Automotive Forging Market

Automotive Forging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703228 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive Forging Market Size

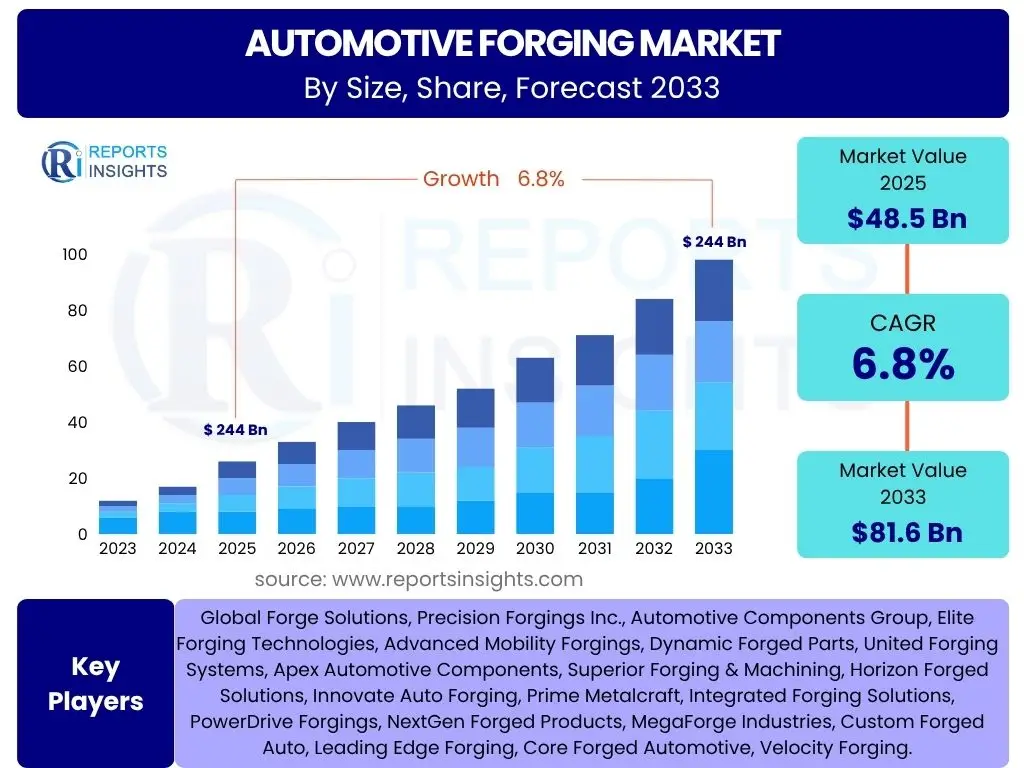

According to Reports Insights Consulting Pvt Ltd, The Automotive Forging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 48.5 billion in 2025 and is projected to reach USD 81.6 billion by the end of the forecast period in 2033.

Key Automotive Forging Market Trends & Insights

The automotive forging market is undergoing significant transformation driven by the shift towards electric vehicles, stringent emission regulations, and the increasing demand for lightweight and high-strength components. Key stakeholders are prioritizing advanced material development and innovative forging processes to meet these evolving industry requirements. Furthermore, the integration of smart manufacturing technologies, including automation and data analytics, is optimizing production efficiency and quality, signaling a strategic evolution within the sector.

Consumer preferences and regulatory pressures are compelling automotive manufacturers to focus on fuel efficiency and reduced carbon footprints, directly impacting component design and material selection. This trend is fostering greater adoption of high-performance alloys and sophisticated forging techniques that can deliver superior strength-to-weight ratios. The competitive landscape is also witnessing consolidation and strategic partnerships as companies aim to enhance their technological capabilities and expand their global footprint, ensuring resilience and adaptability in a dynamic market.

- Growing demand for lightweight components due to EV adoption and fuel efficiency mandates.

- Increased focus on advanced materials like aluminum alloys, titanium, and high-strength steels.

- Integration of automation, robotics, and smart manufacturing processes in forging operations.

- Shift towards complex geometries and near-net shape forging to reduce material waste and machining.

- Emphasis on sustainability and circular economy principles in manufacturing and material sourcing.

- Supply chain regionalization and diversification strategies to enhance resilience.

AI Impact Analysis on Automotive Forging

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is poised to revolutionize the automotive forging industry by enhancing process control, predictive maintenance, and design optimization. Users are keenly interested in how AI can reduce manufacturing defects, improve material utilization, and shorten production cycles. There is a general expectation that AI will lead to higher quality outputs, lower operational costs, and greater operational efficiency across forging plants, addressing long-standing challenges related to consistency and throughput.

However, common concerns revolve around the initial investment required for AI implementation, the need for specialized skills to manage and interpret AI-driven insights, and data security issues associated with highly connected systems. Despite these challenges, the overwhelming sentiment is positive, with industry players seeking to leverage AI for real-time monitoring of forging parameters, anomaly detection, and the development of intelligent tooling. AI's capacity to analyze vast datasets can unlock new levels of precision and adaptability, enabling manufacturers to respond more effectively to dynamic market demands and accelerate innovation in material science and component design.

- Enhanced predictive maintenance of forging equipment, reducing downtime and operational costs.

- Real-time quality control and defect detection through AI-powered vision systems and sensor data analysis.

- Optimization of forging parameters (temperature, pressure, speed) for improved material flow and component integrity.

- Accelerated design and simulation of new forging dies and component geometries, reducing prototyping cycles.

- Improved supply chain management and demand forecasting for raw materials and finished products.

- Robotics and automation integration with AI for autonomous forging operations and material handling.

Key Takeaways Automotive Forging Market Size & Forecast

The projected substantial growth of the automotive forging market underscores its critical role in the evolving automotive landscape, particularly with the global shift towards electric and hybrid vehicles. This growth is driven by the intrinsic need for durable, lightweight, and high-performance components that forging processes inherently provide. Stakeholders should recognize the significant investment opportunities within this sector, not just in traditional forging capabilities but also in advanced materials and smart manufacturing technologies that can unlock new efficiencies and product capabilities.

The market's expansion is not merely quantitative but also qualitative, reflecting a pivot towards more complex and specialized forging solutions. Companies that strategically invest in research and development for new alloys, sustainable manufacturing practices, and AI-driven process enhancements will likely capture a larger share of this growing market. Furthermore, the forecast highlights the importance of adaptability and innovation for forging companies to navigate evolving regulatory environments and fluctuating raw material costs, emphasizing long-term growth potential through technological leadership and strategic foresight.

- Significant growth projected, signaling robust demand for forged automotive components.

- Lightweighting remains a core driver, pushing innovation in material science and forging processes.

- Electric Vehicle (EV) segment presents a major growth catalyst, requiring specialized forging for battery enclosures, motor shafts, and structural components.

- Technological advancements, including automation and AI, are crucial for competitive advantage and operational efficiency.

- Emphasis on sustainable and circular economy practices is becoming a key differentiator.

- Emerging economies in Asia Pacific and Latin America are expected to contribute significantly to market expansion.

Automotive Forging Market Drivers Analysis

The automotive forging market is primarily driven by the escalating demand for lightweight yet high-strength components, which are crucial for improving fuel efficiency in conventional vehicles and extending range in electric vehicles. Stricter global emission regulations are compelling manufacturers to reduce vehicle weight, making forged components an ideal solution due to their superior material integrity and performance. Concurrently, the increasing production volumes of automobiles worldwide, especially in developing regions, further fuel the demand for forged parts for chassis, powertrain, and engine applications.

Technological advancements in forging processes, such as warm and hot forging, precision forging, and hybrid forging techniques, allow for the creation of more complex geometries with less material waste, enhancing overall manufacturing efficiency. The continuous innovation in material science, including the development of advanced high-strength steels and aluminum alloys suitable for forging, also acts as a significant driver. These developments ensure that forging remains a competitive and vital manufacturing process for the modern automotive industry, supporting both performance and sustainability objectives.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweight Components | +1.5% | Global, particularly Europe & North America | Short to Long-term (2025-2033) |

| Growth in Electric Vehicle (EV) Production | +1.2% | Global, particularly Asia Pacific & Europe | Mid to Long-term (2026-2033) |

| Stringent Vehicle Emission Regulations | +1.0% | Europe, North America, China, India | Short to Mid-term (2025-2029) |

Automotive Forging Market Restraints Analysis

The automotive forging market faces significant restraints, including the high initial capital investment required for forging machinery and infrastructure, which can be a barrier for new entrants and small-to-medium enterprises. The volatility of raw material prices, particularly steel and aluminum, directly impacts production costs and profitability, creating unpredictability for manufacturers. Furthermore, intense competition from alternative manufacturing processes such as casting, stamping, and additive manufacturing, which may offer advantages in certain applications or production volumes, poses a challenge to market growth.

Another notable restraint is the ongoing shortage of skilled labor capable of operating and maintaining advanced forging equipment and executing complex forging processes. This human capital challenge can lead to operational inefficiencies and increased labor costs. Additionally, stringent environmental regulations related to energy consumption, emissions, and waste disposal in forging operations require significant compliance investments, adding to the overall cost burden for manufacturers and potentially slowing down expansion initiatives in certain regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Setup Costs | -0.8% | Global, particularly emerging economies | Long-term (2025-2033) |

| Volatility in Raw Material Prices | -0.7% | Global | Short to Mid-term (2025-2028) |

| Competition from Alternative Manufacturing Processes | -0.5% | Global | Mid to Long-term (2026-2033) |

Automotive Forging Market Opportunities Analysis

Significant opportunities in the automotive forging market stem from the accelerating transition to electric vehicles (EVs), which necessitates new types of forged components for battery enclosures, motor shafts, and structural elements designed for weight reduction and crash safety. This shift creates a fresh demand landscape that traditional internal combustion engine (ICE) components cannot fully address, providing a unique avenue for growth and specialization. Furthermore, the ongoing research and development into new lightweight alloys, such as advanced aluminum grades and composite materials amenable to forging, present opportunities for manufacturers to expand their product portfolios and capture higher-value segments.

The adoption of Industry 4.0 technologies, including automation, IoT, and AI, offers immense potential for optimizing forging processes, enhancing efficiency, and reducing costs. Companies embracing smart manufacturing can achieve higher precision, better quality control, and faster turnaround times. Additionally, the expansion of the automotive manufacturing base in emerging economies, coupled with increased consumer purchasing power, creates new geographical markets for forged components. Strategic partnerships and collaborations between forging companies and automotive OEMs can further unlock opportunities by co-developing advanced components tailored to future vehicle architectures and performance requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Electric Vehicle Component Manufacturing | +1.8% | Global, particularly Asia Pacific & Europe | Mid to Long-term (2026-2033) |

| Integration of Smart Manufacturing & AI Technologies | +1.3% | Global | Mid to Long-term (2027-2033) |

| Development of New High-Performance Alloys | +0.9% | North America, Europe, Japan | Long-term (2028-2033) |

Automotive Forging Market Challenges Impact Analysis

The automotive forging market faces several persistent challenges, notably the rapid pace of technological change within the automotive industry, which demands constant adaptation and investment in new forging techniques and materials. Geopolitical uncertainties, trade disputes, and economic downturns can disrupt global supply chains, impacting raw material availability and export opportunities for forged components. Furthermore, the increasing complexity of vehicle designs and the integration of new technologies require forging companies to produce components with tighter tolerances and more intricate geometries, often necessitating significant R&D expenditure.

Another critical challenge is maintaining profitability amidst rising energy costs and the growing pressure to reduce the carbon footprint of manufacturing operations. Forging is an energy-intensive process, and fluctuating energy prices can severely impact margins. Additionally, the threat of intellectual property theft and the need for robust cybersecurity measures for smart factories pose significant risks, potentially undermining competitive advantages and operational security. These factors collectively require forging companies to be agile, innovative, and resilient to navigate the evolving market landscape successfully.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Fluctuations in Energy Prices | -0.6% | Global, particularly Europe | Short to Mid-term (2025-2028) |

| Adaptation to Rapid Automotive Technological Shifts | -0.5% | Global | Mid to Long-term (2026-2033) |

| Global Supply Chain Disruptions | -0.4% | Global | Short to Mid-term (2025-2027) |

Automotive Forging Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automotive Forging Market, offering a detailed segmentation by material type, vehicle type, application, and process. It delves into current market trends, growth drivers, restraints, opportunities, and challenges influencing market dynamics from 2025 to 2033. The scope includes an assessment of the competitive landscape, profiling key players, and an extensive regional analysis spanning North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

The report's objective is to equip stakeholders with actionable insights to make informed strategic decisions, identify emerging market opportunities, and understand the impact of technological advancements, including AI, on the industry. It covers historical data from 2019 to 2023, establishes 2024 as the base year, and provides detailed forecasts up to 2033, serving as a vital resource for market participants seeking to understand and capitalize on the evolving automotive forging sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 48.5 Billion |

| Market Forecast in 2033 | USD 81.6 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Forge Solutions, Precision Forgings Inc., Automotive Components Group, Elite Forging Technologies, Advanced Mobility Forgings, Dynamic Forged Parts, United Forging Systems, Apex Automotive Components, Superior Forging & Machining, Horizon Forged Solutions, Innovate Auto Forging, Prime Metalcraft, Integrated Forging Solutions, PowerDrive Forgings, NextGen Forged Products, MegaForge Industries, Custom Forged Auto, Leading Edge Forging, Core Forged Automotive, Velocity Forging. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive forging market is meticulously segmented to provide a granular understanding of its diverse components and their respective growth trajectories. This segmentation allows for precise analysis of market dynamics across different material types, vehicle types, specific applications, and various forging processes. Each segment presents unique opportunities and challenges, reflecting the evolving technological landscape and demand patterns within the global automotive industry.

By dissecting the market into these key categories, stakeholders can identify high-growth areas, assess competitive advantages, and tailor their strategies to specific niches. The detailed breakdown facilitates a clearer understanding of where investment is most effective, how new technologies are impacting traditional segments, and which segments are poised for significant expansion due to the shift towards electric mobility and lightweighting trends. This comprehensive view is essential for strategic planning and informed decision-making in a rapidly transforming market.

- By Material Type: This segment includes steel forging, aluminum forging, and other materials such as titanium and magnesium. Steel remains dominant due to its strength and cost-effectiveness, while aluminum is rapidly gaining traction due to lightweighting trends.

- By Vehicle Type: Categorization covers passenger vehicles (PC), light commercial vehicles (LCV), heavy commercial vehicles (HCV), and a growing focus on electric vehicles (EVs). Each vehicle type demands distinct forged components tailored to its specific performance and structural requirements.

- By Application: Key applications include powertrain components (crankshafts, connecting rods, camshafts, gears), chassis components (suspension arms, steering knuckles), body components (door hinges, structural parts), axle & drive train components (axle beams, CV joints), and engine components (valves, pistons).

- By Process: Encompasses hot forging, cold forging, warm forging, precision forging, and roll forging. Each process is chosen based on material properties, desired component characteristics, and production efficiency, with precision forging gaining prominence for complex parts.

Regional Highlights

- Asia Pacific: Emerging as the largest and fastest-growing market due to robust automotive production bases in China, India, Japan, and South Korea. The region benefits from increasing domestic demand for vehicles, rapid adoption of electric vehicles, and significant investments in automotive manufacturing infrastructure. Government initiatives promoting local manufacturing and rising disposable incomes further fuel market expansion.

- Europe: A mature but technologically advanced market, driven by stringent emission norms and a strong emphasis on premium and luxury vehicles. Germany, France, and the UK are key contributors, focusing on lightweighting solutions, precision forging, and the development of high-performance components for both ICE and EV platforms. Sustainability initiatives and advanced material research are key drivers.

- North America: Characterized by significant demand for light trucks and SUVs, alongside a growing shift towards electric vehicles. The United States and Mexico lead the market, with an increasing focus on localized production to enhance supply chain resilience. Investments in automation and advanced forging technologies are prevalent, aiming for higher efficiency and quality in automotive component manufacturing.

- Latin America: Showing steady growth, particularly in Brazil and Mexico, driven by increasing vehicle production and a rising middle class. The market is influenced by foreign investments in automotive assembly plants, leading to a consistent demand for forged components. Economic stability and trade agreements play a crucial role in shaping market dynamics.

- Middle East and Africa (MEA): A developing market with potential, primarily driven by investments in infrastructure and a gradual increase in vehicle sales in select countries like Saudi Arabia, UAE, and South Africa. While currently smaller in scale, the region's long-term growth is supported by efforts to diversify economies and establish local manufacturing capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Forging Market.- Global Forge Solutions

- Precision Forgings Inc.

- Automotive Components Group

- Elite Forging Technologies

- Advanced Mobility Forgings

- Dynamic Forged Parts

- United Forging Systems

- Apex Automotive Components

- Superior Forging & Machining

- Horizon Forged Solutions

- Innovate Auto Forging

- Prime Metalcraft

- Integrated Forging Solutions

- PowerDrive Forgings

- NextGen Forged Products

- MegaForge Industries

- Custom Forged Auto

- Leading Edge Forging

- Core Forged Automotive

- Velocity Forging

Frequently Asked Questions

Analyze common user questions about the Automotive Forging market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current size and projected growth of the Automotive Forging Market?

The Automotive Forging Market is estimated at USD 48.5 billion in 2025 and is projected to reach USD 81.6 billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 6.8%. This growth is primarily driven by the increasing demand for lightweight, high-strength components in both traditional and electric vehicles.

How is the rise of Electric Vehicles (EVs) impacting the Automotive Forging Market?

The shift to EVs significantly impacts the automotive forging market by altering demand for specific components. While some traditional powertrain parts may see reduced demand, new opportunities arise for forged components in EV battery enclosures, motor shafts, and lightweight structural parts, which are crucial for extending range and ensuring safety. This shift is driving innovation in material selection and forging processes.

What are the key drivers propelling growth in the Automotive Forging Market?

Key drivers include the escalating global demand for lightweight and high-strength automotive components, increasingly stringent vehicle emission regulations, and the rapid expansion of electric vehicle production. Additionally, continuous technological advancements in forging processes and material science contribute significantly to market growth by enabling more efficient and precise manufacturing.

What challenges does the Automotive Forging Market face?

The market faces challenges such as high initial capital investments for advanced equipment, volatility in raw material prices (e.g., steel and aluminum), intense competition from alternative manufacturing techniques like casting, and the persistent shortage of skilled labor. Additionally, adapting to rapid technological shifts in the automotive industry and navigating global supply chain disruptions pose ongoing hurdles.

Which regions are leading the Automotive Forging Market?

Asia Pacific is currently the largest and fastest-growing region in the Automotive Forging Market, driven by robust automotive manufacturing sectors in China, India, Japan, and South Korea. Europe and North America also hold significant market shares, characterized by strong demand for advanced and lightweight forged components, driven by stringent regulations and technological innovation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted