Stainless Steel Forging Market

Stainless Steel Forging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703389 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Stainless Steel Forging Market Size

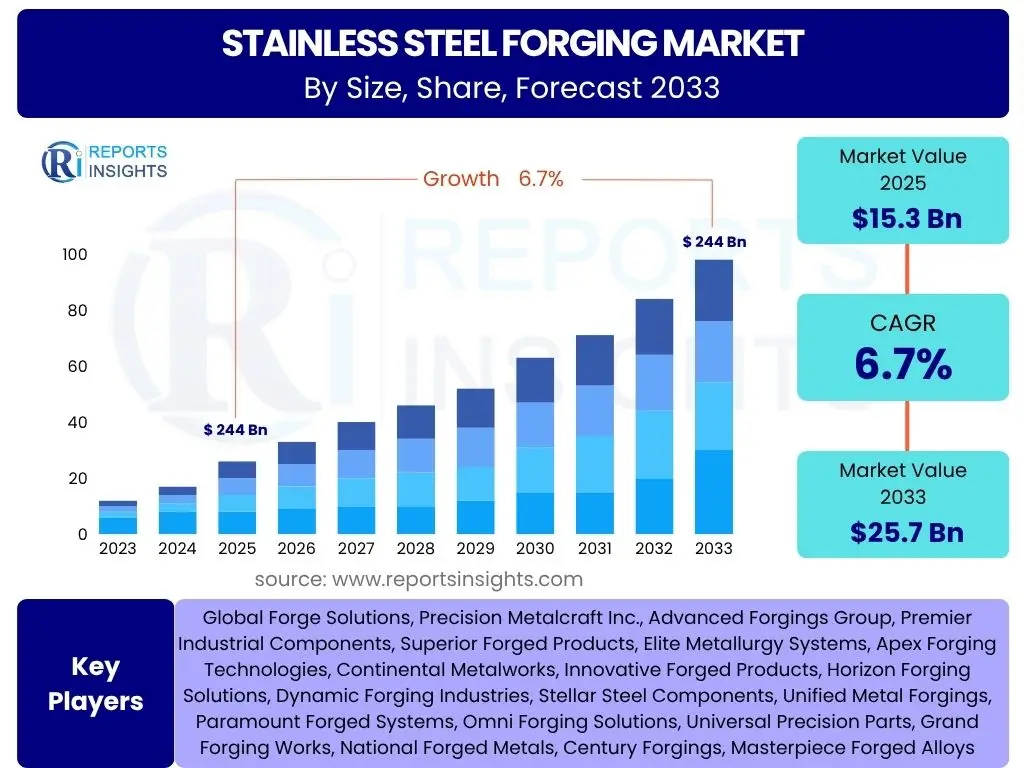

According to Reports Insights Consulting Pvt Ltd, The Stainless Steel Forging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 15.3 Billion in 2025 and is projected to reach USD 25.7 Billion by the end of the forecast period in 2033.

Key Stainless Steel Forging Market Trends & Insights

The Stainless Steel Forging market is experiencing dynamic shifts driven by evolving industrial demands and technological advancements. Users frequently inquire about the primary trends shaping market growth, with particular interest in how new material grades and manufacturing techniques are influencing product development and application areas. There is a notable focus on the increasing adoption of lightweight yet high-strength stainless steel components across various end-use industries, necessitating continuous innovation in forging processes and material science. Furthermore, the market is witnessing a strong push towards enhanced automation and digitalization within forging operations to improve efficiency and precision.

Another significant trend revolves around the growing emphasis on sustainability and circular economy principles. Market participants are exploring eco-friendly forging methods, reducing material waste, and optimizing energy consumption, driven by stricter environmental regulations and corporate social responsibility initiatives. The convergence of these trends suggests a future where stainless steel forging is not only about robust component production but also about intelligent, efficient, and environmentally conscious manufacturing. Users are also keen to understand how these trends translate into new opportunities for market players and the implications for supply chain resilience.

- Growing demand for high-strength, corrosion-resistant components across diverse industries.

- Increasing adoption of duplex and super duplex stainless steels for critical applications.

- Advancements in forging technologies, including isothermal forging and near-net-shape forging.

- Emphasis on automation and digitalization to enhance production efficiency and quality control.

- Rising demand from electric vehicle (EV) manufacturing for lightweight forged parts.

- Focus on sustainable manufacturing practices and waste reduction.

- Customization and specialization of forged components to meet specific industry requirements.

AI Impact Analysis on Stainless Steel Forging

User queries regarding the impact of Artificial Intelligence (AI) on the Stainless Steel Forging sector reveal a keen interest in how this technology can revolutionize traditional manufacturing processes. Common questions center on AI's potential to optimize forging parameters, improve quality consistency, and reduce production costs. Stakeholders are exploring AI-driven solutions for predictive maintenance of forging machinery, real-time process monitoring, and anomaly detection, which can significantly enhance operational efficiency and minimize downtime. The application of machine learning algorithms for material characterization and defect prediction is also a key area of inquiry, promising to elevate product quality and reduce material waste.

Furthermore, there is considerable curiosity about AI's role in design optimization and simulation. AI algorithms can rapidly analyze complex material behaviors under various forging conditions, enabling engineers to refine designs for optimal performance and manufacturability before physical prototyping. This not only accelerates product development cycles but also significantly reduces the costs associated with trial-and-error manufacturing. The integration of AI in supply chain management for demand forecasting and inventory optimization also presents a compelling use case, ensuring a more resilient and responsive forging ecosystem. Users anticipate that AI will lead to more intelligent factories, capable of self-optimization and adaptive manufacturing strategies.

- AI-driven optimization of forging parameters for improved material flow and reduced defects.

- Predictive maintenance of forging equipment to minimize unscheduled downtime.

- Enhanced quality control through AI-powered visual inspection and defect detection systems.

- Optimization of energy consumption in forging furnaces and processes using AI algorithms.

- Accelerated design and simulation of forged components using machine learning.

- Improved supply chain management and demand forecasting through AI analytics.

- Automation of repetitive tasks and process monitoring to increase operational efficiency.

Key Takeaways Stainless Steel Forging Market Size & Forecast

The Stainless Steel Forging market is poised for robust growth, reflecting increasing industrialization and demand for high-performance materials globally. Key inquiries from users often revolve around the underlying factors driving this expansion and the critical insights that define its future trajectory. A primary takeaway is the indispensable role of stainless steel forgings in critical applications across diverse sectors, including automotive, aerospace, and energy, where their superior strength, corrosion resistance, and durability are paramount. The market's growth is also significantly influenced by technological advancements in forging processes, enabling the production of more complex and precise components efficiently.

Another crucial insight is the dynamic interplay between market drivers, restraints, opportunities, and challenges that shape the overall forecast. While strong demand from end-use industries and material innovation act as significant drivers, factors like raw material price volatility and stringent environmental regulations pose ongoing challenges. Nevertheless, emerging opportunities in electric vehicles, renewable energy infrastructure, and smart manufacturing initiatives present substantial avenues for expansion. Understanding these interconnected elements is vital for stakeholders to navigate the market effectively, capitalize on growth prospects, and mitigate potential risks, ensuring sustained profitability and competitive advantage in the long term.

- The market exhibits steady growth, driven by increasing industrialization and demand for high-performance components.

- Automotive, aerospace, and energy sectors are primary growth engines for stainless steel forgings.

- Technological advancements in forging techniques are crucial for meeting evolving application requirements.

- Opportunities in emerging sectors like electric vehicles and renewable energy are set to fuel future expansion.

- Raw material price fluctuations and environmental regulations remain key considerations for market players.

- Innovation in material science and process optimization will be critical for competitive advantage.

- Regional disparities in industrial development significantly influence market dynamics and demand patterns.

Stainless Steel Forging Market Drivers Analysis

The Stainless Steel Forging market is propelled by a confluence of factors stemming from various industrial applications that increasingly rely on high-performance materials. A significant driver is the expanding automotive sector, particularly the growing demand for lightweight, high-strength components essential for fuel efficiency and structural integrity in both conventional and electric vehicles. Stainless steel forgings offer superior mechanical properties and corrosion resistance, making them ideal for critical engine parts, transmission components, and structural elements. This sustained demand is reinforced by the global shift towards enhanced vehicle safety standards and performance optimization.

Furthermore, the aerospace and defense industries contribute substantially to market growth, requiring components that withstand extreme temperatures, pressures, and corrosive environments. Stainless steel forgings are integral to aircraft landing gear, engine parts, and structural frames due to their reliability and durability. The ongoing expansion of infrastructure projects worldwide, including bridges, pipelines, and power generation facilities, also fuels demand for robust and long-lasting forged stainless steel parts. Additionally, the oil and gas sector's need for corrosion-resistant equipment in exploration, drilling, and processing further solidifies the market's growth trajectory, ensuring consistent demand for specialized stainless steel forgings that can operate reliably in harsh conditions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Automotive & Aerospace Demand | +1.8% | North America, Europe, Asia Pacific | 2025-2033 |

| Expansion of Industrial Machinery & Equipment Sector | +1.5% | Asia Pacific, Europe, North America | 2025-2033 |

| Increasing Investment in Oil & Gas and Power Generation | +1.2% | Middle East & Africa, North America, Asia Pacific | 2025-2030 |

| Technological Advancements in Forging Processes | +0.9% | Global | 2025-2033 |

| Rising Demand for High-Performance, Corrosion-Resistant Materials | +0.7% | Global | 2025-2033 |

Stainless Steel Forging Market Restraints Analysis

The Stainless Steel Forging market faces several constraints that can temper its growth trajectory. A significant restraint is the inherent volatility and fluctuation in raw material prices, particularly for key alloying elements such as nickel, chromium, and molybdenum. These price instabilities directly impact manufacturing costs, leading to unpredictable production expenses and potentially narrower profit margins for forging companies. Such unpredictability makes long-term planning and fixed-price contracts challenging, often forcing manufacturers to absorb cost increases or pass them on to consumers, which can affect market competitiveness and demand.

Another critical restraint involves stringent environmental regulations and compliance costs. The forging process, especially traditional methods, can be energy-intensive and produce emissions, requiring significant investments in pollution control technologies and sustainable practices. Adhering to evolving environmental standards, particularly in developed regions, adds to operational overheads and can deter new market entrants. Furthermore, the high capital investment required for establishing and upgrading forging facilities, including specialized machinery and skilled labor, poses a barrier, particularly for small and medium-sized enterprises, limiting overall market expansion and technological adoption speed.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Nickel, Chromium) | -1.3% | Global | 2025-2033 |

| High Capital Investment and Production Costs | -0.8% | Global | 2025-2033 |

| Stringent Environmental Regulations and Compliance Costs | -0.7% | Europe, North America, Asia Pacific | 2025-2033 |

| Competition from Alternative Manufacturing Processes | -0.5% | Global | 2028-2033 |

Stainless Steel Forging Market Opportunities Analysis

The Stainless Steel Forging market is presented with several promising opportunities that can significantly accelerate its growth. A major opportunity lies in the rapid expansion of the electric vehicle (EV) market. As EV manufacturers prioritize lightweighting and durability, stainless steel forgings are increasingly being adopted for critical components like battery housings, chassis parts, and motor shafts, offering superior strength-to-weight ratios and corrosion resistance compared to traditional materials. This segment represents a burgeoning demand avenue that is expected to continue its upward trajectory for the foreseeable future.

Furthermore, the growing global focus on renewable energy infrastructure, including wind turbines, solar power systems, and hydroelectric projects, creates substantial demand for high-strength, durable stainless steel forgings. Components in these applications often endure harsh environmental conditions and high stresses, making forged stainless steel an ideal material choice. Additionally, the ongoing trend of industrial automation and Industry 4.0 integration offers opportunities for forging companies to enhance their operational efficiency, reduce waste, and improve product quality through smart manufacturing technologies. Tailoring customized forging solutions for specialized industrial applications, particularly in emerging economies, also provides a lucrative pathway for market expansion and increased revenue generation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Electric Vehicle (EV) Sector | +1.4% | Asia Pacific, Europe, North America | 2025-2033 |

| Expansion in Renewable Energy Infrastructure | +1.1% | Global | 2025-2033 |

| Increasing Adoption of Industry 4.0 and Automation | +0.9% | North America, Europe, Asia Pacific | 2025-2033 |

| Development of New High-Performance Stainless Steel Alloys | +0.6% | Global | 2027-2033 |

Stainless Steel Forging Market Challenges Impact Analysis

The Stainless Steel Forging market contends with several notable challenges that require strategic responses from industry participants. A primary concern is the persistent shortage of skilled labor, particularly experienced metallurgists, forging operators, and quality control specialists. The specialized nature of forging operations demands specific expertise, and the aging workforce coupled with a lack of new talent entering the field creates significant operational bottlenecks and impacts production efficiency. This challenge is exacerbated by the need for continuous training to keep pace with evolving technologies and material science.

Furthermore, the market is vulnerable to fluctuations in energy costs, as forging processes are inherently energy-intensive. Surges in electricity or fuel prices can directly erode profit margins and increase overall manufacturing expenses, making it challenging for companies to maintain competitive pricing. Supply chain disruptions, often stemming from geopolitical events, natural disasters, or global pandemics, also pose a significant challenge. These disruptions can lead to delays in raw material delivery, increased freight costs, and interruptions in production schedules, impacting timely product delivery and overall market stability. Addressing these multifaceted challenges requires robust operational planning, investment in automation, and diversification of supply chains.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Skilled Labor | -0.9% | Global | 2025-2033 |

| Fluctuations in Energy Costs | -0.8% | Global | 2025-2033 |

| Supply Chain Disruptions and Lead Times | -0.7% | Global | 2025-2028 |

| Waste Management and Disposal Issues | -0.4% | Europe, North America | 2025-2033 |

Stainless Steel Forging Market - Updated Report Scope

This comprehensive report delves into the Stainless Steel Forging market, offering a detailed analysis of its current state and future trajectory. It provides an in-depth examination of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. The scope encompasses detailed segmentation by type, application, and end-use industry, alongside a robust competitive landscape analysis of leading market players. The report also incorporates an AI impact analysis, providing a forward-looking perspective on technological integration within the forging industry, aiming to equip stakeholders with actionable insights for strategic decision-making and sustainable growth.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.3 Billion |

| Market Forecast in 2033 | USD 25.7 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Forge Solutions, Precision Metalcraft Inc., Advanced Forgings Group, Premier Industrial Components, Superior Forged Products, Elite Metallurgy Systems, Apex Forging Technologies, Continental Metalworks, Innovative Forged Products, Horizon Forging Solutions, Dynamic Forging Industries, Stellar Steel Components, Unified Metal Forgings, Paramount Forged Systems, Omni Forging Solutions, Universal Precision Parts, Grand Forging Works, National Forged Metals, Century Forgings, Masterpiece Forged Alloys |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Stainless Steel Forging market is comprehensively segmented to provide a granular view of its diverse dynamics and application areas. This segmentation helps in understanding the specific demands and growth drivers within different product types, end-use industries, and manufacturing processes. By analyzing each segment, stakeholders can identify niche opportunities, tailor product offerings, and devise targeted market strategies. The primary segmentation categories include the type of stainless steel used, the application industries that consume these forgings, and the specific forging processes employed, each contributing uniquely to the overall market landscape.

The segmentation by stainless steel type differentiates between Austenitic, Ferritic, Martensitic, and Duplex stainless steel forgings, reflecting their varying mechanical properties and suitability for distinct applications. For instance, Duplex stainless steels are increasingly preferred for their high strength and corrosion resistance in demanding environments like oil and gas. The application segment categorizes demand from crucial sectors such as automotive, aerospace, industrial machinery, and oil and gas, highlighting the indispensable role of forgings in these industries. Finally, the forging process segment, including open-die, closed-die, and ring rolling, identifies the predominant manufacturing techniques and their respective technological advancements and cost efficiencies, providing insights into production capabilities and market preferences.

- By Type:

- Austenitic Stainless Steel Forging

- Ferritic Stainless Steel Forging

- Martensitic Stainless Steel Forging

- Duplex Stainless Steel Forging

- Others (Precipitation Hardening Stainless Steel)

- By Application:

- Automotive

- Aerospace

- Industrial Machinery

- Oil & Gas

- Construction

- Power Generation

- Medical Devices

- Marine

- Others (Food Processing, Chemical Processing)

- By Forging Process:

- Open-Die Forging

- Closed-Die Forging

- Ring Rolling

Regional Highlights

- Asia Pacific: This region is anticipated to be the largest and fastest-growing market for stainless steel forgings, driven by rapid industrialization, robust growth in the automotive, construction, and manufacturing sectors, especially in countries like China, India, and Japan. Increased investments in infrastructure development and manufacturing capabilities contribute significantly to demand.

- North America: A mature market with consistent demand from the aerospace, automotive, and oil and gas industries. Technological advancements, a focus on high-performance materials, and significant R&D activities contribute to its steady growth. The region emphasizes precision and specialized forgings for critical applications.

- Europe: Characterized by strong demand from the automotive, industrial machinery, and energy sectors, particularly for high-quality and customized stainless steel forgings. Strict environmental regulations also drive innovation towards more sustainable forging processes. Germany, France, and the UK are key contributors.

- Latin America: Expected to show moderate growth, primarily fueled by investments in infrastructure, mining, and oil and gas exploration. Economic recovery and industrial development in countries like Brazil and Mexico will support the adoption of forged stainless steel components.

- Middle East and Africa (MEA): This region's growth is largely attributed to significant investments in the oil and gas sector, power generation, and infrastructure development. The demand for robust, corrosion-resistant components in harsh environments drives the market, particularly in countries like Saudi Arabia and the UAE.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Stainless Steel Forging Market.- Global Forge Solutions

- Precision Metalcraft Inc.

- Advanced Forgings Group

- Premier Industrial Components

- Superior Forged Products

- Elite Metallurgy Systems

- Apex Forging Technologies

- Continental Metalworks

- Innovative Forged Products

- Horizon Forging Solutions

- Dynamic Forging Industries

- Stellar Steel Components

- Unified Metal Forgings

- Paramount Forged Systems

- Omni Forging Solutions

- Universal Precision Parts

- Grand Forging Works

- National Forged Metals

- Century Forgings

- Masterpiece Forged Alloys

Frequently Asked Questions

What are the primary applications of stainless steel forgings?

Stainless steel forgings are predominantly used in industries requiring high-strength, corrosion-resistant, and durable components. Key applications include critical parts in the automotive sector (engine components, transmission shafts), aerospace (landing gear, turbine blades), industrial machinery (gears, valves), oil and gas (wellhead equipment, pipe fittings), construction (structural components), and power generation (turbine parts, nuclear components).

What factors are driving the growth of the Stainless Steel Forging market?

The market's growth is primarily driven by increasing demand from the automotive (including electric vehicles) and aerospace industries, rising investments in infrastructure and industrial machinery, and the expanding oil and gas sector. Furthermore, advancements in forging technology and the growing need for high-performance, corrosion-resistant materials across various critical applications are significant growth accelerators.

What are the main challenges faced by the Stainless Steel Forging industry?

Key challenges include the volatility of raw material prices (especially nickel and chromium), the high capital investment required for modern forging facilities, stringent environmental regulations, and a persistent shortage of skilled labor. Additionally, competition from alternative manufacturing processes and potential supply chain disruptions can impact market stability.

How is Artificial Intelligence (AI) impacting the Stainless Steel Forging market?

AI is transforming the stainless steel forging market by enabling process optimization, predictive maintenance of machinery, and enhanced quality control through advanced defect detection. It also assists in accelerating design and simulation, improving supply chain efficiency, and automating complex tasks, leading to higher productivity, reduced waste, and improved product consistency.

Which regions are key contributors to the Stainless Steel Forging market?

Asia Pacific is the leading and fastest-growing region due to rapid industrialization and manufacturing expansion in countries like China and India. North America and Europe are mature markets with consistent demand from high-tech industries. The Middle East and Africa show significant growth driven by oil and gas and infrastructure investments, while Latin America is gradually expanding its industrial base.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted