High Voltage Direct Current Transmission System Market

High Voltage Direct Current Transmission System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704330 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

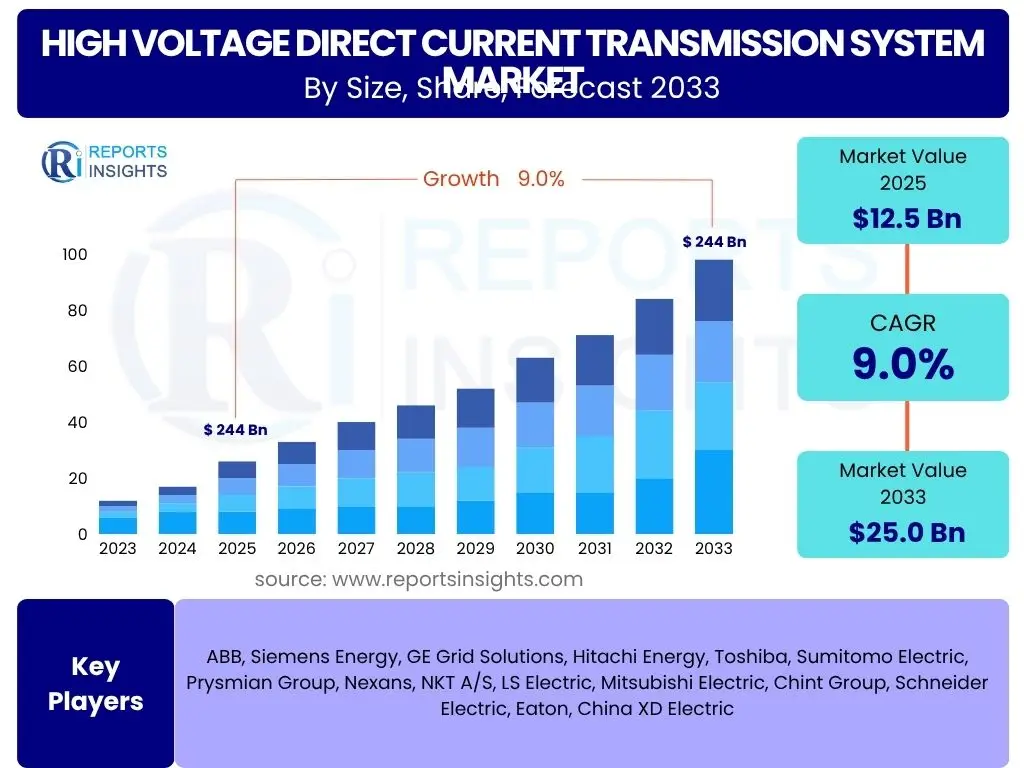

High Voltage Direct Current Transmission System Market Size

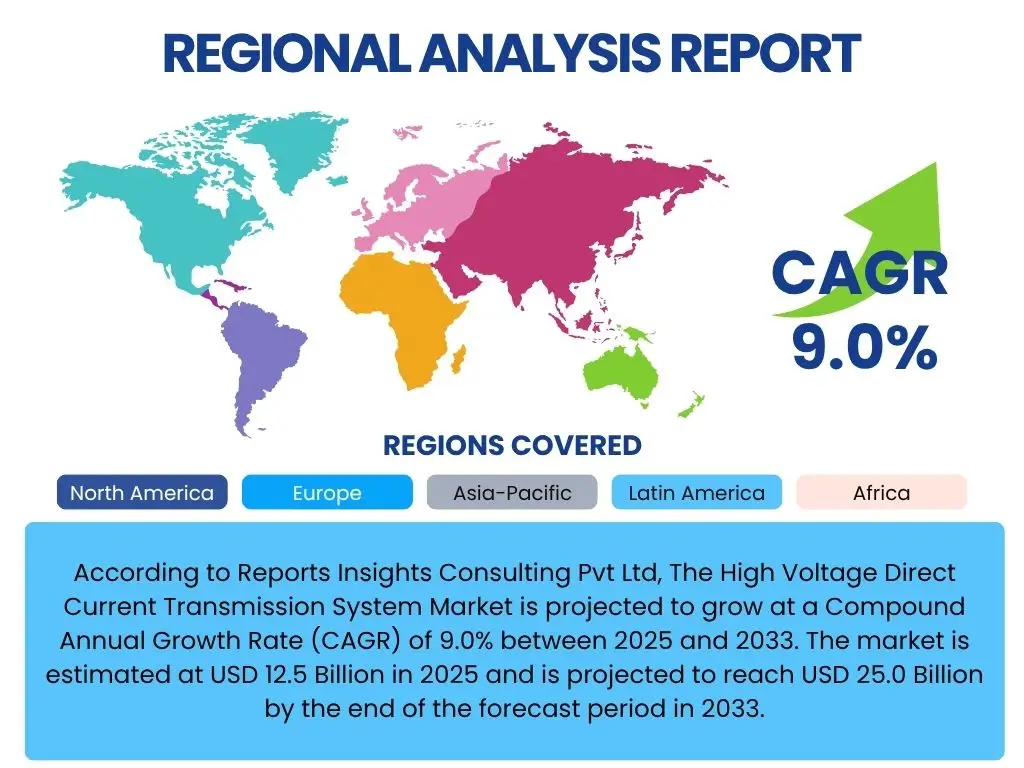

According to Reports Insights Consulting Pvt Ltd, The High Voltage Direct Current Transmission System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.0% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 25.0 Billion by the end of the forecast period in 2033.

Key High Voltage Direct Current Transmission System Market Trends & Insights

The High Voltage Direct Current (HVDC) transmission system market is undergoing a significant transformation, driven by global energy transitions and increasing demands for efficient power delivery. Users frequently inquire about the forces shaping this market, particularly the shift towards renewable energy sources and the critical need for robust, interconnected grids. Key trends indicate a strong focus on enhancing grid stability, integrating distant clean energy generation, and improving the overall efficiency of power transmission. There is a growing emphasis on adopting advanced converter technologies, particularly Voltage Source Converters (VSC), which offer enhanced flexibility and control compared to traditional Line Commutated Converters (LCC). Furthermore, the expansion of international and cross-border grid interconnections is a pivotal trend, as countries seek to leverage diverse energy resources and strengthen regional energy security.

Another significant trend is the increasing investment in offshore power transmission, primarily for connecting large-scale offshore wind farms to national grids. This application leverages HVDC's advantages in long-distance underwater power transfer with minimal losses. Digitalization and smart grid initiatives are also influencing the HVDC market, with an increased adoption of digital control systems, advanced monitoring, and data analytics for improved operational efficiency and predictive maintenance. The growing urgency to reduce carbon emissions globally is accelerating the deployment of HVDC systems, making them an indispensable component of future energy infrastructures. This comprehensive evolution underscores HVDC's role as a cornerstone technology for modern, sustainable power grids.

- Rapid integration of renewable energy sources, especially offshore wind power.

- Increasing global demand for long-distance, high-capacity bulk power transmission.

- Growing adoption of Voltage Source Converter (VSC) technology for enhanced grid control and flexibility.

- Expansion of cross-border and intercontinental grid interconnections for energy security.

- Emphasis on grid modernization and stability enhancements through HVDC solutions.

- Digitalization and implementation of advanced control and monitoring systems in HVDC substations.

AI Impact Analysis on High Voltage Direct Current Transmission System

Users are increasingly curious about the transformative role of Artificial Intelligence (AI) in critical infrastructure sectors, specifically how it might enhance the High Voltage Direct Current (HVDC) transmission system. Common questions revolve around AI's capabilities in improving operational efficiency, predictive maintenance, and overall grid resilience. There is significant expectation that AI can optimize the complex control systems inherent in HVDC, leading to more stable and reliable power flow. Concerns often include data security, the initial investment required for AI integration, and the potential impact on human operational roles. Despite these considerations, the overarching sentiment is that AI holds immense potential to revolutionize how HVDC systems are managed and maintained, offering unprecedented levels of insight and automation.

The deployment of AI in HVDC is anticipated to move beyond conventional automation, enabling systems to learn from operational data, predict potential failures, and adapt to changing grid conditions in real-time. This includes sophisticated fault detection and isolation, optimization of power dispatch, and dynamic control adjustments to prevent system instabilities. The ability of AI to process vast amounts of sensor data from converter stations and transmission lines allows for proactive maintenance scheduling, reducing downtime and operational costs. Moreover, AI can enhance the cybersecurity posture of HVDC systems by identifying anomalous behaviors and potential threats more rapidly than traditional methods. As HVDC systems become more complex and interconnected, AI's role in ensuring their reliable and efficient operation is becoming increasingly vital, making it a key focus for future development and investment in the sector.

- Enhanced predictive maintenance and fault diagnosis in HVDC converter stations.

- Real-time optimization of power flow and grid stability through intelligent control algorithms.

- Improved cybersecurity and anomaly detection for critical infrastructure.

- Advanced data analytics for performance monitoring and operational efficiency improvements.

- Automated system responses to grid disturbances and unforeseen events.

Key Takeaways High Voltage Direct Current Transmission System Market Size & Forecast

The High Voltage Direct Current (HVDC) transmission system market is poised for robust expansion, driven primarily by the global imperative for energy transition and the growing need for resilient power grids. Key inquiries from users often center on understanding the fundamental drivers behind this growth, the dominant technological trends, and the geographical regions experiencing the most significant development. The market forecast indicates substantial investment across various applications, underscoring the critical role HVDC plays in modern energy infrastructure. The insights reveal that the market's trajectory is strongly influenced by policy support for renewable energy, advancements in converter technologies, and the increasing demand for cross-border electricity trade. Furthermore, strategic collaborations and technological innovation are anticipated to be pivotal in shaping the competitive landscape.

A central takeaway is the pervasive adoption of Voltage Source Converter (VSC) technology, which continues to drive market innovation due to its inherent advantages in flexibility, modularity, and black start capabilities. Regions such as Asia Pacific and Europe are identified as frontrunners in HVDC deployment, fueled by ambitious renewable energy targets and extensive grid modernization efforts. While high initial capital costs and complex regulatory frameworks present notable challenges, the long-term benefits of HVDC in terms of efficiency, reduced transmission losses, and enhanced grid stability overwhelmingly support continued market growth. Stakeholders across the energy value chain are increasingly recognizing HVDC as an indispensable component for achieving sustainable and interconnected global energy systems.

- The HVDC market is experiencing significant growth, projected to double in value by 2033, reflecting its critical role in global energy infrastructure.

- Integration of renewable energy sources, particularly offshore wind, is a primary catalyst for market expansion.

- Voltage Source Converter (VSC) technology is a key enabler, offering advanced control and operational flexibility.

- Asia Pacific and Europe are leading regional markets due to substantial investments in grid modernization and renewable energy projects.

- Despite high initial costs and regulatory complexities, HVDC offers long-term benefits in transmission efficiency and grid stability.

- Strategic partnerships and continuous technological innovation are vital for competitive advantage and market development.

High Voltage Direct Current Transmission System Market Drivers Analysis

The expansion of the High Voltage Direct Current (HVDC) transmission system market is propelled by several fundamental drivers that align with global energy transition goals and the increasing complexity of modern power grids. A primary driver is the accelerating integration of large-scale renewable energy sources, such as distant wind farms (onshore and offshore) and solar power plants, which often require efficient long-distance transmission to demand centers. HVDC technology is uniquely suited for this purpose, minimizing transmission losses over vast distances and enabling the stable integration of intermittent renewable power into existing AC grids. Governments and energy companies worldwide are heavily investing in green energy initiatives, directly stimulating the demand for HVDC solutions.

Another significant driver is the growing need for enhanced grid interconnections and cross-border power trade. As countries seek to improve energy security, optimize resource utilization, and balance supply and demand across regions, HVDC links facilitate the seamless exchange of electricity between asynchronous AC grids. These interconnections not only bolster grid stability but also allow for the diversification of energy sources, reducing reliance on single-point generation. Furthermore, the increasing demand for electricity driven by urbanization, industrialization, and electrification of transport systems globally places immense pressure on existing grid infrastructure, necessitating the deployment of high-capacity and efficient transmission solutions like HVDC.

Lastly, governmental support through favorable policies, subsidies, and regulatory frameworks for grid modernization and renewable energy deployment significantly contributes to market growth. Many nations have set ambitious targets for decarbonization and grid resilience, providing a strong impetus for investment in advanced transmission technologies. The inherent advantages of HVDC, such as lower transmission losses, smaller right-of-way requirements compared to AC lines, and superior control capabilities, make it an attractive solution for utilities and grid operators seeking to build a more robust, efficient, and sustainable power infrastructure for the future.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Renewable Energy Sources | +3.5% | Europe, Asia Pacific, North America | Mid-term to Long-term |

| Growing Demand for Grid Interconnection and Cross-Border Power Trade | +2.8% | Europe, Asia Pacific, South America | Mid-term |

| Need for Grid Stability and Resilience | +1.5% | Global | Short-term to Mid-term |

| Urbanization and Industrialization Driving Electricity Demand | +1.2% | Asia Pacific, Middle East, Africa | Long-term |

| Government Initiatives and Policy Support for Sustainable Energy | +1.0% | Global | Short-term to Long-term |

High Voltage Direct Current Transmission System Market Restraints Analysis

Despite the strong growth prospects for the High Voltage Direct Current (HVDC) transmission system market, several significant restraints pose challenges to its wider adoption and development. A primary impediment is the high initial capital investment required for HVDC projects. The complex converter stations, specialized equipment, and extensive engineering involved in designing and constructing HVDC links translate into substantial upfront costs, which can be a deterrent for utilities and project developers, particularly in regions with limited financial resources or uncertain regulatory environments. This high cost often necessitates long-term financial planning and substantial funding, potentially slowing down project approvals and implementation timelines compared to conventional AC infrastructure.

Another critical restraint involves the complex regulatory frameworks and extensive permitting processes associated with large-scale HVDC projects. Gaining approvals for new transmission lines, especially those crossing multiple jurisdictions or international borders, can be a protracted and challenging endeavor. Environmental impact assessments, land acquisition issues, and public opposition (often referred to as NIMBY - Not In My Backyard) can lead to significant delays, increased project costs, and even project cancellations. The lack of standardized regulations across different countries can further complicate cross-border projects, requiring intricate negotiations and compliance with diverse legal requirements, adding layers of complexity to project execution.

Furthermore, cybersecurity risks represent a growing concern for HVDC systems. As these systems become increasingly digitized and interconnected, they become more vulnerable to cyberattacks that could disrupt power flow, compromise sensitive operational data, or even cause widespread blackouts. Protecting these critical infrastructure assets from sophisticated cyber threats requires continuous investment in advanced security measures and robust monitoring systems, adding to the operational complexity and cost. Lastly, the inherent technological complexity of HVDC systems, particularly Voltage Source Converters (VSCs), necessitates a highly skilled workforce for design, installation, operation, and maintenance. A shortage of qualified engineers and technicians in this specialized field can limit deployment capabilities and increase labor costs, posing a long-term challenge to market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment and Project Costs | -2.0% | Global | Short-term to Mid-term |

| Complex Regulatory and Permitting Processes | -1.5% | North America, Europe | Mid-term |

| Land Acquisition and Public Opposition (NIMBY) | -1.0% | Europe, North America | Mid-term to Long-term |

| Cybersecurity Risks and System Vulnerabilities | -0.8% | Global | Short-term to Long-term |

| Technological Complexity and Skilled Workforce Requirements | -0.7% | Global | Long-term |

High Voltage Direct Current Transmission System Market Opportunities Analysis

The High Voltage Direct Current (HVDC) transmission system market is characterized by numerous strategic opportunities that are set to drive its future expansion and innovation. A significant opportunity lies in the burgeoning offshore wind power sector. As countries globally invest heavily in large-scale offshore wind farms to meet renewable energy targets, HVDC technology becomes indispensable for efficiently transmitting power from these distant generation sites to onshore grids. The ability of HVDC to minimize losses over long subsea cables and provide stable grid connections makes it the preferred choice for this rapidly expanding segment. The sheer scale of planned offshore wind projects presents a substantial and sustained demand for new HVDC installations.

Another substantial opportunity arises from the ongoing development of smart grids and increasing digitalization within the power sector. Integration of advanced digital technologies, including AI, IoT, and big data analytics, into HVDC systems can unlock new levels of efficiency, predictive maintenance, and operational control. This transition towards smarter, more interconnected grids creates demand for HVDC solutions that can seamlessly integrate with these digital platforms, enabling dynamic power management and enhanced grid resilience. Utilities are increasingly seeking solutions that offer real-time monitoring and adaptive control, which aligns perfectly with the evolving capabilities of modern HVDC systems.

Furthermore, continuous advancements in Voltage Source Converter (VSC) technology present a profound opportunity. VSC-HVDC systems offer enhanced flexibility, lower harmonic distortion, and easier integration with weak AC grids compared to traditional LCC-HVDC. Innovations such as multi-level converters and hybrid HVDC systems are expanding the application possibilities, making HVDC suitable for a wider range of scenarios, including urban infeed and connecting isolated loads. The ongoing research and development in areas like superconducting HVDC and modular solutions promise to further reduce costs, improve efficiency, and simplify deployment, thereby creating new market niches. Finally, the growing electricity needs in emerging economies, coupled with their efforts to modernize aging infrastructure and integrate renewable energy, represent a vast untapped market for HVDC technology. These regions can leapfrog conventional grid development by directly adopting advanced HVDC solutions, facilitating rapid and sustainable electrification.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Offshore Wind Farms | +4.0% | Europe, Asia Pacific, North America | Mid-term to Long-term |

| Development of Smart Grids and Digitalization | +2.5% | Global | Mid-term |

| Advancements in Voltage Source Converter (VSC) Technology | +2.0% | Global | Short-term to Long-term |

| Emerging Markets with Growing Electricity Needs | +1.5% | Asia Pacific, Africa, Latin America | Long-term |

| Potential for Green Hydrogen Production and Transmission | +1.0% | Europe, Australia, Middle East | Long-term |

High Voltage Direct Current Transmission System Market Challenges Impact Analysis

Despite its significant advantages, the High Voltage Direct Current (HVDC) transmission system market faces several pertinent challenges that could impede its growth and widespread adoption. One critical challenge is grid congestion and the complex integration issues that arise when incorporating new HVDC links into existing AC grid infrastructures. Ensuring seamless operation and maintaining grid stability while connecting asynchronous HVDC systems requires sophisticated planning, advanced control strategies, and extensive coordination among grid operators. The increasing penetration of HVDC can also lead to new forms of grid interaction challenges, such as sub-synchronous resonance, which demand innovative mitigation techniques and robust system design.

Another substantial challenge revolves around environmental and social impact concerns related to the construction of new transmission lines and converter stations. Public acceptance issues, often stemming from visual impact, potential electromagnetic fields, and the disruption of local ecosystems, can lead to strong opposition and protracted legal battles. Securing right-of-way for long-distance HVDC lines through diverse landscapes requires careful environmental assessments, community engagement, and often complex compensation negotiations. These factors can significantly delay project timelines and escalate overall costs, making the planning and execution phases particularly arduous for developers.

Furthermore, global supply chain disruptions and volatile material costs present ongoing challenges for HVDC project delivery. The highly specialized components required for HVDC systems, such as power semiconductors, transformers, and high-performance cables, rely on a global manufacturing and supply network. Geopolitical events, trade disputes, and natural disasters can disrupt these supply chains, leading to material shortages, extended lead times, and unpredictable price fluctuations. This instability can impact project budgets and timelines, making it difficult for developers to adhere to original estimates. Lastly, the lack of standardization across different HVDC systems and manufacturers poses compatibility and interoperability challenges, particularly for multi-vendor projects or future grid expansions. While efforts are underway to establish common standards, the fragmented nature of the market can complicate maintenance, upgrades, and future interconnections, potentially increasing operational complexities and costs for grid operators.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Grid Congestion and Integration Issues | -1.8% | Global | Short-term to Mid-term |

| Environmental and Social Impact Concerns | -1.4% | Europe, North America, Asia Pacific | Mid-term to Long-term |

| Supply Chain Disruptions and Material Costs | -1.2% | Global | Short-term |

| Lack of Standardization Across HVDC Systems | -0.9% | Global | Long-term |

| Talent Shortage in HVDC Engineering and Operations | -0.6% | Global | Long-term |

High Voltage Direct Current Transmission System Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the High Voltage Direct Current (HVDC) Transmission System Market, offering a detailed segmentation by technology, configuration, components, application, and voltage level. It covers market trends, drivers, restraints, opportunities, and challenges, providing a strategic outlook for stakeholders. The report meticulously examines historical data from 2019 to 2023, establishes 2024 as the base year, and projects market growth through 2033, including detailed market size estimations for 2025 and 2033. Furthermore, it highlights the impact of emerging technologies like AI and profiles key market players, offering regional insights across North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 25.0 Billion |

| Growth Rate | 9.0% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB, Siemens Energy, GE Grid Solutions, Hitachi Energy, Toshiba, Sumitomo Electric, Prysmian Group, Nexans, NKT A/S, LS Electric, Mitsubishi Electric, Chint Group, Schneider Electric, Eaton, China XD Electric |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The High Voltage Direct Current (HVDC) transmission system market is extensively segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for a detailed analysis of market dynamics, identifying key growth areas and technological preferences across various industry verticals and geographical regions. Understanding these distinct segments is crucial for stakeholders to develop targeted strategies, optimize resource allocation, and identify emerging opportunities within the complex landscape of power transmission.

- By Technology: This segment distinguishes between Line Commutated Converters (LCC) and Voltage Source Converters (VSC). LCC technology, traditionally used for bulk power transfer, offers robustness, while VSC technology provides greater flexibility, black start capability, and independent control of active and reactive power, making it ideal for offshore wind integration and weak grid connections.

- By Configuration: The market is analyzed based on different system configurations including Monopolar, Bipolar, and Back-to-Back. Monopolar systems are the simplest, while bipolar systems offer redundancy and often operate at higher voltage levels. Back-to-Back configurations are used for interconnecting two asynchronous AC networks without a long transmission line.

- By Component: Key components of an HVDC system are categorized, encompassing Converters (the heart of the system), Transformers (stepping up/down voltages), Harmonic Filters (to manage power quality), Circuit Breakers (for protection), DC Cables (for transmission), and Other ancillary equipment. Each component plays a vital role in the overall system's functionality and efficiency.

- By Application: This segmentation highlights the primary uses of HVDC systems, including Grid Interconnection (connecting different power networks), Offshore Power Transmission (especially for renewable energy), Renewable Energy Integration (beyond offshore, including large-scale solar and onshore wind), Urban Infeed (delivering power to dense urban areas), and Other Industrial Applications (such as power supply to large industrial complexes).

- By Voltage Level: HVDC systems are classified by their operational voltage levels: Below 500 kV, 500-800 kV, and Above 800 kV (Ultra-High Voltage DC or UHVDC). Higher voltage levels enable more efficient long-distance power transmission and greater power capacity.

Regional Highlights

- Asia Pacific (APAC): This region is a dominant market due to rapid industrialization, burgeoning electricity demand, and extensive investments in renewable energy infrastructure, particularly in China and India. Large-scale grid expansion projects and cross-border interconnections are significant drivers.

- Europe: Europe stands as a leading market driven by ambitious renewable energy targets, especially for offshore wind power integration, and the strong emphasis on building a unified European energy market through extensive grid interconnections between member states.

- North America: The market in North America is characterized by efforts to modernize aging grid infrastructure, integrate renewable energy from remote areas, and enhance grid resilience. Investments in interregional transmission lines are a key focus.

- Latin America: This region is experiencing growth driven by increasing electricity demand, the exploitation of hydropower resources often located far from consumption centers, and the development of regional grid integration initiatives.

- Middle East and Africa (MEA): Emerging as a high-growth market, MEA benefits from significant investments in large-scale solar power projects, urbanization, industrial expansion, and ambitious plans for regional power pools, particularly in the Gulf Cooperation Council (GCC) countries and North Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the High Voltage Direct Current Transmission System Market.- ABB

- Siemens Energy

- GE Grid Solutions

- Hitachi Energy

- Toshiba

- Sumitomo Electric

- Prysmian Group

- Nexans

- NKT A/S

- LS Electric

- Mitsubishi Electric

- Chint Group

- Schneider Electric

- Eaton

- China XD Electric

Frequently Asked Questions

What is High Voltage Direct Current (HVDC) technology and why is it important?

High Voltage Direct Current (HVDC) is an electrical power transmission system that uses direct current for the bulk transmission of electrical power, in contrast to the more common alternating current (AC) systems. It is crucial for long-distance power transmission, interconnecting asynchronous grids, and integrating large-scale renewable energy sources because it minimizes transmission losses, enhances grid stability, and offers precise power control.

What are the primary drivers for the HVDC market's growth?

The main drivers for the HVDC market's growth include the increasing integration of remote renewable energy sources (especially offshore wind), the rising demand for cross-border grid interconnections to enhance energy security, and the critical need for grid stability and resilience in modern power systems. Favorable government policies and urbanization-driven electricity demand also play significant roles.

How does HVDC differ from High Voltage Alternating Current (HVAC) transmission?

HVDC transmits electricity as direct current, while HVAC uses alternating current. HVDC is more efficient for long distances and undersea cables due to lower losses and no reactive power flow. It also allows the interconnection of asynchronous grids and offers better power flow control. HVAC is more common for shorter distances and extensive branched networks due to easier voltage transformation and fault interruption.

What are the key applications of HVDC systems?

Key applications of HVDC systems include long-distance bulk power transmission, interconnecting asynchronous AC grids (e.g., between different countries or regions), integrating large-scale renewable energy sources (such as offshore wind farms), feeding power into congested urban areas, and stabilizing weak AC networks.

What technological advancements are shaping the future of HVDC?

The future of HVDC is largely shaped by advancements in Voltage Source Converter (VSC) technology, leading to more flexible and compact systems. Other key advancements include the development of multi-level converters, hybrid HVDC systems, intelligent control and protection systems incorporating AI, and continued research into UHVDC (Ultra-High Voltage DC) for even greater transmission capacities and efficiency over longer distances.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted