Autonomou Driving Solid State LiDAR Market

Autonomou Driving Solid State LiDAR Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703536 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Autonomou Driving Solid State LiDAR Market Size

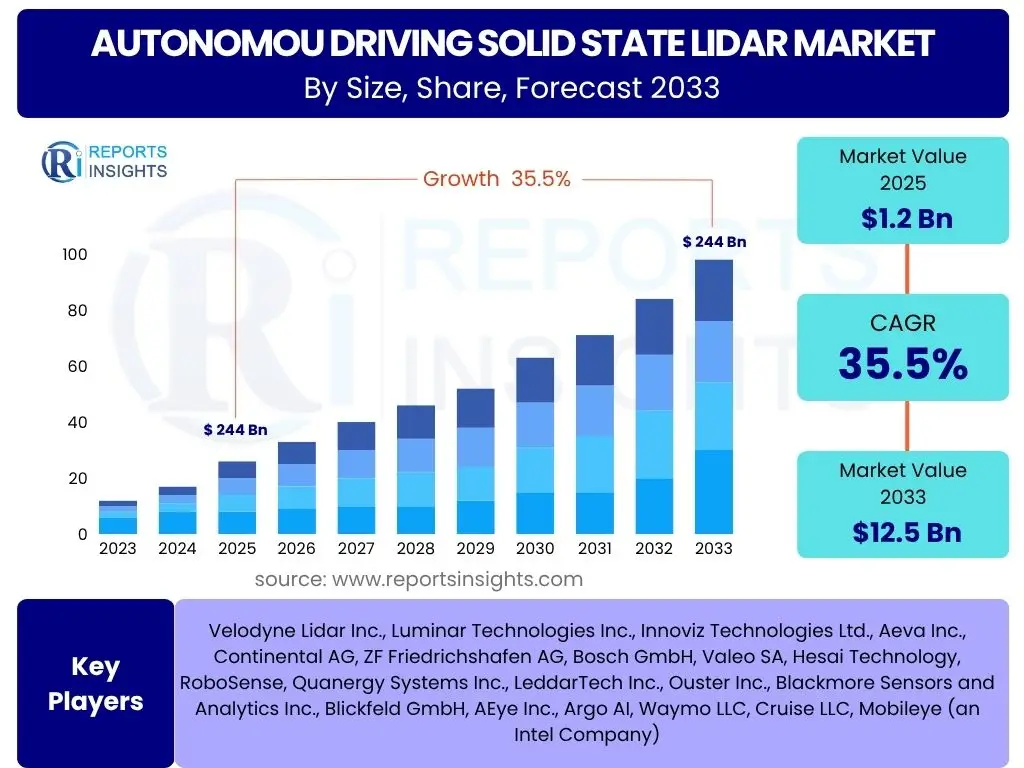

According to Reports Insights Consulting Pvt Ltd, The Autonomou Driving Solid State LiDAR Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 35.5% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 12.5 Billion by the end of the forecast period in 2033.

Key Autonomou Driving Solid State LiDAR Market Trends & Insights

The autonomous driving solid state LiDAR market is undergoing significant transformations driven by a confluence of technological advancements, evolving regulatory landscapes, and increasing demand for higher levels of vehicle autonomy. Key user inquiries often center on the progress of miniaturization and cost reduction, the integration capabilities with other sensor modalities, and the overall reliability and performance under diverse environmental conditions. There is a strong interest in understanding how solid-state LiDAR addresses the limitations of traditional mechanical systems, particularly concerning durability, scalability, and mass production feasibility.

Another area of consistent user interest revolves around the adoption curve of this technology across different vehicle segments, from passenger cars to commercial fleets and robotaxis. Users frequently seek insights into the competitive landscape, examining which technological approaches (e.g., MEMS, OPA, Flash) are gaining traction and why. The push for enhanced safety features and the development of advanced driver-assistance systems (ADAS) are primary drivers, leading to questions about LiDAR's role in achieving Level 3, 4, and 5 autonomous capabilities, and how these advancements are shaping the future of mobility.

- Miniaturization and Cost Reduction: Continuous advancements in manufacturing processes and semiconductor technology are enabling smaller, more cost-effective solid-state LiDAR units, crucial for mass market adoption.

- Sensor Fusion Integration: Growing emphasis on seamlessly integrating solid-state LiDAR with cameras, radar, and ultrasonic sensors to create a robust and redundant perception system for autonomous vehicles.

- AI-Powered Perception: Increasing reliance on artificial intelligence and machine learning algorithms to process complex LiDAR data, enabling enhanced object detection, classification, and tracking capabilities.

- Regulatory Support and Standardization: Governments and industry bodies are working towards establishing clear regulatory frameworks and performance standards for autonomous vehicle sensors, accelerating deployment.

- Diverse Application Expansion: Beyond passenger cars, solid-state LiDAR is finding increasing applications in commercial vehicles, logistics, robotaxis, smart infrastructure, and industrial automation, diversifying market opportunities.

- Improved Reliability and Durability: Solid-state designs offer inherently greater resistance to vibrations, shocks, and environmental elements compared to mechanical counterparts, leading to longer operational lifespans.

- Enhanced Range and Resolution: Ongoing research and development efforts are focused on improving the range, angular resolution, and reflectivity measurement capabilities of solid-state LiDARs, crucial for high-speed autonomous driving scenarios.

AI Impact Analysis on Autonomou Driving Solid State LiDAR

Common user questions regarding AI's impact on autonomous driving solid state LiDAR primarily focus on how artificial intelligence enhances the raw data generated by LiDAR sensors to improve perception accuracy and decision-making for autonomous systems. Users are keen to understand how AI algorithms can filter noise, interpret complex scenes, and predict object behavior, thereby elevating the utility of LiDAR beyond simple distance measurement. Concerns often arise about the computational demands of AI-driven LiDAR processing and the need for robust, real-time inferencing capabilities to ensure vehicle safety.

Furthermore, there is significant interest in how AI facilitates sensor fusion, optimizing the combined strengths of LiDAR with other sensor modalities like cameras and radar. Users frequently inquire about AI's role in self-calibration, anomaly detection, and the development of sophisticated perception stacks that can operate reliably in challenging environmental conditions, such as heavy rain, fog, or snow. The overarching expectation is that AI will unlock the full potential of solid-state LiDAR, moving it from a data generator to an intelligent perception component vital for truly autonomous operation.

- Enhanced Data Processing: AI algorithms enable real-time processing of vast LiDAR point cloud data, reducing latency and providing immediate environmental insights.

- Improved Object Recognition and Classification: Machine learning models trained on diverse datasets significantly enhance the accuracy of identifying and categorizing objects (e.g., pedestrians, vehicles, cyclists) within the LiDAR scan.

- Predictive Analytics: AI-powered analytics can forecast the trajectory and behavior of detected objects, contributing to safer and more proactive path planning for autonomous vehicles.

- Noise Reduction and Signal Enhancement: AI filters out environmental noise and interference, improving the clarity and reliability of LiDAR data in adverse conditions.

- Sensor Fusion Optimization: AI acts as the central intelligence for fusing data from LiDAR with other sensors (camera, radar), creating a comprehensive and redundant environmental model.

- Adaptive Perception: AI allows LiDAR systems to adapt their scanning patterns and parameters in real-time based on environmental conditions and driving scenarios, optimizing performance.

- Calibration and Self-Optimization: AI facilitates continuous self-calibration of LiDAR sensors and optimizes their performance over time, reducing maintenance and ensuring consistent accuracy.

Key Takeaways Autonomou Driving Solid State LiDAR Market Size & Forecast

Analysis of user inquiries about the autonomous driving solid state LiDAR market size and forecast reveals a strong interest in understanding the core growth drivers, the pace of technological maturation, and the implications for investment and industry strategy. Users are keen to ascertain the trajectory of market expansion, particularly how quickly the technology will transition from niche, high-end applications to mass-market integration within consumer vehicles. There's a persistent curiosity about the tipping points for adoption, such as specific cost thresholds or regulatory mandates that could accelerate market growth significantly.

Furthermore, users seek clarity on which segments within the autonomous driving ecosystem will be the primary beneficiaries and drivers of LiDAR demand. Questions often revolve around the projected revenues, the competitive intensity among sensor manufacturers, and the overall long-term viability of solid-state LiDAR as the foundational sensor for future autonomous mobility solutions. The insights gained from these forecasts directly inform strategic decisions for automotive OEMs, Tier 1 suppliers, and technology developers aiming to capitalize on this rapidly evolving market.

- High Growth Potential: The market is poised for exponential growth, driven by increasing adoption of autonomous driving features and the indispensable role of LiDAR in achieving higher levels of autonomy.

- Technology Maturation: Solid-state LiDAR technology is rapidly evolving, addressing previous limitations related to cost, size, and performance, paving the way for widespread commercialization.

- Ecosystem Collaboration: Strategic partnerships between LiDAR manufacturers, automotive OEMs, and software developers are crucial for accelerating integration and market penetration.

- Cost-Performance Optimization: Continued innovation is focused on reducing the unit cost of solid-state LiDARs while simultaneously improving their range, resolution, and reliability, making them more attractive for mass production.

- Regulatory Harmonization: Global efforts to standardize regulations for autonomous vehicles will provide a clear pathway for the deployment of LiDAR-equipped systems, reducing market uncertainties.

- Diverse Application Horizon: While automotive remains the primary driver, emerging applications in smart cities, industrial robotics, and logistics significantly expand the total addressable market.

Autonomou Driving Solid State LiDAR Market Drivers Analysis

The autonomous driving solid state LiDAR market is primarily driven by the escalating demand for advanced driver-assistance systems (ADAS) and full autonomous driving capabilities across the automotive sector. As vehicles progress from Level 2+ to Level 3, 4, and 5 autonomy, the need for robust, high-resolution 3D environmental perception becomes paramount. Solid state LiDAR offers unparalleled accuracy and reliability in object detection, localization, and mapping, making it a critical sensor for ensuring safety and performance in complex driving scenarios.

Furthermore, increasingly stringent safety regulations and consumer expectations for enhanced vehicle safety are compelling automotive manufacturers to integrate more sophisticated sensor technologies. Governments worldwide are pushing for technologies that can significantly reduce road accidents and fatalities. Solid state LiDAR, with its ability to perform reliably in varying lighting conditions and provide precise depth information, directly addresses these safety imperatives. This regulatory push, combined with competitive pressures among OEMs to differentiate their offerings with superior autonomous features, fuels the market's expansion.

Technological advancements, particularly in semiconductor manufacturing and signal processing, have enabled the development of smaller, more affordable, and durable solid state LiDAR units. These innovations are crucial for overcoming previous barriers to mass adoption, such as high cost and bulkiness. The continuous improvement in performance parameters like range, resolution, and field of view, coupled with the inherent durability of solid-state designs, makes this technology increasingly attractive for integration into production vehicles, thereby propelling market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing ADAS and Autonomous Driving Adoption | +8.5% | Global, particularly North America, Europe, China | Short- to Mid-term (2025-2030) |

| Stringent Vehicle Safety Regulations | +7.0% | Europe, North America, Japan | Short- to Mid-term (2025-2029) |

| Demand for High-Resolution 3D Environmental Perception | +6.2% | Global | Mid- to Long-term (2027-2033) |

| Advancements in Semiconductor and Micro-electromechanical Systems (MEMS) Technology | +5.8% | Asia Pacific (South Korea, Taiwan), North America, Europe | Short- to Mid-term (2025-2031) |

| Growing Investment in Robotaxis and Commercial Autonomous Fleets | +4.5% | North America, China, Europe | Mid- to Long-term (2028-2033) |

| Expansion of Smart City Infrastructure and V2X Communication | +3.5% | China, Singapore, Europe, UAE | Long-term (2030-2033) |

Autonomou Driving Solid State LiDAR Market Restraints Analysis

Despite its significant potential, the autonomous driving solid state LiDAR market faces several restraints that could impede its growth. One primary concern is the relatively high cost of solid state LiDAR sensors compared to other perception technologies like radar and cameras. While costs are declining, they still pose a significant barrier for widespread adoption in mainstream consumer vehicles, particularly for lower and mid-range segments. This cost sensitivity limits the integration of multiple LiDAR units per vehicle, which is often desirable for achieving robust 360-degree perception for higher autonomy levels.

Another significant restraint involves technical challenges, particularly concerning performance in adverse weather conditions. Although solid state LiDAR is more robust than mechanical LiDAR, heavy rain, dense fog, or snow can still degrade its performance by scattering laser beams, leading to reduced range or erroneous readings. While ongoing research aims to mitigate these effects through advanced signal processing and AI, achieving consistent reliability across all weather conditions remains a hurdle. Furthermore, the complexity of integrating these sophisticated sensors into existing vehicle architectures and ensuring seamless sensor fusion with other modalities presents a substantial engineering challenge for OEMs.

Supply chain complexities and the nascent stage of mass production for certain solid-state LiDAR technologies also act as restraints. The specialized components and advanced manufacturing processes required for solid state LiDAR can lead to bottlenecks, affecting scalability and increasing lead times. Moreover, the lack of standardized protocols for LiDAR data format and communication across different manufacturers can hinder widespread interoperability and integration, adding to development costs and timelines for autonomous vehicle developers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Solid State LiDAR Sensors | -6.0% | Global, particularly emerging markets | Short- to Mid-term (2025-2029) |

| Performance Limitations in Adverse Weather Conditions | -5.5% | Regions with diverse climates (e.g., North America, Europe, parts of Asia) | Short- to Mid-term (2025-2030) |

| Complex Integration and Calibration Challenges | -4.8% | Global | Short-term (2025-2027) |

| Lack of Industry-Wide Standardization | -4.0% | Global | Mid-term (2027-2031) |

| Computational Demands for Data Processing | -3.5% | Global | Short- to Mid-term (2025-2028) |

Autonomou Driving Solid State LiDAR Market Opportunities Analysis

Significant opportunities exist for the autonomous driving solid state LiDAR market, primarily stemming from the expansion of autonomous technology into new and diverse application areas beyond traditional passenger vehicles. The rapidly growing sectors of robotaxis, autonomous shuttles, and logistics vehicles present a substantial untapped market. These applications often operate in geo-fenced or controlled environments, where solid-state LiDAR's precise mapping and obstacle detection capabilities can be immediately leveraged, offering quicker ROI and facilitating earlier deployment compared to mass-market consumer cars.

Furthermore, the evolution of smart city initiatives and the increasing adoption of Vehicle-to-Everything (V2X) communication technologies create new avenues for LiDAR integration. LiDAR sensors can be deployed as stationary infrastructure sensors to monitor traffic flow, pedestrian activity, and potential hazards, providing crucial data for autonomous vehicles and city management systems. This infrastructure-as-a-sensor model enhances the perception capabilities of connected and autonomous vehicles, while also contributing to overall urban intelligence and safety, presenting a lucrative growth opportunity.

Technological advancements, particularly in the realm of 4D LiDAR and frequency-modulated continuous wave (FMCW) technology, also represent key opportunities. These innovations promise enhanced capabilities such as instantaneous velocity detection and immunity to interference from other LiDARs, further improving the robustness and reliability of autonomous perception. As these advanced solid-state LiDAR types mature and become more cost-effective, they are expected to open new use cases and accelerate adoption across a broader spectrum of autonomous driving applications, securing LiDAR's foundational role in the future of mobility.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Robotaxis, Autonomous Shuttles, and Logistics Vehicles | +7.0% | North America, China, Europe | Short- to Mid-term (2025-2030) |

| Integration with Smart City Infrastructure and V2X Communication | +6.5% | China, Singapore, Europe, Middle East | Mid- to Long-term (2028-2033) |

| Development of 4D LiDAR and FMCW Technologies | +5.8% | Global (leading R&D hubs: US, Germany, Israel) | Mid- to Long-term (2027-2033) |

| Increased Demand for Industrial Automation and Off-Highway Autonomous Vehicles | +4.2% | Europe, North America, Japan | Mid-term (2026-2032) |

| Strategic Partnerships and Ecosystem Development | +3.5% | Global | Short- to Mid-term (2025-2030) |

Autonomou Driving Solid State LiDAR Market Challenges Impact Analysis

The autonomous driving solid state LiDAR market faces several significant challenges that could hinder its full potential and widespread adoption. One key challenge is the ongoing battle to achieve comprehensive sensor redundancy and fusion that is robust enough for Level 4 and Level 5 autonomous driving. While LiDAR excels in depth perception, it still requires seamless integration with cameras for color information and radar for adverse weather resilience. Ensuring that these diverse sensor modalities work harmoniously without conflicts or data interpretation discrepancies remains a complex engineering hurdle, impacting overall system reliability and development timelines.

Another major challenge revolves around standardization across the industry. The absence of universal protocols for LiDAR data formats, interfaces, and performance metrics creates fragmentation, making it difficult for OEMs to integrate components from different suppliers and for software developers to create scalable perception stacks. This lack of standardization can lead to higher development costs, slower innovation cycles, and interoperability issues, thereby delaying the broad commercialization of autonomous vehicles equipped with solid-state LiDAR.

Furthermore, regulatory uncertainties and public acceptance pose formidable challenges. Governments globally are still in the process of defining comprehensive legal frameworks for autonomous vehicles, including liabilities, testing methodologies, and deployment guidelines. These evolving regulations can create ambiguity for manufacturers and delay market entry. Simultaneously, gaining public trust in autonomous technology, especially after high-profile incidents, is critical. Concerns around safety, data privacy, and the ethical implications of AI-driven decisions need to be effectively addressed to foster widespread adoption, directly impacting the demand for core autonomous technologies like solid-state LiDAR.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Robust Sensor Fusion and Redundancy | -5.0% | Global | Short- to Mid-term (2025-2030) |

| Lack of Industry Standards for Data and Integration | -4.5% | Global | Mid-term (2027-2032) |

| Regulatory Uncertainties and Evolving Legal Frameworks | -4.0% | North America, Europe, China | Short- to Mid-term (2025-2029) |

| Public Perception and Trust in Autonomous Technology | -3.5% | Global | Long-term (2028-2033) |

| Cybersecurity Risks and Data Privacy Concerns | -3.0% | Global | Mid- to Long-term (2027-2033) |

Autonomou Driving Solid State LiDAR Market - Updated Report Scope

This market insights report provides an in-depth analysis of the Autonomous Driving Solid State LiDAR Market, offering a comprehensive overview of its current landscape and future growth trajectory. The scope encompasses detailed market sizing and forecasting, key trends, impact analysis of artificial intelligence, and a thorough examination of market drivers, restraints, opportunities, and challenges. The report segments the market by technology type, application, autonomy level, and component, providing granular insights across various dimensions. Additionally, it highlights regional dynamics and profiles leading market players to offer a complete competitive outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 12.5 Billion |

| Growth Rate | 35.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Velodyne Lidar Inc., Luminar Technologies Inc., Innoviz Technologies Ltd., Aeva Inc., Continental AG, ZF Friedrichshafen AG, Bosch GmbH, Valeo SA, Hesai Technology, RoboSense, Quanergy Systems Inc., LeddarTech Inc., Ouster Inc., Blackmore Sensors and Analytics Inc., Blickfeld GmbH, AEye Inc., Argo AI, Waymo LLC, Cruise LLC, Mobileye (an Intel Company) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The autonomous driving solid state LiDAR market is segmented to provide a granular understanding of its diverse components and applications, enabling targeted analysis of growth opportunities and market dynamics. This segmentation helps identify specific technological preferences, application-specific requirements, and the varying levels of adoption across different autonomy stages. Each segment is critical for market players to develop tailored strategies and for stakeholders to understand the underlying forces driving innovation and commercialization in this complex ecosystem.

- By Type:

- MEMS LiDAR: Utilizes micro-electromechanical systems mirrors for beam steering, offering a balance of performance and cost efficiency.

- OPA (Optical Phased Array) LiDAR: Employs no moving parts by manipulating light waves, promising ultimate solid-state reliability and speed.

- Flash LiDAR: Illuminates the entire scene with a single laser pulse, capturing a 3D image instantly, ideal for short-range applications.

- FSR (Frequency-Scanned Range) LiDAR: Utilizes frequency modulation to determine depth, offering potential immunity to interference.

- Others: Includes emerging technologies or niche solid-state approaches.

- By Application:

- Passenger Vehicles: Integration into consumer cars for ADAS and higher levels of autonomy.

- Commercial Vehicles: Use in trucks, buses, and other heavy-duty vehicles for logistics and transportation.

- Robotaxis/Shuttles: Essential for fully autonomous ride-hailing and public transport services.

- Logistics/Delivery Vehicles: Enabling autonomous operations in last-mile delivery and warehousing.

- Industrial Vehicles: Applications in mining, construction, and agricultural autonomous machinery.

- Others: Includes drones for mapping, smart infrastructure monitoring, and security applications.

- By Autonomy Level:

- Level 2+ (Advanced Driver-Assistance Systems): Enhancing features like adaptive cruise control and lane keeping with better perception.

- Level 3 (Conditional Automation): Requiring driver intervention under specific conditions but allowing hands-off driving.

- Level 4 (High Automation): Operating autonomously in defined operational design domains (ODDs) without driver intervention.

- Level 5 (Full Automation): Capable of autonomous driving under all conditions and scenarios.

- By Component:

- Transceivers: Involving laser emitters and receivers (photodetectors) that send and detect light pulses.

- Photodetectors: Including Avalanche Photodiodes (APDs) and Silicon Photomultipliers (SiPMs) for converting light into electrical signals.

- Scanners: Such as MEMS mirrors or optical phased arrays that steer the laser beam.

- Processors: ASICs (Application-Specific Integrated Circuits) and FPGAs (Field-Programmable Gate Arrays) for real-time data processing.

- Optical Components: Lenses, filters, and other elements critical for LiDAR performance.

- Software: Algorithms for point cloud processing, object detection, classification, and tracking.

Regional Highlights

- North America: This region is a leading market for autonomous driving solid state LiDAR, primarily driven by significant investments in autonomous vehicle technology by tech giants, automotive OEMs, and startups. The presence of major research and development centers, coupled with a proactive stance on testing and deploying autonomous fleets (especially robotaxis), positions North America at the forefront. Regulatory support in several states for AV testing and a strong consumer interest in advanced automotive technologies further stimulate market growth.

- Europe: Europe represents a robust market with a strong emphasis on automotive safety regulations and the development of premium ADAS features. Countries like Germany and France are key players, with leading automotive manufacturers heavily investing in autonomous capabilities. While the regulatory landscape is more conservative than in some parts of the US, a clear roadmap towards higher autonomy levels and significant R&D spending on sensor fusion and AI are expected to fuel solid state LiDAR adoption.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, largely due to rapid technological adoption and substantial government support, particularly in China and South Korea. China's ambitious national strategy for autonomous vehicles, coupled with massive investments in smart city infrastructure and a large automotive production base, makes it a dominant force. Japan and South Korea also contribute significantly with their advanced automotive industries and focus on technological innovation in sensing solutions.

- Latin America: While an emerging market, Latin America shows potential for growth in the long term. Initial adoption is expected in commercial fleets, logistics, and specific public transportation projects where operational efficiencies can justify the investment in autonomous technologies. The development of supportive infrastructure and regulatory frameworks will be crucial for the widespread integration of solid state LiDAR in this region.

- Middle East and Africa (MEA): The MEA region is characterized by significant investments in smart city initiatives, particularly in countries like UAE and Saudi Arabia, which are experimenting with autonomous public transport and smart infrastructure. While the overall automotive market might be smaller, targeted projects in smart cities and specific industrial applications are expected to drive the initial uptake of autonomous driving solid state LiDAR technology.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Autonomou Driving Solid State LiDAR Market.- Velodyne Lidar Inc.

- Luminar Technologies Inc.

- Innoviz Technologies Ltd.

- Aeva Inc.

- Continental AG

- ZF Friedrichshafen AG

- Bosch GmbH

- Valeo SA

- Hesai Technology

- RoboSense

- Quanergy Systems Inc.

- LeddarTech Inc.

- Ouster Inc.

- Blackmore Sensors and Analytics Inc.

- Blickfeld GmbH

- AEye Inc.

- Argo AI

- Waymo LLC

- Cruise LLC

- Mobileye (an Intel Company)

Frequently Asked Questions

What is solid-state LiDAR and how does it differ from traditional LiDAR?

Solid-state LiDAR is an advanced type of LiDAR sensor that uses no mechanical moving parts for beam steering, relying instead on technologies like MEMS (Micro-Electromechanical Systems), Optical Phased Arrays (OPA), or Flash illumination. This design eliminates the bulky, rotating components of traditional mechanical LiDAR, leading to smaller, more durable, more reliable, and potentially more cost-effective units, making them suitable for mass production and seamless integration into vehicles.

Why is solid-state LiDAR considered crucial for autonomous driving?

Solid-state LiDAR is considered crucial because it provides high-resolution, precise 3D environmental mapping and object detection capabilities that are vital for safe and reliable autonomous driving. Its ability to perform accurately in varying lighting conditions, combined with its inherent durability and potential for mass production, makes it an indispensable sensor for robust perception, contributing to superior obstacle detection, localization, and collision avoidance in complex driving scenarios.

What are the main applications of autonomous driving solid state LiDAR?

The primary applications include advanced driver-assistance systems (ADAS) in passenger vehicles, fully autonomous vehicles (Level 3-5), robotaxis and autonomous shuttles, commercial vehicles (trucks, buses), logistics and delivery vehicles, and industrial autonomous machinery. Emerging applications also include smart city infrastructure monitoring and V2X communication enhancements.

What are the key challenges facing the adoption of solid-state LiDAR?

Key challenges include the high initial cost, limitations in performance under certain adverse weather conditions (e.g., heavy fog, snow), complex integration requirements with other sensors, a lack of universal industry standardization, and the ongoing need for robust cybersecurity measures. Public perception and regulatory uncertainties also pose significant hurdles to widespread adoption.

How is AI impacting the development and performance of solid-state LiDAR?

AI is profoundly impacting solid-state LiDAR by enhancing its capabilities in real-time data processing, improving object recognition and classification, and enabling predictive analytics for object behavior. AI also facilitates noise reduction, optimizes sensor fusion with other modalities, and allows for adaptive perception and self-calibration, making LiDAR systems more intelligent, accurate, and reliable for autonomous driving.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted