NOx Sensor Market

NOx Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704296 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

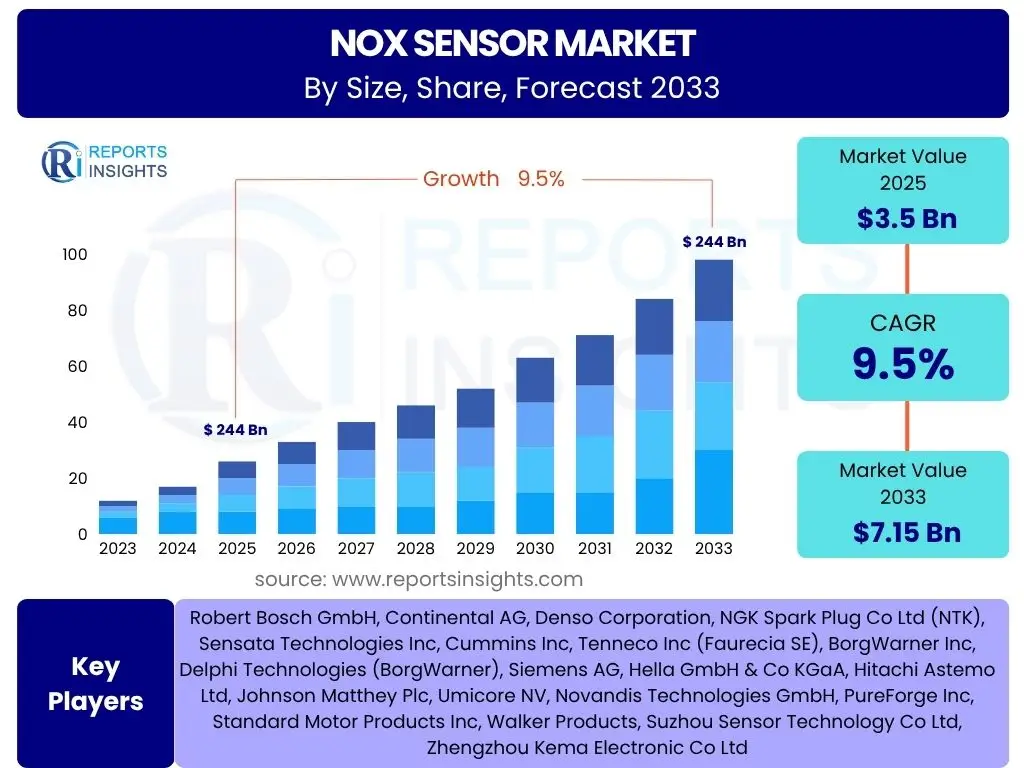

NOx Sensor Market Size

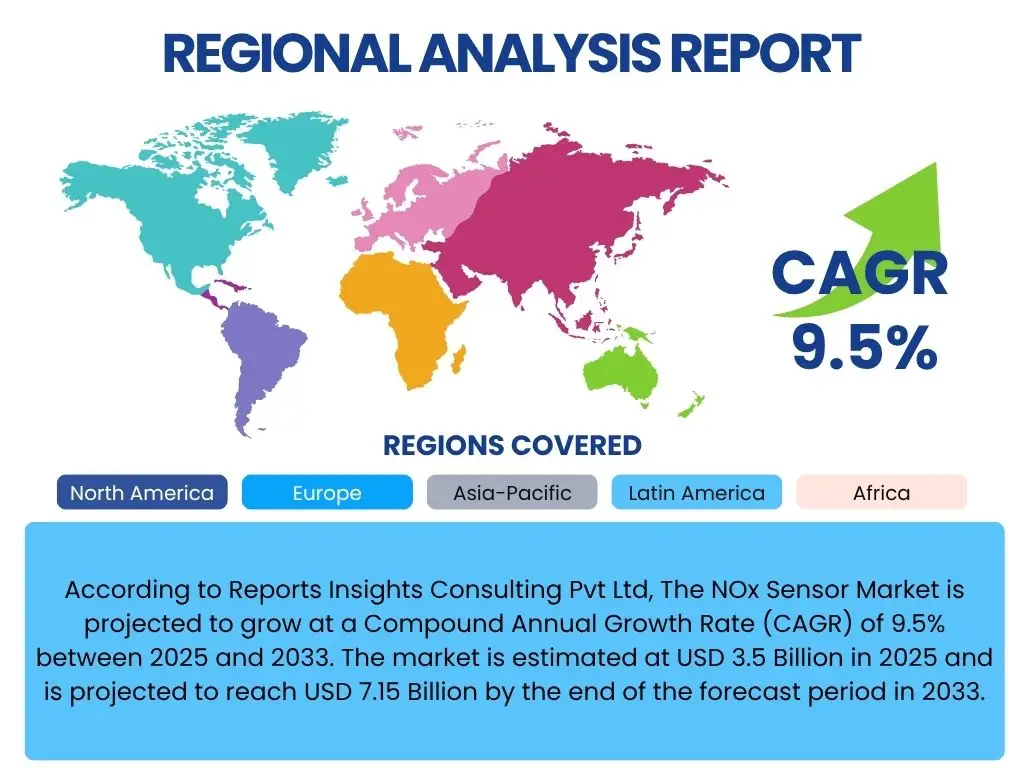

According to Reports Insights Consulting Pvt Ltd, The NOx Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 3.5 Billion in 2025 and is projected to reach USD 7.15 Billion by the end of the forecast period in 2033.

Key NOx Sensor Market Trends & Insights

Common inquiries from stakeholders and market participants consistently highlight several pivotal trends shaping the NOx Sensor market. These questions often revolve around technological advancements, the influence of evolving regulatory landscapes, and the strategic adaptations of manufacturers. A predominant theme is the continuous drive towards enhanced sensor accuracy, durability, and miniaturization, which directly impacts integration capabilities and overall system efficiency. Furthermore, the market is witnessing a notable diversification of applications beyond traditional automotive sectors, extending into industrial, marine, and power generation domains, reflecting a broader societal emphasis on emission control.

Another significant area of interest concerns the long-term viability of NOx sensors in the context of the global shift towards electric vehicles (EVs). While EVs do not require NOx sensors, the sustained growth in hybrid vehicles and internal combustion engine (ICE) vehicles, particularly in emerging economies and commercial fleets, ensures continued demand. Market players are also focusing on developing smart sensors capable of real-time diagnostics and predictive maintenance, leveraging data analytics to improve performance and reduce operational costs. This innovation-driven environment is fostering a competitive landscape where efficiency, reliability, and cost-effectiveness are paramount.

- Stringent global emission regulations, such as Euro 7 and evolving EPA standards, driving demand for advanced NOx monitoring.

- Continuous technological advancements leading to improved sensor materials, enhanced accuracy, and extended durability.

- Increasing integration of NOx sensors with sophisticated vehicle diagnostics and engine control units (ECUs) for optimized performance.

- Growing adoption in non-automotive sectors, including industrial machinery, marine vessels, and power generation plants.

- Development of next-generation sensor technologies, such as solid-state and electrochemical sensors, offering higher precision and faster response times.

- Emphasis on real-time emission monitoring and data analytics for compliance and operational efficiency.

- Miniaturization of sensors for easier integration into diverse vehicle architectures and industrial equipment.

- Rise in demand for NOx sensors in the commercial vehicle and off-highway equipment segments due to stricter regulatory enforcement.

AI Impact Analysis on NOx Sensor

User queries frequently explore the transformative potential of Artificial Intelligence (AI) within the NOx Sensor domain, particularly regarding its ability to enhance sensor performance, data interpretation, and overall emission control strategies. There is a keen interest in how AI algorithms can process complex emission data more efficiently, moving beyond simple detection to predictive analysis and system optimization. Users anticipate AI to play a crucial role in enabling more adaptive and precise calibration of sensors, compensating for environmental variations and sensor aging, thereby extending operational lifespan and maintaining accuracy over time.

Furthermore, discussions highlight AI's prospective contribution to developing intelligent emission control systems that can dynamically adjust engine parameters in real-time based on sensor feedback. This capability could lead to significant reductions in harmful emissions and improvements in fuel efficiency. The integration of AI also holds promise for predictive maintenance, allowing for early detection of sensor malfunctions or performance degradation, thereby minimizing downtime and repair costs. Overall, the market anticipates AI to drive a new era of smart, self-optimizing emission management solutions, significantly impacting the efficacy and sustainability of NOx reduction technologies.

- Enhanced data processing and pattern recognition for real-time emission monitoring and anomaly detection.

- Development of predictive maintenance algorithms to forecast sensor longevity and prevent failures.

- Implementation of adaptive calibration systems that optimize sensor performance in varying operating conditions.

- Integration with engine control units (ECUs) to enable AI-driven optimization of combustion processes for reduced NOx output.

- Advanced analytics for identifying and understanding complex emission signatures from diverse fuel types and engine loads.

- Facilitation of closed-loop emission control systems that continuously learn and adapt for optimal environmental performance.

- Support for remote diagnostics and over-the-air updates for sensor software and calibration models.

Key Takeaways NOx Sensor Market Size & Forecast

Analysis of market inquiries regarding the NOx Sensor market size and forecast reveals a consistent focus on the underlying drivers of growth and the long-term outlook for the technology. Users are keen to understand the primary forces propelling market expansion, particularly the role of escalating environmental concerns and global regulatory mandates. The prevailing sentiment is that despite advancements in electric vehicle technology, the enduring presence of internal combustion engine vehicles, especially in commercial and heavy-duty segments, will ensure sustained demand for NOx sensors well into the forecast period.

Furthermore, stakeholders are interested in the geographical disparities in market growth, recognizing that varying emission standards and adoption rates across regions will influence market dynamics. The key insight is that the market's trajectory is fundamentally linked to global efforts to combat air pollution, making NOx sensors an indispensable component of modern emission control systems. This underscores the market's resilience and its critical role in achieving environmental sustainability targets, positioning it for robust and steady expansion.

- The NOx Sensor market demonstrates robust growth, primarily propelled by increasingly stringent global emission regulations.

- The automotive sector, particularly commercial and heavy-duty vehicles, remains the predominant revenue driver for NOx sensors.

- Significant opportunities are emerging in non-automotive applications, including industrial and marine sectors, expanding the market scope.

- Technological innovation, focusing on enhanced accuracy, durability, and cost-effectiveness, is crucial for competitive advantage and market penetration.

- Regional disparities in emission standards and economic development will lead to varied adoption rates and market growth patterns worldwide.

- The market's long-term forecast indicates sustained demand, even with the rise of electric vehicles, due to the substantial existing and future ICE fleet.

- Investments in research and development for next-generation sensor technologies will be key to unlocking further market potential.

NOx Sensor Market Drivers Analysis

The NOx Sensor market is primarily driven by an accelerating global impetus towards environmental protection and cleaner air. Governments and international bodies are continuously introducing and tightening emission regulations for vehicles and industrial processes, making the accurate monitoring and reduction of nitrogen oxides (NOx) imperative. This regulatory pressure mandates the integration of advanced NOx sensing technologies to ensure compliance and avoid penalties, thereby creating a sustained demand across various sectors. The global automotive industry, in particular, is undergoing significant transformations to meet these stricter standards, positioning NOx sensors as critical components in modern emission control systems.

Beyond regulatory compliance, the market is also propelled by technological advancements that enhance sensor performance, durability, and cost-efficiency. Innovations in materials science and manufacturing processes have led to the development of more robust and reliable sensors capable of operating effectively in harsh environments. Furthermore, the growing awareness among consumers and industries about the health impacts of air pollution is fostering a demand for cleaner technologies, encouraging manufacturers to invest in and adopt advanced emission reduction solutions, including sophisticated NOx sensors.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Global Emission Regulations (e.g., Euro 7, EPA) | +2.5% | Global, particularly Europe, North America, China | Short-to-Mid term (2025-2029) |

| Growing Automotive Production, especially Commercial Vehicles | +1.8% | Asia Pacific (China, India), North America | Mid-to-Long term (2027-2033) |

| Technological Advancements in Sensor Accuracy & Durability | +1.5% | Global | Short-to-Mid term (2025-2029) |

| Increasing Focus on Industrial Emission Monitoring & Control | +1.0% | Europe, North America, Asia Pacific | Mid-to-Long term (2027-2033) |

| Rising Demand for Fuel-Efficient & High-Performance Engines | +0.8% | Global | Mid term (2026-2030) |

NOx Sensor Market Restraints Analysis

Despite significant growth drivers, the NOx Sensor market faces several notable restraints that could temper its expansion. One primary concern is the relatively high manufacturing cost associated with these sophisticated sensors, which can increase the overall cost of vehicles and industrial equipment. This cost factor can be particularly impactful in price-sensitive emerging markets, potentially slowing down the widespread adoption of advanced emission control systems. Additionally, the complex chemical and electrical components required for accurate NOx detection contribute to these higher production expenses, posing a challenge for manufacturers aiming for economies of scale.

Another significant restraint stems from the durability and reliability issues sometimes encountered in NOx sensors due to their exposure to harsh operating environments, including extreme temperatures, vibrations, and corrosive exhaust gases. These conditions can lead to sensor degradation, requiring frequent replacements and maintenance, which adds to the total cost of ownership for end-users. Furthermore, the rapid global transition towards electric vehicles (EVs) represents a long-term existential challenge for the NOx sensor market, as EVs produce zero tailpipe emissions and thus do not require these sensors. While the shift to EVs will not immediately negate demand, it represents a significant market shift that will increasingly impact the long-term growth prospects for ICE-dependent technologies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing and Replacement Costs | -1.2% | Global, particularly price-sensitive markets | Short-to-Mid term (2025-2029) |

| Durability and Reliability Challenges in Harsh Environments | -0.9% | Global | Short term (2025-2027) |

| Accelerated Shift Towards Electric Vehicles (EVs) | -2.0% | Europe, North America, China | Long term (2030-2033) |

| Supply Chain Vulnerabilities and Component Shortages | -0.7% | Global | Short term (2025-2026) |

NOx Sensor Market Opportunities Analysis

The NOx Sensor market is poised for significant opportunities driven by the expanding scope of emission control applications and continuous technological innovation. One major opportunity lies in the burgeoning demand from emerging economies, particularly in Asia Pacific, Latin America, and Africa. As these regions experience rapid industrialization and urbanization, their governments are increasingly adopting and enforcing stricter emission regulations, mirroring the standards of developed nations. This creates vast untapped markets for NOx sensors in both new vehicle sales and the retrofitting of existing fleets and industrial facilities, representing a substantial growth avenue for manufacturers and suppliers.

Furthermore, the development of next-generation sensor technologies presents a compelling opportunity. Research and development efforts are focused on creating more precise, durable, and cost-effective sensors, including solid-state and smart sensors with integrated diagnostic capabilities. These advancements can overcome current market restraints and unlock new applications. The aftermarket segment also offers considerable potential, driven by the need for replacement sensors in older vehicles and industrial equipment to maintain compliance and optimal performance. Additionally, the integration of NOx sensors with advanced vehicle systems, such as IoT and real-time data analytics platforms, can create value-added services and enhance overall emission management efficiency.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets with Developing Regulations | +1.8% | Asia Pacific (India, Southeast Asia), Latin America, MEA | Mid-to-Long term (2027-2033) |

| Development and Commercialization of Next-Generation Sensor Technologies | +1.5% | Global | Mid-to-Long term (2028-2033) |

| Growth in Aftermarket Sales and Replacement Demand | +1.2% | Global | Long term (2029-2033) |

| Integration with IoT and Predictive Maintenance Systems | +1.0% | North America, Europe, China | Mid term (2026-2030) |

| Diversification of Applications into Marine and Off-Highway Segments | +0.9% | Europe, North America, Asia Pacific | Mid-to-Long term (2027-2033) |

NOx Sensor Market Challenges Impact Analysis

The NOx Sensor market navigates various significant challenges that demand strategic responses from industry participants. Intense price competition, particularly from manufacturers in lower-cost regions, pressures profit margins and necessitates continuous innovation to maintain competitive advantage. This competition often leads to a focus on cost reduction, which can sometimes conflict with the imperative for high performance and durability in critical emission control components. Furthermore, the complexity involved in the precise calibration and long-term maintenance of NOx sensors poses operational challenges for vehicle manufacturers and service providers. Ensuring consistent accuracy throughout a sensor's lifespan in varying environmental conditions requires sophisticated algorithms and robust quality control, adding to the operational burden.

Another profound challenge stems from the rapid pace of technological change within the automotive industry, particularly the accelerating transition towards alternative fuel vehicles and electric powertrains. While NOx sensors remain vital for internal combustion engines, the long-term uncertainty regarding the future market share of ICE vehicles presents a strategic dilemma for sensor manufacturers. This forces companies to diversify their product portfolios and invest in new technologies, even as they continue to support existing ICE platforms. Additionally, ensuring the long-term reliability and robustness of sensors in harsh operating environments, where they are exposed to extreme temperatures, vibrations, and corrosive gases, remains a persistent engineering challenge that directly impacts product reputation and market acceptance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition Among Manufacturers | -0.8% | Global | Short-to-Mid term (2025-2029) |

| Complexity of Calibration and Maintenance Requirements | -0.6% | Global | Mid term (2026-2030) |

| Technological Obsolescence Due to EV Transition | -1.5% | Europe, North America, China | Long term (2030-2033) |

| Ensuring Long-term Reliability in Harsh Operating Environments | -0.7% | Global | Mid term (2026-2030) |

| Managing Complex and Fragmented Supply Chains | -0.5% | Global | Short term (2025-2027) |

NOx Sensor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global NOx Sensor market, encompassing its current landscape, historical performance from 2019 to 2023, and future projections through 2033. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and key challenges impacting the industry. It covers various market segmentations by technology, vehicle type, application, fuel type, and component, offering granular insights into market dynamics. The report also features a thorough regional analysis highlighting key country-level developments and profiles of leading market participants, providing a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 7.15 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Continental AG, Denso Corporation, NGK Spark Plug Co Ltd (NTK), Sensata Technologies Inc, Cummins Inc, Tenneco Inc (Faurecia SE), BorgWarner Inc, Delphi Technologies (BorgWarner), Siemens AG, Hella GmbH & Co KGaA, Hitachi Astemo Ltd, Johnson Matthey Plc, Umicore NV, Novandis Technologies GmbH, PureForge Inc, Standard Motor Products Inc, Walker Products, Suzhou Sensor Technology Co Ltd, Zhengzhou Kema Electronic Co Ltd |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The NOx Sensor market is comprehensively segmented to provide a detailed understanding of its diverse components and evolving demand patterns. This segmentation allows for precise market sizing and forecasting, identifying key growth areas and niche opportunities. By categorizing the market based on various parameters such as technology, vehicle type, application, fuel type, and component, stakeholders can gain granular insights into specific market dynamics, technological preferences, and regional adoption trends. This structured approach facilitates strategic planning, enabling market players to tailor their product offerings and business development efforts to specific high-potential segments.

- By Technology:

- Ceramic NOx Sensors

- Electrochemical NOx Sensors

- Infrared (IR) NOx Sensors

- Others (e.g., Optical, Solid-State)

- By Vehicle Type:

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy-Duty Commercial Vehicles (HDVs)

- Off-Highway Vehicles

- Construction Equipment

- Agricultural Equipment

- Mining Equipment

- By Application:

- Automotive

- Original Equipment Manufacturer (OEM)

- Aftermarket

- Industrial

- Power Generation Plants

- Marine Vessels

- Industrial Furnaces and Boilers

- Oil and Gas Facilities

- Others (e.g., Chemical Processing)

- Automotive

- By Fuel Type:

- Gasoline Engines

- Diesel Engines

- Alternative Fuel Engines (e.g., CNG, LPG, Hybrid)

- By Component:

- Sensor Element

- Control Unit (ECU)

- Wiring Harness

- Catalytic Converter Integration Modules

Regional Highlights

- North America: This region is characterized by stringent emission standards enforced by the Environmental Protection Agency (EPA) and California Air Resources Board (CARB), driving consistent demand for NOx sensors in both automotive and industrial sectors. The presence of major automotive OEMs and a strong aftermarket further contributes to market growth. Focus on heavy-duty truck and off-highway equipment emission reduction is particularly significant.

- Europe: A pioneer in adopting advanced emission regulations, with standards like Euro 6 and the upcoming Euro 7 compelling significant integration of NOx sensors. Europe's strong automotive manufacturing base, coupled with increasing environmental awareness and investments in green technologies, positions it as a leading market for sensor adoption across passenger, commercial, and marine applications.

- Asia Pacific (APAC): Expected to be the fastest-growing market due to rapid industrialization, increasing vehicle production, and the gradual implementation of stricter emission norms, particularly in countries like China and India. The expanding middle class and growing demand for commercial vehicles are key drivers. Japan and South Korea also contribute significantly through technological innovation and stringent domestic regulations.

- Latin America: This region presents an emerging market with growing awareness of air pollution and the gradual adoption of emission control technologies. While regulations may not be as stringent as in developed economies, increasing urbanization and vehicle parc growth are expected to drive demand for NOx sensors, especially in the commercial vehicle segment.

- Middle East and Africa (MEA): The MEA region is characterized by a gradual increase in regulatory oversight concerning vehicle emissions, often influenced by European and American standards. Demand for NOx sensors primarily stems from the import of advanced vehicles and increasing industrial projects that require emission monitoring. The market here is still nascent but poised for growth as environmental regulations become more pervasive.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the NOx Sensor Market.- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- NGK Spark Plug Co Ltd (NTK)

- Sensata Technologies Inc

- Cummins Inc

- Tenneco Inc (Faurecia SE)

- BorgWarner Inc

- Delphi Technologies (BorgWarner)

- Siemens AG

- Hella GmbH & Co KGaA

- Hitachi Astemo Ltd

- Johnson Matthey Plc

- Umicore NV

- Novandis Technologies GmbH

- PureForge Inc

- Standard Motor Products Inc

- Walker Products

- Suzhou Sensor Technology Co Ltd

- Zhengzhou Kema Electronic Co Ltd

Frequently Asked Questions

What is a NOx sensor and why is it crucial for vehicles?

A NOx sensor (Nitrogen Oxide sensor) is a critical component in the exhaust system of internal combustion engine vehicles, particularly diesel engines. It measures the concentration of nitrogen oxides, which are harmful pollutants, in the exhaust gases. This measurement is crucial because it allows the vehicle's engine control unit (ECU) to optimize the engine's combustion process and the efficiency of the Selective Catalytic Reduction (SCR) system, ensuring compliance with stringent emission regulations and reducing environmental impact.

How do global emission regulations impact the NOx sensor market?

Global emission regulations, such as Euro 6/7 in Europe and EPA standards in North America, are the primary drivers of the NOx sensor market. These regulations mandate significant reductions in harmful pollutants, including NOx, from vehicle exhaust and industrial emissions. Consequently, manufacturers are compelled to integrate advanced NOx sensors into their systems to meet compliance requirements, fostering continuous demand and technological advancements in the sensor market.

What are the primary technologies used in NOx sensors?

The primary technologies used in NOx sensors include ceramic (zirconia-based) sensors, which are widely adopted due to their robustness and accuracy, and electrochemical sensors. Ceramic sensors typically operate at high temperatures and measure the concentration of NOx by monitoring oxygen ion conductivity. Research and development are also exploring infrared (IR) and solid-state technologies for enhanced performance, durability, and cost-effectiveness in diverse applications.

How is the rise of electric vehicles (EVs) affecting the NOx sensor market?

The rise of electric vehicles (EVs) represents a long-term challenge for the NOx sensor market, as EVs produce zero tailpipe emissions and do not require NOx sensors. However, the market for internal combustion engine (ICE) vehicles, particularly in commercial, heavy-duty, and hybrid segments, is expected to remain substantial for the foreseeable future. This ensures continued, albeit evolving, demand for NOx sensors, prompting manufacturers to innovate and diversify into non-automotive industrial applications to mitigate the long-term impact of EV adoption.

Which regions are leading the adoption and innovation in NOx sensor technology?

Europe and North America are leading regions in the adoption and innovation of NOx sensor technology due to their early implementation of stringent emission regulations and robust automotive industries. Asia Pacific, particularly China and India, is emerging as a significant growth market, driven by rapid industrialization and increasing governmental focus on air quality, leading to accelerated adoption of emission control technologies, including advanced NOx sensors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted