Solid State Cooling Market

Solid State Cooling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701204 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

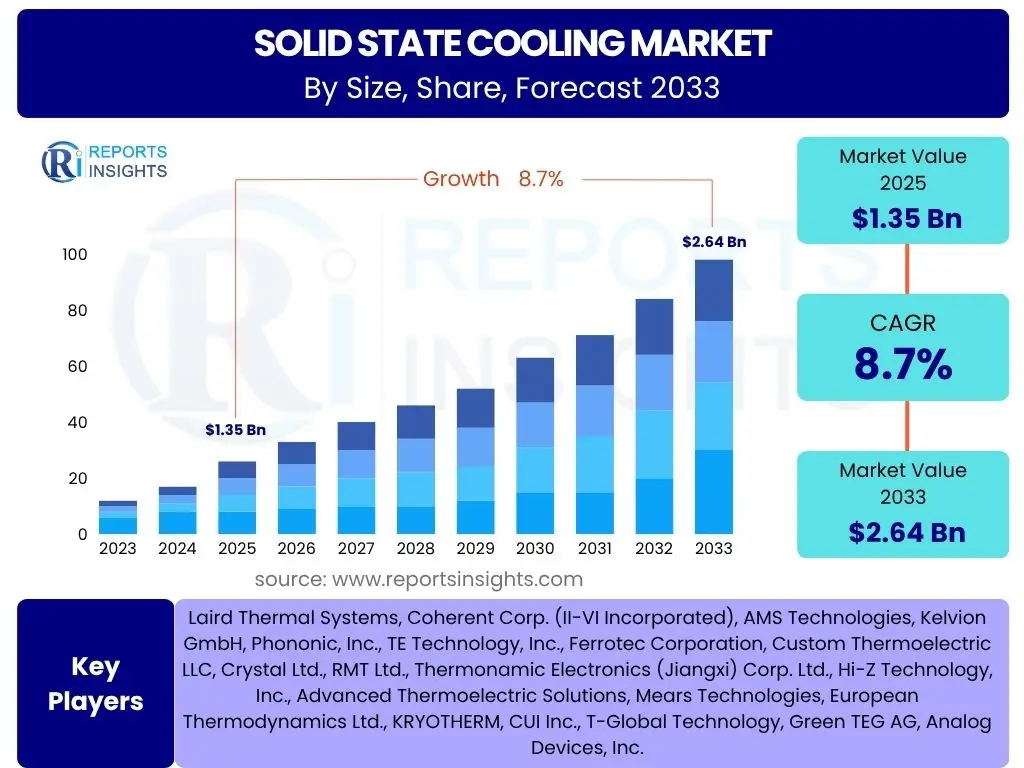

Solid State Cooling Market Size

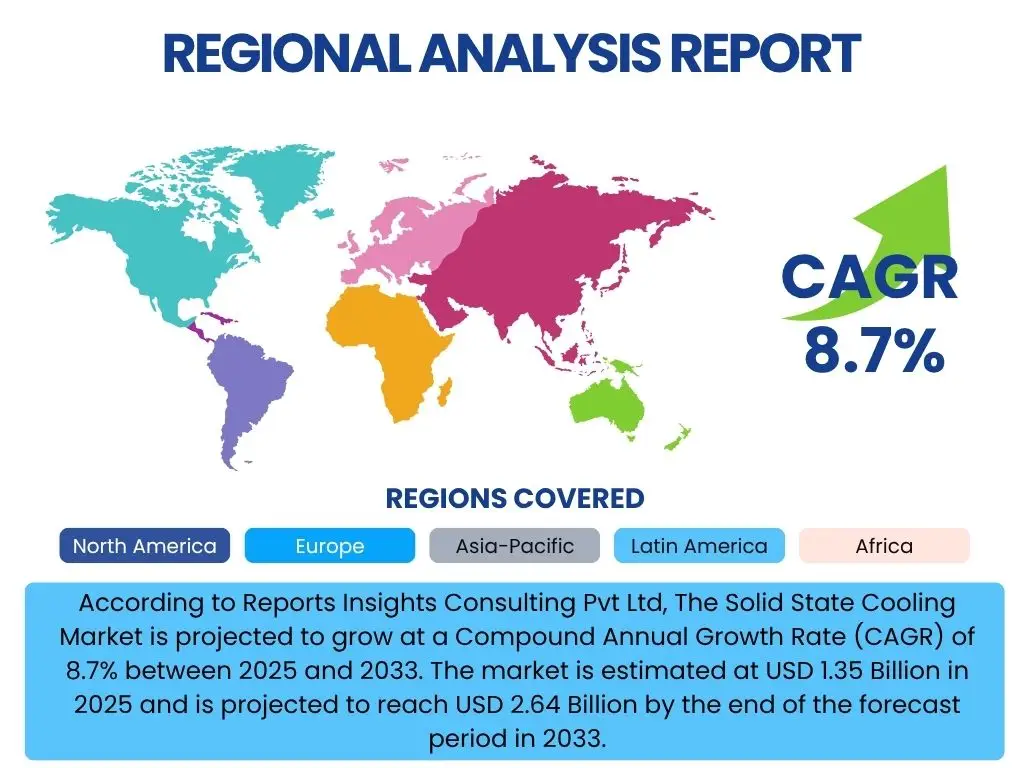

According to Reports Insights Consulting Pvt Ltd, The Solid State Cooling Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 1.35 Billion in 2025 and is projected to reach USD 2.64 Billion by the end of the forecast period in 2033.

Key Solid State Cooling Market Trends & Insights

The Solid State Cooling Market is experiencing significant transformation, driven by an escalating demand for highly efficient, compact, and environmentally friendly thermal management solutions across diverse industries. Key user inquiries frequently center on the underlying technological shifts and application advancements that are shaping this evolving landscape. Consumers and industry professionals are increasingly seeking insights into the adoption rates of these technologies in emerging sectors, along with the performance benchmarks that differentiate solid state cooling from conventional methods. There is a strong interest in understanding how miniaturization, increased power density in electronics, and stringent energy efficiency regulations are collectively pushing the boundaries of solid state thermal management, fostering innovation in materials science and system design.

Furthermore, user questions often highlight the expanding application spectrum of solid state cooling, moving beyond traditional electronics into areas such as medical devices, automotive electrification, and telecommunications infrastructure. The focus is not just on cooling performance, but also on aspects like silent operation, vibration-free performance, and precise temperature control, which are critical in sensitive environments. The market's trajectory is also influenced by advancements in manufacturing processes and economies of scale, which are gradually reducing the cost barrier to widespread adoption. This holistic evolution in technology, application, and economic viability underscores the dynamic nature of the solid state cooling industry.

- Miniaturization and compact designs for advanced electronics and portable devices.

- Increasing adoption of thermoelectric coolers (TECs) in automotive thermal management, particularly for electric vehicles (EVs).

- Growing demand for silent, vibration-free, and precise temperature control solutions in medical and laboratory equipment.

- Integration of solid state cooling systems with Internet of Things (IoT) and smart home devices for enhanced efficiency.

- Research and development in novel materials like magnetocaloric and electrocaloric for improved cooling efficiency and broader applications.

AI Impact Analysis on Solid State Cooling

Common user questions regarding the impact of Artificial Intelligence (AI) on Solid State Cooling revolve around its potential to revolutionize design, optimization, and real-time operational efficiency. Users are keenly interested in how AI algorithms can enhance the predictive capabilities of thermal management systems, enabling proactive adjustments to cooling parameters based on anticipated thermal loads or environmental conditions. This includes inquiries about AI's role in optimizing energy consumption, extending component lifespan through precise temperature regulation, and identifying potential system failures before they occur. The integration of AI is seen as a crucial step towards creating truly "smart" cooling solutions that can adapt and learn, thereby maximizing performance while minimizing energy expenditure and maintenance requirements.

Furthermore, there is significant curiosity about AI's application in the design and material discovery phases of solid state cooling technologies. Users often question how AI-driven simulations and data analysis can accelerate the development of more efficient thermoelectric materials, improve heat sink designs, or optimize the overall architecture of solid state cooling modules. The capacity of AI to process vast amounts of thermal data, identify complex patterns, and generate innovative design iterations is a key theme in these discussions. This shift towards AI-enhanced engineering promises to unlock new levels of performance and cost-effectiveness, moving solid state cooling solutions beyond conventional limitations and making them more viable for a wider range of high-performance and critical applications.

- AI-driven optimization of solid state cooling system parameters for enhanced energy efficiency and performance.

- Predictive maintenance capabilities using AI to monitor cooling system health and anticipate failures.

- AI-assisted material discovery and design for novel thermoelectric, magnetocaloric, and electrocaloric compounds.

- Real-time thermal management adjustments enabled by AI for dynamic cooling requirements in complex electronic systems.

- Integration of AI with sensor networks to create intelligent, adaptive solid state cooling solutions in smart environments.

Key Takeaways Solid State Cooling Market Size & Forecast

Analyzing common user questions about the Solid State Cooling market size and forecast reveals a strong emphasis on understanding the primary growth catalysts and the long-term investment potential of this sector. Users frequently inquire about the specific technological advancements driving market expansion, such as improvements in thermoelectric material efficiency and the emergence of new solid state cooling principles. There is significant interest in identifying the fastest-growing application areas and geographical regions, which informs strategic planning and market entry decisions for businesses. The overarching sentiment is one of optimism regarding the market's trajectory, particularly given the global push for energy efficiency and sustainable technologies, positioning solid state cooling as a critical component in future high-tech infrastructure.

Furthermore, insights gleaned from user queries highlight the critical role of evolving industry standards and regulatory frameworks in shaping market growth. Stakeholders are keen to understand how stricter environmental regulations, particularly concerning traditional refrigerants, are accelerating the adoption of solid state alternatives. The scalability and cost-effectiveness of these technologies over the forecast period are also frequent topics of discussion, as these factors directly impact mass market penetration. The market's growth is therefore not just a function of technological innovation, but also of a confluence of environmental pressures, economic viability, and expanding application diversity, all contributing to a robust and promising outlook for solid state cooling.

- The market is poised for significant expansion, driven by increasing power densities in electronics and the demand for silent, vibration-free cooling.

- Technological advancements in thermoelectric materials and the exploration of new cooling phenomena are key to future growth.

- Growing adoption in niche and high-value applications such as medical devices, automotive, and aerospace will fuel market expansion.

- Environmental regulations promoting alternatives to traditional refrigerants are a strong market catalyst.

- Asia Pacific is expected to remain a dominant and rapidly growing region due to robust electronics manufacturing and increasing industrialization.

Solid State Cooling Market Drivers Analysis

The Solid State Cooling Market is primarily propelled by a convergence of technological imperatives and environmental pressures. The relentless miniaturization of electronic components across consumer electronics, telecommunications, and computing sectors necessitates highly compact and efficient thermal management solutions that traditional cooling systems cannot adequately provide. As devices become smaller and more powerful, the heat flux density increases exponentially, driving the demand for solid state cooling technologies like thermoelectric coolers that offer precise temperature control within limited spaces without moving parts or refrigerants. This miniaturization trend is a fundamental driver, pushing manufacturers towards innovative cooling methods that align with evolving design paradigms.

Moreover, global initiatives promoting energy efficiency and sustainable practices are significantly bolstering the market. Strict environmental regulations aimed at phasing out ozone-depleting substances and high-GWP (Global Warming Potential) refrigerants, coupled with the increasing cost of energy, make solid state cooling an attractive alternative. Its inherent advantages—such as silent operation, low maintenance, and environmental friendliness—resonate with industrial and consumer demands for sustainable technologies. The growing adoption of solid state cooling in critical applications like medical devices, electric vehicle battery thermal management, and data centers further underscores its indispensable role in addressing modern cooling challenges and supporting advanced technological ecosystems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization of Electronics and Increasing Power Density | +2.1% | Global, particularly North America, APAC, Europe | Short to Long Term (2025-2033) |

| Growing Demand for Energy-Efficient and Environmentally Friendly Cooling Solutions | +1.8% | Global, especially Europe, North America, China | Medium to Long Term (2026-2033) |

| Advancements in Thermoelectric Materials and Manufacturing Processes | +1.5% | Global, especially Japan, South Korea, Germany | Medium to Long Term (2027-2033) |

| Increasing Adoption in Niche and High-Value Applications (e.g., Medical, Automotive EV, Aerospace) | +1.3% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2030) |

| Regulatory Support and Incentives for Green Technologies | +1.0% | Europe, North America, Japan | Medium to Long Term (2026-2033) |

Solid State Cooling Market Restraints Analysis

Despite its inherent advantages, the Solid State Cooling Market faces significant restraints that could impede its growth trajectory. One of the primary limiting factors is the relatively high initial cost associated with solid state cooling modules, particularly for high-capacity applications, when compared to conventional vapor compression systems. The specialized materials, precise manufacturing processes, and smaller production volumes for many advanced thermoelectric or magnetocaloric devices contribute to a higher unit cost, making them less competitive for cost-sensitive, large-scale industrial or commercial cooling needs. This cost disparity often acts as a deterrent for broader adoption, confining solid state solutions primarily to niche or premium applications where their specific advantages outweigh the higher investment.

Another notable restraint is the inherent lower cooling capacity and efficiency of current solid state technologies, especially at higher temperature differentials or for very large heat loads. While excellent for precise temperature control and cooling smaller areas, these technologies often struggle to match the bulk cooling power of traditional compressors, making them unsuitable for applications requiring significant heat removal over large volumes. Furthermore, the efficiency of thermoelectric coolers, a dominant solid state technology, can degrade significantly as the temperature difference between the hot and cold sides increases, limiting their practical application range. These technical limitations, coupled with a general lack of widespread awareness or understanding among potential end-users regarding their full capabilities and appropriate applications, present considerable barriers to accelerating market penetration and achieving broader market share.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost Compared to Traditional Cooling Systems | -1.5% | Global, especially developing economies | Short to Medium Term (2025-2030) |

| Lower Cooling Capacity and Efficiency for Large-Scale Applications | -1.2% | Global, particularly industrial sectors | Short to Medium Term (2025-2030) |

| Limited Awareness and Understanding Among End-Users | -0.8% | Emerging markets, niche industries | Short Term (2025-2028) |

| Challenges in Heat Dissipation at the Hot Side | -0.7% | Global, high-power density applications | Short to Medium Term (2025-2030) |

| Material Limitations and Manufacturing Scalability Issues | -0.5% | Global, particularly for novel technologies | Medium Term (2026-2031) |

Solid State Cooling Market Opportunities Analysis

The Solid State Cooling Market is ripe with opportunities, primarily driven by continuous innovation in material science and the emergence of new application domains. Significant advancements in thermoelectric materials, including the development of new alloys and nanostructured materials, are paving the way for higher efficiencies and broader temperature ranges, directly addressing some of the traditional limitations of solid state cooling. These material breakthroughs are crucial for improving the coefficient of performance (COP) and power density of solid state modules, making them more competitive against conventional cooling technologies and expanding their utility in demanding environments. Investments in research and development for novel magnetocaloric, electrocaloric, and thermionic cooling technologies also present substantial long-term growth avenues, promising even greater efficiency and unique operational characteristics.

Furthermore, the expanding landscape of consumer electronics, wearable technology, and the burgeoning Internet of Things (IoT) ecosystem offers substantial opportunities for solid state cooling solutions. As devices become smarter, smaller, and more pervasive, the need for compact, silent, and reliable thermal management intensifies. Solid state coolers are ideally suited for these applications due to their small form factor, lack of moving parts, and ability to provide precise temperature control, which is crucial for sensitive electronics and extended battery life. Additionally, the growing focus on sustainable technologies and the push for renewable energy sources present opportunities for solid state cooling in niche applications such as waste heat recovery and energy harvesting, further diversifying market revenue streams and bolstering long-term market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Thermoelectric and Novel Caloric Materials | +1.9% | Global, particularly APAC (China, Japan, South Korea), Europe, North America | Medium to Long Term (2027-2033) |

| Expansion into New and Emerging Applications (Wearables, IoT, Flexible Electronics) | +1.6% | Global, especially North America, Europe, China | Short to Medium Term (2025-2030) |

| Integration with Renewable Energy Systems and Waste Heat Recovery | +1.4% | Europe, North America, Japan | Medium to Long Term (2026-2033) |

| Increasing Demand for Micro-cooling and Spot Cooling in High-Density Systems | +1.2% | Global, particularly Data Centers, Telecommunications | Short to Medium Term (2025-2030) |

| Strategic Partnerships and Collaborations for R&D and Market Expansion | +0.9% | Global | Short to Long Term (2025-2033) |

Solid State Cooling Market Challenges Impact Analysis

The Solid State Cooling Market faces several significant challenges that necessitate ongoing innovation and strategic market development. One major challenge is the inherent limitation in cooling capacity and efficiency, particularly when dealing with large thermal loads or requiring substantial temperature differentials. Current solid state cooling technologies, such as thermoelectric modules, are often optimized for precise temperature control over small areas but tend to exhibit lower coefficients of performance (COP) compared to traditional vapor compression systems for bulk cooling applications. This efficiency gap can lead to higher power consumption for the same cooling effect in certain scenarios, posing a hurdle for widespread adoption in energy-intensive industries and requiring sophisticated heat sinking on the hot side to maintain efficiency.

Another critical challenge lies in the complexity of system integration and thermal management. Effectively integrating solid state cooling modules into diverse electronic systems requires meticulous design to manage heat dissipation from the hot side of the cooler, often necessitating additional heat sinks, fans, or liquid cooling loops. This adds to the overall system complexity, size, and cost, diminishing some of the advantages of solid state cooling's compact nature. Furthermore, ensuring the long-term reliability and longevity of solid state devices, especially under constant thermal cycling and varying environmental conditions, remains an engineering challenge. Addressing these issues through advanced materials, improved module design, and streamlined integration processes is crucial for the market to overcome these barriers and realize its full potential across a broader range of applications.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Efficiency Limitations and Thermal Management Complexity | -1.0% | Global, especially high-power applications | Short to Medium Term (2025-2030) |

| Cost-Effectiveness at Scale for Mass Market Applications | -0.9% | Global, particularly consumer electronics | Short to Medium Term (2025-2030) |

| Long-Term Reliability and Durability Under Extreme Conditions | -0.6% | Global, especially industrial, aerospace, and automotive sectors | Medium Term (2026-2031) |

| Competition from Established Conventional Cooling Technologies | -0.5% | Global, particularly in traditional HVAC and refrigeration | Short to Medium Term (2025-2030) |

| Standardization and Interoperability of Solid State Cooling Modules | -0.4% | Global, across various industries | Long Term (2028-2033) |

Solid State Cooling Market - Updated Report Scope

This comprehensive report delves into the Solid State Cooling Market, providing a detailed analysis of its size, growth trajectories, and key influencing factors over the forecast period. It offers an in-depth examination of market dynamics, including drivers, restraints, opportunities, and challenges, along with a thorough segmentation analysis by technology type, application, and end-use industry. The report also highlights regional market performance, identifying leading and emerging geographical segments, and profiles key competitive players to offer a holistic view of the market landscape. The insights are designed to assist stakeholders in making informed strategic decisions, understanding market trends, and capitalizing on growth opportunities within the solid state cooling domain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 Billion |

| Market Forecast in 2033 | USD 2.64 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Laird Thermal Systems, Coherent Corp. (II-VI Incorporated), AMS Technologies, Kelvion GmbH, Phononic, Inc., TE Technology, Inc., Ferrotec Corporation, Custom Thermoelectric LLC, Crystal Ltd., RMT Ltd., Thermonamic Electronics (Jiangxi) Corp. Ltd., Hi-Z Technology, Inc., Advanced Thermoelectric Solutions, Mears Technologies, European Thermodynamics Ltd., KRYOTHERM, CUI Inc., T-Global Technology, Green TEG AG, Analog Devices, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Solid State Cooling Market is extensively segmented to provide a granular understanding of its diverse components and their respective contributions to overall market growth. This segmentation allows for a detailed analysis of specific technologies, their varied applications across industries, and the distinct needs of different end-use sectors. By dissecting the market along these lines, stakeholders can identify high-growth areas, target specific customer segments with tailored solutions, and develop strategies that leverage the unique advantages of solid state cooling where they are most impactful. The inherent versatility of solid state cooling technologies, capable of precise temperature control and quiet operation, drives their adoption across a wide array of specialized requirements.

The market is primarily segmented by type, encompassing Thermoelectric Coolers (TECs), which utilize the Peltier effect for heating or cooling, alongside emerging technologies like Thermionic, Magnetocaloric, and Electrocaloric Coolers, each with distinct operational principles and efficiency profiles. The application segment delineates the broad range of industries benefiting from solid state cooling, from the omnipresent consumer electronics to highly specialized medical devices, critical automotive systems, and telecommunications infrastructure. Finally, the end-use industry segmentation provides insight into commercial, residential, industrial, and military/government sectors, reflecting the varying scales and requirements of cooling solutions. This multi-dimensional segmentation is crucial for understanding the market's current structure and forecasting its future evolution, as each segment responds to unique market forces and technological advancements.

- By Type:

- Thermoelectric Coolers (TECs)

- Thermionic Coolers

- Magnetocaloric Coolers

- Electrocaloric Coolers

- By Application:

- Consumer Electronics (smartphones, laptops, wearables)

- Automotive (EV battery thermal management, cabin cooling)

- Medical & Healthcare (diagnostic devices, portable medical equipment, laboratory instruments)

- Aerospace & Defense (avionics, satellite thermal control, infrared sensors)

- Industrial (process cooling, semiconductor manufacturing, laser cooling)

- Telecommunications (data centers, optical communication devices)

- Scientific & Research

- By End-Use Industry:

- Commercial

- Residential

- Industrial

- Military & Government

Regional Highlights

The Solid State Cooling Market exhibits distinct regional dynamics, with certain geographies leading in adoption and innovation due to varying industrial landscapes, technological maturity, and regulatory environments. Asia Pacific (APAC) is projected to dominate the market share, primarily driven by its robust electronics manufacturing base, rapid industrialization, and increasing investment in data centers and telecommunications infrastructure, particularly in countries like China, Japan, and South Korea. The region's large consumer electronics market and the continuous demand for miniaturized and high-performance devices significantly contribute to the widespread adoption of solid state cooling solutions. Furthermore, government initiatives supporting green technologies and energy efficiency are accelerating the transition towards these advanced cooling methods.

North America and Europe also represent significant markets, characterized by high adoption rates in advanced medical devices, automotive (especially electric vehicles), and aerospace & defense sectors. These regions prioritize energy efficiency, environmental regulations, and advanced technological integration, fostering an environment conducive to solid state cooling innovation and deployment. The presence of key research institutions and leading technology companies further fuels market growth through continuous R&D and product commercialization. Latin America, the Middle East, and Africa (MEA) are emerging markets, expected to witness steady growth as industrialization progresses, infrastructure develops, and awareness about energy-efficient cooling solutions increases. While currently smaller in market share, these regions offer long-term growth potential, particularly in the telecommunications and nascent electric vehicle sectors.

- North America: Strong demand from medical, aerospace, and automotive (EV) sectors; significant R&D investments and stringent energy efficiency regulations. Key countries include the United States and Canada.

- Europe: Driven by strong environmental regulations, focus on sustainable technologies, and robust automotive and industrial sectors; high adoption in precision cooling applications. Key countries include Germany, France, and the UK.

- Asia Pacific (APAC): Dominant market due to extensive electronics manufacturing, increasing industrialization, and rapid growth in data centers and telecommunications; significant contributions from China, Japan, South Korea, and India.

- Latin America: Emerging market with growing industrial and commercial sectors; increasing awareness and adoption of energy-efficient solutions. Key countries include Brazil and Mexico.

- Middle East and Africa (MEA): Gradual growth anticipated with infrastructure development, increasing urbanization, and investments in telecommunications and renewable energy projects. Key countries include UAE and Saudi Arabia.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Solid State Cooling Market.- Laird Thermal Systems

- Coherent Corp. (II-VI Incorporated)

- AMS Technologies

- Kelvion GmbH

- Phononic, Inc.

- TE Technology, Inc.

- Ferrotec Corporation

- Custom Thermoelectric LLC

- Crystal Ltd.

- RMT Ltd.

- Thermonamic Electronics (Jiangxi) Corp. Ltd.

- Hi-Z Technology, Inc.

- Advanced Thermoelectric Solutions

- Mears Technologies

- European Thermodynamics Ltd.

- KRYOTHERM

- CUI Inc.

- T-Global Technology

- Green TEG AG

- Analog Devices, Inc.

Frequently Asked Questions

What is solid state cooling?

Solid state cooling refers to thermal management technologies that use no moving parts, refrigerants, or compressors to transfer heat. These systems typically rely on thermoelectric, thermionic, magnetocaloric, or electrocaloric effects to create a temperature difference, offering advantages such as silent operation, precise temperature control, compact size, and environmental friendliness.

How does solid state cooling differ from traditional cooling methods?

Unlike traditional vapor compression systems that use mechanical compressors, refrigerants, and fans, solid state cooling operates electronically through the direct conversion of electrical energy into thermal energy. This eliminates moving parts, reducing noise, vibration, and maintenance, while offering greater precision in temperature control and a smaller form factor, making it ideal for miniaturized and sensitive applications.

What are the primary applications of solid state cooling?

Solid state cooling finds applications across a broad spectrum of industries including consumer electronics (smartphones, laptops, wearables), medical devices (diagnostic equipment, portable coolers), automotive (electric vehicle battery thermal management, cabin cooling), aerospace and defense, industrial process cooling, telecommunications infrastructure (data centers, optical devices), and scientific research requiring precise temperature control.

What are the key advantages of solid state cooling?

The main advantages include silent and vibration-free operation, compact and lightweight designs, precise temperature control, high reliability due to the absence of moving parts, long lifespan, and environmental friendliness as they do not use ozone-depleting or high global warming potential refrigerants. These benefits make them suitable for sensitive and space-constrained environments.

What is the market outlook for solid state cooling?

The Solid State Cooling Market is projected for substantial growth, driven by increasing demand for compact, energy-efficient, and environmentally friendly thermal management solutions. Factors such as the miniaturization of electronics, advancements in material science, and stringent environmental regulations are expected to propel market expansion, particularly in high-growth application areas like electric vehicles, medical devices, and data centers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted