Advanced Driver Assistance System Market

Advanced Driver Assistance System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704503 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Advanced Driver Assistance System Market Size

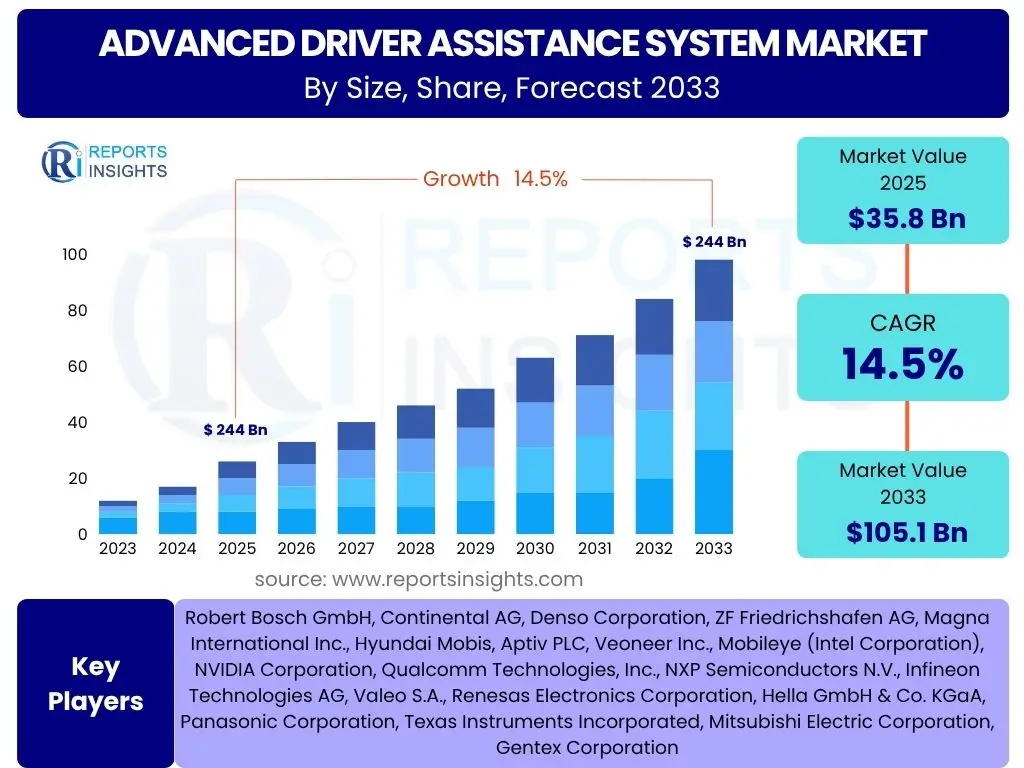

According to Reports Insights Consulting Pvt Ltd, The Advanced Driver Assistance System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2025 and 2033. The market is estimated at USD 35.8 Billion in 2025 and is projected to reach USD 105.1 Billion by the end of the forecast period in 2033.

Key Advanced Driver Assistance System Market Trends & Insights

The Advanced Driver Assistance System (ADAS) market is currently undergoing a significant transformation, driven by a confluence of technological advancements, evolving regulatory landscapes, and increasing consumer demand for vehicle safety and convenience. Key trends indicate a shift towards more sophisticated, integrated systems that leverage enhanced sensor technologies and artificial intelligence for superior environmental perception and decision-making. There is a clear emphasis on achieving higher levels of automation, moving beyond basic driver alerts to systems capable of partial or conditional autonomous operation, thereby redefining the driving experience.

Furthermore, the market is witnessing robust growth in sensor fusion technologies, where data from multiple sensor types such as radar, lidar, cameras, and ultrasonic sensors are combined to create a comprehensive and reliable understanding of the vehicle’s surroundings. This integration is crucial for improving the accuracy and redundancy of ADAS functionalities, especially in challenging weather conditions or complex urban environments. The proliferation of connected vehicle technologies also plays a pivotal role, enabling vehicles to communicate with each other (V2V), infrastructure (V2I), and other road users, which promises to enhance the effectiveness of ADAS features like traffic jam assist and predictive collision warning systems. The automotive industry's pursuit of zero accidents and reduced traffic congestion is accelerating the adoption and innovation within this sector.

Another prominent trend involves the modularization and scalability of ADAS platforms. Vehicle manufacturers are increasingly looking for flexible architectures that can be adapted across various vehicle segments and updated over the air, allowing for continuous improvement and the introduction of new features post-purchase. This approach not only streamlines development and reduces costs but also extends the lifecycle of ADAS technologies within vehicles, contributing to long-term market expansion. The integration of ADAS features into entry-level and mid-range vehicles, previously reserved for premium segments, is democratizing these safety innovations and broadening the market's demographic reach.

- Integration of advanced sensor fusion for enhanced perception.

- Increased adoption of Level 2+ and Level 3 autonomous driving features.

- Development of cloud-connected ADAS for real-time data exchange.

- Focus on software-defined vehicles enabling over-the-air (OTA) updates for ADAS.

- Miniaturization and cost reduction of ADAS components driving wider adoption.

AI Impact Analysis on Advanced Driver Assistance System

Artificial Intelligence (AI) is fundamentally reshaping the Advanced Driver Assistance System (ADAS) landscape, elevating its capabilities from mere assistance to intelligent, predictive, and adaptive driving functions. Common user questions often revolve around how AI makes ADAS smarter, what new functionalities it enables, and what are the implications for safety and reliability. AI's core contribution lies in its ability to process vast amounts of complex sensor data in real-time, identify patterns, and make informed decisions, which is crucial for advanced features like automated driving, pedestrian detection, and intelligent cruise control.

Specifically, AI-powered algorithms, including deep learning and machine learning, significantly enhance the accuracy and robustness of perception systems. For instance, neural networks enable cameras to better classify objects, understand traffic scenarios, and predict the behavior of other road users, surpassing the limitations of traditional rule-based systems. This allows for more precise lane keeping, safer emergency braking, and more intuitive adaptive cruise control. Users are keen to understand how AI mitigates false positives and improves overall system reliability, especially in challenging environmental conditions such as adverse weather or low light, where AI can leverage its learning capabilities to maintain performance.

Moreover, AI's role extends to predictive capabilities, allowing ADAS to anticipate potential hazards before they fully develop, thereby proactive rather than merely reactive. This includes predicting driver fatigue, road conditions, or even the trajectory of a pedestrian. The integration of AI also facilitates personalization and continuous improvement of ADAS features, as systems can learn from individual driving styles and adapt accordingly. This potential for ongoing enhancement through AI, often delivered via over-the-air updates, is a significant draw for consumers and a key driver of innovation within the ADAS market, addressing user expectations for increasingly sophisticated and adaptive vehicle safety systems.

- Enhanced perception and object classification through deep learning algorithms.

- Improved predictive capabilities for proactive safety interventions.

- Real-time decision-making for complex driving scenarios.

- Facilitation of personalized ADAS features and adaptive driving styles.

- Enabling of higher levels of autonomous driving through advanced AI inference at the edge.

Key Takeaways Advanced Driver Assistance System Market Size & Forecast

The Advanced Driver Assistance System (ADAS) market is poised for substantial expansion, with a robust compound annual growth rate projected to lead to a significant increase in market valuation over the forecast period. Common user inquiries frequently focus on the magnitude of this growth, the primary drivers behind it, and what this implies for the future of automotive safety and autonomy. A key takeaway is the pervasive integration of ADAS features across all vehicle segments, transitioning from luxury vehicle staples to standard equipment in mainstream models, fueled by increasing consumer awareness of safety benefits and evolving regulatory mandates worldwide.

Another critical insight is the technological evolution driving this growth, particularly the advancements in sensor technologies, processing power, and the integration of artificial intelligence. These innovations are enabling more sophisticated and reliable ADAS functionalities, paving the way for higher levels of automated driving. The market's upward trajectory is also underpinned by the ongoing investments in research and development by automotive OEMs and technology providers, aiming to enhance existing systems and introduce novel solutions that address complex driving challenges and improve overall road safety. The drive towards reducing traffic fatalities and injuries remains a fundamental catalyst for market expansion.

Ultimately, the forecast indicates a strategic shift in the automotive industry, where ADAS is not merely an add-on but an integral component of vehicle design and functionality, crucial for market competitiveness. The increasing volume of data generated by ADAS-equipped vehicles is also creating new business models, from insurance telematics to predictive maintenance. This holistic growth, characterized by technological maturity, regulatory support, and consumer acceptance, positions the ADAS market as a central pillar in the future of mobility, offering significant opportunities for innovation and commercial success across the value chain.

- Significant market expansion driven by safety regulations and consumer demand.

- Technological advancements in sensors and AI are key growth enablers.

- Increasing integration of ADAS features as standard across vehicle segments.

- Strong emphasis on moving towards higher levels of driving automation.

- Market growth influenced by continuous R&D investment and evolving vehicle architectures.

Advanced Driver Assistance System Market Drivers Analysis

The Advanced Driver Assistance System (ADAS) market is propelled by several potent drivers, primarily centered around the global imperative for enhanced road safety and the pursuit of autonomous driving capabilities. Stringent government regulations worldwide, mandating the inclusion of specific ADAS features such as Automatic Emergency Braking (AEB) and Lane Departure Warning (LDW), are creating a baseline demand across all new vehicles. This regulatory push is complemented by a growing consumer awareness and demand for advanced safety features, as drivers increasingly prioritize technologies that mitigate risks, reduce accidents, and enhance the overall driving experience. The convergence of these factors creates a fertile ground for ADAS market expansion.

Technological advancements also serve as a significant driver, particularly in the areas of sensor development (radar, lidar, cameras), high-performance computing, and artificial intelligence. These innovations are making ADAS more accurate, reliable, and capable of handling complex driving scenarios, thereby expanding their utility and appeal. The continuous evolution of these core technologies enables the development of sophisticated features, moving beyond basic warnings to active intervention systems and paving the way for conditional and higher levels of autonomy. Furthermore, the automotive industry's strategic shift towards software-defined vehicles and electric vehicles inherently supports ADAS integration, as these platforms are designed with the necessary electrical and electronic architectures to host advanced safety systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Road Safety Regulations | +3.5% | Europe, North America, Asia Pacific | 2025-2033 |

| Growing Consumer Awareness and Demand for Safety Features | +2.8% | North America, Europe, China | 2025-2033 |

| Technological Advancements in Sensors and AI | +3.2% | Global | 2025-2033 |

| Rise of Autonomous Vehicle Development | +2.5% | USA, Germany, Japan, China | 2028-2033 |

Advanced Driver Assistance System Market Restraints Analysis

Despite the strong growth trajectory, the Advanced Driver Assistance System (ADAS) market faces several notable restraints that could temper its expansion. One primary concern is the high cost associated with advanced ADAS components and systems, which can significantly increase the overall manufacturing cost of a vehicle. This cost factor can limit the widespread adoption of comprehensive ADAS suites, especially in cost-sensitive emerging markets or in entry-level vehicle segments, where manufacturers strive to maintain competitive pricing. The expense of integrating complex sensor arrays, high-performance processing units, and sophisticated software often translates into a higher sticker price for consumers, potentially slowing down market penetration.

Another significant restraint involves the complexity of integrating diverse ADAS technologies and ensuring their interoperability across different vehicle platforms and manufacturers. Achieving seamless communication between various sensors, Electronic Control Units (ECUs), and software algorithms from multiple suppliers poses substantial engineering challenges. This complexity extends to calibration, validation, and testing, which are time-consuming and resource-intensive processes crucial for guaranteeing the reliability and safety of ADAS features. Furthermore, the inherent complexity can lead to potential system malfunctions or conflicts if not meticulously managed, impacting consumer trust and adoption rates.

Additionally, cybersecurity risks and data privacy concerns present growing restraints for the ADAS market. As vehicles become more connected and reliant on external data, they become potential targets for cyberattacks, which could compromise system integrity, vehicle control, or sensitive user data. Consumers are increasingly wary of how their driving data is collected, stored, and utilized by vehicle manufacturers and third-party service providers. Addressing these concerns requires robust cybersecurity frameworks, secure data handling protocols, and transparent privacy policies, which add another layer of complexity and cost for manufacturers and can influence consumer acceptance of highly connected and data-intensive ADAS. Regulatory uncertainties surrounding data ownership and liability for autonomous systems also contribute to market hesitations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of ADAS Components and Integration | -2.1% | Global, particularly Emerging Markets | 2025-2030 |

| Complexity of System Integration and Validation | -1.8% | Global | 2025-2033 |

| Cybersecurity Risks and Data Privacy Concerns | -1.5% | North America, Europe | 2025-2033 |

| Limited Consumer Awareness/Trust in Some Regions | -1.0% | Emerging Markets, Specific Demographics | 2025-2028 |

Advanced Driver Assistance System Market Opportunities Analysis

The Advanced Driver Assistance System (ADAS) market is ripe with opportunities, particularly driven by the accelerating journey towards higher levels of autonomous driving and the expansion into new vehicle segments. The push for Level 3 (conditional automation) and Level 4 (high automation) systems presents a significant avenue for growth, requiring more sophisticated sensor suites, powerful AI processors, and redundant systems, thereby increasing the value proposition of integrated ADAS solutions. This transition unlocks new revenue streams for technology providers and automotive manufacturers as they develop and deploy increasingly complex and high-value autonomous functionalities, moving beyond basic driver aids.

Furthermore, the aftermarket segment for ADAS offers substantial growth opportunities. While new vehicle sales are a primary channel, there is a growing demand for retrofitting existing vehicles with ADAS features, especially in regions with a large installed base of older vehicles. This includes solutions for blind spot detection, parking assistance, and dashcam-integrated ADAS, providing accessible safety enhancements without the need for a new vehicle purchase. This segment caters to a broad consumer base and expands the market beyond the new car sales cycle, driven by consumer desire for improved safety and convenience in their current vehicles.

Another promising opportunity lies in the integration of ADAS with Vehicle-to-Everything (V2X) communication technologies. V2X connectivity enables vehicles to communicate with other vehicles, infrastructure, pedestrians, and the cloud, providing a holistic view of the driving environment that is impossible with on-board sensors alone. This synergy allows for predictive collision warnings, optimized traffic flow, and enhanced safety in complex urban settings, opening doors for innovative ADAS applications and services that leverage real-time external data. The development of smart city initiatives and 5G infrastructure further catalyzes this opportunity, creating a connected ecosystem where ADAS can operate with unprecedented levels of awareness and precision, leading to significantly safer and more efficient transportation systems.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Level 3 and 4 Autonomous Driving Systems | +3.0% | North America, Europe, Asia Pacific (China, Japan) | 2027-2033 |

| Expansion into Aftermarket ADAS Solutions | +2.2% | Global, particularly North America, Europe | 2025-2033 |

| Integration with V2X Communication Technologies | +2.5% | Global, especially Smart Cities | 2026-2033 |

| Growth in Commercial Vehicle and Logistics Sector ADAS Adoption | +1.8% | Global | 2025-2033 |

Advanced Driver Assistance System Market Challenges Impact Analysis

The Advanced Driver Assistance System (ADAS) market confronts several significant challenges that necessitate strategic solutions for sustained growth and widespread adoption. One major hurdle is the need for standardization and regulatory harmonization across different regions and countries. The absence of a universally accepted framework for ADAS performance, testing, and deployment creates complexities for manufacturers operating on a global scale, leading to varied safety requirements and hindering the economies of scale. Achieving consensus on regulatory definitions for autonomous levels, liability in case of accidents involving ADAS, and data sharing protocols remains a critical challenge that impacts market predictability and speed of innovation.

Another key challenge pertains to sensor limitations and environmental robustness. Current ADAS sensors, such as cameras and lidar, can be affected by adverse weather conditions like heavy rain, snow, fog, or direct sunlight, which can compromise their accuracy and reliability. This vulnerability impacts the performance of ADAS features in real-world driving scenarios, potentially leading to system disengagement or reduced effectiveness, thereby limiting consumer trust. Developing sensor technologies that maintain high performance across all environmental conditions and lighting scenarios is an ongoing engineering challenge requiring significant research and development investment.

Furthermore, consumer acceptance and trust, particularly for higher levels of automation, pose a notable challenge. While basic ADAS features are widely accepted, there is apprehension among some consumers regarding the reliability and safety of advanced automated systems. Concerns about potential system failures, over-reliance on technology, and the ethical implications of autonomous decision-making can hinder adoption. Overcoming this challenge requires extensive public education, robust testing, transparent communication about system capabilities and limitations, and a flawless safety record to build confidence and foster widespread societal acceptance of increasingly automated vehicles.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Harmonization and Standardization | -1.9% | Global | 2025-2030 |

| Sensor Limitations in Adverse Weather Conditions | -1.7% | Global | 2025-2033 |

| Consumer Acceptance and Trust for Higher Automation Levels | -1.5% | Global | 2025-2033 |

| High Computational Demands and Power Consumption | -1.2% | Global | 2025-2029 |

Advanced Driver Assistance System Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Advanced Driver Assistance System (ADAS) market, encompassing historical data, current market dynamics, and future growth projections from 2025 to 2033. It details market size estimations, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report is designed to offer strategic insights for stakeholders, enabling informed decision-making within the evolving automotive safety and automation landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.8 Billion |

| Market Forecast in 2033 | USD 105.1 Billion |

| Growth Rate | 14.5% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, Magna International Inc., Hyundai Mobis, Aptiv PLC, Veoneer Inc., Mobileye (Intel Corporation), NVIDIA Corporation, Qualcomm Technologies, Inc., NXP Semiconductors N.V., Infineon Technologies AG, Valeo S.A., Renesas Electronics Corporation, Hella GmbH & Co. KGaA, Panasonic Corporation, Texas Instruments Incorporated, Mitsubishi Electric Corporation, Gentex Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Advanced Driver Assistance System (ADAS) market is comprehensively segmented to provide a detailed understanding of its diverse components, applications, and operational contexts. This segmentation allows for precise market sizing and forecasting, identifying key growth areas and technological adoption patterns across different vehicle types, levels of automation, and sales channels. Analyzing these segments reveals the intricate dynamics of the market, from the foundational hardware components to the sophisticated software-driven systems that collectively enhance vehicle safety and autonomy.

- By Component Type: This segment includes the various hardware and software elements crucial for ADAS functionality, such as Cameras, Radar Sensors, Ultrasonic Sensors, Lidar Sensors, and Electronic Control Units (ECUs), along with other ancillary components.

- By System Type: This covers specific ADAS functionalities, including Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Lane Keep Assist (LKA), Blind Spot Detection (BSD), Parking Assist System (PAS), Traffic Sign Recognition (TSR), Driver Monitoring System (DMS), and Night Vision System (NVS), among others.

- By Vehicle Type: This segmentation distinguishes between the application of ADAS in Passenger Cars and Commercial Vehicles, further broken down into Light Commercial Vehicles and Heavy Commercial Vehicles, reflecting their unique operational requirements and adoption rates.

- By Level of Autonomy: This categorizes ADAS based on the Society of Automotive Engineers (SAE) automation levels, ranging from Level 0 (no automation) to Level 5 (full automation), illustrating the progression of autonomous capabilities in vehicles.

- By Sales Channel: This segment differentiates between ADAS systems integrated at the Original Equipment Manufacturer (OEM) stage during vehicle production and those sold through the Aftermarket for retrofitting existing vehicles.

Regional Highlights

- North America: This region is characterized by early adoption of advanced ADAS features, driven by strong consumer demand for safety, significant investments in autonomous driving technologies, and supportive regulatory frameworks. The presence of major automotive OEMs and tech companies fuels innovation and market growth.

- Europe: Europe stands out due to its stringent safety regulations, such as mandatory AEB and LDW, which accelerate ADAS penetration. The region exhibits high consumer awareness regarding vehicle safety and a strong focus on premium vehicle segments, where advanced ADAS features are often standard.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to rapid economic development, increasing vehicle production (especially in China and India), rising disposable incomes, and growing concerns for road safety. Government initiatives and a large, expanding middle class contribute to significant adoption rates.

- Latin America: This region is experiencing gradual ADAS adoption, influenced by evolving safety regulations and increasing awareness. The market here is more cost-sensitive, leading to a higher focus on basic ADAS features, but with potential for growth as economic conditions improve.

- Middle East and Africa (MEA): The MEA region is at an nascent stage of ADAS adoption, with growth primarily concentrated in affluent countries. Development in infrastructure and increasing regulatory emphasis on road safety are expected to drive future growth, particularly for essential safety features.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Advanced Driver Assistance System Market.- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Magna International Inc.

- Hyundai Mobis

- Aptiv PLC

- Veoneer Inc.

- Mobileye (Intel Corporation)

- NVIDIA Corporation

- Qualcomm Technologies, Inc.

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Valeo S.A.

- Renesas Electronics Corporation

- Hella GmbH & Co. KGaA

- Panasonic Corporation

- Texas Instruments Incorporated

- Mitsubishi Electric Corporation

- Gentex Corporation

Frequently Asked Questions

Analyze common user questions about the Advanced Driver Assistance System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Advanced Driver Assistance System (ADAS)?

ADAS refers to electronic systems in vehicles that assist drivers in driving and parking functions. These systems are designed to increase car safety and more generally road safety by warning the driver of potential problems, or by taking over control of the vehicle to avoid a collision.

How does ADAS contribute to vehicle safety?

ADAS enhances vehicle safety by providing features like automatic emergency braking to prevent collisions, lane-keeping assistance to prevent unintentional lane departures, and blind spot detection to warn of unseen vehicles, thereby significantly reducing the risk of accidents and protecting occupants.

What are the key components of an ADAS?

The key components of an ADAS typically include various sensors such as cameras, radar, lidar, and ultrasonic sensors that gather data from the vehicle's surroundings. This data is then processed by an Electronic Control Unit (ECU) which runs complex algorithms to interpret the information and trigger appropriate actions or warnings.

What are the different levels of autonomous driving in ADAS?

The Society of Automotive Engineers (SAE) defines six levels of driving automation, from Level 0 (no automation) to Level 5 (full automation). ADAS primarily covers Levels 1 (driver assistance like adaptive cruise control) and Level 2 (partial automation like combined adaptive cruise control and lane centering), with some systems now progressing towards Level 3 (conditional automation).

What are the primary challenges facing ADAS adoption?

Key challenges for ADAS adoption include the high cost of implementation, which can limit widespread integration into all vehicle segments, the complexity of integrating diverse technologies from multiple vendors, the need for regulatory harmonization across different regions, and consumer acceptance and trust, particularly for higher levels of automation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted