Water Quality Monitoring Sensor Market

Water Quality Monitoring Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704313 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

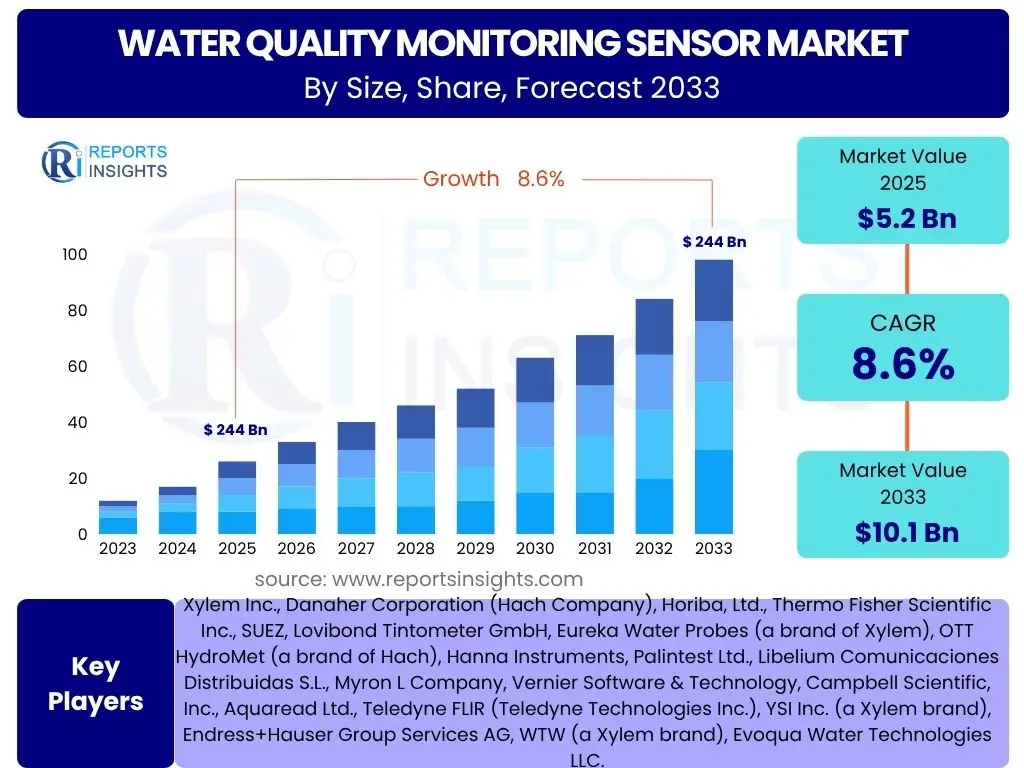

Water Quality Monitoring Sensor Market Size

According to Reports Insights Consulting Pvt Ltd, The Water Quality Monitoring Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.6% between 2025 and 2033. The market is estimated at USD 5.2 Billion in 2025 and is projected to reach USD 10.1 Billion by the end of the forecast period in 2033.

Key Water Quality Monitoring Sensor Market Trends & Insights

The water quality monitoring sensor market is experiencing dynamic shifts driven by escalating environmental concerns, stringent regulatory frameworks, and rapid technological advancements. Users frequently inquire about the integration of smart technologies, the demand for real-time data, and the emergence of more precise and versatile sensing solutions. These inquiries highlight a collective interest in how monitoring capabilities are evolving to address complex water quality challenges globally, moving beyond traditional methods to incorporate digitalization and automation for more efficient and comprehensive analysis.

A significant trend involves the miniaturization and increased portability of sensors, enabling broader deployment in remote or previously inaccessible locations. This is complemented by the growing adoption of IoT-enabled devices, which facilitate continuous, remote data transmission and analytics. The market is also witnessing a surge in multi-parameter sensors capable of simultaneously measuring several indicators, significantly enhancing efficiency and accuracy in complex environmental scenarios. The drive for sustainability and resource optimization underpins many of these technological advancements, pushing manufacturers to develop more durable, energy-efficient, and cost-effective monitoring solutions.

- Integration of Internet of Things (IoT) for real-time data collection and remote monitoring.

- Development of smart, connected sensors offering predictive analytics capabilities.

- Increasing adoption of multi-parameter sensors for comprehensive water quality assessment.

- Miniaturization and enhanced portability of sensor devices for diverse applications.

- Rising demand for autonomous underwater vehicles (AUVs) and drones equipped with sensors.

- Emphasis on energy-efficient and sustainable sensor technologies.

- Advancements in cloud-based data storage and analytical platforms for water quality data.

AI Impact Analysis on Water Quality Monitoring Sensor

Common user questions regarding AI's impact on water quality monitoring sensors often revolve around its ability to enhance data accuracy, automate processes, and provide predictive insights. Users are keen to understand how artificial intelligence can move beyond simple data logging to offer actionable intelligence, such as anticipating pollution events or optimizing treatment processes. There is also interest in AI's role in improving sensor calibration, anomaly detection, and reducing human intervention, thereby lowering operational costs and increasing system reliability.

Artificial intelligence is revolutionizing the water quality monitoring sensor landscape by enabling sophisticated data interpretation and predictive modeling. AI algorithms can process vast amounts of sensor data, identifying subtle patterns and anomalies that might be imperceptible to human analysis. This capability allows for more accurate real-time assessments of water quality, early detection of contamination, and proactive management of water resources. Furthermore, AI contributes to optimizing sensor network deployment and maintenance schedules, leading to more efficient and cost-effective monitoring operations.

The application of AI also extends to improving sensor performance through advanced calibration techniques and drift compensation, ensuring long-term accuracy and reliability. AI-powered systems can learn from historical data to predict future water quality trends, which is invaluable for water resource planning, emergency response, and regulatory compliance. While challenges exist regarding data quality and model interpretability, the transformative potential of AI in creating more intelligent, autonomous, and responsive water quality monitoring systems is undeniable, fostering greater confidence in water safety and environmental protection.

- Enhancement of predictive analytics for anticipating water quality issues and pollution events.

- Automated anomaly detection and real-time alert systems for immediate response.

- Optimization of sensor network deployment and data collection strategies.

- Improved data interpretation and complex pattern recognition for comprehensive insights.

- Development of self-calibrating and self-correcting sensor systems.

Key Takeaways Water Quality Monitoring Sensor Market Size & Forecast

Common user inquiries about key takeaways from the water quality monitoring sensor market size and forecast frequently focus on identifying primary growth drivers, understanding regional market dynamics, and anticipating future technological advancements. Users seek concise summaries of market expansion opportunities, the influence of regulatory changes, and the role of innovation in sustaining market momentum. These questions underscore a desire for strategic insights that can inform investment decisions, product development, and market entry strategies within this crucial sector.

The water quality monitoring sensor market is poised for robust and sustained growth through 2033, driven fundamentally by increasing global awareness of water pollution and the imperative for effective water resource management. Stringent environmental regulations imposed by governments worldwide are mandating higher standards for industrial discharges and municipal wastewater treatment, compelling industries and utilities to adopt advanced monitoring solutions. This regulatory pressure, coupled with a growing demand for safe drinking water, forms the bedrock of market expansion.

Technological innovation, particularly in sensor miniaturization, IoT integration, and AI-driven data analytics, is a significant catalyst for market growth. These advancements enable more precise, real-time, and cost-effective monitoring, broadening the application scope of water quality sensors across various sectors. The Asia Pacific region is expected to emerge as a dominant growth hub, propelled by rapid industrialization, urbanization, and a heightened focus on environmental protection initiatives. Overall, the market's trajectory indicates a shift towards more intelligent, interconnected, and comprehensive monitoring systems designed to address complex water challenges efficiently.

- The market exhibits strong growth potential, driven by global water quality degradation and regulatory mandates.

- Technological advancements, including IoT and AI, are pivotal in enabling advanced monitoring solutions.

- Asia Pacific is anticipated to be a major growth engine due to rapid industrial and infrastructure development.

- Increasing public and private investment in water infrastructure and treatment facilities is a key accelerant.

- Real-time, continuous monitoring solutions are gaining precedence over traditional spot testing methods.

Water Quality Monitoring Sensor Market Drivers Analysis

The escalating global water pollution levels represent a primary driver for the water quality monitoring sensor market. Rapid industrialization, agricultural run-off, and urbanization contribute significantly to the contamination of water bodies, necessitating continuous and accurate monitoring to protect ecosystems and human health. This pervasive issue creates a constant demand for advanced sensing technologies capable of detecting a wide range of pollutants, from heavy metals to emerging contaminants, thereby ensuring the safety and potability of water resources.

Stringent environmental regulations and government initiatives aimed at preserving water quality are also instrumental in driving market growth. Regulatory bodies globally are implementing stricter limits on discharge parameters for industries and municipalities, making water quality compliance a non-negotiable aspect of operations. These regulations often mandate the use of certified monitoring equipment and real-time data reporting, directly stimulating the demand for sophisticated water quality sensors. Furthermore, public awareness campaigns and increasing community engagement regarding environmental protection are putting pressure on authorities and industries to adopt more proactive monitoring measures, fostering market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Water Pollution Levels | +2.5% | Global, particularly Asia Pacific & Africa | Short to Long-term |

| Stringent Environmental Regulations | +2.0% | North America, Europe, China | Medium to Long-term |

| Growing Demand for Real-time Monitoring | +1.8% | Global, particularly Developed Economies | Short to Medium-term |

| Advancements in Sensor Technology | +1.5% | Global | Short to Medium-term |

| Expansion of Industrial and Municipal Infrastructure | +1.2% | Emerging Economies, particularly APAC | Medium to Long-term |

Water Quality Monitoring Sensor Market Restraints Analysis

Despite significant market potential, the water quality monitoring sensor market faces several notable restraints, primarily related to the high initial investment costs associated with advanced monitoring systems. The deployment of comprehensive sensor networks, particularly those incorporating IoT and AI capabilities, often requires substantial capital outlay for equipment purchase, installation, and software integration. This high upfront cost can be a barrier for smaller municipalities, developing regions, and small to medium-sized enterprises (SMEs), limiting their adoption of cutting-edge solutions and potentially slowing overall market growth.

Another significant restraint is the technical complexity involved in the operation and maintenance of sophisticated water quality sensors. These systems often require specialized expertise for calibration, data interpretation, and troubleshooting, which can be challenging for organizations with limited technical staff or training resources. Furthermore, sensor fouling, a common issue in various water environments, necessitates frequent cleaning and recalibration, adding to operational expenditures and potentially impacting data accuracy. The need for regular maintenance and the associated costs can deter potential users, especially in remote or difficult-to-access monitoring locations, thus impeding wider market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Operational Costs | -1.5% | Developing Regions, SMEs Globally | Short to Medium-term |

| Technical Complexities and Maintenance Requirements | -1.0% | Global, particularly less technically advanced regions | Medium-term |

| Lack of Awareness and Standardization | -0.8% | Emerging Markets | Medium-term |

| Data Management and Security Concerns | -0.7% | Global | Short to Medium-term |

| Limited Lifespan and Calibration Needs of Sensors | -0.5% | Global | Long-term |

Water Quality Monitoring Sensor Market Opportunities Analysis

The burgeoning smart city initiatives worldwide present a significant growth opportunity for the water quality monitoring sensor market. As urban centers prioritize smart infrastructure development, the integration of advanced water quality sensors into smart grids, intelligent water management systems, and public health networks becomes imperative. These initiatives emphasize real-time data collection, efficient resource allocation, and predictive capabilities to ensure sustainable water supply and sanitation for growing populations. This trend opens new avenues for sensor manufacturers and solution providers to offer integrated and scalable monitoring systems that contribute to urban resilience and environmental sustainability.

Another key opportunity lies in the expanding applications across diverse sectors such as aquaculture, agriculture, and industrial Internet of Things (IIoT). In aquaculture, precise water quality monitoring is crucial for fish health and productivity, while in agriculture, smart irrigation systems utilize sensors to optimize water usage and prevent run-off contamination. The broader adoption of IIoT across manufacturing and processing industries is driving demand for sensors that can monitor discharge quality and process water in real-time, ensuring compliance and operational efficiency. These specialized applications represent niche but high-growth segments where tailored sensor solutions can address specific industry needs and drive market diversification.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Smart Cities and Smart Water Initiatives | +1.8% | North America, Europe, Asia Pacific (China, India) | Medium to Long-term |

| Growth in Aquaculture and Agriculture Applications | +1.5% | Asia Pacific, Latin America | Short to Medium-term |

| Development of Low-Cost and Portable Sensors | +1.2% | Developing Economies, Remote Areas | Short to Medium-term |

| Integration with Industrial IoT and Cloud Platforms | +1.0% | Global | Medium-term |

| Focus on Water Recycling and Reuse Programs | +0.9% | Middle East, Arid Regions, Developed Countries | Long-term |

Water Quality Monitoring Sensor Market Challenges Impact Analysis

The water quality monitoring sensor market faces significant challenges, primarily related to sensor fouling and calibration issues. In aquatic environments, sensors are highly susceptible to fouling by biological growth, mineral deposits, and particulate matter, which can severely degrade accuracy and require frequent cleaning and recalibration. This issue leads to increased operational costs and can compromise the reliability of continuous monitoring data, particularly in long-term deployments or harsh conditions. Overcoming sensor fouling necessitates ongoing research into anti-fouling coatings and self-cleaning mechanisms, which are still evolving.

Another critical challenge is ensuring data security and managing the vast amounts of data generated by extensive sensor networks. As more sensors become connected via IoT, the vulnerability to cyber threats increases, posing risks to data integrity and system control. Furthermore, processing, storing, and deriving meaningful insights from high-volume, real-time data streams require robust data management infrastructure and advanced analytical capabilities. The lack of standardized data protocols and interoperability between different sensor systems also presents a barrier, complicating the integration of diverse monitoring solutions and hindering a unified approach to water quality assessment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Sensor Fouling and Calibration Issues | -1.2% | Global | Ongoing |

| Data Security and Management Complexities | -1.0% | Global | Medium to Long-term |

| High Power Consumption for Remote Deployments | -0.8% | Remote and Developing Regions | Short to Medium-term |

| Lack of Standardization and Interoperability | -0.7% | Global | Long-term |

| Environmental Factors Affecting Sensor Performance | -0.5% | Specific Climatic Regions | Ongoing |

Water Quality Monitoring Sensor Market - Updated Report Scope

This report provides an in-depth analysis of the global water quality monitoring sensor market, covering market size estimations, growth forecasts, key trends, and a comprehensive examination of drivers, restraints, opportunities, and challenges influencing the industry from 2025 to 2033. It includes detailed segmentation analysis by sensor type, application, end-user, technology, and portability, alongside regional market insights and competitive landscape assessment, offering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.2 Billion |

| Market Forecast in 2033 | USD 10.1 Billion |

| Growth Rate | 8.6% |

| Number of Pages | 255 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Xylem Inc., Danaher Corporation (Hach Company), Horiba, Ltd., Thermo Fisher Scientific Inc., SUEZ, Lovibond Tintometer GmbH, Eureka Water Probes (a brand of Xylem), OTT HydroMet (a brand of Hach), Hanna Instruments, Palintest Ltd., Libelium Comunicaciones Distribuidas S.L., Myron L Company, Vernier Software & Technology, Campbell Scientific, Inc., Aquaread Ltd., Teledyne FLIR (Teledyne Technologies Inc.), YSI Inc. (a Xylem brand), Endress+Hauser Group Services AG, WTW (a Xylem brand), Evoqua Water Technologies LLC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The water quality monitoring sensor market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a detailed analysis of specific sensor types, their applications across various industries, the primary end-users, underlying technologies, and the degree of portability, allowing for targeted market strategies and product development. Each segment reveals unique growth patterns and demand drivers, reflecting the varied requirements for water quality assessment across different contexts and geographies.

- By Type: pH Sensors, Conductivity Sensors, Dissolved Oxygen (DO) Sensors, Turbidity Sensors, Oxidation-Reduction Potential (ORP) Sensors, Total Organic Carbon (TOC) Sensors, Nutrient Sensors (Nitrate, Phosphate, Ammonia), Chloride Sensors, Multi-parameter Sensors, Others (e.g., Temperature, Salinity).

- By Application: Environmental Monitoring, Industrial Process Control, Drinking Water Monitoring, Wastewater Treatment, Aquaculture, Agriculture, Research & Academic, Commercial & Residential.

- By End-User: Government & Utilities, Industrial, Commercial, Residential.

- By Technology: Electrochemical, Optical, Spectroscopic, Photometric, Titrimetric, Microfluidic.

- By Portability: Portable/Handheld, Online/Continuous, Benchtop.

Regional Highlights

- North America: This region demonstrates a mature market driven by stringent environmental regulations, advanced technological adoption, and a strong emphasis on smart water infrastructure development. The United States and Canada are key contributors, with significant investments in both municipal and industrial water treatment facilities. Demand is particularly high for real-time and multi-parameter monitoring solutions, bolstered by research and development activities and the presence of leading market players.

- Europe: Europe represents a significant market, characterized by strict environmental policies, high public awareness regarding water quality, and widespread adoption of sustainable water management practices. Countries like Germany, the UK, and France are at the forefront of implementing advanced monitoring technologies, including IoT-enabled sensors for both drinking water and wastewater management. Innovation in sensor development and integration with digital platforms are key regional trends.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to rapid industrialization, urbanization, and increasing water pollution levels in countries like China and India. Growing populations and expanding manufacturing sectors are intensifying the demand for efficient water quality monitoring to ensure public health and environmental compliance. Government initiatives aimed at improving water infrastructure and promoting sustainable practices are creating immense opportunities for market expansion.

- Latin America: This region is experiencing steady growth in the water quality monitoring sensor market, driven by increasing awareness of water scarcity and pollution, coupled with developing regulatory frameworks. Countries such as Brazil and Mexico are investing in improving water and wastewater treatment facilities, leading to a rising demand for monitoring solutions. Challenges related to infrastructure development and economic stability can influence the pace of adoption.

- Middle East and Africa (MEA): The MEA region is witnessing gradual market growth, spurred by acute water scarcity issues, particularly in arid areas, and a growing focus on water reuse and desalination projects. Increased investments in oil and gas industries also contribute to the demand for process water monitoring. While some parts of the region lag in adopting advanced technologies, emerging economies are actively seeking solutions to manage their limited water resources effectively.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Water Quality Monitoring Sensor Market.- Xylem Inc.

- Danaher Corporation (Hach Company)

- Horiba, Ltd.

- Thermo Fisher Scientific Inc.

- SUEZ

- Lovibond Tintometer GmbH

- Eureka Water Probes (a brand of Xylem)

- OTT HydroMet (a brand of Hach)

- Hanna Instruments

- Palintest Ltd.

- Libelium Comunicaciones Distribuidas S.L.

- Myron L Company

- Vernier Software & Technology

- Campbell Scientific, Inc.

- Aquaread Ltd.

- Teledyne FLIR (Teledyne Technologies Inc.)

- YSI Inc. (a Xylem brand)

- Endress+Hauser Group Services AG

- WTW (a Xylem brand)

- Evoqua Water Technologies LLC.

Frequently Asked Questions

What is the projected growth rate for the Water Quality Monitoring Sensor Market?

The Water Quality Monitoring Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.6% between 2025 and 2033, driven by increasing water pollution and regulatory mandates.

How does AI impact water quality monitoring sensors?

AI significantly impacts water quality monitoring sensors by enabling predictive analytics, automated anomaly detection, optimized sensor network deployment, and enhanced data interpretation, leading to more proactive and efficient water management.

What are the key drivers for the Water Quality Monitoring Sensor Market?

Key drivers for the market include increasing global water pollution levels, stringent environmental regulations, growing demand for real-time monitoring solutions, and continuous advancements in sensor technologies.

Which regions are expected to show significant growth in this market?

The Asia Pacific region is anticipated to exhibit the fastest growth, primarily due to rapid industrialization, urbanization, and increasing government focus on environmental protection in countries like China and India.

What are the primary challenges faced by the Water Quality Monitoring Sensor Market?

Primary challenges include sensor fouling and calibration issues, complexities in data security and management, high power consumption for remote deployments, and a lack of universal standardization and interoperability among different sensor systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted