Automotive Driver Monitoring System Market

Automotive Driver Monitoring System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704387 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive Driver Monitoring System Market Size

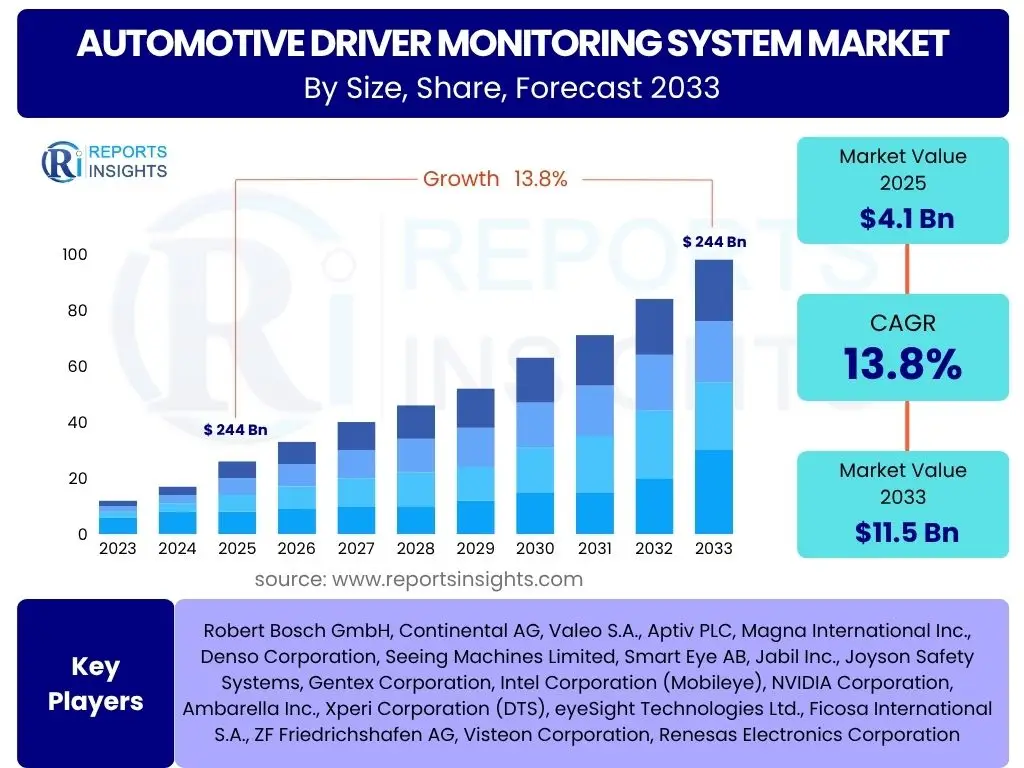

According to Reports Insights Consulting Pvt Ltd, The Automotive Driver Monitoring System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.8% between 2025 and 2033. The market is estimated at USD 4.1 Billion in 2025 and is projected to reach USD 11.5 Billion by the end of the forecast period in 2033.

Key Automotive Driver Monitoring System Market Trends & Insights

User inquiries frequently highlight the evolving regulatory landscape and the rapid integration of advanced technologies as primary drivers shaping the Automotive Driver Monitoring System (DMS) market. There is significant interest in how increasing levels of vehicle autonomy influence DMS development, moving from basic distraction detection to comprehensive occupant monitoring. Furthermore, the role of artificial intelligence and machine learning in enhancing the accuracy and predictive capabilities of these systems is a recurring theme, alongside concerns regarding data privacy and system reliability in diverse driving conditions.

A notable trend is the shift towards holistic in-cabin sensing solutions, which combine driver monitoring with occupant monitoring, gesture control, and personalized comfort features. This integration aims to create a more intuitive and safer vehicle environment, responding to driver state, passenger presence, and cabin conditions. Additionally, the proliferation of connected vehicle ecosystems is enabling DMS data to be utilized for fleet management, insurance telematics, and predictive maintenance, extending the value proposition beyond immediate safety warnings.

The market is also witnessing a trend towards miniaturization and cost reduction of sensor technologies, making DMS more accessible for integration across a wider range of vehicle segments, including entry-level models. Original Equipment Manufacturers (OEMs) are increasingly incorporating these systems as standard features, driven by upcoming mandates and a competitive desire to offer superior safety packages. This widespread adoption is fostering innovation in software algorithms and edge computing, allowing for real-time processing of complex behavioral patterns and precise intervention strategies.

- Integration of advanced AI and Machine Learning for enhanced driver state detection.

- Shift towards holistic in-cabin sensing incorporating driver and occupant monitoring.

- Increasing standardization of DMS in new vehicle models due to regulatory pressures.

- Growth in demand for personalized in-cabin experiences and predictive safety features.

- Development of robust, miniaturized, and cost-effective sensor technologies.

- Expansion of DMS functionality beyond distraction to include fatigue and health monitoring.

AI Impact Analysis on Automotive Driver Monitoring System

Common user questions regarding AI's influence on Automotive Driver Monitoring Systems frequently revolve around its capability to enhance detection accuracy, minimize false positives, and enable predictive analytics. Users are keen to understand how AI-driven algorithms can differentiate between various states of driver distraction, drowsiness, or impairment with higher precision than traditional rule-based systems. There is also a strong expectation that AI will facilitate the seamless integration of DMS with other Advanced Driver Assistance Systems (ADAS), leading to more coordinated safety responses and a higher degree of contextual awareness within the vehicle.

Furthermore, concerns are often raised about the ethical implications of AI in DMS, particularly regarding data privacy, the potential for bias in algorithms, and the transparency of decision-making processes. Users seek assurances that AI systems are developed responsibly, ensuring fair and equitable monitoring without intrusive data collection practices. The ability of AI to adapt to diverse driver behaviors and environmental conditions, alongside its capacity for continuous learning and improvement through over-the-air updates, is also a significant area of interest, reflecting a desire for future-proof and highly adaptable safety solutions.

The implementation of AI is expected to revolutionize DMS by enabling more sophisticated behavioral analysis, moving beyond simple head pose or eye-tracking to understand cognitive load and emotional states. This allows for truly personalized interventions, such as adaptive warnings or even semi-autonomous vehicle control takeovers, based on a comprehensive assessment of the driver's current state and capability. AI also plays a crucial role in sensor fusion, combining data from various in-cabin cameras, infrared sensors, and biometric inputs to create a robust and reliable picture of the driver's condition, even in challenging lighting or visibility scenarios.

- Enhanced accuracy in detecting driver distraction, drowsiness, and impairment.

- Enabling predictive analytics for proactive safety interventions.

- Facilitating seamless integration with other ADAS features for holistic safety.

- Addressing ethical considerations such as data privacy and algorithmic bias.

- Continuous learning and adaptation of systems through AI-driven updates.

- Advanced behavioral analysis, including cognitive load and emotional state assessment.

Key Takeaways Automotive Driver Monitoring System Market Size & Forecast

User queries about the Automotive Driver Monitoring System market size and forecast consistently focus on understanding the primary growth catalysts and the scale of market expansion. A key insight is that the market's substantial projected growth is largely attributable to evolving global safety regulations, which are increasingly mandating DMS in new vehicles. This regulatory push, combined with a heightened consumer awareness regarding vehicle safety, is driving rapid adoption across various automotive segments. The forecast indicates a robust trajectory, suggesting that DMS will become a standard feature rather than a premium add-on in the coming decade.

Another significant takeaway is the pivotal role of technological advancements, particularly in artificial intelligence, computer vision, and sensor technology. These innovations are not only improving the efficacy and reliability of DMS but also contributing to cost reduction, making the technology more accessible for mass market integration. The market's expansion is further bolstered by the increasing penetration of advanced driver assistance systems (ADAS) and the accelerating development of autonomous vehicles, where DMS is an indispensable component for monitoring human-machine interaction and ensuring safe transitions of control.

The market forecast also highlights the growing importance of regional mandates, with Europe and North America leading the charge in implementing stringent safety standards, followed closely by Asia Pacific. This global regulatory harmonization, alongside competitive pressures among automakers to enhance vehicle safety ratings, will continue to propel market growth. The projected substantial increase in market value underscores the critical role DMS will play in reducing road fatalities and injuries, transforming the automotive safety landscape comprehensively through predictive and reactive measures.

- Significant market growth driven by global safety regulations and consumer awareness.

- Technological advancements in AI, computer vision, and sensors are key accelerators.

- DMS is becoming a standard feature across vehicle segments, moving beyond premium offerings.

- Integral role of DMS in the evolution and adoption of ADAS and autonomous driving.

- Strong market expansion anticipated across all major geographical regions.

- Increasing importance of DMS in reducing road accidents and enhancing overall vehicle safety.

Automotive Driver Monitoring System Market Drivers Analysis

The Automotive Driver Monitoring System (DMS) market is significantly propelled by a confluence of factors, primarily global regulatory mandates and the escalating demand for enhanced vehicle safety. Governments and regulatory bodies worldwide are increasingly recognizing the critical role of DMS in mitigating driver distraction and fatigue, leading to the enactment of stringent safety legislation. These mandates compel automakers to integrate sophisticated monitoring systems, thereby creating a foundational demand for the technology. The push for active safety systems is a direct response to the alarming statistics of accidents caused by human error, positioning DMS as an essential component in future vehicle designs.

Another powerful driver is the rapid advancement and integration of Artificial Intelligence (AI) and Machine Learning (ML) within automotive systems. These technologies enable DMS to move beyond simple alerts to sophisticated real-time analysis of driver behavior, cognitive load, and emotional state. AI-powered DMS can accurately detect subtle signs of impairment or distraction, providing more timely and effective interventions. This technological evolution not only improves the efficacy of DMS but also facilitates its seamless integration with other Advanced Driver Assistance Systems (ADAS), creating a synergistic effect that enhances overall vehicle safety and performance.

Furthermore, increasing consumer awareness regarding vehicle safety features and a willingness to pay for advanced technologies contribute significantly to market expansion. Consumers are becoming more educated about the benefits of active safety systems that can prevent accidents rather than merely mitigate their impact. The desire for a safer driving experience, coupled with the potential for reduced insurance premiums and improved passenger comfort, acts as a strong incentive for widespread adoption. This demand from the end-user side complements the regulatory push, creating a robust and sustained growth environment for the DMS market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Safety Regulations (e.g., EU GSR, NHTSA) | +4.5% | Europe, North America, China, Japan | Short to Mid-term (2025-2029) |

| Advancements in AI and Machine Learning for DMS | +3.0% | Global | Mid to Long-term (2027-2033) |

| Increasing Consumer Demand for Vehicle Safety Features | +2.5% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Growth in Autonomous and Semi-Autonomous Vehicles | +3.8% | Global, particularly developed economies | Mid to Long-term (2028-2033) |

Automotive Driver Monitoring System Market Restraints Analysis

Despite the strong growth drivers, the Automotive Driver Monitoring System (DMS) market faces several notable restraints that could temper its expansion. One of the primary concerns revolves around the high cost associated with integrating sophisticated DMS technology into vehicles. The components, including advanced cameras, infrared sensors, and powerful processing units, along with the complex software algorithms, add a significant premium to the vehicle's manufacturing cost. This cost factor can be particularly restrictive for mass-market vehicle segments, potentially hindering widespread adoption, especially in price-sensitive emerging markets where manufacturers aim to keep vehicle prices competitive.

Another substantial restraint is public perception and privacy concerns related to constant in-cabin monitoring. Consumers often express discomfort with the idea of being continuously observed by cameras and sensors inside their vehicles, raising questions about data collection, storage, and potential misuse. This apprehension can lead to resistance against DMS adoption, requiring manufacturers to implement robust data protection measures and communicate transparently about the scope and purpose of data usage. Overcoming these privacy concerns necessitates a careful balance between safety benefits and individual rights, posing a significant challenge for market penetration.

Furthermore, the complexity of integrating DMS with diverse vehicle architectures and existing Advanced Driver Assistance Systems (ADAS) presents a technical restraint. Achieving seamless compatibility and optimal performance across various car models, operating systems, and sensor suites requires extensive research and development, as well as significant investment. Issues such as false positives or false negatives, which can erode driver trust and lead to system disengagement, also represent a challenge. Ensuring the reliability and robustness of DMS in varying environmental conditions and for a wide range of driver demographics further complicates development and deployment efforts, adding to the development timeline and costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Integration and System Components | -2.0% | Global, particularly emerging markets | Short to Mid-term (2025-2028) |

| Privacy Concerns and Data Security Issues | -1.5% | North America, Europe | Mid-term (2026-2030) |

| Complexity of System Integration and Calibration | -1.0% | Global | Short to Mid-term (2025-2029) |

| Potential for False Alarms or System Malfunctions | -0.8% | Global | Short-term (2025-2027) |

Automotive Driver Monitoring System Market Opportunities Analysis

The Automotive Driver Monitoring System (DMS) market is characterized by several significant opportunities for growth and innovation. One key area is the burgeoning development of higher levels of autonomous driving, specifically Level 3 (conditional automation) and beyond. While these systems aim to reduce driver intervention, DMS becomes critical for monitoring driver readiness to take back control when necessary and ensuring safe transitions between automated and manual driving modes. This human-machine interface monitoring is an indispensable component, opening vast avenues for advanced DMS solutions tailored to autonomous vehicle requirements and compliance with future regulations.

Another substantial opportunity lies in the expansion of DMS applications beyond traditional safety warnings to encompass in-cabin personalization and user experience enhancements. Integrating DMS with vehicle infotainment and comfort systems can enable features like personalized climate control, adaptive audio settings, or even biometric authentication based on driver state. This convergence allows manufacturers to differentiate their vehicles by offering a more intuitive, comfortable, and tailored driving environment, thereby increasing consumer appeal and demand for vehicles equipped with sophisticated DMS capabilities.

Furthermore, the growth of shared mobility services and commercial fleets presents a lucrative market segment for DMS. In ride-hailing, car-sharing, and logistics operations, driver monitoring can enhance safety, optimize fleet management, and potentially reduce insurance costs by tracking driver behavior and fatigue. For commercial vehicles, where driver fatigue is a significant concern and regulatory compliance is paramount, advanced DMS can improve operational efficiency and safety records, making it a compelling investment for fleet operators. The demand for robust and reliable DMS solutions in these sectors is expected to grow substantially, driven by both safety imperatives and operational efficiencies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Autonomous Driving (L3+) Systems | +3.5% | Global, particularly developed automotive markets | Mid to Long-term (2028-2033) |

| Expansion into In-Cabin Personalization and UX Enhancement | +2.8% | North America, Europe, Asia Pacific | Mid-term (2027-2032) |

| Adoption in Commercial Vehicles and Shared Mobility Fleets | +2.2% | Global | Short to Mid-term (2025-2030) |

| Emergence of Software-Defined Vehicles and Over-The-Air Updates | +1.5% | Global | Mid to Long-term (2029-2033) |

Automotive Driver Monitoring System Market Challenges Impact Analysis

The Automotive Driver Monitoring System (DMS) market faces several complex challenges that require innovative solutions and strategic approaches. One significant hurdle is the management of vast amounts of sensitive driver data collected by these systems. Ensuring robust data privacy and cybersecurity measures is paramount to comply with stringent regulations like GDPR and to maintain consumer trust. The risk of data breaches or unauthorized access can severely undermine public acceptance and adoption rates, compelling manufacturers to invest heavily in secure data handling and encryption protocols to safeguard personal information collected through in-cabin sensors and cameras.

Another considerable challenge is achieving universal reliability and accuracy of DMS across diverse driver demographics, environmental conditions, and vehicle types. Factors such as varying lighting conditions (day, night, glare), different driver physiognomies (facial features, eyewear), and diverse driving behaviors can impact the system's ability to accurately detect distraction or fatigue. Ensuring consistent performance without false positives or negatives is critical for user acceptance and regulatory compliance, necessitating advanced algorithms, robust sensor technologies, and extensive testing in real-world scenarios to validate their efficacy and reduce errors.

Furthermore, the integration of DMS with other complex vehicle systems, including Advanced Driver Assistance Systems (ADAS) and infotainment units, presents technical and architectural challenges. Achieving seamless communication and synergistic operation among these systems requires standardized protocols and advanced software development capabilities. Calibration complexities for varied vehicle models, the need for continuous software updates to enhance functionality and address new threats, and the challenge of managing hardware obsolescence in a rapidly evolving technological landscape also pose significant hurdles for manufacturers. Overcoming these integration and maintenance challenges is crucial for the long-term viability and widespread deployment of DMS.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Privacy and Cybersecurity Concerns | -1.8% | Global, especially Europe, North America | Short to Mid-term (2025-2029) |

| Ensuring Accuracy and Reliability across Diverse Conditions | -1.2% | Global | Mid-term (2026-2030) |

| Integration Complexity with Existing Vehicle Architecture | -0.9% | Global | Short to Mid-term (2025-2028) |

| Consumer Acceptance and Trust Building | -0.7% | Global | Short to Mid-term (2025-2027) |

Automotive Driver Monitoring System Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Automotive Driver Monitoring System (DMS) market, offering a detailed overview of its current size, historical trends, and future growth projections. The report segments the market by component, vehicle type, level of autonomy, technology, and sales channel, providing granular insights into each category. It also includes a thorough regional analysis, identifying key growth opportunities and challenges across major geographies. Furthermore, the report profiles leading market players, analyzing their strategies, product portfolios, and competitive positioning, along with an assessment of the impact of artificial intelligence and emerging industry trends on the market landscape. This holistic approach ensures stakeholders gain actionable intelligence for strategic decision-making in this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.1 Billion |

| Market Forecast in 2033 | USD 11.5 Billion |

| Growth Rate | 13.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Continental AG, Valeo S.A., Aptiv PLC, Magna International Inc., Denso Corporation, Seeing Machines Limited, Smart Eye AB, Jabil Inc., Joyson Safety Systems, Gentex Corporation, Intel Corporation (Mobileye), NVIDIA Corporation, Ambarella Inc., Xperi Corporation (DTS), eyeSight Technologies Ltd., Ficosa International S.A., ZF Friedrichshafen AG, Visteon Corporation, Renesas Electronics Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Driver Monitoring System market is meticulously segmented to provide a granular understanding of its diverse components and applications, enabling targeted analysis of market dynamics across various dimensions. This comprehensive segmentation highlights the different technological approaches, vehicle applications, and sales channels that contribute to the overall market structure. By dissecting the market into these distinct categories, the report offers detailed insights into the specific drivers, challenges, and opportunities pertinent to each segment, allowing stakeholders to identify high-growth areas and formulate precise market strategies. The segmentation also clarifies the evolving landscape of DMS, from basic hardware components to sophisticated software solutions and their integration across various vehicle types and levels of autonomy.

- By Component: This segment includes the essential hardware and software elements of a DMS.

- Cameras: Image sensors used for monitoring driver's face, eyes, and head movements.

- Sensors: Infrared sensors for night vision, pressure sensors for seat occupancy, and other biometric sensors.

- Processors: High-performance chips required for real-time data analysis and algorithm execution.

- Software: Algorithms for driver state detection, behavior analysis, and system integration.

- Other Hardware: Includes lighting components, enclosures, and connectivity modules.

- By Vehicle Type: Categorizes DMS adoption based on the automotive segment.

- Passenger Cars: The largest segment, driven by consumer safety demand and regulatory mandates.

- Commercial Vehicles: Includes light and heavy commercial vehicles, driven by fleet safety and operational efficiency needs.

- By Level of Autonomy: Differentiates DMS based on its role in different autonomous driving levels.

- Semi-Autonomous (L0-L2): Focuses on driver distraction and fatigue for human-driven vehicles.

- Autonomous (L3-L5): Emphasizes driver readiness for takeover, human-machine interaction, and occupant monitoring in automated vehicles.

- By Technology: Identifies the primary technological approaches used in DMS.

- Camera-Based DMS: Relies on visual input for monitoring, often incorporating infrared capabilities.

- Sensor-Based DMS: Utilizes non-camera sensors like pressure sensors or steering wheel sensors to infer driver state.

- By Sales Channel: Distinguishes between direct integration and aftermarket sales.

- Original Equipment Manufacturer (OEM): Systems integrated directly by vehicle manufacturers during production.

- Aftermarket: Standalone DMS units or integrated solutions installed post-vehicle purchase.

Regional Highlights

- North America: This region is a significant market for Automotive Driver Monitoring Systems, driven by strong consumer awareness regarding vehicle safety and the proactive stance of regulatory bodies. The National Highway Traffic Safety Administration (NHTSA) in the United States actively promotes advanced safety features, and consumer advocacy groups play a role in increasing demand. Furthermore, the presence of major automotive OEMs and a robust research and development ecosystem contribute to the rapid adoption and technological advancement of DMS. The region is witnessing an increasing integration of DMS in new vehicle models, often bundled with other ADAS features, leading to steady market growth.

- Europe: Europe is at the forefront of DMS adoption, largely propelled by stringent safety regulations such as the European Union's General Safety Regulation (GSR), which mandates DMS in all new vehicle types from 2024 and all new vehicles from 2026. This regulatory push provides a significant impetus for market expansion. The region also benefits from a mature automotive industry, high consumer safety expectations, and continuous innovation from key technology providers. Countries like Germany, France, and the UK are key contributors to market growth due to their advanced automotive manufacturing base and focus on vehicle safety standards.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for Automotive Driver Monitoring Systems, driven by increasing vehicle production, rising disposable incomes, and a growing emphasis on road safety in countries like China, Japan, South Korea, and India. While regulatory mandates are still evolving in some parts of the region, the competitive landscape among domestic and international OEMs is fostering the integration of advanced safety features, including DMS. The large population base and rapid urbanization in countries like China and India present substantial opportunities for market penetration as vehicle ownership continues to expand.

- Latin America: The Latin American market for DMS is characterized by gradual growth, influenced by evolving regulatory frameworks and increasing awareness of vehicle safety. While adoption rates may lag behind developed regions, the growing automotive manufacturing sector in countries like Brazil and Mexico, coupled with efforts to improve road safety, indicates a promising future for DMS. Economic development and a rising middle class are also contributing to a greater demand for vehicles equipped with modern safety features.

- Middle East and Africa (MEA): The MEA region is an emerging market for DMS, with growth primarily concentrated in economically developed countries within the Middle East, such as Saudi Arabia and the UAE, where luxury vehicle sales and infrastructure development are strong. Road safety initiatives are gaining traction in several countries, slowly driving the demand for advanced safety systems. However, widespread adoption across the entire region is challenged by varying economic conditions and regulatory inconsistencies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Driver Monitoring System Market.- Robert Bosch GmbH

- Continental AG

- Valeo S.A.

- Aptiv PLC

- Magna International Inc.

- Denso Corporation

- Seeing Machines Limited

- Smart Eye AB

- Jabil Inc.

- Joyson Safety Systems

- Gentex Corporation

- Intel Corporation (Mobileye)

- NVIDIA Corporation

- Ambarella Inc.

- Xperi Corporation (DTS)

- eyeSight Technologies Ltd.

- Ficosa International S.A.

- ZF Friedrichshafen AG

- Visteon Corporation

- Renesas Electronics Corporation

Frequently Asked Questions

Analyze common user questions about the Automotive Driver Monitoring System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an Automotive Driver Monitoring System (DMS)?

An Automotive Driver Monitoring System (DMS) is an in-vehicle technology designed to detect and alert drivers to signs of distraction, drowsiness, or impairment. It typically uses cameras, sensors, and AI algorithms to monitor driver behavior, such as eye gaze, head position, and blinking patterns, to enhance vehicle safety and prevent accidents.

Why is DMS becoming increasingly important in new vehicles?

DMS is gaining importance due to rising global safety regulations, which increasingly mandate its inclusion in new vehicles to reduce accidents caused by human error. Additionally, the proliferation of higher levels of autonomous driving necessitates DMS for safe human-machine interaction and driver readiness monitoring during transitions of control.

How does AI impact the effectiveness of DMS?

Artificial Intelligence significantly enhances DMS effectiveness by enabling more accurate and nuanced detection of driver states. AI algorithms can analyze complex behavioral patterns, differentiate between various forms of distraction or drowsiness, and integrate seamlessly with other vehicle systems to provide proactive and context-aware safety interventions.

What are the main challenges for the DMS market?

Key challenges for the DMS market include addressing privacy concerns related to in-cabin data collection, ensuring high accuracy and reliability across diverse environmental conditions and driver demographics, and managing the technical complexity and cost of integrating these systems into various vehicle architectures.

What are the future opportunities for the DMS market?

Future opportunities for the DMS market include its integral role in the development of Level 3 and higher autonomous vehicles, expansion into in-cabin personalization and user experience enhancement, and growing adoption in commercial vehicle fleets and shared mobility services for improved safety and operational efficiency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted