Steel Alloy Aluminium Alloy Aerospace Material Market

Steel Alloy Aluminium Alloy Aerospace Material Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707789 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Steel Alloy Aluminium Alloy Aerospace Material Market Size

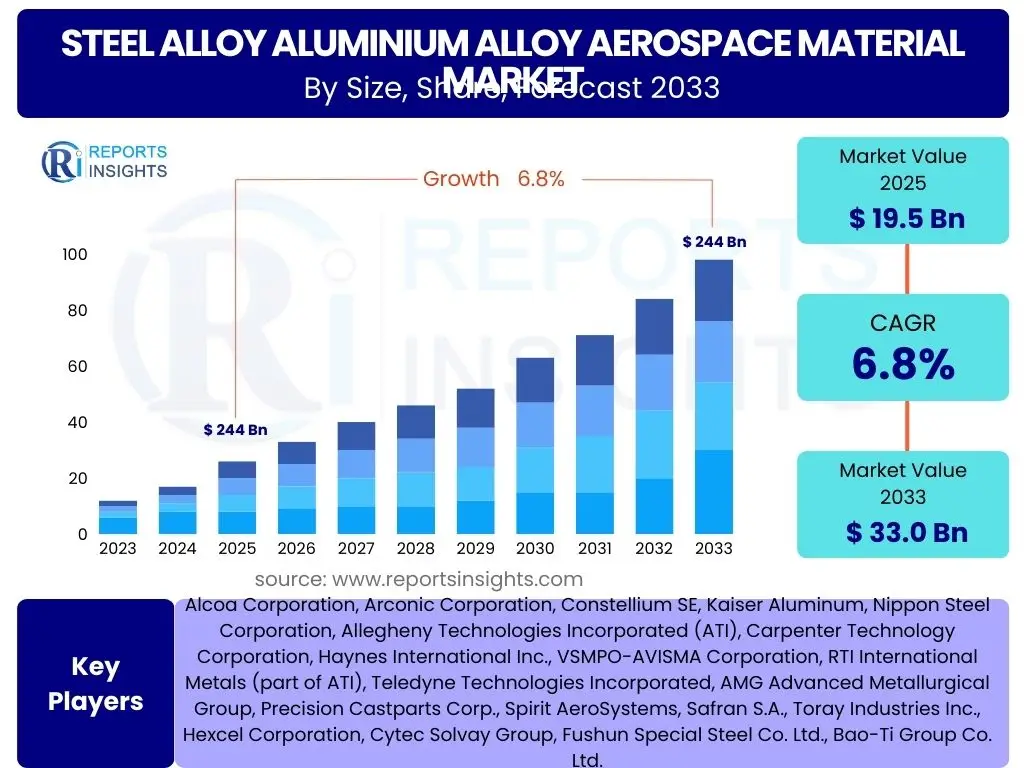

According to Reports Insights Consulting Pvt Ltd, The Steel Alloy Aluminium Alloy Aerospace Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 19.5 Billion in 2025 and is projected to reach USD 33.0 Billion by the end of the forecast period in 2033.

Key Steel Alloy Aluminium Alloy Aerospace Material Market Trends & Insights

The Steel Alloy Aluminium Alloy Aerospace Material market is significantly influenced by a paradigm shift towards advanced, lightweight, and high-performance materials. Manufacturers are increasingly focused on reducing aircraft weight to improve fuel efficiency and minimize carbon emissions, directly impacting material selection. This trend is driving demand for advanced aluminum-lithium alloys, high-strength steels, and next-generation composite materials that offer superior strength-to-weight ratios and enhanced fatigue resistance.

Furthermore, the market is witnessing robust innovation in manufacturing processes, particularly in additive manufacturing (3D printing) of complex aerospace components. This technology enables the production of parts with intricate geometries, reduced material waste, and shorter lead times, revolutionizing supply chains and material design possibilities. Concurrently, increasing global defense expenditures and the continuous development of new commercial aircraft programs are sustaining the demand for reliable and durable aerospace-grade materials, pushing the boundaries of material science and engineering.

- Lightweighting initiatives for enhanced fuel efficiency and reduced emissions.

- Increased adoption of advanced manufacturing techniques, including additive manufacturing.

- Growing demand for high-strength, corrosion-resistant, and temperature-tolerant alloys.

- Emphasis on sustainable material sourcing and recycling within the aerospace industry.

- Integration of smart materials and sensors for structural health monitoring.

- Development of new aircraft platforms driving demand for innovative material solutions.

AI Impact Analysis on Steel Alloy Aluminium Alloy Aerospace Material

Artificial intelligence is poised to revolutionize the Steel Alloy Aluminium Alloy Aerospace Material sector by fundamentally altering how materials are discovered, designed, and manufactured. Users are keenly interested in AI's capability to accelerate the material R&D cycle, allowing for faster identification of optimal alloy compositions and microstructures with desired properties. AI-driven simulations and machine learning algorithms can predict material performance under various conditions, significantly reducing the need for extensive physical testing and thus compressing development timelines and costs.

Beyond material design, AI's influence extends into the manufacturing and quality control phases. It enables predictive maintenance for production machinery, optimizes parameters for processes like forging, casting, and additive manufacturing, and enhances anomaly detection in finished components through advanced imaging and data analysis. The integration of AI tools promises to improve consistency, reduce defects, and boost overall efficiency across the entire value chain of aerospace material production, addressing user concerns about quality, cost-effectiveness, and supply chain resilience.

- Accelerated material discovery and design through AI-driven simulations and data analysis.

- Optimization of manufacturing processes (e.g., forging, heat treatment, additive manufacturing) for improved material properties and reduced waste.

- Enhanced quality control and defect detection using AI-powered visual inspection and predictive analytics.

- Predictive maintenance for production equipment, minimizing downtime and increasing operational efficiency.

- Supply chain optimization and risk management through AI-driven demand forecasting and logistics.

- Development of intelligent materials with self-healing or adaptive properties facilitated by AI.

Key Takeaways Steel Alloy Aluminium Alloy Aerospace Material Market Size & Forecast

The Steel Alloy Aluminium Alloy Aerospace Material market is poised for substantial growth through 2033, driven by the increasing global demand for new aircraft, advancements in material science, and stringent performance and environmental regulations. Stakeholders should recognize the market's resilience, underpinned by continuous innovation in material properties and manufacturing techniques, ensuring its critical role in the future of aerospace. The forecast indicates a steady expansion, making it a pivotal sector for investment and technological development, particularly in lightweight and high-strength solutions.

A key insight from the market forecast is the strong emphasis on sustainability and efficiency, which are becoming non-negotiable aspects of material development. This translates into a competitive landscape where companies investing in eco-friendly production methods, recyclability, and fuel-efficient material compositions will gain a significant advantage. Furthermore, the convergence of traditional metallurgy with advanced digital technologies like AI and additive manufacturing is creating new avenues for market leadership and product differentiation.

- Robust market growth projected at a 6.8% CAGR through 2033.

- Market size estimated to reach USD 33.0 Billion by 2033.

- Innovation in lightweight and high-performance materials is a primary growth driver.

- Adoption of advanced manufacturing technologies is critical for market competitiveness.

- Sustainability and environmental compliance are increasingly influencing material selection and development.

- Commercial aviation and defense sectors remain core demand generators.

Steel Alloy Aluminium Alloy Aerospace Material Market Drivers Analysis

The Steel Alloy Aluminium Alloy Aerospace Material market is fundamentally driven by the robust growth in commercial aviation, propelled by rising air passenger traffic and the expansion of airline fleets globally. This necessitates the production of new aircraft, which in turn fuels the demand for high-performance steel and aluminum alloys capable of meeting stringent safety and operational requirements. Concurrently, increased defense budgets and modernization programs across various nations significantly contribute to market growth, as military aircraft and space vehicles require specialized, high-strength materials for demanding applications.

Another pivotal driver is the relentless pursuit of fuel efficiency and emission reduction by aircraft manufacturers and airlines. This imperative pushes for the development and adoption of lighter, yet stronger, materials to decrease aircraft weight, leading to lower fuel consumption and a reduced environmental footprint. Advancements in material science and manufacturing technologies, such as additive manufacturing, further support this trend by enabling the creation of complex, optimized components that were previously unfeasible, thereby accelerating material innovation and market penetration.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Commercial Aircraft | +2.5% | Global, particularly APAC and North America | Short to Mid-term (2025-2030) |

| Increasing Global Defense Expenditure | +1.8% | North America, Europe, Asia Pacific | Mid-term (2025-2033) |

| Focus on Fuel Efficiency and Emission Reduction | +1.5% | Global | Long-term (2025-2033) |

| Technological Advancements in Material Science & Manufacturing | +1.0% | North America, Europe, China | Ongoing, Long-term |

Steel Alloy Aluminium Alloy Aerospace Material Market Restraints Analysis

The Steel Alloy Aluminium Alloy Aerospace Material market faces significant restraints primarily due to the exceptionally high research and development (R&D) and certification costs associated with new materials for aerospace applications. The stringent regulatory environment, including extensive testing and qualification processes mandated by aviation authorities, means that introducing novel materials is a time-consuming and capital-intensive endeavor. This often limits the pace of innovation and can deter smaller players from entering the market, concentrating power among established material providers.

Furthermore, volatility in raw material prices, particularly for critical elements like aluminum, steel, titanium, and specialized alloys, poses a considerable challenge. Fluctuations in commodity markets can directly impact production costs for aerospace material manufacturers, which can then be passed on to aircraft producers, potentially affecting aircraft production volumes and market stability. The long product development and qualification cycles inherent in the aerospace industry also act as a restraint, as it can take many years for a new material to gain acceptance and be integrated into aircraft designs, delaying market adoption and return on investment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D and Certification Costs | -1.2% | Global | Long-term (2025-2033) |

| Stringent Regulatory Framework and Long Qualification Cycles | -1.0% | Global | Long-term (2025-2033) |

| Volatility in Raw Material Prices | -0.8% | Global | Short to Mid-term (2025-2030) |

| Complex Supply Chain and Geopolitical Risks | -0.7% | Global | Short to Mid-term (2025-2030) |

Steel Alloy Aluminium Alloy Aerospace Material Market Opportunities Analysis

Significant opportunities exist in the Steel Alloy Aluminium Alloy Aerospace Material market, particularly with the expanding adoption of additive manufacturing (AM) for complex aerospace components. AM offers unprecedented design freedom, enabling the creation of intricate parts with optimized geometries that are lighter and stronger than traditionally manufactured ones, thereby opening new applications for existing and novel material formulations. This technological shift provides a fertile ground for innovation in powder metallurgy and material development tailored for AM processes.

Furthermore, the growing emphasis on sustainable aviation and circular economy principles presents an opportunity for developing advanced recyclable alloys and composite materials. This includes researching novel ways to incorporate recycled content into aerospace-grade materials without compromising performance, and designing materials for easier end-of-life recycling. Emerging markets, particularly in Asia Pacific, also represent a substantial opportunity due to increasing investments in aerospace infrastructure, military modernization, and a burgeoning commercial aviation sector, driving demand for both established and next-generation aerospace materials.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Additive Manufacturing | +1.5% | Global, particularly North America, Europe, Asia Pacific | Mid to Long-term (2026-2033) |

| Development of Sustainable and Recyclable Materials | +1.2% | Europe, North America | Long-term (2028-2033) |

| Expansion in Emerging Aviation Markets | +1.0% | Asia Pacific, Latin America, Middle East | Short to Mid-term (2025-2030) |

| Integration of Smart Materials and Sensors | +0.8% | North America, Europe | Long-term (2028-2033) |

Steel Alloy Aluminium Alloy Aerospace Material Market Challenges Impact Analysis

The Steel Alloy Aluminium Alloy Aerospace Material market is confronted by several significant challenges, notably the complex and often unpredictable nature of global supply chains. Geopolitical tensions, natural disasters, and pandemics can lead to disruptions in the supply of critical raw materials, impacting production schedules and increasing costs. This necessitates a focus on building more resilient and diversified supply networks, a challenging task given the specialized nature of aerospace material sourcing.

Another major challenge is the increasing stringency of environmental regulations and the growing pressure for sustainable manufacturing practices. While presenting opportunities, meeting these evolving standards requires substantial investment in new technologies and processes, and adapting existing infrastructure. Furthermore, the aerospace industry faces a persistent talent shortage, particularly for skilled metallurgists, material scientists, and manufacturing engineers, which can hinder innovation and production capacity. The long development and qualification cycles for new aircraft programs also create demand volatility, as material suppliers must align their production with highly specific and often delayed aircraft rollout schedules, presenting a forecasting and inventory management challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions | -0.9% | Global | Short to Mid-term (2025-2028) |

| Stringent Environmental Regulations and Sustainability Pressures | -0.7% | Europe, North America | Mid to Long-term (2026-2033) |

| Talent Shortage in Material Science and Engineering | -0.6% | Global | Long-term (2025-2033) |

| High Capital Investment for New Production Technologies | -0.5% | Global | Long-term (2025-2033) |

Steel Alloy Aluminium Alloy Aerospace Material Market - Updated Report Scope

This market research report provides an in-depth analysis of the Steel Alloy Aluminium Alloy Aerospace Material market, encompassing historical data, current market dynamics, and future projections. It delivers comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry landscape. The report also includes detailed segmentation analysis by material type, application, and end-use, alongside a thorough regional assessment to identify key growth pockets and strategic initiatives. Furthermore, a competitive landscape analysis profiles leading market players, offering a holistic view for strategic decision-making and market understanding.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.5 Billion |

| Market Forecast in 2033 | USD 33.0 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Alcoa Corporation, Arconic Corporation, Constellium SE, Kaiser Aluminum, Nippon Steel Corporation, Allegheny Technologies Incorporated (ATI), Carpenter Technology Corporation, Haynes International Inc., VSMPO-AVISMA Corporation, RTI International Metals (part of ATI), Teledyne Technologies Incorporated, AMG Advanced Metallurgical Group, Precision Castparts Corp., Spirit AeroSystems, Safran S.A., Toray Industries Inc., Hexcel Corporation, Cytec Solvay Group, Fushun Special Steel Co. Ltd., Bao-Ti Group Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Steel Alloy Aluminium Alloy Aerospace Material market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of demand patterns, technological shifts, and competitive strategies across various material types, applications, and end-use components within the aerospace sector. Each segment reflects specific performance requirements and market dynamics, contributing uniquely to the overall market landscape.

Understanding these segments is crucial for stakeholders to identify niche opportunities, optimize product portfolios, and tailor manufacturing capabilities to specific industry needs. For instance, the demand for high-strength steel alloys might be concentrated in landing gear and engine components, while advanced aluminum alloys are prevalent in airframes due to their excellent strength-to-weight ratio. The rapid evolution of material science further necessitates a detailed breakdown to track the adoption of next-generation materials and processes across different aerospace applications.

- By Material Type: Steel Alloy (High-Strength Steel, Stainless Steel, Maraging Steel, Others), Aluminium Alloy (2xxx series, 7xxx series, 6xxx series, Aluminium-Lithium Alloys, Others), Titanium Alloy, Nickel Alloy, Composites (Carbon Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites), Other Advanced Materials (Magnesium Alloys, Superalloys).

- By Application: Commercial Aviation, Military Aviation, Space.

- By End-Use: Airframe, Engine, Landing Gear, Interiors, Other Components.

- By Manufacturing Process: Forging, Casting, Extrusion, Rolling, Additive Manufacturing.

Regional Highlights

- North America: This region dominates the Steel Alloy Aluminium Alloy Aerospace Material market, driven by the presence of major aircraft manufacturers, robust defense spending, and significant investments in aerospace R&D. The United States, in particular, leads in both commercial and military aircraft production, fostering high demand for advanced aerospace materials and promoting innovation in material science and manufacturing technologies.

- Europe: Europe represents a strong market for aerospace materials, attributed to the presence of key aerospace companies, extensive R&D facilities, and a focus on sustainable aviation. Countries like France, Germany, and the UK are at the forefront of aircraft manufacturing and material innovation, particularly in areas concerning lightweighting and advanced composites.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, fueled by increasing air passenger traffic, expanding commercial fleets, and growing defense budgets, especially in China and India. Rapid urbanization and industrialization are driving the demand for new aircraft, creating substantial opportunities for aerospace material suppliers.

- Latin America: While smaller, this region shows consistent growth potential due to expanding commercial aviation and military modernization efforts. Brazil stands out as a significant market, with its domestic aircraft manufacturing capabilities driving local and regional demand.

- Middle East and Africa (MEA): The MEA region is experiencing growth in its aerospace sector, driven by strategic geographical location for air travel, increasing investments in airport infrastructure, and military acquisitions. Demand for aerospace materials is rising as air travel expands and defense capabilities are strengthened.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Steel Alloy Aluminium Alloy Aerospace Material Market.- Alcoa Corporation

- Arconic Corporation

- Constellium SE

- Kaiser Aluminum

- Nippon Steel Corporation

- Allegheny Technologies Incorporated (ATI)

- Carpenter Technology Corporation

- Haynes International Inc.

- VSMPO-AVISMA Corporation

- RTI International Metals (part of ATI)

- Teledyne Technologies Incorporated

- AMG Advanced Metallurgical Group

- Precision Castparts Corp.

- Spirit AeroSystems

- Safran S.A.

- Toray Industries Inc.

- Hexcel Corporation

- Cytec Solvay Group

- Fushun Special Steel Co. Ltd.

- Bao-Ti Group Co. Ltd.

Frequently Asked Questions

Analyze common user questions about the Steel Alloy Aluminium Alloy Aerospace Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary factors driving the growth of the Steel Alloy Aluminium Alloy Aerospace Material market?

The market's growth is primarily driven by increasing global demand for commercial and military aircraft, the imperative for enhanced fuel efficiency through lightweight materials, and continuous technological advancements in material science and manufacturing processes like additive manufacturing.

How does artificial intelligence impact the future of aerospace material development?

AI significantly impacts aerospace material development by accelerating material discovery, optimizing alloy design and manufacturing parameters, and enhancing quality control and predictive maintenance. This leads to faster R&D cycles, improved material performance, and reduced production costs.

What are the key challenges faced by manufacturers in the Steel Alloy Aluminium Alloy Aerospace Material market?

Key challenges include high R&D and certification costs, stringent regulatory requirements, volatility in raw material prices, complex global supply chain disruptions, and the need to meet increasingly strict environmental and sustainability standards.

Which regions are expected to exhibit the most significant growth in the aerospace material market?

The Asia Pacific region, particularly China and India, is projected to show the most significant growth due to expanding commercial aviation fleets, rising air passenger traffic, and increased defense spending. North America and Europe will continue to be dominant markets driven by established aerospace industries.

What types of materials are most critical for next-generation aircraft designs?

Next-generation aircraft designs heavily rely on advanced lightweight materials such as aluminum-lithium alloys, high-strength steels, titanium alloys, nickel-based superalloys, and particularly advanced composites like carbon fiber reinforced polymers (CFRPs), to achieve superior strength-to-weight ratios and enhanced performance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted