Thin Film Precursor Market

Thin Film Precursor Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707619 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Thin Film Precursor Market Size

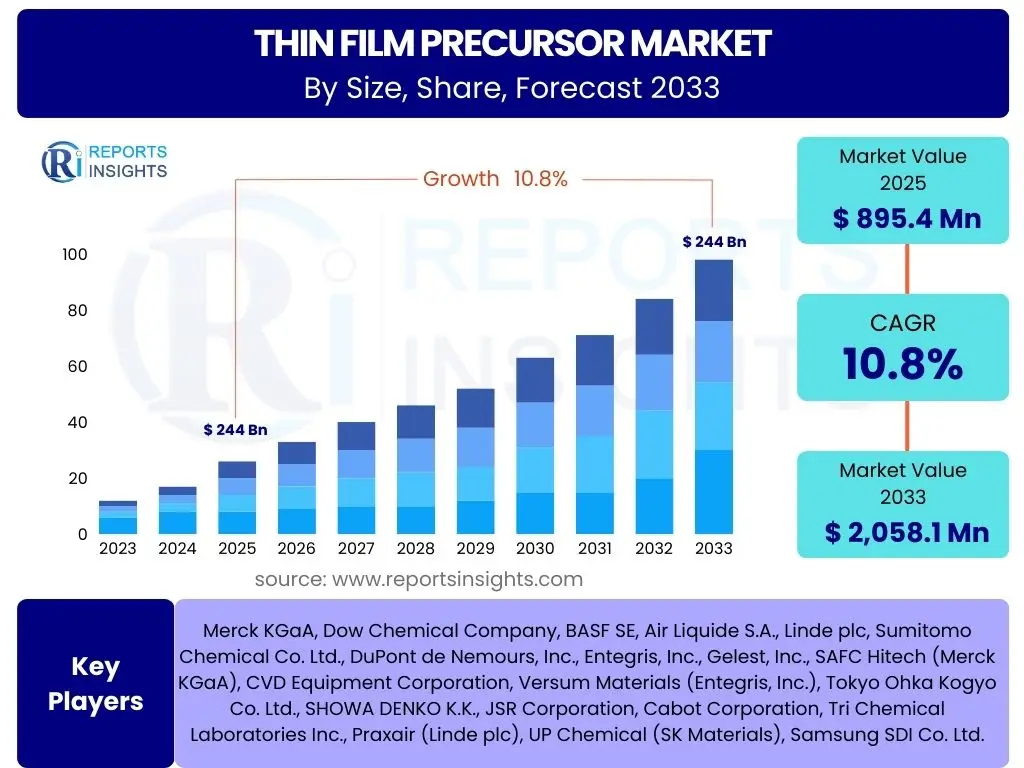

According to Reports Insights Consulting Pvt Ltd, The Thin Film Precursor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 895.4 million in 2025 and is projected to reach USD 2,058.1 million by the end of the forecast period in 2033.

Key Thin Film Precursor Market Trends & Insights

User queries regarding the Thin Film Precursor market frequently center on emerging technological shifts, material advancements, and applications driving demand. Key insights reveal a significant push towards high-purity and novel precursor materials essential for advanced semiconductor fabrication and next-generation display technologies. The industry is witnessing a trend toward environmentally benign and sustainable precursor chemistries to align with stricter regulatory frameworks and corporate sustainability goals. Additionally, the miniaturization of electronic components and the increasing complexity of integrated circuits necessitate more precise and efficient deposition techniques, directly impacting precursor development and adoption.

A notable trend is the escalating demand from the photovoltaics sector, particularly for thin-film solar cells, where precursors enable higher efficiency and lower manufacturing costs. Furthermore, there is a growing interest in precursors for Atomic Layer Deposition (ALD) due to its ability to create highly conformal and uniform thin films with atomic-level control, crucial for sub-nanometer scale devices. The convergence of these trends points towards a market prioritizing performance, environmental responsibility, and manufacturing precision.

- Growing demand for high-purity and novel precursor materials in advanced electronics.

- Increased adoption of ALD and CVD techniques driving demand for specialized precursors.

- Focus on environmentally benign and sustainable precursor chemistries.

- Miniaturization and increasing complexity of semiconductor devices.

- Expansion of applications in photovoltaics and flexible electronics.

AI Impact Analysis on Thin Film Precursor

User inquiries about the impact of Artificial Intelligence (AI) on the Thin Film Precursor domain primarily revolve around process optimization, material discovery, and quality control. AI's ability to analyze vast datasets from deposition processes enables real-time adjustments, significantly enhancing film uniformity, composition, and overall yield. This data-driven approach minimizes material waste and reduces manufacturing costs, directly benefiting precursor utilization efficiency. Furthermore, AI algorithms are being employed in computational chemistry to accelerate the discovery and design of new precursor molecules with desired properties, such as improved volatility, thermal stability, or reduced toxicity, thereby shortening development cycles for advanced materials.

In the realm of predictive maintenance, AI monitors the performance of deposition equipment and precursor delivery systems, foreseeing potential failures before they occur. This proactive maintenance reduces downtime and ensures consistent film quality, which is paramount in high-precision manufacturing environments. Additionally, AI-powered vision systems are being integrated for automated defect detection on thin films, allowing for immediate identification and correction of process anomalies. The overarching expectation is that AI will drive efficiency, innovation, and quality improvements across the entire thin film precursor value chain, from synthesis to application.

- Optimization of thin film deposition processes for improved yield and quality.

- Accelerated discovery and design of novel thin film precursor materials.

- Predictive maintenance for precursor delivery systems and deposition equipment.

- Enhanced quality control and automated defect detection in thin film manufacturing.

- Data-driven insights for efficient resource utilization and cost reduction.

Key Takeaways Thin Film Precursor Market Size & Forecast

User questions regarding the key takeaways from the Thin Film Precursor market size and forecast highlight interest in market growth trajectories, dominant application areas, and influential regional dynamics. The market is poised for robust expansion, primarily fueled by the incessant innovation within the semiconductor industry and the global transition towards renewable energy sources, particularly solar power. The forecast indicates sustained growth driven by the escalating demand for high-performance electronic components and advanced materials, which rely heavily on precise thin film deposition. This expansion is further supported by ongoing research and development efforts aimed at introducing new precursor chemistries and optimizing existing ones for enhanced performance and environmental compliance.

A crucial takeaway is the increasing strategic importance of Asia Pacific, which is projected to maintain its leadership position due to its extensive manufacturing base for semiconductors, displays, and solar cells. North America and Europe are expected to contribute significantly through their strong R&D infrastructure and adoption of cutting-edge technologies. The market's growth is also underpinned by the shift towards atomic layer deposition (ALD) and advanced chemical vapor deposition (CVD) techniques, which demand highly specialized and pure precursor materials. Ultimately, the market's trajectory is firmly linked to technological advancements across multiple high-growth industries, making it a critical enabling sector.

- Significant growth anticipated due to semiconductor industry expansion and renewable energy adoption.

- Asia-Pacific is projected to remain the dominant region in terms of consumption and manufacturing.

- Increasing R&D investments in novel and high-purity precursor materials are vital.

- Technological advancements in ALD and CVD are key drivers for specialized precursor demand.

- The market is essential for enabling miniaturization and performance enhancements in electronic devices.

Thin Film Precursor Market Drivers Analysis

The Thin Film Precursor market is significantly propelled by the relentless expansion of the global semiconductor industry, which forms the foundational demand for these specialized chemicals. As integrated circuits become more complex, dense, and miniaturized, the necessity for atomic-level precision in deposition processes intensifies. This drives the adoption of advanced techniques like Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD), which are highly dependent on high-purity and specialized precursor materials. The ongoing development of new memory technologies, advanced logic devices, and micro-electromechanical systems (MEMS) consistently fuels the need for novel and improved precursors capable of meeting stringent performance and yield requirements.

Another major driver is the burgeoning demand for thin-film solar cells, driven by increasing global efforts towards sustainable energy and favorable government policies. Thin film technology offers advantages such as flexibility, lower material consumption, and diverse applications in large-area photovoltaics. Precursors play a critical role in manufacturing these cells efficiently and cost-effectively, contributing to higher conversion efficiencies and reduced environmental impact. Furthermore, advancements in display technologies, including OLED and flexible displays, and the growth of advanced packaging solutions in electronics, also contribute substantially to the market’s upward trajectory by creating diverse application opportunities for thin film deposition.

The continuous innovation in material science and engineering, leading to the development of new functional materials with tailored properties, further stimulates the demand for thin film precursors. Researchers and manufacturers are actively exploring new chemistries to enhance film quality, improve deposition rates, and reduce process temperatures, thereby broadening the applicability of thin films across various industries. This pursuit of enhanced material performance and manufacturing efficiency ensures a steady demand for a diverse range of high-quality precursor materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Semiconductor Industry | +3.5% | Global, particularly Asia Pacific (Taiwan, South Korea, China) | Short to Long Term (2025-2033) |

| Increasing Demand for Photovoltaics | +2.8% | Asia Pacific (China, India), Europe, North America | Medium to Long Term (2026-2033) |

| Advancements in Display Technologies | +1.9% | Asia Pacific (South Korea, Japan, China) | Short to Medium Term (2025-2030) |

| Rising Adoption of Advanced Packaging | +1.5% | North America, Asia Pacific | Medium Term (2027-2032) |

| Increased R&D in Novel Materials | +1.1% | Global, especially North America, Europe, Japan | Long Term (2028-2033) |

Thin Film Precursor Market Restraints Analysis

The Thin Film Precursor market faces significant restraints primarily due to the high production cost and complexity associated with synthesizing ultra-high purity materials. Precursors, especially those used in advanced semiconductor fabrication, require meticulous synthesis processes and rigorous purification steps to meet the extremely stringent purity specifications. Any trace impurities can lead to defects in the thin film, compromising device performance and yield. This intricate production process drives up manufacturing costs, which can, in turn, affect the overall cost-effectiveness of thin film deposition processes and potentially limit broader adoption in cost-sensitive applications.

Supply chain complexities and volatility in raw material prices also act as considerable restraints. The specialized nature of precursor chemicals often means reliance on a limited number of suppliers for specific raw materials, making the supply chain vulnerable to disruptions such as geopolitical tensions, trade restrictions, or natural disasters. Fluctuations in the prices of key raw materials directly impact the production costs of precursors, leading to unpredictable pricing for end-users and affecting market stability. Furthermore, the intellectual property landscape surrounding novel precursor chemistries is highly fragmented and fiercely protected, creating barriers to entry for new players and increasing the cost of innovation through licensing agreements or litigation.

Another notable restraint is the inherent toxicity and hazardous nature of certain precursor chemicals. Many common precursors are pyrophoric, corrosive, or highly reactive, necessitating specialized handling, storage, and transportation protocols. This not only increases operational costs due to safety measures and compliance but also poses significant environmental and health risks if not managed properly. Stringent environmental regulations concerning the use and disposal of hazardous chemicals add further compliance burdens and costs, potentially slowing down the adoption of some high-performance but hazardous precursor materials, pushing research towards more benign alternatives.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Cost of Ultra-High Purity Precursors | -2.1% | Global | Short to Long Term (2025-2033) |

| Supply Chain Complexities & Raw Material Volatility | -1.8% | Global | Short to Medium Term (2025-2030) |

| Environmental and Health Concerns of Hazardous Precursors | -1.5% | Europe, North America, Japan | Medium to Long Term (2027-2033) |

| Stringent Regulatory Compliance | -1.2% | Europe, North America, East Asia | Medium Term (2026-2031) |

| Competition from Alternative Deposition Methods | -0.9% | Global | Medium Term (2027-2032) |

Thin Film Precursor Market Opportunities Analysis

The Thin Film Precursor market presents significant opportunities driven by the emergence of new applications beyond traditional electronics and solar cells. The healthcare and biotechnology sectors, for instance, are increasingly utilizing thin films for medical sensors, implantable devices, and drug delivery systems, creating a niche but high-value demand for biocompatible and precise precursor materials. The development of advanced flexible electronics, wearable devices, and the Internet of Things (IoT) further expands the application scope, requiring precursors suitable for deposition on diverse substrates and at lower temperatures. These sectors offer avenues for market diversification and the development of highly specialized precursor chemistries tailored to specific functional requirements.

Another substantial opportunity lies in the continuous innovation and development of eco-friendly and sustainable precursor chemistries. As environmental regulations become stricter and industry focus shifts towards green manufacturing, there is a growing demand for precursors that are less toxic, less hazardous, and produce fewer harmful byproducts. Companies investing in research and development to produce fluorine-free, halogen-free, or lower global warming potential (GWP) precursors will gain a competitive edge and address a critical market need. This trend not only aligns with global sustainability goals but also opens up new markets where environmental compliance is a primary concern.

Furthermore, the increasing adoption of 3D ICs and advanced packaging technologies offers a burgeoning opportunity. As chip stacking and heterogeneous integration become more prevalent to achieve higher performance and smaller form factors, the need for highly conformal and uniform thin films in complex 3D structures intensifies. This drives demand for precursors suitable for high-aspect-ratio features and low-temperature deposition processes. Strategic partnerships and collaborations between precursor manufacturers, equipment suppliers, and end-users are also key opportunities, fostering innovation, reducing R&D costs, and accelerating market entry for novel solutions. These collaborations facilitate the co-development of optimized processes and materials, addressing specific industry challenges more effectively.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Healthcare & Biotech | +2.3% | North America, Europe, Japan | Medium to Long Term (2027-2033) |

| Development of Eco-Friendly & Sustainable Precursors | +1.9% | Europe, North America, South Korea | Medium to Long Term (2026-2033) |

| Increasing Adoption of 3D ICs & Advanced Packaging | +1.7% | Global, particularly Asia Pacific | Short to Medium Term (2025-2030) |

| Expansion into Flexible Electronics & IoT Devices | +1.4% | Asia Pacific, North America | Medium Term (2027-2032) |

| Strategic Partnerships & Collaborations | +1.1% | Global | Short to Long Term (2025-2033) |

Thin Film Precursor Market Challenges Impact Analysis

The Thin Film Precursor market faces significant challenges related to the stringent purity and consistency requirements demanded by advanced manufacturing processes. The performance of a thin film device, particularly in semiconductors, is highly sensitive to the presence of even trace impurities or variations in precursor composition. Achieving and maintaining ultra-high purity levels for metal-organic and inorganic precursors throughout synthesis, purification, and delivery is technically challenging and resource-intensive. Any deviation can lead to defects, affecting device yield and reliability, which directly impacts manufacturing costs and time-to-market for complex electronic components. This constant need for unparalleled material quality puts immense pressure on precursor manufacturers to invest heavily in advanced analytical techniques and quality control measures.

Another major challenge is technological obsolescence, driven by the rapid pace of innovation in the semiconductor and display industries. As new device architectures and fabrication techniques emerge, the demand for specific precursor chemistries can shift rapidly. Precursor manufacturers must continuously invest in research and development to anticipate future material needs and develop novel chemistries that are compatible with next-generation processes. This includes developing precursors that enable lower deposition temperatures, higher film growth rates, or offer improved selectivity, often requiring significant capital investment and long development cycles without guaranteed returns. Failure to adapt quickly can result in significant market share loss.

Furthermore, volatile raw material prices and the complexities of logistics for hazardous chemicals pose ongoing operational challenges. Many precursors rely on niche raw materials, whose prices can fluctuate based on global supply and demand dynamics, impacting the overall cost structure and profitability for manufacturers. The hazardous nature of some precursors, being pyrophoric, corrosive, or toxic, necessitates specialized and expensive packaging, transportation, and storage solutions, complicating global distribution networks. Adherence to a myriad of international and regional regulatory compliance standards for hazardous materials adds another layer of complexity and cost, requiring robust safety protocols and comprehensive risk management strategies to ensure safe handling and mitigate environmental impact.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Purity and Consistency Requirements | -2.3% | Global | Short to Long Term (2025-2033) |

| Technological Obsolescence & Rapid Innovation Cycles | -2.0% | Global | Short to Medium Term (2025-2030) |

| Volatile Raw Material Prices & Supply Chain Risk | -1.6% | Global | Short Term (2025-2027) |

| Stringent Regulatory Compliance & Handling Costs | -1.3% | Europe, North America, Japan | Medium to Long Term (2026-2033) |

| Intellectual Property & Patent Disputes | -1.0% | Global | Long Term (2028-2033) |

Thin Film Precursor Market - Updated Report Scope

This report provides a comprehensive analysis of the Thin Film Precursor market, covering its size, growth projections, key trends, drivers, restraints, opportunities, and challenges from 2025 to 2033. It details market segmentation by type, application, end-use industry, and deposition method, offering granular insights into each category. The report also includes a thorough regional analysis and profiles of key market players, delivering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 895.4 million |

| Market Forecast in 2033 | USD 2,058.1 million |

| Growth Rate | 10.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Merck KGaA, Dow Chemical Company, BASF SE, Air Liquide S.A., Linde plc, Sumitomo Chemical Co. Ltd., DuPont de Nemours, Inc., Entegris, Inc., Gelest, Inc., SAFC Hitech (Merck KGaA), CVD Equipment Corporation, Versum Materials (Entegris, Inc.), Tokyo Ohka Kogyo Co. Ltd., SHOWA DENKO K.K., JSR Corporation, Cabot Corporation, Tri Chemical Laboratories Inc., Praxair (Linde plc), UP Chemical (SK Materials), Samsung SDI Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Thin Film Precursor market is comprehensively segmented to provide a detailed understanding of its diverse landscape and the dynamics influencing various sub-sectors. This segmentation allows for precise analysis of growth drivers, technological shifts, and application-specific demands across the market. Each segment represents a critical facet of the industry, reflecting different chemistries, end-uses, and manufacturing processes, enabling a granular view of market opportunities and challenges.

The categorization by type highlights the chemical composition and form of the precursors, which directly impacts their properties and suitability for different deposition techniques. Application segmentation sheds light on the primary industries and specific device types where thin films are employed, indicating areas of high growth and technological advancement. End-use industry breakdown provides a broader economic perspective, showing how various sectors like electronics, energy, and automotive drive overall demand. Finally, the deposition method segment details the technologies used to apply the thin films, underscoring the specific requirements for precursors in processes like CVD and ALD, which are critical for precision manufacturing.

- By Type:

- Metal-Organic Precursors: Organometallic compounds used for depositing metal, metal oxide, and metal nitride films.

- Inorganic Precursors: Compounds like hydrides, halides, or simple inorganic salts, often used for elemental or binary compound films.

- Hydride Precursors: Compounds containing hydrogen and another element, common in semiconductor manufacturing for Group III-V materials.

- Halide Precursors: Compounds containing a halogen element, used for various metal and non-metal thin films.

- By Application:

- Semiconductors: Critical for integrated circuits, transistors, and memory devices.

- Solar Cells: Used in the fabrication of thin-film photovoltaic devices.

- Displays: Essential for OLED, LCD, and other advanced display technologies.

- Optical Coatings: Applied in lenses, mirrors, and other optical components for enhanced performance.

- Data Storage: Utilized in hard drives and other magnetic/optical storage media.

- MEMS (Micro-Electro-Mechanical Systems): For micro-sensors, actuators, and other miniature devices.

- Medical Devices: For biocompatible coatings and sensors in healthcare applications.

- Advanced Packaging: For interconnections and insulation in modern chip packaging.

- By End-Use Industry:

- Electronics: Encompasses semiconductors, displays, and consumer electronics.

- Energy: Primarily includes solar cells and energy storage applications.

- Automotive: For sensors, displays, and protective coatings in vehicles.

- Medical: For devices, diagnostics, and pharmaceutical applications.

- Aerospace & Defense: For durable coatings and specialized components.

- By Deposition Method:

- Chemical Vapor Deposition (CVD): A chemical process used to produce high-quality, high-performance solid materials.

- Atomic Layer Deposition (ALD): A thin film deposition technique that enables the deposition of films with atomic layer control.

- Physical Vapor Deposition (PVD): Includes techniques like sputtering and evaporation, though precursors are less common here compared to CVD/ALD.

Regional Highlights

- Asia Pacific (APAC): The Asia Pacific region stands as the undisputed leader in the Thin Film Precursor market, primarily driven by its robust and expanding electronics manufacturing ecosystem. Countries such as Taiwan, South Korea, China, and Japan are global hubs for semiconductor fabrication, display panel production, and solar cell manufacturing. The immense scale of these industries creates a foundational demand for high volumes of diverse thin film precursors. Furthermore, significant government investments in advanced manufacturing capabilities and a large consumer electronics market contribute to the region's dominance. The presence of major foundries and original equipment manufacturers (OEMs) ensures a continuous demand for advanced precursor materials to support technological innovations and increase production capacities. As these countries continue to push the boundaries of miniaturization and device performance, the need for ultra-high purity and specialized precursors remains paramount, solidifying APAC's pivotal role in the global market.

- North America: North America represents a significant market for Thin Film Precursors, characterized by its strong emphasis on research and development, particularly in advanced semiconductor technologies and next-generation materials. The region is home to leading technology companies, research institutions, and defense contractors that drive innovation in thin film applications. While manufacturing might not be on the same scale as in APAC, North America excels in high-value, niche applications, including advanced computing, aerospace, and medical devices, which demand cutting-edge precursor solutions. The focus here is often on developing novel chemistries and advanced deposition processes that push the performance envelope, contributing significantly to market value through intellectual property and high-end product development.

- Europe: Europe is a key player in the Thin Film Precursor market, driven by its strong automotive, industrial, and renewable energy sectors. The region has a significant focus on sustainable manufacturing practices and environmental regulations, which spurs demand for eco-friendly and less hazardous precursor materials. European countries are also leaders in advanced research in nanotechnology and material science, fostering innovation in precursor development for various applications, including specialized coatings, sensors, and components for electric vehicles. The emphasis on stringent quality standards and performance, coupled with a growing push towards green technologies, shapes the market dynamics within the region.

- Latin America, Middle East, and Africa (MEA): These regions currently hold a smaller share of the Thin Film Precursor market but are poised for gradual growth, driven by increasing industrialization, infrastructure development, and nascent electronics manufacturing. In Latin America, growth is often linked to the expansion of automotive and consumer electronics assembly. The Middle East is witnessing investments in solar energy projects and diversifying its economy away from oil, which could boost demand for precursors in photovoltaics and specialized industrial coatings. Africa, while having limited advanced manufacturing capabilities, offers long-term potential as its industrial base develops. Overall, these regions represent emerging opportunities, although their market maturity and adoption rates for advanced thin film technologies are still evolving.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Thin Film Precursor Market.- Merck KGaA

- Dow Chemical Company

- BASF SE

- Air Liquide S.A.

- Linde plc

- Sumitomo Chemical Co. Ltd.

- DuPont de Nemours, Inc.

- Entegris, Inc.

- Gelest, Inc.

- SAFC Hitech (Merck KGaA)

- CVD Equipment Corporation

- Versum Materials (Entegris, Inc.)

- Tokyo Ohka Kogyo Co. Ltd.

- SHOWA DENKO K.K.

- JSR Corporation

- Cabot Corporation

- Tri Chemical Laboratories Inc.

- Praxair (Linde plc)

- UP Chemical (SK Materials)

- Samsung SDI Co. Ltd.

Frequently Asked Questions

What are Thin Film Precursors?

Thin film precursors are specialized chemical compounds, typically in liquid or gaseous form, used as source materials in various thin film deposition processes. They decompose or react under specific conditions to deposit a thin layer of material onto a substrate, crucial for manufacturing electronic devices, solar cells, and optical coatings.

What industries heavily utilize Thin Film Precursors?

The semiconductor industry is the largest consumer, using precursors for integrated circuits and memory. Other major industries include photovoltaics for solar cells, displays for screens, and optics for specialized coatings. Emerging applications are also found in medical devices and advanced packaging.

How do deposition methods impact precursor choice?

The chosen deposition method, primarily Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD), dictates the required properties of a precursor. ALD, for instance, demands high volatility, thermal stability, and self-limiting reaction characteristics for precise atomic-scale layer control, while CVD can accommodate a broader range of precursor properties.

What are the key drivers for the Thin Film Precursor market growth?

Primary drivers include the continuous growth and technological advancements in the semiconductor industry, increasing global demand for renewable energy (especially thin-film solar cells), and innovation in display technologies. The drive for miniaturization and enhanced performance in electronic components also fuels market expansion.

What are the main challenges faced by the Thin Film Precursor market?

Significant challenges include the high production costs associated with achieving ultra-high purity levels, complexities in the supply chain for specialized raw materials, and the inherent toxicity or hazardous nature of some precursors, which necessitates stringent safety and environmental compliance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted