Thin Film Material Market

Thin Film Material Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707025 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Thin Film Material Market Size

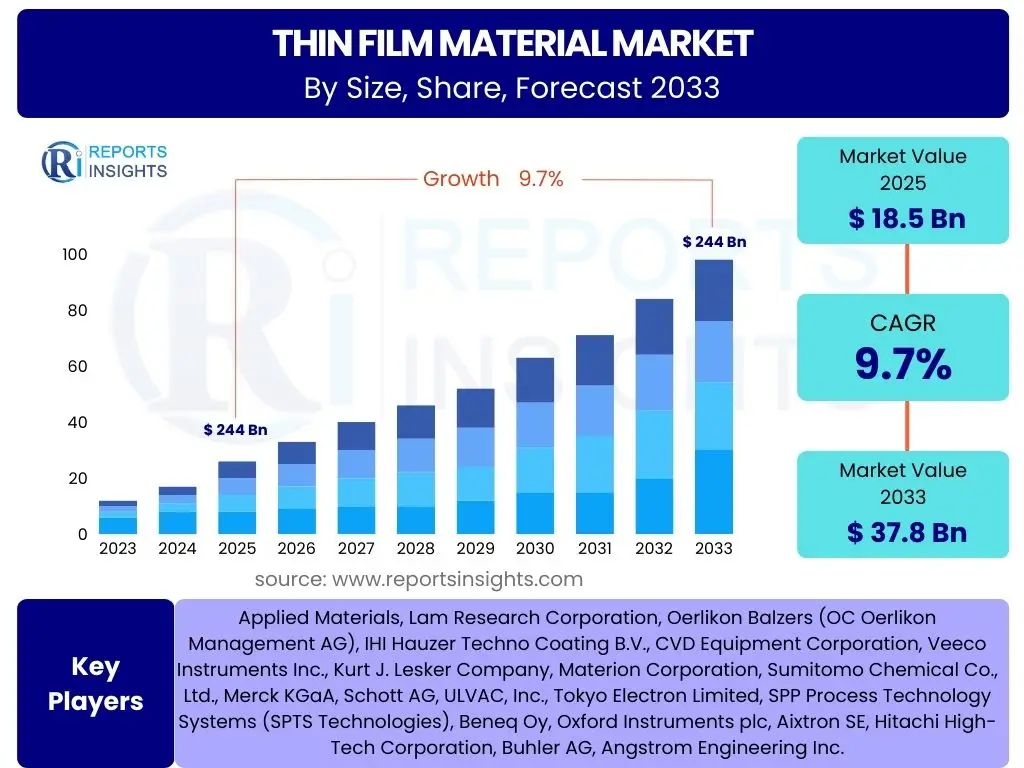

According to Reports Insights Consulting Pvt Ltd, The Thin Film Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.7% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 37.8 Billion by the end of the forecast period in 2033.

Key Thin Film Material Market Trends & Insights

The Thin Film Material market is experiencing robust growth driven by advancements across various high-tech sectors. Key trends include the increasing demand for miniaturized electronic components, the rapid expansion of renewable energy solutions, and the continuous innovation in display technologies. These factors are compelling industries to adopt thin film solutions for their superior performance characteristics, such as enhanced efficiency, durability, and reduced material consumption, making them indispensable for next-generation products.

Furthermore, the market is witnessing a surge in research and development activities focused on novel thin film materials and deposition techniques. This includes the exploration of two-dimensional materials, flexible substrates, and advanced atomic layer deposition (ALD) methods, which promise breakthroughs in areas like flexible electronics, advanced sensors, and high-efficiency solar cells. The drive towards sustainable and cost-effective manufacturing processes is also a significant trend, promoting the development of eco-friendly thin film solutions.

- Miniaturization in electronics and semiconductors

- Rapid adoption of renewable energy technologies, particularly solar photovoltaics

- Advancements in display technologies (OLED, QLED)

- Growing demand for flexible and wearable electronic devices

- Emergence of advanced packaging solutions in semiconductors

- Increasing application in medical devices and biocompatible coatings

- Focus on energy-efficient and eco-friendly manufacturing processes

AI Impact Analysis on Thin Film Material

Artificial Intelligence (AI) is set to revolutionize the Thin Film Material market by optimizing various stages of the material lifecycle, from discovery and design to manufacturing and quality control. Users frequently inquire about how AI can accelerate material development, improve process efficiency, and enhance the performance of thin films. AI-driven simulations and data analytics can predict material properties with high accuracy, significantly reducing the time and cost associated with experimental trials, thereby enabling faster innovation cycles for novel thin film compositions and structures.

In manufacturing, AI algorithms are being deployed for real-time process monitoring, predictive maintenance of deposition equipment, and automated defect detection. This allows for unparalleled precision and consistency in film growth, leading to higher yields and reduced waste. Furthermore, AI can optimize complex deposition parameters to achieve desired film characteristics, pushing the boundaries of what is possible with traditional methods. The integration of AI also facilitates the creation of digital twins for thin film systems, offering a comprehensive virtual representation for continuous optimization and performance prediction throughout the production chain.

- Accelerated material discovery and design through AI-driven simulations

- Optimization of thin film deposition processes (e.g., PVD, CVD, ALD)

- Enhanced quality control and real-time defect detection

- Predictive maintenance for thin film manufacturing equipment

- Improved material property prediction and characterization

- Automation of complex experimental procedures and data analysis

- Development of self-correcting feedback loops in production lines

Key Takeaways Thin Film Material Market Size & Forecast

The Thin Film Material market is poised for substantial growth, largely driven by its pivotal role in several high-growth industries. The increasing global demand for sophisticated electronic devices, the aggressive push for renewable energy sources, and continuous advancements in display technologies are primary catalysts. These factors underscore the critical importance of thin films in enabling next-generation products that are more efficient, compact, and powerful, solidifying the market's trajectory towards significant expansion.

A key takeaway from the market forecast is the sustained innovation within the thin film sector, focusing on novel materials and advanced deposition techniques. This includes the development of flexible thin films for wearable electronics and biocompatible coatings for medical implants, expanding the application scope beyond traditional domains. The forecast also highlights the growing emphasis on sustainability and cost-effectiveness in thin film production, indicating a shift towards more environmentally friendly and economically viable manufacturing processes, which will further fuel market penetration across diverse sectors.

- Significant growth driven by electronics, solar, and display industries

- Continued innovation in material science and deposition techniques

- Increasing adoption in emerging applications like flexible electronics and IoT

- Emphasis on high-performance, durable, and energy-efficient solutions

- Global expansion, with Asia Pacific leading in manufacturing and adoption

- Integration of advanced technologies like AI for process optimization

Thin Film Material Market Drivers Analysis

The expansion of the Thin Film Material market is significantly propelled by the pervasive digitalization across industries and the escalating demand for high-performance, miniaturized components. The semiconductor industry, a foundational consumer of thin films, continues its relentless pursuit of smaller, more powerful chips, driving the need for advanced thin film deposition and etching techniques. Similarly, the global imperative for clean energy solutions has spurred massive investments in solar photovoltaic technologies, where thin film materials are crucial for efficient energy conversion. These macroeconomic trends, coupled with ongoing technological advancements, create a robust environment for market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Semiconductor Industry | +2.5% | Global, particularly Asia Pacific (Taiwan, South Korea, China), North America | 2025-2033 (Long-term) |

| Growth in Solar Photovoltaic (PV) Market | +2.0% | Global, particularly Asia Pacific (China, India), Europe, North America | 2025-2033 (Long-term) |

| Advancements in Display Technologies (OLED, QLED) | +1.5% | Asia Pacific (South Korea, Japan, China), North America | 2025-2030 (Mid-term) |

| Rising Adoption in Medical and Healthcare Devices | +1.0% | North America, Europe, Asia Pacific | 2026-2033 (Long-term) |

| Emergence of Flexible and Wearable Electronics | +0.8% | Asia Pacific, North America, Europe | 2027-2033 (Mid to Long-term) |

Thin Film Material Market Restraints Analysis

Despite significant growth prospects, the Thin Film Material market faces several restraints that could impede its expansion. The high capital expenditure required for advanced thin film deposition equipment and the intricate, often proprietary, manufacturing processes pose considerable barriers to entry for new players. Furthermore, the reliance on specific rare earth elements or specialty chemicals for certain advanced thin films introduces supply chain vulnerabilities and cost volatility, which can impact profitability and market stability. These factors necessitate substantial upfront investment and expertise, limiting broader market participation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Production Costs | -1.2% | Global | 2025-2033 (Long-term) |

| Complex Manufacturing Processes and Technical Challenges | -1.0% | Global | 2025-2030 (Mid-term) |

| Volatility in Raw Material Prices and Supply Chain Disruptions | -0.8% | Global, particularly regions dependent on specific mineral imports | 2025-2028 (Short to Mid-term) |

| Environmental Regulations and Disposal Concerns | -0.5% | Europe, North America, parts of Asia Pacific | 2026-2033 (Long-term) |

Thin Film Material Market Opportunities Analysis

The Thin Film Material market is rich with opportunities stemming from emerging technological frontiers and the ongoing quest for superior material performance. The burgeoning fields of quantum computing and advanced energy storage systems present novel applications for thin films, requiring precise control over material properties at atomic scales. Moreover, the increasing adoption of IoT devices and smart infrastructure creates a demand for integrated, flexible, and energy-efficient sensors, where thin film technologies offer distinct advantages. These new avenues are expected to open significant revenue streams and drive further innovation within the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Materials (e.g., 2D materials, Perovskites) | +1.8% | Global, R&D intensive regions like North America, Europe, Japan | 2028-2033 (Long-term) |

| Expansion into New Applications (e.g., Quantum Computing, Smart Sensors) | +1.5% | Global | 2027-2033 (Long-term) |

| Growing Demand for Anti-corrosion and Protective Coatings | +1.0% | Global, particularly industrial and automotive sectors | 2025-2030 (Mid-term) |

| Increasing Investment in R&D for Advanced Deposition Techniques | +0.7% | Global, academic and corporate research hubs | 2025-2033 (Long-term) |

Thin Film Material Market Challenges Impact Analysis

The Thin Film Material market faces several formidable challenges that require strategic solutions for sustained growth. One major hurdle is the need for highly specialized technical expertise and skilled labor to operate and maintain advanced deposition systems, which can be a bottleneck for expansion. Furthermore, the inherent complexity of integrating thin films into diverse product designs, along with ensuring long-term reliability and performance under various environmental conditions, presents significant engineering challenges. These factors, coupled with intense competition and the constant pressure for innovation, demand continuous investment in research and development to stay competitive and address evolving market needs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Need for Highly Skilled Workforce and Technical Expertise | -0.9% | Global | 2025-2033 (Long-term) |

| Integration Complexities with Existing Manufacturing Processes | -0.7% | Global | 2025-2030 (Mid-term) |

| Ensuring Long-term Stability and Durability of Thin Films | -0.6% | Global, particularly in harsh environment applications | 2025-2033 (Long-term) |

| Intense Competition and Pricing Pressures | -0.4% | Global | 2025-2028 (Short to Mid-term) |

Thin Film Material Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Thin Film Material market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges. It covers an extensive period, from historical trends to future projections, segmented by material type, deposition method, application, end-use industry, and geographical regions. The report aims to equip stakeholders with critical data for strategic decision-making in this evolving technological landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 37.8 Billion |

| Growth Rate | 9.7% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials, Lam Research Corporation, Oerlikon Balzers (OC Oerlikon Management AG), IHI Hauzer Techno Coating B.V., CVD Equipment Corporation, Veeco Instruments Inc., Kurt J. Lesker Company, Materion Corporation, Sumitomo Chemical Co., Ltd., Merck KGaA, Schott AG, ULVAC, Inc., Tokyo Electron Limited, SPP Process Technology Systems (SPTS Technologies), Beneq Oy, Oxford Instruments plc, Aixtron SE, Hitachi High-Tech Corporation, Buhler AG, Angstrom Engineering Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Thin Film Material market is comprehensively segmented to provide a granular view of its diverse landscape and intricate dynamics. This segmentation facilitates a deeper understanding of specific market drivers, regional preferences, and technological adoption patterns across various industries. By categorizing the market based on material type, deposition method, application, and end-use industry, the analysis highlights key areas of growth, emerging opportunities, and competitive intensity within each segment, allowing stakeholders to identify niche markets and tailor their strategies effectively.

The material type segmentation reveals the dominance of metals, oxides, and nitrides due to their widespread use in electronics, optics, and protective coatings, while advanced polymers and ceramics gain traction in specialized applications. Deposition methods, such as Physical Vapor Deposition (PVD) and Chemical Vapor Deposition (CVD), represent foundational technologies, continuously evolving with new variants like Atomic Layer Deposition (ALD) for ultra-precise layering. Application-wise, the market is broadly driven by optical, protective, and conductive coatings, with increasing uptake in energy devices and sensors. Finally, end-use industry segmentation underscores the critical reliance of the electronics, solar energy, and display sectors on thin film materials, alongside growing demand from automotive, medical, and aerospace industries.

- By Material Type: Metals, Oxides, Nitrides, Polymers, Ceramics, Other Materials

- By Deposition Method: Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD), Atomic Layer Deposition (ALD), Electrochemical Deposition, Spin Coating, Other Methods

- By Application: Optical Coatings, Protective Coatings, Conductive Coatings, Dielectric Coatings, Sensors, Energy Devices (Solar Cells, Batteries), Biomedical Coatings, Others

- By End-Use Industry: Electronics & Semiconductors, Automotive, Solar Energy, Optics & Displays, Medical & Healthcare, Aerospace & Defense, Industrial & Manufacturing, Others

Regional Highlights

Regional analysis of the Thin Film Material market reveals distinct growth patterns and dominant application areas influenced by local industrial landscapes and technological advancements. Each region contributes uniquely to the global market, driven by specific economic factors, government initiatives, and consumer demands, shaping the adoption and innovation of thin film technologies. Understanding these regional nuances is crucial for companies planning market entry, expansion, or strategic partnerships.

- Asia Pacific (APAC): Dominates the market due to its robust manufacturing base for electronics, semiconductors, and solar panels. Countries like China, South Korea, Japan, and Taiwan are at the forefront of thin film production and consumption, driven by high demand for consumer electronics and significant investments in renewable energy infrastructure. The region also benefits from a large pool of skilled labor and increasing R&D activities.

- North America: Characterized by strong R&D capabilities, significant investments in advanced technologies, and a growing demand from the aerospace, defense, and medical sectors. The presence of leading semiconductor companies and a focus on high-performance computing further fuels the adoption of sophisticated thin film materials. Innovation in areas like quantum computing and advanced sensors also plays a key role.

- Europe: A mature market with strong emphasis on automotive, industrial, and renewable energy applications. Countries such as Germany, France, and the UK are key players, driven by stringent environmental regulations promoting solar energy and a focus on advanced manufacturing. Research initiatives for novel materials and sustainable production methods are prominent in this region.

- Latin America: An emerging market for thin film materials, with increasing industrialization and growing adoption of renewable energy technologies. Brazil and Mexico are leading the way, fueled by investments in electronics manufacturing and infrastructure development, though the market size remains comparatively smaller than other regions.

- Middle East and Africa (MEA): Shows promising growth, particularly in the solar energy sector, driven by abundant sunlight and government initiatives to diversify energy sources. Investments in smart city projects and industrialization also contribute to the demand for thin film technologies, especially for protective coatings and architectural applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Thin Film Material Market.- Applied Materials

- Lam Research Corporation

- Oerlikon Balzers (OC Oerlikon Management AG)

- IHI Hauzer Techno Coating B.V.

- CVD Equipment Corporation

- Veeco Instruments Inc.

- Kurt J. Lesker Company

- Materion Corporation

- Sumitomo Chemical Co., Ltd.

- Merck KGaA

- Schott AG

- ULVAC, Inc.

- Tokyo Electron Limited

- SPP Process Technology Systems (SPTS Technologies)

- Beneq Oy

- Oxford Instruments plc

- Aixtron SE

- Hitachi High-Tech Corporation

- Buhler AG

- Angstrom Engineering Inc.

Frequently Asked Questions

Analyze common user questions about the Thin Film Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Thin Film Materials used for?

Thin film materials are utilized across a vast array of high-tech applications, primarily for their unique electrical, optical, mechanical, and chemical properties when deposited as thin layers. Key applications include semiconductors (for transistors and interconnects), solar cells (for light absorption and conversion), display technologies (for optical clarity and conductivity in screens), optical coatings (for anti-reflection, filters), protective coatings (for corrosion and wear resistance), sensors, and advanced medical devices, enabling enhanced performance, miniaturization, and new functionalities.

How is the Thin Film Material market growing?

The Thin Film Material market is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of 9.7% between 2025 and 2033. This expansion is predominantly driven by increasing demand from the electronics and semiconductor industries, the accelerating adoption of solar energy technologies, and continuous advancements in display and optical technologies. The market's growth is further supported by innovations in material science and deposition techniques, expanding its utility into emerging fields such as flexible electronics and advanced sensors.

What are the primary types of Thin Film Materials?

The Thin Film Material market encompasses several primary types, classified based on their chemical composition and resulting properties. These include metals (e.g., aluminum, copper, silver, gold) used for conductive layers and interconnects; oxides (e.g., ITO, ZnO, TiO2) for transparent conductive coatings and dielectrics; nitrides (e.g., TiN, AlN, GaN) for hard coatings and semiconductor applications; polymers (e.g., Parylene, polyimide) for flexible electronics and biocompatible layers; and ceramics, used for specialized protective and dielectric applications. Each type offers distinct advantages tailored to specific functional requirements.

What are the major challenges in the Thin Film Material market?

The Thin Film Material market faces several significant challenges, including the high capital expenditure required for advanced deposition equipment and complex manufacturing processes, which can deter new entrants. Other challenges involve ensuring the long-term stability and durability of thin films, managing volatile raw material prices and potential supply chain disruptions, and overcoming the need for highly skilled labor and specialized technical expertise. These factors necessitate continuous innovation and substantial R&D investment to maintain competitiveness and meet evolving industry demands.

Who are the leading companies in the Thin Film Material market?

The Thin Film Material market is characterized by a mix of established global leaders and specialized innovators. Key players include companies providing deposition equipment and those focused on material manufacturing. Prominent equipment providers like Applied Materials, Lam Research Corporation, Oerlikon Balzers, Veeco Instruments, and ULVAC, Inc., are crucial. Material suppliers such as Materion Corporation, Sumitomo Chemical Co., Ltd., and Merck KGaA also hold significant market positions, alongside specialized firms like Beneq Oy and Aixtron SE, who contribute to advanced deposition technologies and materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted