Precision Tube Market

Precision Tube Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703894 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

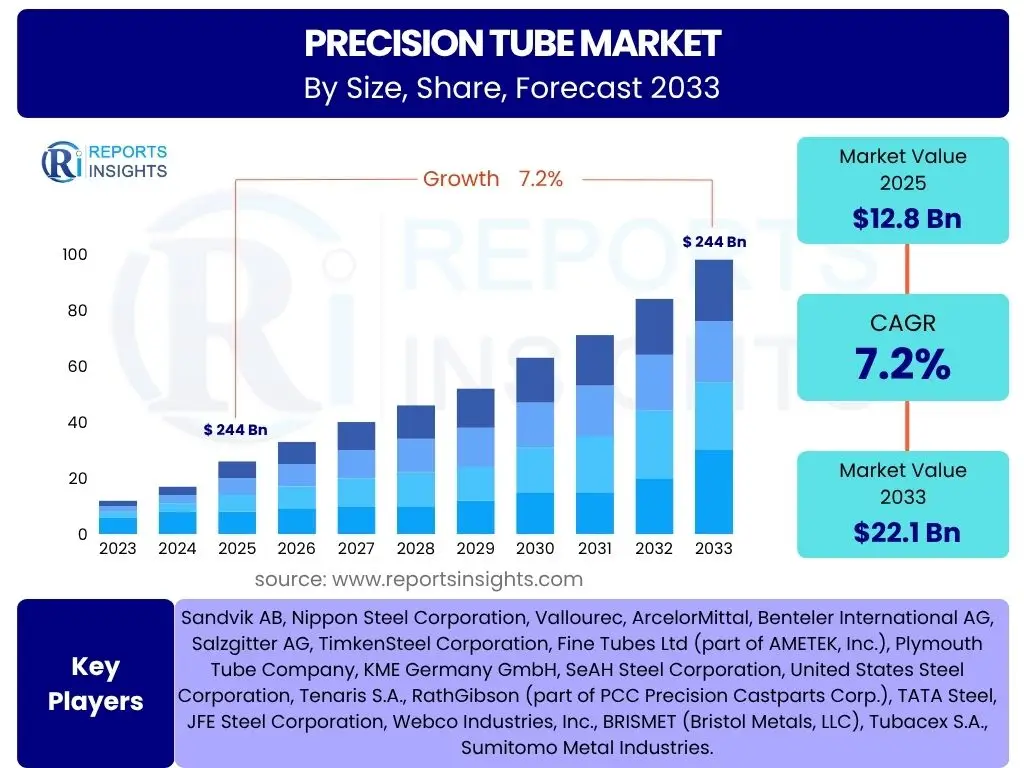

Precision Tube Market Size

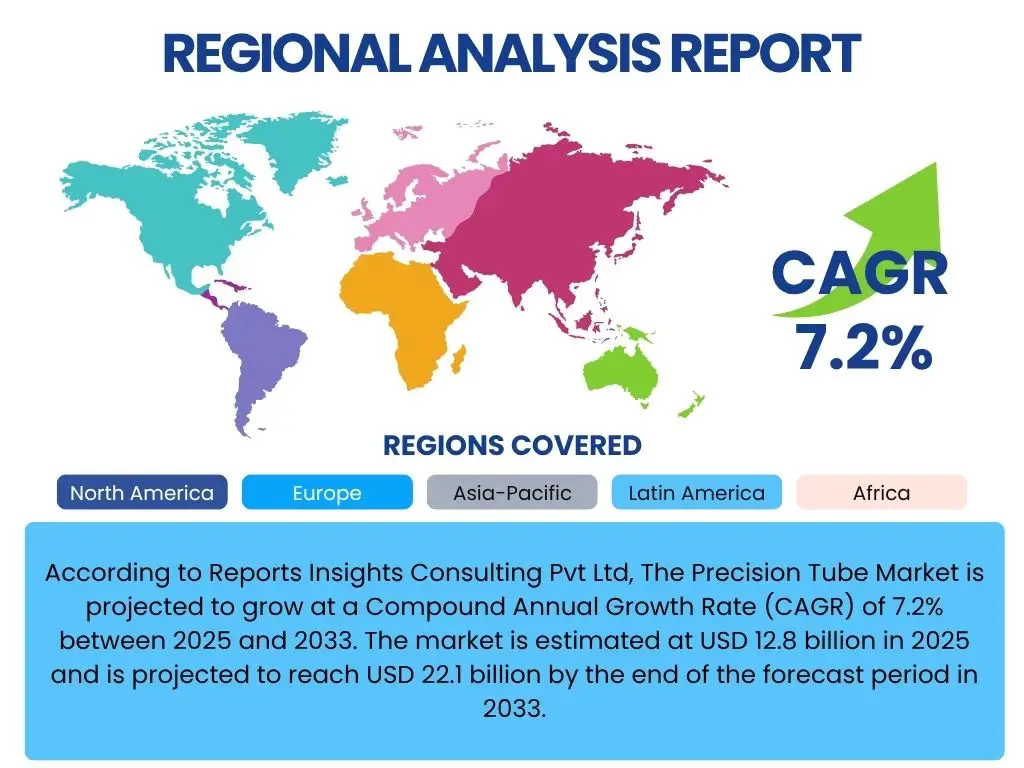

According to Reports Insights Consulting Pvt Ltd, The Precision Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 12.8 billion in 2025 and is projected to reach USD 22.1 billion by the end of the forecast period in 2033.

Key Precision Tube Market Trends & Insights

User queries regarding trends in the precision tube market frequently center on technological advancements, material innovation, and shifting demand patterns across end-use industries. There is significant interest in understanding how new manufacturing processes, such as additive manufacturing, are influencing production capabilities and the properties of precision tubes. Furthermore, questions arise about the increasing adoption of specialized alloys and their impact on performance characteristics and applications in demanding environments. Users also seek information on the evolving regulatory landscape and sustainability initiatives driving market changes.

Another area of focus for user inquiries pertains to the growing demand from high-growth sectors like healthcare, aerospace, and electric vehicles. These industries require tubes with increasingly stringent tolerances, superior material properties, and enhanced corrosion resistance. Consequently, manufacturers are investing in research and development to meet these evolving requirements, leading to the emergence of ultra-precision tubes and micro-tubes for niche applications. The trend towards miniaturization in electronics and medical devices is a recurring theme, highlighting the need for smaller, more precise tubing solutions.

Additionally, users are keen on understanding the regional dynamics influencing market growth, particularly the industrialization trends in Asia Pacific and the recovery of manufacturing sectors in North America and Europe. The global supply chain resilience and the impact of geopolitical factors on raw material availability and pricing are also critical areas of interest, shaping strategic decisions for market participants.

- Increasing adoption of advanced materials such as high-nickel alloys, titanium, and specialized stainless steels.

- Growth in demand from electric vehicle (EV) manufacturing for battery cooling systems and lightweight structures.

- Expansion of minimally invasive surgical procedures driving demand for micro-tubes in medical devices.

- Integration of smart manufacturing and IoT for enhanced process control and quality assurance.

- Rising focus on sustainability and circular economy principles in tube production, including recycling efforts.

AI Impact Analysis on Precision Tube

Common user questions regarding AI's impact on the precision tube market typically revolve around its role in optimizing manufacturing processes, improving quality control, and enabling predictive maintenance. Users are interested in how AI algorithms can analyze vast datasets from production lines to identify anomalies, predict equipment failures before they occur, and enhance overall operational efficiency. There's also curiosity about AI's potential in designing new tube geometries or material compositions, speeding up research and development cycles. The expectation is that AI will lead to higher precision levels, reduced waste, and more cost-effective production, addressing the complex requirements of advanced applications.

Furthermore, inquiries often touch upon the automation aspects of AI, specifically how it contributes to lights-out manufacturing and autonomous quality inspection systems. The implementation of AI-powered vision systems for defect detection and dimensional analysis is seen as a transformative step, moving beyond traditional manual or semi-automated inspection methods. This shift is anticipated to significantly reduce human error and improve the consistency and reliability of precision tubes, which is critical for industries such as aerospace and medical where failures can have severe consequences.

However, user concerns also emerge regarding the initial investment costs, the need for skilled personnel to manage and interpret AI systems, and the data security implications of collecting and processing sensitive manufacturing data. The integration challenges with legacy systems and the ethical considerations surrounding job displacement due to automation are also frequently discussed. Despite these challenges, there is a strong consensus on AI's potential to revolutionize the precision tube industry by enabling unprecedented levels of control, efficiency, and innovation.

- Enhanced predictive maintenance and equipment uptime through AI-driven analytics.

- Optimized manufacturing parameters for improved yield and reduced material waste.

- Automated quality control and defect detection using AI-powered vision systems.

- Accelerated material design and new alloy development through AI simulations.

- Supply chain optimization and demand forecasting for better inventory management.

Key Takeaways Precision Tube Market Size & Forecast

User inquiries about key takeaways from the precision tube market size and forecast consistently highlight the robust growth trajectory, driven primarily by the escalating demand from high-growth end-use sectors. The market's projected expansion reflects significant opportunities for manufacturers specializing in advanced materials and high-tolerance products. A critical insight is the increasing differentiation within the market, where standard tube production is yielding to specialized solutions tailored for specific industrial applications, demanding higher investments in technology and material science expertise.

Another significant takeaway is the strong regional disparities in market growth, with Asia Pacific expected to lead in terms of both production and consumption due to its rapid industrialization and burgeoning manufacturing base, particularly in automotive and electronics. North America and Europe will continue to be vital markets, emphasizing high-value applications in aerospace, medical, and energy sectors, driving innovation in material properties and dimensional accuracy. The forecast underscores the importance of a global presence and diversified client portfolio for market participants to capitalize on varying regional demands.

Furthermore, the market's future is intrinsically linked to technological innovation, including the advent of smart manufacturing, automation, and advanced material processing techniques. Companies that invest in these areas, along with research and development for new alloys and coating technologies, are poised for sustained growth. The report’s insights emphasize that adaptability to evolving industry standards, commitment to stringent quality controls, and strategic partnerships across the value chain will be crucial for competitive advantage in this dynamic market.

- The precision tube market is poised for significant growth, driven by increasing industrial application in demanding sectors.

- Technological advancements in manufacturing processes and material science are critical enablers for market expansion.

- Asia Pacific is projected to be the fastest-growing region, presenting substantial investment and market penetration opportunities.

- Specialization in high-performance materials and ultra-precise dimensions offers a competitive edge.

- Strategic focus on sustainability and compliance with evolving regulatory standards will be essential for long-term success.

Precision Tube Market Drivers Analysis

The global precision tube market is significantly propelled by the escalating demand from key end-use industries that require high-performance, accurate tubing for critical applications. The aerospace and defense sectors, for instance, heavily rely on precision tubes for hydraulic systems, engine components, and structural elements where lightweight and high-strength materials are paramount. Similarly, the automotive industry, particularly with the shift towards electric vehicles, increasingly demands precision tubes for battery cooling lines, brake systems, and fuel injection components, necessitating exceptional durability and corrosion resistance. The expansion of these industries directly correlates with the growth in the precision tube market.

Another major driver is the rapid advancement in the medical device industry, which requires micro-tubes and ultra-precision tubes for minimally invasive surgeries, catheters, and surgical instruments. The stringent quality and biocompatibility requirements in this sector push manufacturers to innovate in materials and production processes, fostering market expansion. Furthermore, the oil and gas industry's continuous need for robust and corrosion-resistant tubing for drilling, exploration, and transportation in harsh environments also contributes substantially to market demand. These sectors' ongoing investments and technological evolutions fuel the need for high-quality precision tubes.

Additionally, the burgeoning industrial sector, including areas such as HVAC, instrumentation, and general engineering, continuously seeks precision tubes for fluid conveyance, heat exchangers, and structural support. The global focus on infrastructure development and renewable energy projects further amplifies this demand. The increasing complexity and performance demands of modern machinery across various industrial applications necessitate precision tubes that can withstand high pressures, temperatures, and corrosive media, thereby driving sustained market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from aerospace & defense sectors | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Expansion of the medical device industry | +1.2% | Global, particularly North America, Europe | 2025-2033 |

| Rising adoption in electric vehicle (EV) manufacturing | +1.0% | Asia Pacific, Europe, North America | 2026-2033 |

| Increasing industrial automation and machinery production | +0.8% | Asia Pacific, Europe | 2025-2033 |

| Advancements in oil & gas exploration and production | +0.7% | Middle East, North America, Latin America | 2025-2030 |

Precision Tube Market Restraints Analysis

The precision tube market faces significant restraints primarily due to the volatility and escalation of raw material prices. Metals such as stainless steel, titanium, nickel, and various specialty alloys, which form the core of precision tube manufacturing, are subject to global commodity market fluctuations, geopolitical tensions, and supply chain disruptions. These price instabilities directly impact production costs, making it challenging for manufacturers to maintain competitive pricing and stable profit margins. The high cost of these advanced materials also translates to higher end-product prices, which can sometimes deter adoption in less critical or cost-sensitive applications, thereby limiting market expansion.

Another substantial restraint is the imposition of stringent environmental regulations and compliance costs, particularly in developed economies. Manufacturing precision tubes involves processes that can generate waste and emissions, leading to increasing pressure from regulatory bodies to adopt cleaner production technologies and waste management practices. Adhering to these regulations often requires significant capital investment in advanced filtration systems, energy-efficient machinery, and sustainable material sourcing, which adds to operational overheads. These compliance burdens can disproportionately affect smaller manufacturers, hindering their growth and innovation capabilities.

Furthermore, the high initial capital investment required for establishing and upgrading precision tube manufacturing facilities acts as a formidable barrier to entry for new players and a restraint for existing ones seeking to expand. The machinery for drawing, welding, heat treatment, and precision finishing is highly specialized and expensive. This, coupled with the need for a highly skilled workforce proficient in operating and maintaining such sophisticated equipment, escalates overall operational costs. The long payback periods for these investments can limit market dynamism and innovation, as companies may be hesitant to undertake significant new projects without clear, long-term market certainty.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile raw material prices | -0.9% | Global | 2025-2033 |

| Stringent environmental regulations & compliance costs | -0.7% | Europe, North America, Asia Pacific | 2025-2033 |

| High initial capital investment & operational costs | -0.6% | Global | 2025-2033 |

| Intense competition and pricing pressure | -0.4% | Global | 2025-2033 |

| Supply chain disruptions and geopolitical instability | -0.3% | Global | 2025-2030 |

Precision Tube Market Opportunities Analysis

The precision tube market presents significant opportunities driven by the expanding scope of applications across various high-growth sectors. The ongoing advancements in medical technology, particularly in robotic surgery and implantable devices, are creating demand for ultra-small, highly precise, and biocompatible tubing made from specialized alloys. This niche but high-value segment offers substantial growth avenues for manufacturers capable of producing micro-tubes with exceptional surface finish and dimensional accuracy. Furthermore, the increasing prevalence of chronic diseases globally fuels the need for sophisticated medical equipment, directly translating into increased demand for precision tubes.

Another compelling opportunity lies in the burgeoning renewable energy sector, encompassing solar, wind, and geothermal power generation. These industries require precision tubes for heat exchangers, fluid conveyance systems, and structural components that can withstand extreme temperatures, pressures, and corrosive environments. As countries worldwide commit to reducing carbon emissions and transitioning to cleaner energy sources, the demand for such specialized tubing is expected to surge. This provides manufacturers with a pathway to diversify their product portfolios and tap into a rapidly expanding market segment.

Moreover, the continuous development of new high-performance alloys and composite materials presents an opportunity for innovation and product differentiation. Manufacturers who invest in research and development to explore these new materials can create tubes with enhanced properties, such as superior strength-to-weight ratios, improved corrosion resistance, and greater thermal stability. This allows them to cater to emerging applications in areas like advanced robotics, high-speed rail, and next-generation defense systems, securing a competitive advantage in a market increasingly defined by material science breakthroughs and specialized application requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from the renewable energy sector | +1.3% | Europe, Asia Pacific, North America | 2025-2033 |

| Emergence of new applications in medical robotics & implants | +1.1% | North America, Europe | 2025-2033 |

| Development of advanced alloys & composite materials | +0.9% | Global | 2025-2033 |

| Increasing industrialization in emerging economies | +0.7% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Focus on lightweighting in automotive & aerospace | +0.6% | Global | 2025-2033 |

Precision Tube Market Challenges Impact Analysis

The precision tube market faces significant challenges, particularly concerning the complexity and cost of maintaining stringent quality control and achieving ultra-high precision standards. Manufacturing tubes with tight tolerances, exceptional surface finishes, and consistent material properties requires sophisticated machinery, advanced metrology equipment, and highly skilled personnel. Any deviation from these standards can lead to product rejection, significant material waste, and reputational damage, especially in critical applications like aerospace or medical where product failure can have catastrophic consequences. The continuous investment in quality assurance systems and training remains a formidable challenge for manufacturers.

Another key challenge is managing the escalating energy costs associated with precision tube production. Processes such as heat treatment, cold drawing, and specialized finishing are energy-intensive, directly impacting operational expenditures. As global energy prices remain volatile and pressure mounts for industries to reduce their carbon footprint, manufacturers are compelled to invest in more energy-efficient technologies and alternative energy sources, adding to their capital outlays. The need to balance energy consumption with production efficiency and environmental compliance presents a complex operational dilemma.

Furthermore, the global supply chain for specialized raw materials and components, crucial for precision tube manufacturing, is prone to disruptions. Geopolitical events, trade disputes, and unforeseen global crises can severely impact the availability and lead times of critical inputs, affecting production schedules and order fulfillment. Manufacturers must navigate complex international logistics, diversify their supplier base, and build resilience into their supply chains to mitigate these risks. This often involves strategic inventory management and the establishment of robust contingency plans, adding layers of complexity to market operations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving and maintaining ultra-high precision standards | -0.8% | Global | 2025-2033 |

| Rising energy costs and sustainability pressures | -0.7% | Europe, North America, Asia Pacific | 2025-2033 |

| Supply chain vulnerabilities & material sourcing complexities | -0.5% | Global | 2025-2030 |

| Skilled labor shortage in advanced manufacturing | -0.4% | North America, Europe, Asia Pacific | 2025-2033 |

| Intellectual property protection & technology diffusion | -0.2% | Global | 2025-2033 |

Precision Tube Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global precision tube market, covering historical data, current market dynamics, and future projections. It segments the market by material type, application, and manufacturing process, offering detailed insights into regional performance and competitive landscapes. The report evaluates key market drivers, restraints, opportunities, and challenges, providing a holistic view of the factors influencing market growth and strategic decision-making for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 22.1 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sandvik AB, Nippon Steel Corporation, Vallourec, ArcelorMittal, Benteler International AG, Salzgitter AG, TimkenSteel Corporation, Fine Tubes Ltd (part of AMETEK, Inc.), Plymouth Tube Company, KME Germany GmbH, SeAH Steel Corporation, United States Steel Corporation, Tenaris S.A., RathGibson (part of PCC Precision Castparts Corp.), TATA Steel, JFE Steel Corporation, Webco Industries, Inc., BRISMET (Bristol Metals, LLC), Tubacex S.A., Sumitomo Metal Industries. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The precision tube market is extensively segmented to provide granular insights into its diverse applications and material compositions. This segmentation allows for a detailed understanding of demand drivers and technological advancements specific to each category, enabling stakeholders to identify niche opportunities and tailor their strategies. The primary segmentation categories include material type, manufacturing process, and end-use application, each influencing the performance characteristics and market value of the precision tubes.

By material, the market distinguishes between various types such as stainless steel, titanium, nickel alloys, carbon steel, and other specialty metals, each chosen for specific properties like corrosion resistance, strength, or temperature tolerance. The manufacturing process segmentation, including seamless, welded, cold drawn, and extruded tubes, highlights the different production methods that impart distinct mechanical properties and surface finishes to the tubes. Lastly, the application-based segmentation showcases the widespread use of precision tubes across critical industries, reflecting the diverse and evolving demands of modern technological advancements.

- By Material:

- Stainless Steel (304, 316, 321, Others)

- Titanium and Titanium Alloys

- Nickel and Nickel Alloys

- Carbon Steel

- Others (Copper, Aluminum, Specialty Alloys)

- By Manufacturing Process:

- Seamless

- Welded (ERW, Drawn, Redrawn)

- Cold Drawn

- Extruded

- By Application:

- Automotive

- Aerospace & Defense

- Medical & Healthcare

- Oil & Gas

- Chemical & Petrochemical

- Power Generation

- HVACR

- Instrumentation

- General Engineering

- Others

Regional Highlights

- North America: A mature market characterized by high demand from aerospace, medical devices, and oil & gas sectors. Focus on high-value, specialized precision tubes with stringent quality requirements. Strong emphasis on innovation and advanced manufacturing technologies.

- Europe: Dominated by robust automotive, chemical, and industrial machinery industries. Significant investments in sustainable manufacturing practices and specialized alloy development. Strong presence of key manufacturers and R&D centers.

- Asia Pacific (APAC): Expected to be the fastest-growing region due to rapid industrialization, expanding automotive production (including EVs), burgeoning electronics, and increasing healthcare infrastructure. China, India, Japan, and South Korea are key contributors to market expansion.

- Latin America: Growing demand from oil & gas, automotive, and construction sectors, particularly in Brazil and Mexico. Potential for growth driven by industrial development and foreign investments.

- Middle East & Africa (MEA): Primarily driven by the oil & gas industry and increasing investments in infrastructure and power generation projects. Opportunities for specialized corrosion-resistant precision tubes.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Precision Tube Market.- Sandvik AB

- Nippon Steel Corporation

- Vallourec

- ArcelorMittal

- Benteler International AG

- Salzgitter AG

- TimkenSteel Corporation

- Fine Tubes Ltd (part of AMETEK, Inc.)

- Plymouth Tube Company

- KME Germany GmbH

- SeAH Steel Corporation

- United States Steel Corporation

- Tenaris S.A.

- RathGibson (part of PCC Precision Castparts Corp.)

- TATA Steel

- JFE Steel Corporation

- Webco Industries, Inc.

- BRISMET (Bristol Metals, LLC)

- Tubacex S.A.

- Sumitomo Metal Industries

Frequently Asked Questions

Analyze common user questions about the Precision Tube market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Precision Tube Market?

The Precision Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033, reaching an estimated USD 22.1 billion by the end of the forecast period.

Which industries are the primary drivers of demand for precision tubes?

Key drivers include the aerospace and defense, medical and healthcare (especially minimally invasive devices), automotive (including electric vehicles), oil and gas, and general engineering sectors, all requiring high-performance and accurate tubing solutions.

How is AI impacting the Precision Tube manufacturing industry?

AI is significantly impacting the industry by enabling predictive maintenance, optimizing manufacturing parameters, enhancing automated quality control through vision systems, and accelerating material design and development, leading to increased efficiency and precision.

What are the main challenges faced by the Precision Tube Market?

Key challenges include maintaining ultra-high precision standards, managing volatile raw material prices, navigating stringent environmental regulations and compliance costs, and addressing supply chain vulnerabilities and skilled labor shortages.

Which regions are expected to show the most significant growth in the Precision Tube Market?

Asia Pacific is anticipated to be the fastest-growing region, driven by rapid industrialization and expansion in manufacturing sectors, while North America and Europe will continue to be vital markets focusing on high-value, specialized applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted