Water Quality Sensor Market

Water Quality Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704431 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

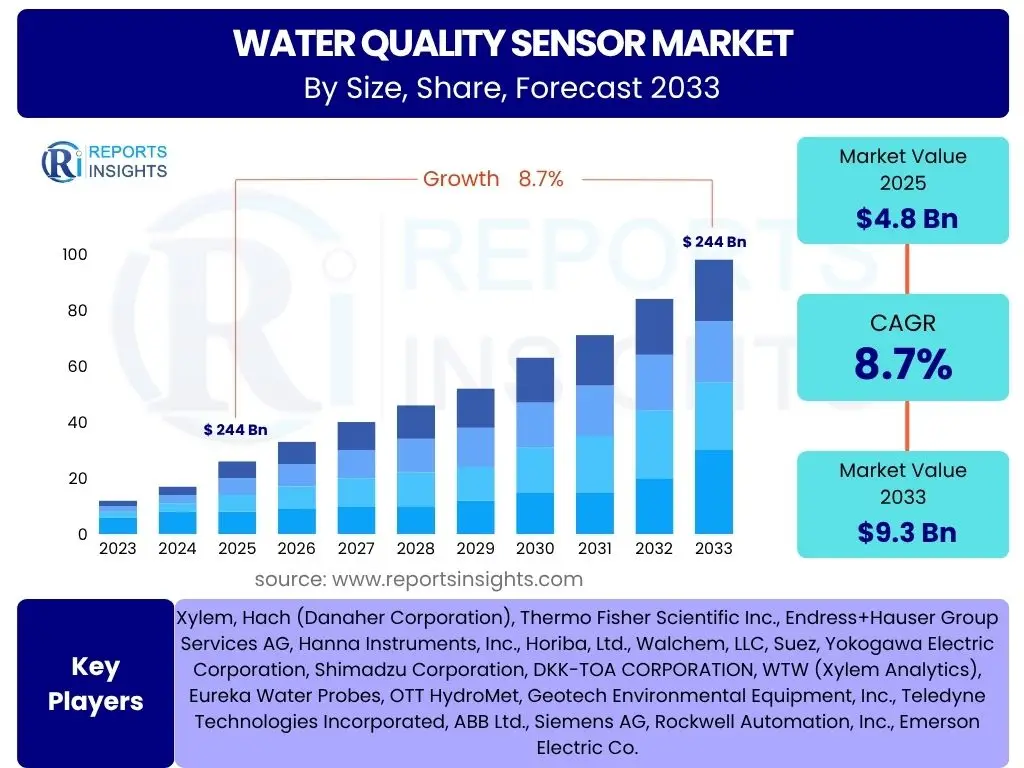

Water Quality Sensor Market Size

According to Reports Insights Consulting Pvt Ltd, The Water Quality Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. This robust growth trajectory is underpinned by increasing global concerns over water scarcity and pollution, coupled with stricter environmental regulations worldwide. The market's expansion is further fueled by rapid advancements in sensor technologies, including the integration of IoT, AI, and miniaturization.

The market is estimated at USD 4.8 Billion in 2025 and is projected to reach USD 9.3 Billion by the end of the forecast period in 2033. This significant increase reflects a rising demand for continuous and accurate water quality monitoring across diverse sectors such as industrial processing, municipal water treatment, environmental surveillance, and aquaculture. Investment in smart water infrastructure and real-time data analytics solutions is also contributing substantially to this projected valuation.

Key Water Quality Sensor Market Trends & Insights

The Water Quality Sensor market is experiencing transformative trends driven by technological innovation, evolving regulatory landscapes, and escalating global water quality challenges. Users frequently inquire about the leading technological advancements and market shifts influencing the adoption and capabilities of water quality sensors. A key insight is the pervasive integration of digital technologies, moving beyond simple measurement to comprehensive, predictive water management systems. This shift is empowering stakeholders with unprecedented levels of data and control over water resources, addressing critical issues from pollution detection to operational efficiency in water treatment plants.

Another prominent trend is the increasing demand for real-time monitoring solutions, spurred by the need for immediate responses to contamination events and for optimizing industrial processes. This demand is leading to the development of more robust, reliable, and network-enabled sensors. Furthermore, the market is witnessing a diversification in application areas, extending beyond traditional environmental monitoring to include sectors like agriculture for smart irrigation and smart cities for urban water management, signifying a broadened scope of utility and market penetration.

- Miniaturization and portability of sensor devices for flexible deployment and ease of use.

- Integration of Internet of Things (IoT) for real-time data transmission, remote monitoring, and cloud-based analytics.

- Adoption of Artificial Intelligence (AI) and Machine Learning (ML) for predictive maintenance, anomaly detection, and advanced data interpretation.

- Development of multi-parameter sensors capable of simultaneously measuring various water quality indicators.

- Increasing demand for autonomous and low-power sensor systems for long-term, remote deployments.

- Focus on enhanced sensor accuracy, stability, and longevity in harsh environmental conditions.

- Growing emphasis on regulatory compliance and stringent water quality standards driving sensor adoption.

- Expansion into smart agriculture, aquaculture, and smart city infrastructure for water resource optimization.

AI Impact Analysis on Water Quality Sensor

User inquiries concerning the impact of Artificial Intelligence (AI) on water quality sensors often revolve around how AI can enhance sensor capabilities, improve data analysis, and contribute to more autonomous water management systems. AI is fundamentally transforming the landscape of water quality monitoring by moving beyond basic data collection to providing predictive insights and enabling smart decision-making. Through machine learning algorithms, sensor data can be analyzed in real-time to identify anomalies, predict potential contamination events, and optimize operational parameters within water treatment facilities, thereby reducing human intervention and improving efficiency. This capability addresses a significant user concern regarding proactive rather than reactive water quality management.

The integration of AI also addresses the challenge of handling vast amounts of data generated by networks of sensors. AI algorithms can process complex datasets, filter out noise, and identify correlations that human analysis might miss, leading to more accurate and actionable insights. Furthermore, AI enables the development of self-calibrating and self-correcting sensor systems, reducing maintenance requirements and ensuring consistent data integrity. This predictive and analytical power of AI is crucial for developing robust, resilient, and adaptive water infrastructure systems globally, allowing for better resource allocation and environmental protection.

- Enhanced data analysis and pattern recognition for identifying subtle changes in water quality.

- Predictive analytics to forecast contamination events or equipment failures, enabling proactive intervention.

- Automated anomaly detection, minimizing false alarms and improving response times to critical incidents.

- Optimization of sensor calibration and maintenance schedules, reducing operational costs and downtime.

- Development of autonomous monitoring systems capable of self-correction and adaptive sampling.

- Improved resource management through AI-driven insights into water usage and treatment efficiency.

- Support for complex decision-making processes in water management and regulatory compliance.

Key Takeaways Water Quality Sensor Market Size & Forecast

Common user questions regarding key takeaways from the Water Quality Sensor market size and forecast often focus on understanding the primary drivers of growth, the segments offering the most promise, and the overall trajectory of the market. A significant takeaway is the strong and sustained growth projected for the market, driven largely by escalating global water scarcity, increasing industrial activities, and the imperative for environmental protection. This growth is not uniform across all segments, with advanced sensor technologies and integrated solutions demonstrating particularly high potential. The market is transitioning from standalone devices to comprehensive, network-enabled monitoring systems.

Another crucial insight is the indispensable role of technological advancements in shaping the market's future. Innovations in IoT, AI, and data analytics are not just enhancing sensor capabilities but are also expanding their applications into new sectors and geographies. The market's resilience is further supported by government initiatives and stringent regulations promoting water quality monitoring and conservation. Consequently, stakeholders across the value chain, from manufacturers to service providers, are positioned for substantial opportunities by aligning with these technological and regulatory shifts.

- The Water Quality Sensor market is poised for significant expansion, driven by environmental concerns and industrial demand.

- Technological advancements, particularly in IoT and AI, are critical enablers of market growth and innovation.

- Demand for real-time, continuous monitoring solutions is accelerating across municipal, industrial, and environmental sectors.

- Stringent regulatory frameworks globally are compelling industries and municipalities to adopt advanced water quality monitoring.

- Asia Pacific and North America are expected to be key growth regions due to industrialization, urbanization, and environmental awareness.

- Investment in smart water infrastructure and digital transformation initiatives will be pivotal for market evolution.

Water Quality Sensor Market Drivers Analysis

The Water Quality Sensor market is propelled by a confluence of powerful drivers, primarily stemming from escalating environmental concerns, stringent regulatory frameworks, and rapid industrialization worldwide. The increasing global population and industrial activities have led to severe water pollution, creating an urgent need for effective monitoring solutions to ensure public health and environmental sustainability. Governments and international bodies are consequently implementing stricter wastewater discharge standards and drinking water quality guidelines, compelling industries and municipalities to invest in advanced sensor technologies to ensure compliance and avoid penalties. This regulatory push is a fundamental catalyst for market expansion, ensuring continuous demand for sophisticated and reliable water quality assessment tools.

Technological advancements also play a critical role, transforming sensor capabilities and broadening their application scope. Innovations in miniaturization, connectivity (IoT), and data analytics (AI/ML) have made sensors more efficient, accurate, and accessible. These advancements enable real-time monitoring, remote data access, and predictive insights, which are invaluable for proactive water management. Furthermore, the growing demand for clean and safe drinking water, coupled with increasing investments in smart city projects and sustainable agriculture practices, further fuels the adoption of water quality sensors. The aquaculture sector, aiming for optimized fish health and yield, also significantly contributes to the demand for precise water quality control.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Environmental Regulations and Standards | +2.5% | Global, particularly Europe, North America, APAC (China, India) | Long-term (2025-2033) |

| Growing Demand for Clean Drinking Water | +2.0% | Global, particularly Developing Economies, MEA, APAC | Long-term (2025-2033) |

| Rapid Industrialization and Urbanization | +1.8% | APAC, Latin America, MEA | Mid to Long-term (2025-2033) |

| Technological Advancements (IoT, AI, Miniaturization) | +1.5% | Global | Short to Long-term (2025-2033) |

| Aging Water Infrastructure and Need for Modernization | +1.2% | North America, Europe | Mid to Long-term (2025-2033) |

| Expansion of Aquaculture and Agriculture Sectors | +0.7% | APAC, Latin America, Europe | Mid-term (2025-2030) |

Water Quality Sensor Market Restraints Analysis

Despite robust growth prospects, the Water Quality Sensor market faces several formidable restraints that could impede its full potential. One significant challenge is the high initial investment cost associated with advanced sensor systems, particularly for comprehensive, multi-parameter monitoring networks. This cost barrier can deter adoption, especially for small and medium-sized enterprises (SMEs) or municipalities with limited budgets in developing regions. Furthermore, the specialized skills required for the installation, calibration, and maintenance of these sophisticated sensors can be a limiting factor, as a shortage of trained personnel can hinder effective deployment and operation.

Another key restraint involves the durability and longevity of sensors in harsh operating environments. Sensors exposed to aggressive chemicals, biofouling, or extreme temperatures may degrade rapidly, leading to frequent replacement and increased operational expenses. Data security and privacy concerns also pose a challenge, particularly with the increasing integration of IoT and cloud-based platforms. Ensuring the integrity and confidentiality of sensitive water quality data is paramount, and any perceived vulnerability can lead to reluctance in adopting networked sensor solutions. These factors necessitate continuous innovation in material science, user-friendliness, and cybersecurity protocols to mitigate their restrictive impact on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Operational Costs | -1.5% | Global, particularly Developing Economies | Long-term (2025-2033) |

| Sensor Calibration, Maintenance, and Fouling Issues | -1.0% | Global | Long-term (2025-2033) |

| Lack of Awareness and Technical Expertise in Certain Regions | -0.8% | MEA, parts of Latin America and APAC | Mid-term (2025-2030) |

| Data Security and Privacy Concerns for IoT-enabled Systems | -0.5% | Global | Mid to Long-term (2025-2033) |

Water Quality Sensor Market Opportunities Analysis

The Water Quality Sensor market is characterized by numerous untapped opportunities for growth and innovation, driven by evolving technological landscapes and expanding application areas. A significant opportunity lies in the burgeoning smart city initiatives globally, which increasingly prioritize intelligent water management systems to ensure sustainable urban development. These initiatives create substantial demand for advanced, networked water quality sensors for monitoring distribution networks, wastewater, and stormwater, presenting lucrative avenues for sensor manufacturers and solution providers.

Furthermore, the integration of water quality sensors with artificial intelligence, machine learning, and big data analytics platforms represents a transformative opportunity. These integrations enable predictive modeling, anomaly detection, and optimized resource allocation, moving beyond mere data collection to offering actionable intelligence. The development of low-cost, portable, and user-friendly sensors also opens up new markets, particularly in remote areas or for small-scale applications, making advanced monitoring accessible to a broader range of users. Lastly, public-private partnerships aimed at improving water infrastructure and promoting environmental sustainability are creating collaborative frameworks for innovative sensor deployment and research, promising sustained growth and market diversification.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with IoT, AI, and Big Data Platforms | +1.8% | Global | Long-term (2025-2033) |

| Development of Low-Cost and Portable Sensor Solutions | +1.5% | Developing Economies, Remote Areas | Mid to Long-term (2025-2033) |

| Expansion into New Application Areas (e.g., Smart Agriculture, Remote Monitoring) | +1.2% | Global | Mid-term (2025-2030) |

| Public-Private Partnerships for Water Infrastructure Modernization | +0.8% | North America, Europe, APAC | Long-term (2025-2033) |

Water Quality Sensor Market Challenges Impact Analysis

The Water Quality Sensor market, while expanding, confronts several significant challenges that necessitate strategic responses from industry participants. One primary challenge is the complexity of data interpretation and management, especially with the proliferation of sensors generating vast volumes of diverse data. Converting raw sensor data into actionable insights requires sophisticated analytical tools and skilled personnel, which can be a bottleneck for many organizations. Ensuring data quality, accuracy, and consistency across varied sensor types and environments further complicates this challenge, impacting decision-making processes.

Another substantial challenge relates to sensor longevity and resilience in harsh operating conditions. Biofouling, chemical corrosion, and physical damage can significantly reduce sensor lifespan and accuracy, leading to frequent maintenance or replacement costs. This is particularly problematic in industrial wastewater or marine environments. Furthermore, achieving standardization across different sensor manufacturers and communication protocols remains a hurdle, hindering seamless integration and interoperability within larger monitoring networks. Addressing these challenges requires continuous research and development into more robust materials, advanced self-cleaning mechanisms, and universally accepted communication standards to foster broader market adoption and ensure reliable long-term performance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Complexity, Interpretation, and Management | -1.2% | Global | Long-term (2025-2033) |

| Sensor Fouling and Longevity in Harsh Environments | -1.0% | Global | Long-term (2025-2033) |

| Lack of Standardization and Interoperability | -0.7% | Global | Mid-term (2025-2030) |

| Competitive Landscape and Price Pressure | -0.5% | Global | Long-term (2025-2033) |

Water Quality Sensor Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Water Quality Sensor Market, offering critical insights into its current size, historical trends, and future growth projections from 2025 to 2033. The scope encompasses detailed market segmentation by type, application, end-use industry, and technology, providing a granular understanding of market dynamics across various dimensions. The report also highlights key growth drivers, formidable restraints, emerging opportunities, and significant challenges impacting the market, accompanied by an analysis of their potential influence on the Compound Annual Growth Rate. Furthermore, it includes a thorough regional analysis, identifying key growth pockets and strategic initiatives within major geographical segments, alongside a detailed competitive landscape profiling the leading players shaping the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 9.3 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Xylem, Hach (Danaher Corporation), Thermo Fisher Scientific Inc., Endress+Hauser Group Services AG, Hanna Instruments, Inc., Horiba, Ltd., Walchem, LLC, Suez, Yokogawa Electric Corporation, Shimadzu Corporation, DKK-TOA CORPORATION, WTW (Xylem Analytics), Eureka Water Probes, OTT HydroMet, Geotech Environmental Equipment, Inc., Teledyne Technologies Incorporated, ABB Ltd., Siemens AG, Rockwell Automation, Inc., Emerson Electric Co. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Water Quality Sensor market is meticulously segmented to provide a detailed understanding of its diverse components and their individual contributions to overall market dynamics. This segmentation allows for targeted analysis of specific product types, applications, end-use industries, and underlying technologies, revealing unique growth patterns, adoption rates, and competitive landscapes within each category. Understanding these segments is crucial for stakeholders to identify lucrative niche markets, tailor product development strategies, and optimize market entry or expansion initiatives.

The multi-faceted segmentation helps to discern the varied demands and requirements across different sectors, from the precise needs of pharmaceutical manufacturing for ultra-pure water to the robust demands of municipal wastewater treatment for continuous monitoring. Each segment is influenced by distinct regulatory environments, technological preferences, and economic factors, making a granular analysis indispensable for an accurate market forecast. This detailed breakdown facilitates strategic planning for market players, allowing them to focus resources on the most promising areas and address specific market challenges effectively.

- By Type: pH Sensors, Conductivity Sensors, Dissolved Oxygen (DO) Sensors, Turbidity Sensors, Oxidation-Reduction Potential (ORP) Sensors, Chlorine Sensors, Nutrient Sensors, Total Organic Carbon (TOC)/Chemical Oxygen Demand (COD) Sensors, Temperature Sensors, Ion-Selective Sensors, and Others.

- By Application: Environmental Monitoring, Industrial Process Monitoring, Wastewater Treatment, Drinking Water Monitoring, Aquaculture, Agriculture, Research and Laboratories, Smart Cities, and Others.

- By End-Use Industry: Municipal, Industrial (Chemical & Petrochemical, Food & Beverage, Pharmaceutical & Biotechnology, Oil & Gas, Power Generation, Mining, Pulp & Paper), Commercial, Residential, and Environmental Agencies & Research Institutions.

- By Technology: Electrochemical Sensors, Optical Sensors, Physical Sensors, Biological Sensors, and Spectroscopic Sensors.

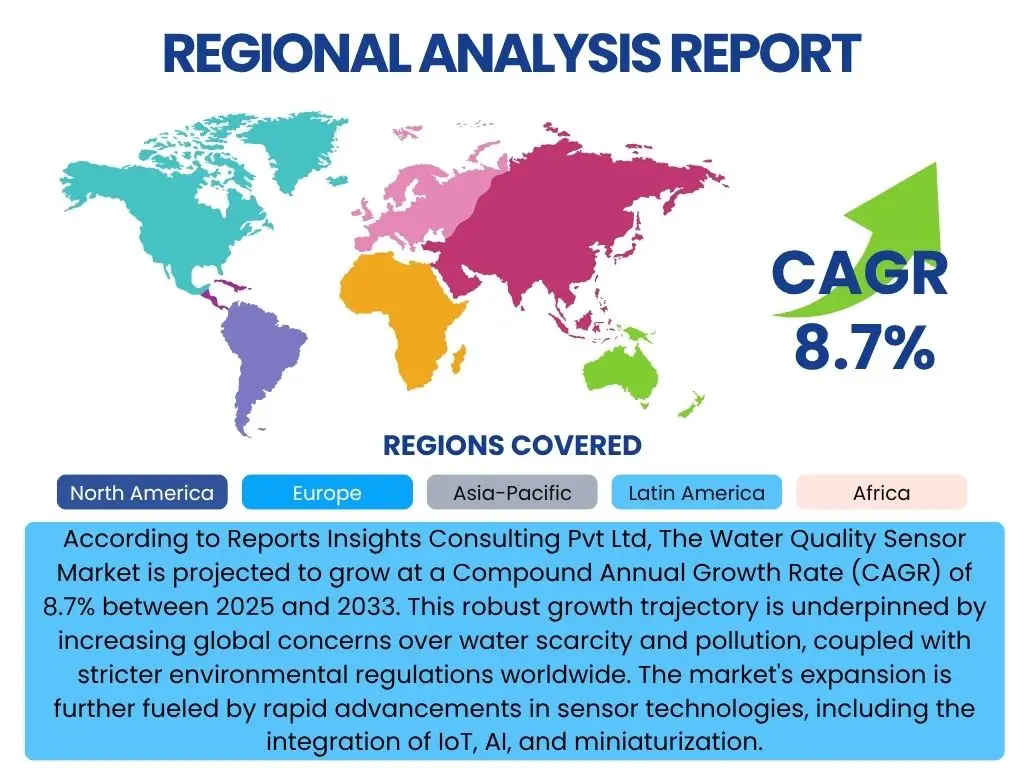

Regional Highlights

- North America: The region demonstrates significant market maturity, driven by stringent environmental regulations, substantial investments in smart water infrastructure, and a strong presence of key market players. The demand for advanced sensor solutions is particularly high in industrial wastewater treatment and municipal drinking water systems, with increasing adoption of IoT-enabled sensors for real-time monitoring and predictive analytics. The U.S. and Canada lead in technology adoption and R&D.

- Europe: Europe is characterized by strict environmental protection policies and a strong emphasis on water quality monitoring and conservation. Countries like Germany, the UK, and France are at the forefront of adopting innovative sensor technologies for both municipal and industrial applications. The region is also witnessing increased deployment of sensors for monitoring aquatic ecosystems and ensuring compliance with EU water directives. Focus on sustainable water management and smart water grids further propels market growth.

- Asia Pacific (APAC): This region is poised for the highest growth rate, fueled by rapid industrialization, urbanization, and a burgeoning population, leading to increased demand for clean water and wastewater treatment. Countries such as China, India, Japan, and South Korea are making significant investments in water infrastructure and environmental protection. The rising awareness of water pollution and supportive government initiatives are key factors driving the adoption of water quality sensors across industrial, agricultural, and municipal sectors.

- Latin America: The market in Latin America is experiencing gradual growth, primarily driven by increasing awareness of water quality issues, growing industrial activities, and governmental efforts to improve water and sanitation infrastructure. Brazil and Mexico are leading the adoption of water quality sensors in the region, particularly for industrial process monitoring and environmental compliance. Challenges include economic instability and a relatively slower pace of regulatory enforcement, but opportunities exist in agricultural applications and remote monitoring.

- Middle East and Africa (MEA): This region faces severe water scarcity issues, making water quality monitoring critical for resource management and desalination processes. Investments in industrial development, particularly in oil and gas and manufacturing, along with increasing efforts to improve public health standards, are driving demand for water quality sensors. Countries like Saudi Arabia, UAE, and South Africa are focusing on developing advanced water treatment facilities, creating opportunities for sensor technology adoption. Challenges include limited infrastructure and diverse regulatory landscapes.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Water Quality Sensor Market.- Xylem

- Hach (Danaher Corporation)

- Thermo Fisher Scientific Inc.

- Endress+Hauser Group Services AG

- Hanna Instruments, Inc.

- Horiba, Ltd.

- Walchem, LLC

- Suez

- Yokogawa Electric Corporation

- Shimadzu Corporation

- DKK-TOA CORPORATION

- WTW (Xylem Analytics)

- Eureka Water Probes

- OTT HydroMet

- Geotech Environmental Equipment, Inc.

- Teledyne Technologies Incorporated

- ABB Ltd.

- Siemens AG

- Rockwell Automation, Inc.

- Emerson Electric Co.

Frequently Asked Questions

Analyze common user questions about the Water Quality Sensor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a water quality sensor and its primary function?

A water quality sensor is an electronic device designed to detect and measure various physical, chemical, and biological parameters of water, such as pH, conductivity, dissolved oxygen, turbidity, and temperature. Its primary function is to provide real-time or near real-time data on water conditions, enabling effective monitoring, management, and protection of water resources for diverse applications like environmental surveillance, industrial processes, and drinking water treatment.

Which industries primarily utilize water quality sensors?

Water quality sensors are extensively utilized across a wide range of industries including municipal water treatment plants for drinking water and wastewater, industrial sectors such as chemical, food & beverage, pharmaceutical, oil & gas, and power generation for process monitoring and effluent discharge control. Additionally, they are crucial in environmental monitoring agencies, aquaculture farms, agriculture (for smart irrigation), and scientific research laboratories.

How does IoT integration impact water quality sensor technology?

IoT integration significantly enhances water quality sensor technology by enabling real-time data transmission, remote monitoring, and cloud-based data storage and analysis. This connectivity allows for continuous surveillance of water bodies and industrial processes, facilitating immediate alerts for anomalies, predictive maintenance, and data-driven decision-making. It transforms standalone sensors into intelligent, networked systems that can be managed from anywhere, improving efficiency and responsiveness.

What are the main challenges in deploying water quality sensors?

Key challenges in deploying water quality sensors include high initial investment costs for advanced systems, the need for regular calibration and maintenance due to sensor fouling or degradation in harsh environments, ensuring data accuracy and reliability, and the complexity of integrating diverse sensor types and data protocols into a unified system. Additionally, data security concerns for networked sensors and a shortage of skilled personnel for installation and interpretation pose significant hurdles.

What is the future outlook for the water quality sensor market?

The future outlook for the water quality sensor market is highly positive, driven by increasing global awareness of water scarcity and pollution, stringent environmental regulations, and ongoing technological advancements. The market is expected to witness robust growth, characterized by greater adoption of AI and machine learning for predictive analytics, the development of more portable and cost-effective sensors, and expanded applications in smart cities, sustainable agriculture, and remote monitoring systems. Continued innovation and regulatory support will ensure sustained expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted