Anti fog Lidding Film Market

Anti fog Lidding Film Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707218 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

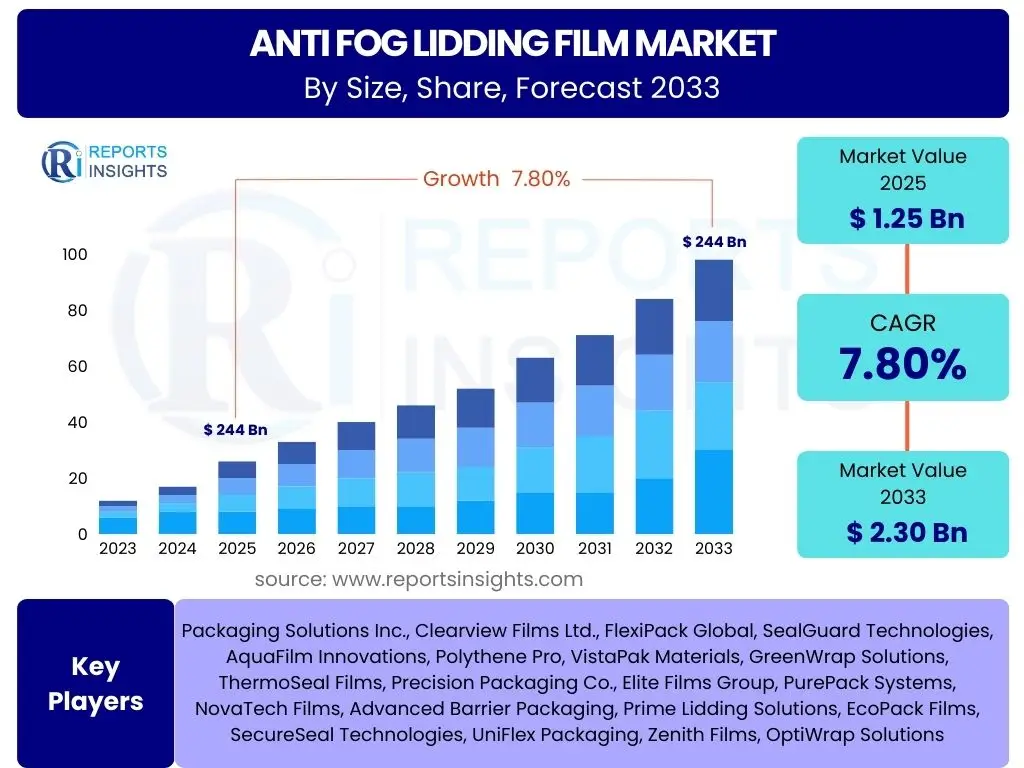

Anti fog Lidding Film Market Size

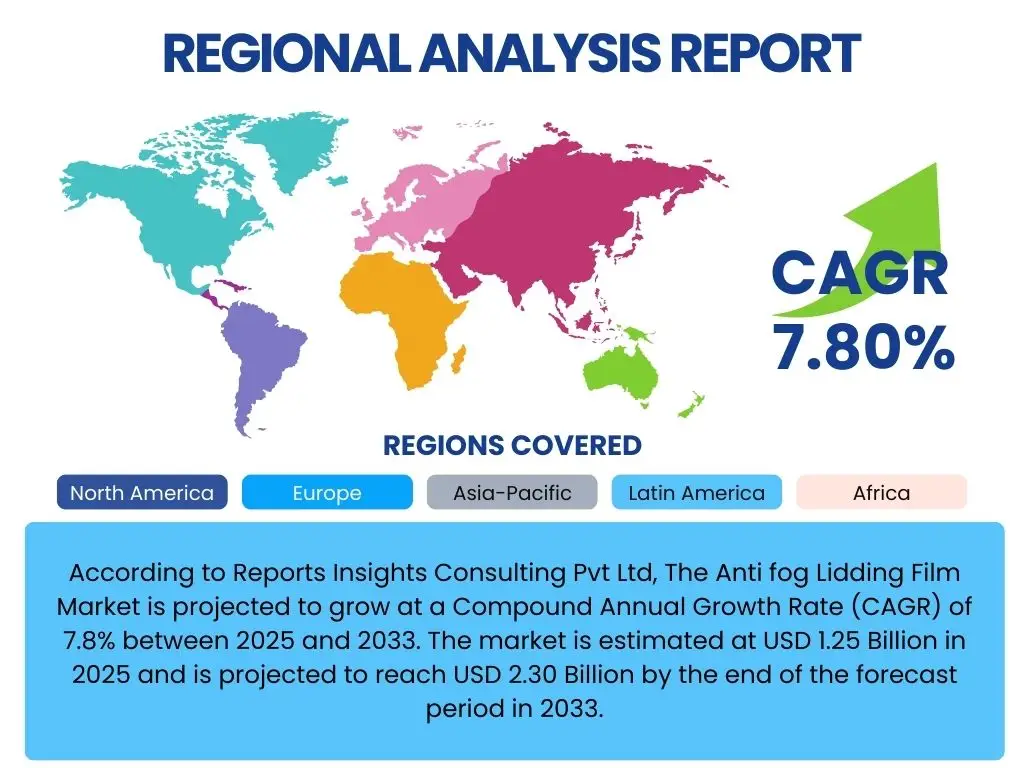

According to Reports Insights Consulting Pvt Ltd, The Anti fog Lidding Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.30 Billion by the end of the forecast period in 2033.

Key Anti fog Lidding Film Market Trends & Insights

The Anti fog Lidding Film market is currently experiencing significant shifts driven by evolving consumer preferences, technological advancements in packaging materials, and a growing emphasis on food safety and waste reduction. Users frequently inquire about the latest innovations in sustainable anti-fog solutions, the impact of e-commerce on packaging demand, and the expanding application areas beyond traditional food items. These inquiries highlight a collective interest in how the industry is adapting to environmental pressures and the logistical demands of modern supply chains, while continuously improving product visibility and shelf life. The market is increasingly characterized by a move towards high-barrier films that offer superior protection and extended freshness, appealing to both manufacturers and end-consumers.

A notable trend is the integration of multi-layer film technologies that enhance anti-fog properties without compromising recyclability or material strength. This development is crucial as manufacturers seek to balance performance with ecological responsibility, addressing consumer and regulatory calls for more sustainable packaging options. Furthermore, the rise of convenience foods and ready-to-eat meals, driven by changing lifestyles and urbanization, is bolstering demand for lidding films that maintain product appeal from production to consumption. The market is also witnessing a surge in customization capabilities, allowing brands to differentiate products through specialized film properties tailored to specific food types and display conditions, thereby optimizing visual merchandising.

- Growing demand for sustainable and recyclable anti-fog films.

- Increased adoption of multi-layer and high-barrier film technologies.

- Expansion of anti-fog films into ready-to-eat and convenience food packaging.

- Technological advancements enhancing clarity and printability for improved visual appeal.

- Shift towards advanced functional additives for enhanced anti-fog performance.

- Integration of smart packaging features for traceability and freshness indicators.

- Rising importance of e-commerce driving demand for robust and visually appealing packaging.

AI Impact Analysis on Anti fog Lidding Film

User queries regarding the impact of Artificial Intelligence (AI) on the Anti fog Lidding Film sector primarily center on how AI can optimize manufacturing processes, enhance quality control, and contribute to the development of smart packaging solutions. There is a strong interest in AI's role in predictive maintenance for production lines, reducing downtime, and ensuring consistent film quality. Users also question AI's potential in supply chain management, from forecasting demand for raw materials to optimizing logistics for finished products, thereby streamlining operations and reducing costs. The expectation is that AI will introduce unprecedented levels of efficiency and precision into the traditionally mechanical aspects of film production.

Furthermore, AI is anticipated to play a crucial role in research and development, particularly in the expedited discovery and formulation of new anti-fog additives and sustainable materials. Machine learning algorithms can analyze vast datasets of chemical properties and performance characteristics, identifying optimal compositions for specific application requirements more rapidly than traditional methods. Beyond the production floor, AI-driven analytics could inform market segmentation strategies, allowing manufacturers to tailor film properties to regional consumer preferences or specific retail environments. This shift signifies a move towards data-driven decision-making across the entire value chain, from raw material sourcing to consumer-facing product presentation.

- AI-driven optimization of manufacturing processes for increased efficiency and reduced waste.

- Enhanced quality control through AI-powered visual inspection systems, ensuring consistent film clarity.

- Predictive maintenance for lidding film production machinery, minimizing downtime.

- AI in supply chain management for demand forecasting and optimized raw material procurement.

- Accelerated R&D for new anti-fog formulations and sustainable materials using machine learning.

- Development of smart packaging solutions with AI-enabled freshness monitoring.

- Data analytics for market trend identification and customized product development.

Key Takeaways Anti fog Lidding Film Market Size & Forecast

Users frequently seek a concise understanding of the primary factors shaping the Anti fog Lidding Film market's trajectory and what this implies for future growth. The central takeaway is the robust and sustained growth projected for the market, driven by an confluence of factors including escalating demand for packaged food, advancements in packaging technology, and increasing consumer awareness regarding food preservation. The forecast indicates a significant expansion in market value, signaling lucrative opportunities for manufacturers and investors. This growth is underpinned by the essential function of anti-fog films in maintaining product visibility and extending shelf life, critical attributes for modern retail and food service sectors.

Another crucial insight is the dynamic interplay between technological innovation and market demand. The industry is not merely reacting to existing needs but proactively developing solutions that address emerging challenges, such as the need for more environmentally friendly materials and more efficient production methods. The projected growth also highlights the resilience of the packaged food industry, where anti-fog lidding films are an indispensable component for maintaining product quality and consumer appeal. Understanding these core drivers and the market's strong upward trend is vital for strategic planning and investment in this sector, pointing towards a future where high-performance, sustainable packaging solutions will dominate.

- The Anti fog Lidding Film market is poised for significant growth, projected to reach USD 2.30 Billion by 2033, indicating robust expansion.

- Sustainable packaging solutions and high-barrier films are key drivers of market innovation and adoption.

- The increasing consumption of convenience foods and fresh produce directly fuels demand for anti-fog lidding films.

- Technological advancements are enhancing film performance, clarity, and environmental profile.

- Market expansion is global, with particular opportunities identified in emerging economies and developed markets prioritizing food waste reduction.

Anti fog Lidding Film Market Drivers Analysis

The Anti fog Lidding Film market is significantly propelled by several key drivers that reinforce its growth trajectory. A primary driver is the accelerating consumer demand for packaged and convenience foods, spurred by busy lifestyles and urbanization. As consumers increasingly opt for ready-to-eat meals, pre-cut fruits, and pre-packaged meats, the need for packaging that maintains product freshness and visual appeal becomes paramount. Anti-fog films play a critical role here by preventing condensation inside packaging, which would otherwise obscure the product and diminish its perceived quality. This direct correlation between changing dietary habits and packaging requirements ensures a steady and rising demand for anti-fog solutions.

Another substantial driver is the growing emphasis on reducing food waste across the supply chain, from producers to consumers. Anti-fog lidding films contribute to this goal by extending the shelf life of perishable goods, thus minimizing spoilage and economic losses. This benefit aligns with global sustainability initiatives and consumer awareness programs advocating for responsible consumption. Furthermore, advancements in packaging technology, including the development of multi-layer films and enhanced barrier properties, are making anti-fog films more effective and versatile. These innovations enable broader applications and improve performance under various storage and transportation conditions, further solidifying their market position. The stringent food safety regulations in various regions also compel manufacturers to use packaging that ensures product integrity, with anti-fog properties being an integral part of maintaining quality inspections and consumer trust.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for packaged and convenience foods | +2.5% | Global, particularly Asia Pacific & North America | Short to Medium Term (2025-2029) |

| Increasing focus on reducing food waste and extending shelf life | +2.0% | Europe, North America, developing economies | Medium to Long Term (2027-2033) |

| Technological advancements in film materials and barrier properties | +1.8% | Global, particularly developed markets | Medium Term (2026-2030) |

| Expansion of organized retail and e-commerce food delivery | +1.5% | Asia Pacific, Latin America, Middle East | Short to Medium Term (2025-2029) |

| Rising awareness of food safety and hygiene among consumers | +1.0% | Global | Long Term (2028-2033) |

Anti fog Lidding Film Market Restraints Analysis

Despite the robust growth prospects, the Anti fog Lidding Film market faces certain restraints that could impede its expansion. One significant challenge is the volatility in raw material prices, primarily polymers like polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET). Fluctuations in crude oil prices, which are a key determinant for polymer costs, can directly impact the manufacturing expenses of anti-fog films, leading to increased production costs for film manufacturers. This volatility can squeeze profit margins and make it difficult for companies to offer competitive pricing, potentially slowing down market adoption, especially in price-sensitive regions or applications.

Another substantial restraint stems from growing environmental concerns regarding plastic waste and the push for sustainable packaging. While efforts are being made to develop recyclable and biodegradable anti-fog films, the majority of current films are still petroleum-based and contribute to plastic pollution. Regulatory pressures and consumer preferences are increasingly shifting towards eco-friendly alternatives, which could divert demand away from conventional anti-fog films if more sustainable options are not readily available or cost-competitive. Furthermore, the availability of alternative packaging solutions, such as modified atmosphere packaging (MAP) without lidding films or other packaging formats, could present competition. These alternatives, while serving similar functions, may not always offer the same visual appeal or cost-effectiveness, but their continuous development poses a potential threat to the market share of lidding films.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in raw material prices (polymers) | -1.2% | Global, particularly regions dependent on imported raw materials | Short to Medium Term (2025-2029) |

| Environmental concerns and stringent regulations on plastic use | -1.0% | Europe, North America, select Asia Pacific countries | Medium to Long Term (2027-2033) |

| Availability of alternative packaging solutions | -0.8% | Global | Medium Term (2026-2030) |

| High initial investment for specialized anti-fog film manufacturing | -0.5% | Developing economies | Short to Medium Term (2025-2029) |

Anti fog Lidding Film Market Opportunities Analysis

The Anti fog Lidding Film market is ripe with opportunities that can significantly accelerate its growth. A paramount opportunity lies in the continuous innovation and adoption of sustainable and biodegradable film materials. As consumer awareness about environmental impact rises and regulatory frameworks become more stringent, there is an escalating demand for packaging solutions that minimize ecological footprints. Developing anti-fog films from plant-based polymers, recycled content, or compostable materials presents a vast untapped market, allowing manufacturers to cater to eco-conscious brands and consumers, thereby opening new revenue streams and enhancing brand reputation. This shift towards circular economy principles offers a substantial competitive advantage.

Furthermore, the expansion into emerging markets, particularly in Asia Pacific, Latin America, and the Middle East, represents a significant growth avenue. These regions are experiencing rapid urbanization, increasing disposable incomes, and the modernization of retail infrastructure, leading to a surge in demand for packaged food and convenience products. Many of these markets are still in nascent stages of adopting advanced packaging solutions, offering ample room for anti-fog film manufacturers to establish a strong presence. The application diversification beyond traditional food sectors, such as in the medical and pharmaceutical industries for sterile packaging or in electronics for moisture protection, also presents lucrative niche opportunities. Tailoring anti-fog properties for these specific non-food applications can unlock new market segments, diversifying revenue streams and reducing reliance on the food sector alone.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and adoption of sustainable and biodegradable films | +2.8% | Global, particularly Europe & North America | Medium to Long Term (2027-2033) |

| Expansion into emerging economies with growing middle-class populations | +2.3% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium Term (2025-2030) |

| Application diversification into non-food sectors (e.g., medical, electronics) | +1.9% | Global, specialized markets | Medium Term (2026-2031) |

| Integration of smart packaging technologies (e.g., QR codes, freshness indicators) | +1.5% | Developed markets | Long Term (2028-2033) |

| Strategic collaborations and partnerships for product innovation | +1.0% | Global | Short to Medium Term (2025-2029) |

Anti fog Lidding Film Market Challenges Impact Analysis

The Anti fog Lidding Film market, while promising, contends with several notable challenges that require strategic navigation. One significant hurdle is the increasing complexity of regulatory compliance across different regions. As food safety and environmental standards evolve, manufacturers must continuously adapt their production processes and material compositions to meet diverse and often stringent requirements. Non-compliance can lead to hefty penalties, product recalls, and reputational damage, making it a critical area of concern. The fragmented nature of these regulations across various countries and trade blocs adds a layer of complexity for global players, demanding significant investment in compliance monitoring and certification.

Another challenge is intense market competition, leading to pricing pressures and a need for continuous innovation. The anti-fog lidding film market features numerous players, ranging from large multinational corporations to specialized regional manufacturers. This competitive landscape often results in price wars and necessitates constant research and development to offer superior products, whether through enhanced anti-fog performance, improved barrier properties, or greater sustainability. Companies must differentiate themselves through quality, innovation, and customer service to maintain market share. Furthermore, the technical complexity involved in developing highly effective and durable anti-fog coatings, particularly for diverse applications and environmental conditions, represents an ongoing challenge. Achieving consistent anti-fog properties while ensuring seal integrity, printability, and overall cost-effectiveness requires significant R&D investment and expertise.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent and evolving regulatory landscape | -1.5% | Europe, North America, regulated markets globally | Medium to Long Term (2027-2033) |

| Intense market competition and pricing pressures | -1.3% | Global | Short to Medium Term (2025-2029) |

| Technical complexities in achieving optimal anti-fog performance | -1.0% | Global | Short to Medium Term (2025-2030) |

| Supply chain disruptions and logistics complexities | -0.7% | Global, particularly impacting cross-border trade | Short Term (2025-2027) |

Anti fog Lidding Film Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Anti fog Lidding Film Market, offering an in-depth analysis of its current landscape, historical performance, and future projections. It covers market size estimations, growth drivers, restraints, opportunities, and challenges, providing a holistic view for stakeholders. The report meticulously segments the market by various criteria, offering granular insights into specific product types, applications, and regional market trends. It also profiles key industry players, offering strategic insights into their competitive positioning and recent developments, making it an invaluable resource for strategic decision-making and market intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.30 Billion |

| Growth Rate | 7.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Packaging Solutions Inc., Clearview Films Ltd., FlexiPack Global, SealGuard Technologies, AquaFilm Innovations, Polythene Pro, VistaPak Materials, GreenWrap Solutions, ThermoSeal Films, Precision Packaging Co., Elite Films Group, PurePack Systems, NovaTech Films, Advanced Barrier Packaging, Prime Lidding Solutions, EcoPack Films, SecureSeal Technologies, UniFlex Packaging, Zenith Films, OptiWrap Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Anti fog Lidding Film market is meticulously segmented to provide a detailed understanding of its diverse components and sub-markets, enabling stakeholders to pinpoint specific areas of growth and opportunity. The primary segmentation categories encompass material type, application, and film thickness, each revealing distinct market dynamics and consumer preferences. Understanding these segments is crucial for manufacturers to tailor their product offerings, for distributors to optimize their supply chains, and for investors to identify high-potential niches within the broader market. This granular analysis facilitates precise market targeting and strategic resource allocation.

By dissecting the market along these dimensions, the report illustrates how different material compositions such as PE, PET, and PP cater to varying packaging requirements and sustainability goals. For instance, PET films are often preferred for their clarity and rigidity, while PE films offer excellent sealing properties and flexibility. The application-based segmentation highlights the dominant role of fresh produce and ready meals in driving demand, but also sheds light on emerging uses in dairy, bakery, and even non-food sectors. Thickness-based segmentation informs about the performance requirements and cost implications, with thicker films generally offering enhanced barrier properties for extended shelf life. This multi-faceted segmentation provides a comprehensive blueprint of the market's structure and potential areas for innovation and expansion.

- By Material:

- Polyethylene (PE)

- Polyethylene Terephthalate (PET)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Others (e.g., EVOH, PLA)

- By Application:

- Fresh Produce

- Meat and Poultry

- Ready Meals

- Bakery and Confectionery

- Dairy and Desserts

- Other Food Applications (e.g., seafood, frozen foods)

- Non-Food Applications (e.g., Medical, Industrial)

- By Thickness:

- Below 50 Microns

- 50-100 Microns

- Above 100 Microns

Regional Highlights

- North America: This region demonstrates a mature market with a high adoption rate of anti-fog lidding films, driven by established organized retail chains, high consumer demand for convenience foods, and stringent food safety regulations. Innovation in sustainable packaging solutions is a key focus.

- Europe: Characterized by strong environmental consciousness and strict regulations concerning plastic use, Europe is a leader in the development and adoption of recyclable and biodegradable anti-fog films. The region's emphasis on reducing food waste further propels market growth.

- Asia Pacific (APAC): Expected to be the fastest-growing region, APAC benefits from rapid urbanization, increasing disposable incomes, and the booming e-commerce sector. Emerging economies within APAC are witnessing significant expansion in organized retail and packaged food consumption, offering immense growth opportunities.

- Latin America: This region is experiencing steady growth, fueled by evolving consumer lifestyles, increasing demand for packaged and processed foods, and the expansion of modern retail formats. Localized production and distribution networks are becoming increasingly important.

- Middle East and Africa (MEA): Growth in MEA is attributed to rising population, economic diversification, and increasing Westernization of dietary habits. Investments in cold chain infrastructure and modern retail outlets are contributing to the adoption of advanced packaging solutions like anti-fog lidding films.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Anti fog Lidding Film Market.- Packaging Solutions Inc.

- Clearview Films Ltd.

- FlexiPack Global

- SealGuard Technologies

- AquaFilm Innovations

- Polythene Pro

- VistaPak Materials

- GreenWrap Solutions

- ThermoSeal Films

- Precision Packaging Co.

- Elite Films Group

- PurePack Systems

- NovaTech Films

- Advanced Barrier Packaging

- Prime Lidding Solutions

- EcoPack Films

- SecureSeal Technologies

- UniFlex Packaging

- Zenith Films

- OptiWrap Solutions

Frequently Asked Questions

Analyze common user questions about the Anti fog Lidding Film market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an anti-fog lidding film?

An anti-fog lidding film is a specialized plastic film used to seal food trays and containers. It contains additives that prevent condensation (fogging) from forming on the inside surface of the film when there is a temperature difference, ensuring clear visibility of the packaged product.

Why is anti-fog lidding film important for packaged food?

Anti-fog lidding film is crucial for packaged food because it maintains product visibility, enhancing consumer appeal and enabling clearer inspection. It also contributes to extending the shelf life of perishable goods by preventing moisture accumulation, which can lead to spoilage and bacterial growth.

What are the primary materials used in anti-fog lidding films?

The primary materials include Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), and Polyvinyl Chloride (PVC). Advanced films may incorporate multi-layer structures and specialized anti-fog coatings for enhanced performance.

How is the anti-fog lidding film market growing?

The market is experiencing significant growth, projected to reach USD 2.30 Billion by 2033 with a CAGR of 7.8%. This growth is driven by increasing demand for packaged convenience foods, a focus on reducing food waste, and advancements in sustainable packaging technologies.

What sustainable options are available for anti-fog lidding films?

Sustainable options include films made from recycled content, bio-based polymers (like PLA), or compostable materials. Manufacturers are increasingly investing in research and development to offer anti-fog films that are both high-performing and environmentally friendly.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted