

- Technological advancements in welding and material science are crucial for product differentiation and market competitiveness.

- Demand for specialized and high-performance stainless steel grades is accelerating across various end-use industries.

- Sustainability and energy efficiency in production processes are becoming key market differentiators.

Stainless Steel Welded Tube Market Drivers Analysis

The expansion of the stainless steel welded tube market is significantly propelled by robust growth in key end-use industries, which increasingly rely on these tubes for their corrosion resistance, durability, and versatility. Global infrastructure development, including residential, commercial, and industrial construction, necessitates large volumes of stainless steel tubes for piping, structural support, and architectural elements. Furthermore, the stringent quality and performance requirements in sectors like automotive, chemical processing, and oil and gas continue to drive demand for high-quality welded tubes. The growing emphasis on lightweighting and fuel efficiency in the automotive industry, for instance, has increased the adoption of stainless steel tubing for exhaust systems and structural components.

Additionally, the burgeoning renewable energy sector, encompassing solar, wind, and hydrogen energy projects, presents a substantial growth avenue for stainless steel welded tubes, especially for fluid conveyance and structural applications in harsh environments. The versatility of stainless steel, coupled with advancements in welding technologies that allow for tailored properties, further solidifies its position as a preferred material. Overall, the market benefits from a confluence of factors including industrial growth, technological advancements, and evolving application requirements across diverse global industries.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from Automotive Industry | +1.5% | Asia Pacific, Europe, North America | 2025-2033 |

| Rapid Industrialization and Urbanization | +1.2% | Asia Pacific, Middle East & Africa | 2025-2033 |

| Increasing Investment in Infrastructure Development | +1.0% | Global, particularly Asia Pacific, North America | 2025-2033 |

| Expansion of Chemical and Petrochemical Industries | +0.8% | North America, Europe, Middle East | 2025-2033 |

| Growth in Renewable Energy Sector (Solar, Hydrogen) | +0.7% | Global, particularly Europe, Asia Pacific | 2025-2033 |

Stainless Steel Welded Tube Market Restraints Analysis

The stainless steel welded tube market faces several significant restraints that could impede its growth trajectory. One primary concern is the volatility of raw material prices, particularly nickel and chromium, which are key components of stainless steel. Fluctuations in these commodity prices directly impact manufacturing costs, leading to unstable pricing for end-products and potentially deterring large-scale investments or long-term contracts. This unpredictability makes inventory management and financial planning challenging for manufacturers.

Additionally, the market is subject to stringent environmental regulations and trade policies that can affect production processes and international trade. Compliance with emissions standards, waste disposal regulations, and anti-dumping duties can increase operational costs and create barriers to market entry. Intense competition from alternative materials, such as plastics, carbon steel, and composite materials, in certain less demanding applications, also poses a restraint. While stainless steel offers superior properties, the cost-effectiveness of alternatives can sometimes be a deciding factor for purchasers, particularly in price-sensitive segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Nickel, Chromium) | -0.9% | Global | 2025-2033 |

| Intense Competition from Alternative Materials | -0.7% | Global | 2025-2033 |

| Stringent Environmental Regulations and Trade Policies | -0.6% | Europe, North America, Asia Pacific (China) | 2025-2033 |

| High Energy Consumption in Manufacturing | -0.5% | Global | 2025-2033 |

| Economic Downturns and Geopolitical Instability | -0.4% | Global | Short to Mid-term (2025-2028) |

Stainless Steel Welded Tube Market Opportunities Analysis

The stainless steel welded tube market is presented with several compelling opportunities for expansion and innovation. A significant avenue lies in the burgeoning demand for lightweight and high-strength materials in the automotive and aerospace sectors, where fuel efficiency and structural integrity are paramount. This creates an opening for advanced stainless steel alloys and optimized tube designs. Furthermore, the global drive towards cleaner energy sources and sustainable infrastructure development, particularly in the solar, hydrogen, and electric vehicle charging station markets, necessitates specialized stainless steel tubing for safe and efficient fluid conveyance and structural applications.

Technological advancements in manufacturing processes, such as additive manufacturing and smart factory integration, offer opportunities to enhance production efficiency, reduce waste, and enable customization. The increasing penetration into new applications, including medical devices, high-purity systems, and niche industrial uses requiring superior corrosion resistance and hygiene, also presents considerable growth prospects. Market players focusing on research and development to create innovative products that meet specific industry needs, alongside strategic collaborations and acquisitions to expand geographic reach and technological capabilities, are well-positioned to capitalize on these emerging opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for Lightweight Materials in Automotive & Aerospace | +1.1% | North America, Europe, Asia Pacific | 2026-2033 |

| Expansion into New Application Areas (e.g., Medical, Hydrogen Transport) | +1.0% | Global | 2027-2033 |

| Technological Advancements in Manufacturing (e.g., Automation, Additive Manufacturing) | +0.9% | Global | 2025-2033 |

| Increased Focus on Sustainable and Eco-friendly Production | +0.8% | Europe, North America, Asia Pacific | 2025-2033 |

| Emerging Markets in Developing Economies | +0.7% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 |

Stainless Steel Welded Tube Market Challenges Impact Analysis

The stainless steel welded tube market faces several inherent challenges that demand strategic responses from manufacturers. One significant challenge is managing complex global supply chains, which are susceptible to disruptions from geopolitical events, natural disasters, and economic downturns. These disruptions can lead to material shortages, increased logistics costs, and delays in delivery, directly impacting production schedules and profitability. Furthermore, maintaining consistent product quality across various manufacturing sites and meeting stringent international standards requires substantial investment in quality control systems and skilled labor.

The industry also grapples with the challenge of skilled labor shortages, particularly in specialized welding techniques and automated machinery operation. Attracting and retaining a skilled workforce is crucial for ensuring high-quality production and efficient operations. Moreover, the capital-intensive nature of stainless steel tube manufacturing, including investments in advanced machinery, research and development, and environmental compliance, can pose a barrier to entry for new players and a financial burden for existing ones, especially during periods of economic uncertainty. These challenges necessitate continuous innovation and adaptive strategies to sustain competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Logistics Volatility | -0.8% | Global | 2025-2028 |

| Intensifying Price Competition and Market Saturation | -0.7% | Asia Pacific, Europe | 2025-2033 |

| Availability and Cost of Skilled Labor | -0.6% | North America, Europe | 2025-2033 |

| High Capital Investment for Technology Upgrades | -0.5% | Global | 2025-2030 |

| Fluctuating Demand from End-Use Industries | -0.4% | Global | 2025-2033 |

Stainless Steel Welded Tube Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Stainless Steel Welded Tube Market, covering historical performance from 2019 to 2023 and offering a detailed forecast from 2025 to 2033. It encompasses market size estimations, growth rates, key trends, and a thorough segmentation by material grade, outer diameter, application, and end-use industry across major global regions. The report further profiles leading market players, offering insights into their strategies and competitive positioning to provide a holistic understanding of the market landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 42.5 Billion |

| Market Forecast in 2033 | USD 72.8 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Tube Mill Global, SteelPipe Solutions, Seamless & Welded Inc., Precision Tubing Systems, Allied Steel Tubes, Summit Stainless, Nova Tube & Pipe, Apex Welded Products, Global Tube Fabricators, Elite Metals Corporation, HydraFlow Systems, Pacific Stainless, UniForm Tubes, MegaSteel Tubes, Innovate Pipe Solutions, Stellar Tube Co., Versatile Welded Pipes, DynaTube Solutions, Quantum Metals, Prime Piping Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The stainless steel welded tube market is meticulously segmented to provide a granular view of its diverse dynamics and identify specific growth pockets. This segmentation allows for a comprehensive analysis of demand patterns based on material properties, size requirements, functional applications, and end-user industries. Understanding these segments is crucial for manufacturers to tailor their product offerings, optimize production, and penetrate specific market niches effectively.

The segmentation by material grade reflects the varying requirements for corrosion resistance, strength, and weldability across different applications, with austenitic grades dominating due to their versatility. Outer diameter segmentation caters to specific fluid flow, structural, or heat exchange capacities. Application-based segmentation highlights the primary use cases, while end-use industry segmentation provides insight into the major consumers of these tubes, from heavy industries like oil & gas to highly regulated sectors such as pharmaceutical and medical.

- By Material Grade: Austenitic, Ferritic, Martensitic, Duplex & Super Duplex, Others

- By Outer Diameter: Up to 1 inch, 1 to 2 inches, 2 to 4 inches, 4 to 6 inches, Above 6 inches

- By Application: Heat Exchanger Tubes, Condenser Tubes, Piping Systems, Structural Applications, Instrumentation & Control, Others

- By End-Use Industry: Oil & Gas, Chemical & Petrochemical, Automotive & Transportation, Building & Construction, Food & Beverage, Power Generation, Water Treatment, Pulp & Paper, Pharmaceutical & Medical, HVAC, Others

Regional Highlights

- North America: Characterized by significant demand from the oil and gas industry, particularly for high-pressure applications, alongside growing investments in infrastructure and manufacturing modernization. The automotive sector's shift towards electric vehicles also presents new opportunities for lightweight stainless steel components.

- Europe: Driven by stringent environmental regulations promoting the use of corrosion-resistant materials and robust demand from the chemical, food & beverage, and pharmaceutical sectors. Germany and the UK are key markets with strong industrial bases. Increasing focus on renewable energy projects also boosts demand.

- Asia Pacific (APAC): Dominates the global market due to rapid industrialization, extensive infrastructure development, and burgeoning manufacturing activities in countries like China, India, Japan, and South Korea. High growth in automotive production, construction, and chemical processing sectors underpins the region's strong market position.

- Latin America: Expected to witness steady growth, primarily fueled by investments in the oil and gas sector (especially Brazil and Mexico), infrastructure development, and a growing manufacturing base. Economic stability and industrial expansion will be key drivers.

- Middle East and Africa (MEA): Growth is primarily driven by significant investments in the oil and gas industry, petrochemical plants, and large-scale construction projects. Economic diversification initiatives in Gulf Cooperation Council (GCC) countries also contribute to the demand for high-quality stainless steel tubes.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Stainless Steel Welded Tube Market.- Tube Mill Global

- SteelPipe Solutions

- Seamless & Welded Inc.

- Precision Tubing Systems

- Allied Steel Tubes

- Summit Stainless

- Nova Tube & Pipe

- Apex Welded Products

- Global Tube Fabricators

- Elite Metals Corporation

- HydraFlow Systems

- Pacific Stainless

- UniForm Tubes

- MegaSteel Tubes

- Innovate Pipe Solutions

- Stellar Tube Co.

- Versatile Welded Pipes

- DynaTube Solutions

- Quantum Metals

- Prime Piping Systems

Frequently Asked Questions

Analyze common user questions about the Stainless Steel Welded Tube market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Stainless Steel Welded Tube Market?

The Stainless Steel Welded Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, indicating robust expansion driven by diverse industrial applications.

Which industries are the primary consumers of stainless steel welded tubes?

Key end-use industries include Oil & Gas, Chemical & Petrochemical, Automotive & Transportation, Building & Construction, Food & Beverage, Power Generation, and Water Treatment, among others, leveraging their corrosion resistance and durability.

What are the key drivers fueling the growth of this market?

Major drivers include rapid industrialization, increasing infrastructure development, growing demand from the automotive sector for lightweight materials, and expansion of the chemical and renewable energy industries.

How is AI impacting the Stainless Steel Welded Tube manufacturing process?

AI is increasingly used for manufacturing optimization, predictive maintenance, enhanced quality control through automated inspection, and improved supply chain efficiency, leading to higher productivity and reduced waste.

Which region is expected to dominate the Stainless Steel Welded Tube Market?

Asia Pacific is anticipated to maintain its dominance in the Stainless Steel Welded Tube Market, propelled by extensive industrial growth, urbanization, and significant investments in manufacturing and infrastructure across the region.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted