Smart Water Meter Market

Smart Water Meter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704392 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

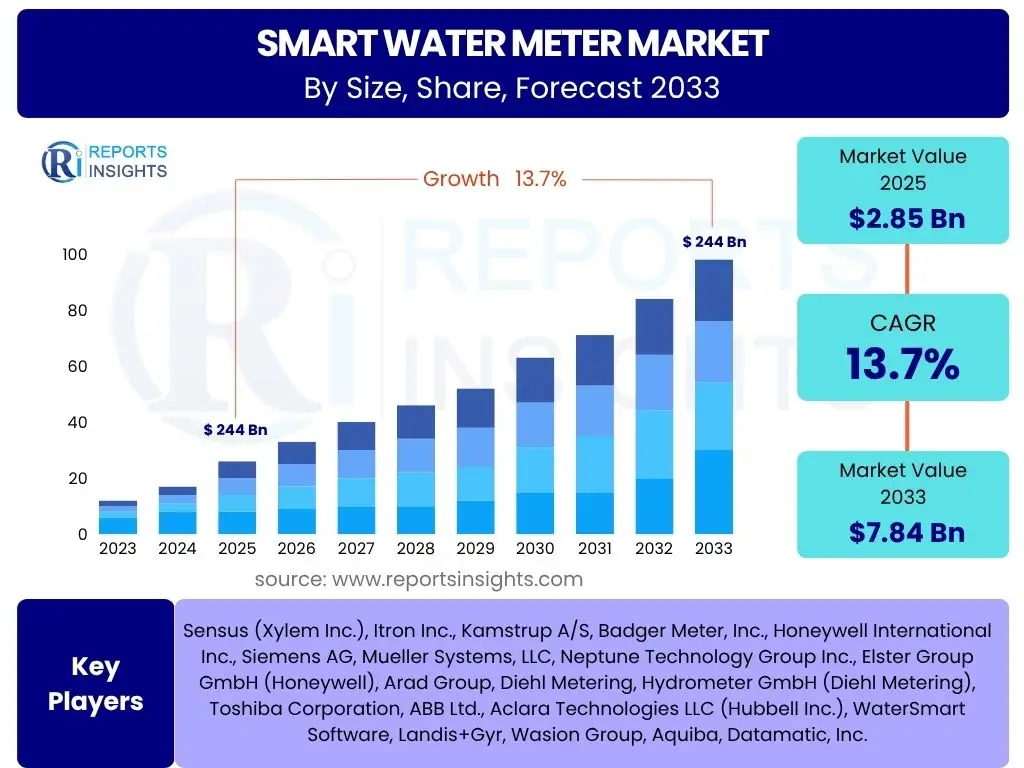

Smart Water Meter Market Size

According to Reports Insights Consulting Pvt Ltd, The Smart Water Meter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 7.84 billion by the end of the forecast period in 2033.

Key Smart Water Meter Market Trends & Insights

The Smart Water Meter market is experiencing significant transformation, driven by a confluence of technological advancements, increasing environmental concerns, and evolving regulatory landscapes. Users frequently inquire about the primary forces shaping this market, specifically focusing on how digital transformation is impacting traditional water management. A key trend involves the widespread adoption of Internet of Things (IoT) technologies, which enable real-time data collection and remote monitoring, fundamentally changing how utilities manage water resources and interact with consumers. This shift is not merely about replacing old meters but about establishing intelligent networks that foster efficiency and sustainability.

Another crucial insight pertains to the growing emphasis on non-revenue water (NRW) reduction, which smart meters effectively address through enhanced leak detection and consumption monitoring capabilities. Furthermore, there is a pronounced trend towards integrating smart water systems within broader smart city initiatives, leveraging data analytics and artificial intelligence to optimize urban resource management. The market is also witnessing a move towards more modular and interoperable solutions, ensuring easier integration with existing infrastructure and future-proofing investments for utility providers. These trends collectively underscore a move towards more proactive, data-driven, and consumer-centric water management practices.

- Increased integration of IoT and advanced sensor technologies for real-time data acquisition.

- Growing focus on Non-Revenue Water (NRW) reduction and leakage detection.

- Rising adoption of cloud-based platforms for data storage, analysis, and management.

- Convergence with smart city initiatives for holistic urban infrastructure management.

- Development of AI and Machine Learning algorithms for predictive analytics and anomaly detection.

- Shift towards advanced metering infrastructure (AMI) over automated meter reading (AMR).

- Emphasis on sustainability and water conservation mandates driving adoption.

AI Impact Analysis on Smart Water Meter

The integration of Artificial Intelligence (AI) is profoundly revolutionizing the Smart Water Meter market, addressing common user inquiries regarding its practical applications and benefits. AI algorithms are significantly enhancing the capabilities of smart water systems by enabling predictive analytics, which allows utilities to forecast water demand patterns with greater accuracy and optimize distribution networks accordingly. This proactive approach minimizes wastage and ensures more efficient resource allocation. Users are keen to understand how AI translates into tangible improvements, and the answer lies in its ability to process vast amounts of data from smart meters to identify anomalies such as leaks, bursts, or unauthorized consumption in real-time, often before they escalate into major issues.

Beyond anomaly detection, AI contributes to operational efficiency by automating decision-making processes, such as optimizing pump schedules and pressure management. This not only reduces energy consumption but also extends the lifespan of infrastructure components. Furthermore, AI-powered analytics can segment customer usage patterns, enabling utilities to offer personalized water conservation advice and improve customer engagement. The transformative potential of AI in this domain is centered on moving from reactive problem-solving to proactive, intelligent management, ensuring a more resilient, sustainable, and economically viable water supply system for communities worldwide.

- Enhanced predictive maintenance and anomaly detection for leaks and bursts.

- Optimized water demand forecasting and supply management.

- Improved operational efficiency through automated pressure and flow control.

- Advanced data analytics for identifying consumption patterns and potential issues.

- Reduced Non-Revenue Water (NRW) through precise identification of unaccounted water.

- Better resource allocation and energy consumption management in pumping stations.

- Personalized insights and alerts for consumers, promoting water conservation.

Key Takeaways Smart Water Meter Market Size & Forecast

Analysis of common user questions concerning the Smart Water Meter market size and forecast reveals a strong interest in the overall growth trajectory and the core reasons behind the projected expansion. A primary takeaway is the robust growth rate anticipated over the forecast period, signaling a significant global transition towards modernized water infrastructure. This growth is underpinned by an increasing recognition of water as a finite and critical resource, driving both public and private sector investments in smart technologies. The market's expansion is not merely incremental but represents a fundamental shift in how water utilities operate, prioritizing efficiency, sustainability, and data-driven decision-making.

Another crucial insight is that the market's value proposition extends beyond simple metering to encompass comprehensive water management solutions. The projected valuation by 2033 indicates a mature yet dynamic market, where technological innovation, regulatory support, and environmental imperatives coalesce to create sustained demand. Stakeholders should note the convergence of various technologies, including IoT, AI, and cloud computing, as fundamental enablers of this growth. The smart water meter market is poised to be a cornerstone of future smart city developments, emphasizing resilience, resource optimization, and enhanced public services.

- The Smart Water Meter market is set for substantial growth, driven by digital transformation and sustainability goals.

- Significant market valuation projected by 2033 underscores widespread adoption and investment.

- Emphasis on Non-Revenue Water (NRW) reduction and operational efficiency is a key market driver.

- Technological integration (IoT, AI, Cloud) is pivotal for market expansion and innovation.

- The market plays a critical role in global water conservation efforts and smart city development.

- Investment in advanced infrastructure and analytics platforms is a recurring theme.

Smart Water Meter Market Drivers Analysis

The Smart Water Meter market's robust growth trajectory is propelled by several critical drivers that address fundamental challenges in water management. A primary driver is the escalating global concern over water scarcity and the imperative for efficient water resource management. As populations grow and climate change impacts intensify, governments and utilities are increasingly investing in technologies that enable precise measurement, leakage detection, and consumption control, making smart meters an indispensable tool for conservation. This global environmental push creates a sustainable demand for intelligent metering solutions.

Furthermore, the aging water infrastructure in many developed regions necessitates substantial upgrades, with smart meters presenting a cost-effective and technologically advanced solution. These meters not only replace outdated mechanical systems but also provide real-time data essential for proactive maintenance and operational optimization. Concurrently, regulatory mandates and government initiatives promoting water efficiency, digital transformation, and smart city development are accelerating the adoption of these technologies. The economic benefits, particularly the reduction of non-revenue water (NRW) losses, offer a compelling return on investment for utilities, making smart meter deployment an attractive proposition despite initial capital outlay.

The continuous advancements in Internet of Things (IoT), communication technologies (e.g., LoRaWAN, NB-IoT), and data analytics capabilities also serve as significant drivers. These technological evolutions make smart meters more accurate, reliable, and cost-effective, enabling seamless integration into broader utility management systems. The ability to collect, transmit, and analyze vast amounts of data in real-time empowers utilities to enhance billing accuracy, improve customer service, and implement demand-side management programs more effectively. This technological enablement ensures that smart meters remain at the forefront of modern water utility operations, driving efficiency and sustainability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Water Scarcity & Conservation Needs | +2.5% | Global | Long-term |

| Aging Water Infrastructure Modernization | +2.0% | North America, Europe | Mid-to-Long-term |

| Government Regulations & Mandates for Water Efficiency | +1.8% | Europe, Asia Pacific | Mid-term |

| Reduction of Non-Revenue Water (NRW) Losses | +1.7% | Global | Ongoing |

| Technological Advancements (IoT, AI, Communication) | +1.5% | Global | Ongoing |

| Rising Awareness Regarding Smart Water Management Benefits | +1.0% | Global | Mid-to-Long-term |

Smart Water Meter Market Restraints Analysis

Despite its significant growth potential, the Smart Water Meter market faces several notable restraints that can impede its wider adoption. One of the most prominent challenges is the high initial capital investment required for deploying smart metering infrastructure. Utilities, especially those in developing regions or with limited budgets, may find it difficult to allocate the substantial funds necessary for purchasing meters, installing communication networks, and integrating new software systems. This financial barrier can significantly slow down the pace of smart meter rollout, particularly in areas where water tariffs are low and cannot easily absorb the investment costs.

Another critical restraint is the complexity associated with data security and privacy concerns. Smart meters collect vast amounts of granular consumption data, which, if compromised, could expose sensitive information about consumer behavior or critical infrastructure vulnerabilities. Ensuring robust cybersecurity measures and adhering to stringent data protection regulations (like GDPR) requires continuous investment and expertise, posing a significant challenge for utilities. Furthermore, the lack of standardization and interoperability among different smart meter technologies and communication protocols can create integration headaches and vendor lock-in issues, complicating deployment and limiting future scalability for some operators.

Public acceptance and consumer resistance also represent a restraint, particularly when initial deployments lead to perceived higher bills or concerns over data privacy. Effective communication strategies are crucial to educate consumers on the benefits of smart meters, such as accurate billing and leak detection, and to address their anxieties. Finally, the technical skill gap within utilities to manage and analyze the complex data generated by smart meters, as well as to maintain the sophisticated infrastructure, can be a limiting factor. Many utilities may lack the trained personnel required to fully leverage the capabilities of smart metering systems, necessitating significant investment in workforce development and training programs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment Costs | -2.0% | Developing Regions, All Regions | Short-to-Mid-term |

| Data Security & Privacy Concerns | -1.5% | Global | Ongoing |

| Lack of Standardization & Interoperability | -1.2% | Global | Mid-term |

| Resistance to Change & Consumer Acceptance Issues | -1.0% | All Regions | Mid-term |

| Technical Skill Gap & Workforce Training Needs | -0.8% | Developing Regions | Short-to-Mid-term |

| Complex Integration with Legacy Systems | -0.7% | Developed Regions | Mid-term |

Smart Water Meter Market Opportunities Analysis

The Smart Water Meter market is characterized by numerous growth opportunities that could significantly accelerate its expansion. A prime opportunity lies in the burgeoning smart city initiatives globally. As urban centers strive to become more sustainable and efficient, integrating smart water metering systems into broader smart infrastructure plans offers a holistic approach to resource management. This integration allows for synergy with other smart services like smart grids and waste management, creating cross-sectoral efficiencies and new value propositions for cities and their residents.

Another compelling opportunity emerges from the continuous advancements in communication technologies, particularly the rollout of Low-Power Wide-Area Network (LPWAN) technologies such as LoRaWAN and NB-IoT. These technologies offer cost-effective, long-range, and low-power connectivity, making smart meter deployments viable even in remote or challenging geographical areas. This expanding connectivity infrastructure reduces deployment costs and enhances data transmission reliability, opening up previously untapped markets. Furthermore, the development of advanced analytics and artificial intelligence platforms presents a significant opportunity to derive deeper insights from meter data, moving beyond basic consumption monitoring to predictive maintenance, demand forecasting, and personalized consumer engagement services.

The vast untapped potential in emerging economies, particularly in Asia Pacific, Latin America, and Africa, represents a substantial market opportunity. These regions often grapple with significant water scarcity, aging infrastructure, and high non-revenue water rates, making smart water meters a crucial tool for sustainable development. Governments and international organizations are increasingly supporting projects in these areas, often through public-private partnerships (PPPs) or direct funding, which facilitates the adoption of smart water solutions. Moreover, the shift towards a service-oriented model, where meter data can be offered as a valuable service to various stakeholders (e.g., insurance companies, property managers), creates new revenue streams and expands the market's reach beyond traditional utility providers, fostering innovation and diversification.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Smart City & Urban Development Projects | +2.0% | North America, Europe, Asia Pacific | Long-term |

| Development of Advanced Analytics & AI Platforms | +1.8% | Global | Ongoing |

| Expansion into Emerging Economies & Underserved Markets | +1.5% | Asia Pacific, Latin America, Africa | Long-term |

| Technological Innovations in LPWAN Communication (LoRaWAN, NB-IoT) | +1.2% | Global | Mid-to-Long-term |

| Public-Private Partnerships (PPPs) & Government Funding | +1.0% | Global | Mid-term |

| Emergence of New Service Models (e.g., Data-as-a-Service) | +0.8% | Developed Regions | Mid-to-Long-term |

Smart Water Meter Market Challenges Impact Analysis

The Smart Water Meter market, while promising, navigates several significant challenges that demand strategic responses from stakeholders. One critical challenge is cybersecurity. As smart meters become integral nodes in critical infrastructure, they present potential targets for cyber-attacks, raising concerns about data integrity, operational disruption, and national security. Ensuring robust encryption, secure communication protocols, and continuous monitoring against evolving cyber threats is paramount, requiring substantial investment and expertise from utilities and technology providers.

Another challenge pertains to the substantial infrastructure requirements, particularly reliable and widespread communication networks, necessary for effective smart meter deployment. In many rural or developing areas, the lack of adequate cellular or LPWAN coverage can hinder seamless data transmission, making large-scale rollouts difficult and costly. This necessitates significant upfront investment in network infrastructure or reliance on alternative, less efficient communication methods, impacting the overall cost-effectiveness and scalability of smart meter projects. Furthermore, the sheer volume of data generated by millions of smart meters creates a challenge in terms of data storage, processing, and actionable analysis. Utilities must develop robust big data management capabilities to transform raw data into valuable insights, avoiding data overload and ensuring data quality for decision-making.

Maintaining the long-term accuracy and functionality of smart meters presents an ongoing challenge. Unlike mechanical meters, electronic smart meters can be susceptible to calibration drift, software glitches, or battery life limitations, requiring regular maintenance, firmware updates, and eventual replacement. Ensuring the longevity and reliable performance of these devices over their projected lifespan is crucial for utilities to realize the full return on investment. Finally, gaining and maintaining public acceptance and trust can be a persistent challenge. Concerns over data privacy, perceived inaccuracies in billing, or disruptions during installation can lead to consumer resistance, highlighting the need for transparent communication, effective customer support, and demonstrable benefits to build confidence and ensure smooth adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats & Data Vulnerabilities | -1.5% | Global | Ongoing |

| Lack of Robust Communication Infrastructure in Certain Regions | -1.2% | Developing Regions, Rural Areas | Mid-term |

| Data Overload & Challenges in Big Data Management | -1.0% | Global | Ongoing |

| Maintenance, Calibration, & Lifespan Issues of Electronic Meters | -0.8% | All Regions | Long-term |

| Public Acceptance & Trust Building | -0.7% | All Regions | Mid-term |

| Interoperability with Diverse Legacy Systems | -0.5% | Developed Regions | Mid-term |

Smart Water Meter Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Smart Water Meter market, offering stakeholders a detailed understanding of market dynamics, growth drivers, restraints, opportunities, and challenges. The scope encompasses a thorough examination of market sizing, historical performance, and future projections across various segments and key regions. The insights derived from extensive primary and secondary research aim to equip businesses with actionable intelligence for strategic decision-making and competitive positioning within the evolving water management landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 7.84 Billion |

| Growth Rate | 13.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sensus (Xylem Inc.), Itron Inc., Kamstrup A/S, Badger Meter, Inc., Honeywell International Inc., Siemens AG, Mueller Systems, LLC, Neptune Technology Group Inc., Elster Group GmbH (Honeywell), Arad Group, Diehl Metering, Hydrometer GmbH (Diehl Metering), Toshiba Corporation, ABB Ltd., Aclara Technologies LLC (Hubbell Inc.), WaterSmart Software, Landis+Gyr, Wasion Group, Aquiba, Datamatic, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Smart Water Meter market is comprehensively segmented to provide granular insights into its diverse components and applications. This segmentation allows for a detailed analysis of specific market niches, enabling stakeholders to identify high-growth areas and tailor strategies accordingly. The market is primarily segmented by type, technology, component, and application, each revealing distinct adoption patterns and growth drivers across various end-user sectors and geographical regions. Understanding these segments is crucial for accurate market forecasting and strategic planning.

- By Type:

- Advanced Metering Infrastructure (AMI): Represents systems that enable two-way communication between meters and utilities, allowing for remote data collection, control, and advanced functionalities.

- Automated Meter Reading (AMR): Involves one-way communication for remote collection of meter data, typically less sophisticated than AMI but more advanced than manual reading.

- By Technology:

- Ultrasonic Meter: Utilizes ultrasonic waves to measure water flow, known for high accuracy and no moving parts, reducing wear and tear.

- Electromagnetic Meter: Measures water flow based on Faraday's law of electromagnetic induction, suitable for conductive liquids and often used in industrial applications.

- Mechanical Meter (with communication module): Traditional mechanical meters equipped with communication modules to transmit readings digitally.

- By Component:

- Meters: The physical smart water metering devices.

- Communication Modules: Hardware enabling data transmission (e.g., radio, cellular, LPWAN).

- Software: Platforms for data collection, analysis, billing, and customer management.

- Services: Installation, maintenance, data analytics, and consulting services.

- By Application:

- Residential: Smart meters deployed in individual homes and multi-dwelling units.

- Commercial: Used in commercial buildings, offices, and retail establishments.

- Industrial: Employed in manufacturing plants and other industrial facilities for process monitoring and efficiency.

- Utilities: Large-scale deployment by public and private water utility providers across their networks.

Regional Highlights

The global Smart Water Meter market exhibits varied growth dynamics across different regions, influenced by factors such as water scarcity, regulatory environments, technological adoption rates, and economic development. North America, for instance, leads in terms of market size and early adoption, driven by the need to replace aging infrastructure, reduce non-revenue water, and integrate smart solutions into existing utility networks. The region benefits from established technological infrastructure and government incentives for water conservation, fostering a strong market for smart metering solutions.

Europe also represents a significant market, propelled by stringent environmental regulations, ambitious water efficiency targets, and widespread smart city initiatives. Countries within the European Union are actively investing in digitalizing their water infrastructure to enhance sustainability and operational resilience. The Asia Pacific region is poised for the most rapid growth, fueled by rapid urbanization, increasing industrialization, and a growing middle class that collectively strains existing water resources. Governments in countries like China and India are undertaking large-scale smart water projects to address water scarcity and improve service delivery in burgeoning urban areas.

Latin America faces considerable challenges related to water management, including high levels of non-revenue water and inconsistent supply. This creates a compelling need and opportunity for smart water meter adoption, with several countries initiating pilot programs and large-scale deployments to improve efficiency and reduce losses. The Middle East and Africa (MEA) region, characterized by extreme water scarcity in many areas, presents a burgeoning market for smart water solutions. Investments in desalination plants and efficient water distribution technologies, including smart meters, are critical for ensuring water security, particularly in oil-rich nations and rapidly developing urban centers seeking sustainable growth strategies.

- North America: Dominates the market due to aging infrastructure replacement, focus on NRW reduction, and advanced technological adoption.

- Europe: Driven by stringent environmental regulations, smart city initiatives, and strong emphasis on water conservation and efficiency.

- Asia Pacific (APAC): Fastest-growing region due to rapid urbanization, increasing population, growing industrial demand, and government initiatives for smart water management.

- Latin America: Emerging market with high potential due to significant water losses, infrastructure development needs, and increasing awareness of water scarcity.

- Middle East and Africa (MEA): Growing demand for smart water solutions driven by severe water scarcity, investments in smart infrastructure, and economic diversification efforts.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Smart Water Meter Market.- Sensus (Xylem Inc.)

- Itron Inc.

- Kamstrup A/S

- Badger Meter, Inc.

- Honeywell International Inc.

- Siemens AG

- Mueller Systems, LLC

- Neptune Technology Group Inc.

- Elster Group GmbH (Honeywell)

- Arad Group

- Diehl Metering

- Hydrometer GmbH (Diehl Metering)

- Toshiba Corporation

- ABB Ltd.

- Aclara Technologies LLC (Hubbell Inc.)

- WaterSmart Software

- Landis+Gyr

- Wasion Group

- Aquiba

- Datamatic, Inc.

Frequently Asked Questions

What is a smart water meter?

A smart water meter is an advanced device that digitally measures water consumption and wirelessly transmits usage data to utilities. It enables real-time monitoring, remote readings, and provides detailed insights into water usage patterns, often aiding in leak detection and conservation efforts.

How do smart water meters help in water conservation?

Smart water meters significantly aid conservation by providing real-time data that helps detect leaks faster, identify wasteful usage patterns, and empower consumers with information to manage their consumption effectively. They enable utilities to implement demand management programs and reduce non-revenue water losses.

What are the main benefits of smart water meters for utilities?

For utilities, smart water meters offer benefits such as accurate billing, reduced operational costs from manual meter reading, improved leak detection and network management, enhanced customer service through transparent data, and better planning for water supply and demand through data analytics.

What is the role of IoT in smart water meters?

IoT (Internet of Things) is fundamental to smart water meters as it enables the connectivity and data exchange between the meters, communication networks, and utility back-end systems. IoT sensors and communication modules allow for automated data collection, remote monitoring, and integration into broader smart infrastructure, driving efficiency and insights.

What are the primary challenges in adopting smart water meters?

Key challenges include the high initial investment costs for installation and infrastructure, concerns regarding data security and privacy, the need for robust communication networks in all areas, and ensuring consumer acceptance and understanding of the technology's benefits.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted