L4 Autonomou Driving Market

L4 Autonomou Driving Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702138 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

L4 Autonomou Driving Market Size

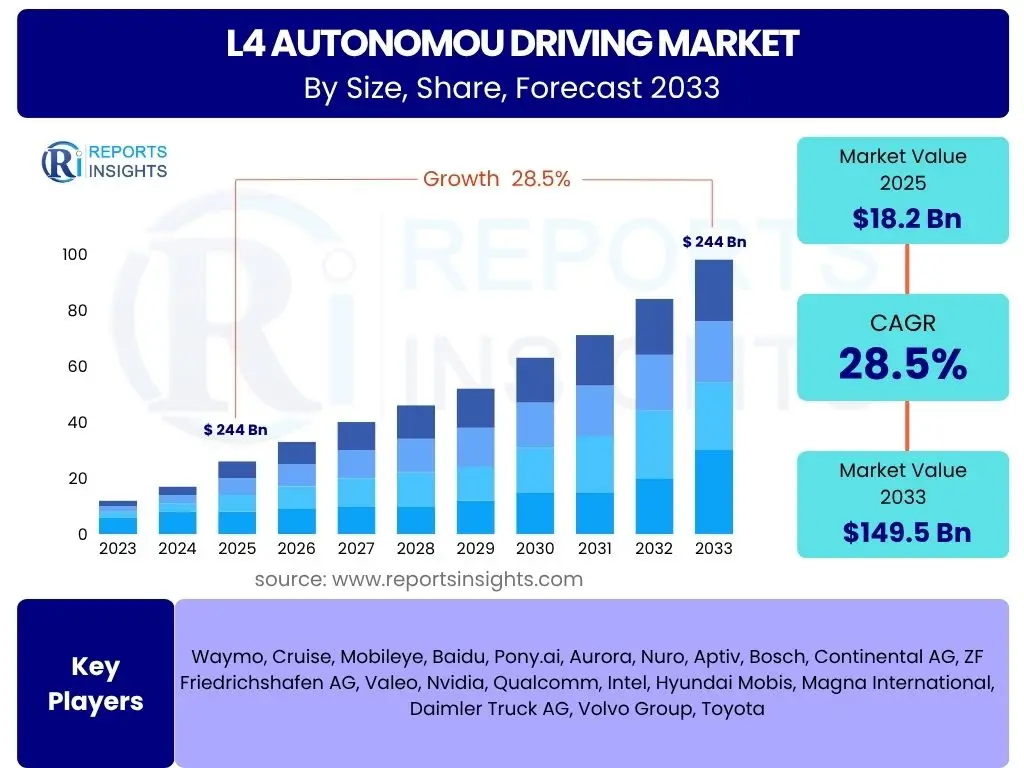

According to Reports Insights Consulting Pvt Ltd, The L4 Autonomou Driving Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 18.2 Billion in 2025 and is projected to reach USD 149.5 Billion by the end of the forecast period in 2033.

Key L4 Autonomou Driving Market Trends & Insights

The L4 autonomous driving market is witnessing transformative trends driven by continuous technological advancements and evolving regulatory landscapes. Users frequently inquire about the progression of sensor technologies, the increasing sophistication of artificial intelligence algorithms, and the integration of these systems into various vehicle platforms. A notable trend is the shift towards software-defined vehicles, where the vehicle's capabilities are increasingly determined by its embedded software and over-the-air updates, enabling rapid feature deployment and performance enhancements. This paradigm allows for greater flexibility and customization in autonomous systems, moving beyond hardware-centric development.

Another significant insight revolves around the burgeoning ecosystem of partnerships and collaborations between traditional automotive original equipment manufacturers (OEMs), technology giants, and specialized artificial intelligence companies. These alliances are crucial for accelerating research and development, sharing the immense costs associated with validation and testing, and navigating complex regulatory hurdles. The industry is also observing a growing emphasis on specific use cases, such as robotaxi services and autonomous logistics, which are proving to be early commercialization pathways. Furthermore, there is a pronounced focus on improving human-machine interaction (HMI) to enhance user trust and acceptance, alongside robust cybersecurity measures to safeguard these complex systems.

- Software-defined vehicle architecture enabling flexible and upgradable autonomous functions.

- Strategic partnerships and collaborations between automotive OEMs, tech firms, and AI specialists.

- Increased focus on commercial applications such as robotaxis, autonomous shuttles, and logistics.

- Advancements in sensor fusion technologies, combining LiDAR, radar, cameras, and ultrasonic sensors for enhanced perception.

- Development of sophisticated mapping and localization technologies, including high-definition (HD) maps.

- Emphasis on vehicle-to-everything (V2X) communication for enhanced situational awareness and coordinated driving.

- Progress in simulation and virtual testing environments to accelerate development and validation processes.

AI Impact Analysis on L4 Autonomou Driving

Artificial intelligence is the foundational pillar for the advancement and practical implementation of L4 autonomous driving systems. Users are keenly interested in how AI enhances perception, decision-making, and control within these complex systems, often asking about the specific AI techniques employed and their implications for safety and reliability. AI, particularly deep learning, allows autonomous vehicles to interpret complex sensory data from cameras, LiDAR, and radar, enabling precise object detection, classification, and tracking even in challenging environmental conditions. This includes identifying pedestrians, other vehicles, traffic signs, and road markings with unprecedented accuracy, directly influencing the vehicle's ability to navigate safely and effectively.

Beyond perception, AI algorithms are critical for predictive analytics, allowing the vehicle to anticipate the actions of other road users and plan its own trajectory accordingly. Reinforcement learning and other advanced AI techniques are being used to train vehicles in diverse driving scenarios, helping them learn optimal behaviors and react intelligently to unforeseen events. The increasing deployment of edge AI allows for real-time processing of vast amounts of data directly within the vehicle, minimizing latency and enabling immediate responses. However, concerns about the explainability and robustness of AI models, particularly in safety-critical situations, are frequently raised, driving research into verifiable AI and ethical considerations within autonomous systems. The continuous evolution of AI is directly correlated with the progress towards full L4 autonomy, addressing technical challenges and fostering greater trust in these sophisticated machines.

- Enhanced Perception: Deep learning models enable highly accurate object detection, classification, and tracking from sensor data.

- Improved Decision-Making: AI-powered algorithms facilitate complex path planning, risk assessment, and behavioral prediction of other road users.

- Real-time Processing: Edge AI solutions deployed directly in vehicles allow for low-latency data processing and rapid response times.

- Adaptive Learning: Reinforcement learning and machine learning optimize driving strategies based on diverse real-world and simulated scenarios.

- Predictive Capabilities: AI helps anticipate pedestrian and vehicle movements, enhancing safety and proactive maneuvering.

- Simulation and Validation: AI is integral to creating realistic simulation environments for testing and validating autonomous driving software.

- Ethical AI: Ongoing research addresses the explainability and ethical implications of AI decisions in autonomous vehicles, especially in unforeseen circumstances.

Key Takeaways L4 Autonomou Driving Market Size & Forecast

The L4 autonomous driving market is poised for significant expansion, reflecting a pivotal shift in the automotive and transportation sectors. Common user inquiries often center on the primary drivers behind this substantial growth and the long-term viability of L4 systems. The market's projected compound annual growth rate indicates a strong and sustained upward trajectory, underscoring increasing investment, technological maturity, and a growing confidence in the commercialization of highly automated vehicles. This rapid growth is primarily fueled by advancements in artificial intelligence, sensor technology, and high-performance computing, which collectively make L4 capabilities increasingly feasible and reliable. The forecast suggests that L4 technology will transition from niche pilot projects to broader commercial applications, particularly within controlled environments and designated operational design domains (ODDs).

A key takeaway from the market forecast is the accelerating pace of innovation and the strategic positioning of major industry players. The substantial increase in market valuation by the end of the forecast period highlights the immense economic potential and transformative impact L4 autonomous driving is expected to have on various industries, including logistics, ride-sharing, and public transportation. This growth is not merely technological but also reflects a changing regulatory landscape that is gradually becoming more accommodating, along with increasing public awareness and potential acceptance of these advanced systems. Stakeholders are recognizing the long-term benefits in terms of safety, efficiency, and new business models, driving continued investment and development efforts that will underpin this impressive market expansion.

- Robust market expansion projected, driven by technological advancements and strategic investments.

- Significant economic opportunities arising from new mobility services and efficiency gains across industries.

- Increasing maturity of core L4 technologies including AI, sensors, and high-performance computing.

- Growing confidence in the commercial viability of L4 applications, especially in specific operational design domains.

- Evolving regulatory frameworks are facilitating broader deployment and testing.

- Collaborations and partnerships are accelerating development and market entry.

- The market is transitioning from research and development to pilot and commercial deployment phases.

L4 Autonomou Driving Market Drivers Analysis

The L4 autonomous driving market is propelled by a convergence of technological advancements, evolving regulatory support, and increasing demand for enhanced safety and efficiency in transportation. Governments and private entities worldwide are investing heavily in smart city initiatives and intelligent transportation systems, which inherently require sophisticated autonomous capabilities. The push for reduced traffic congestion, lower carbon emissions, and improved road safety also acts as a significant catalyst, as L4 vehicles are engineered to mitigate human error, which is a leading cause of accidents. Furthermore, the development of robust 5G infrastructure and V2X communication technologies is providing the necessary connectivity backbone for L4 systems to operate effectively and interact with their environment.

The growing demand for mobility-as-a-service (MaaS) solutions, particularly robotaxi fleets and autonomous shuttles, is another potent driver. These services promise reduced operational costs, increased vehicle utilization, and greater accessibility, particularly in urban areas. Companies are increasingly recognizing the potential for significant cost savings in logistics and last-mile delivery through autonomous trucking and delivery vehicles. As sensor technology, artificial intelligence, and computing power become more affordable and sophisticated, the overall development and deployment costs of L4 systems are gradually becoming more economically viable, encouraging further investment and adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Advancements (AI, Sensors, Computing) | +7.5% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Increasing Focus on Road Safety and Efficiency | +6.0% | Global | Mid to Long-term (2027-2033) |

| Growth of Mobility-as-a-Service (MaaS) and Robotaxis | +5.5% | Urban centers, developed economies (US, China, Europe) | Short to Mid-term (2025-2029) |

| Supportive Regulatory Frameworks and Policies | +4.0% | North America, Europe, parts of Asia | Mid to Long-term (2026-2033) |

| Investment in Smart City Infrastructure and 5G | +3.5% | Global, specifically China, South Korea, EU, US | Mid-term (2025-2030) |

L4 Autonomou Driving Market Restraints Analysis

Despite the immense potential, the L4 autonomous driving market faces significant restraints that could temper its growth trajectory. The most prominent barrier is the exorbitant cost associated with the research, development, testing, and deployment of L4 systems. The integration of advanced sensors like LiDAR, high-performance computing platforms, and sophisticated software stacks significantly increases the overall vehicle cost, making widespread consumer adoption challenging in the initial phases. Furthermore, the extensive validation and verification processes required to ensure safety and reliability for L4 systems are capital-intensive and time-consuming, prolonging market entry for new solutions.

Another major restraint is the complex and fragmented regulatory landscape across different jurisdictions. A lack of uniform international standards for testing, certification, and liability poses a considerable hurdle for global deployment and scalability. Public apprehension and trust issues also represent a significant restraint; concerns about safety, cybersecurity vulnerabilities, and the ethical implications of autonomous decision-making can hinder consumer acceptance and adoption. High-profile incidents, even if rare, tend to erode public confidence, requiring extensive efforts in public education and robust safety assurances. Lastly, the inherent technical complexity, including the challenges of handling unpredictable real-world scenarios, adverse weather conditions, and nuanced human behavior, continues to demand extensive R&D resources, further impacting development timelines and costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development & Deployment Costs | -5.0% | Global | Short to Mid-term (2025-2029) |

| Complex & Fragmented Regulatory Landscape | -4.5% | Global, particularly across multiple nations | Mid-term (2026-2031) |

| Public Acceptance and Trust Issues | -4.0% | Global, particularly in early adoption markets | Mid to Long-term (2027-2033) |

| Cybersecurity Risks and Data Privacy Concerns | -3.5% | Global | Ongoing |

| Infrastructure Readiness and Digital Mapping Limitations | -3.0% | Developing regions, some urban areas | Mid to Long-term (2028-2033) |

L4 Autonomou Driving Market Opportunities Analysis

The L4 autonomous driving market presents a myriad of opportunities for innovation, market expansion, and economic growth. A significant opportunity lies in the burgeoning market for specialized L4 services beyond personal vehicle ownership, such as autonomous ride-hailing fleets, last-mile delivery solutions, and long-haul trucking. These applications offer compelling economic benefits through optimized fleet utilization, reduced labor costs, and enhanced logistical efficiency, making them attractive for commercial operators and logistics companies. The demand for safer and more accessible transportation options in underserved or rural areas also opens up new avenues for L4 shuttle services, potentially revolutionizing public transport.

Furthermore, the development of robust, scalable software platforms and AI solutions specifically for L4 autonomy creates significant opportunities for technology providers. As hardware components become more commoditized, the value shifts towards proprietary software, advanced algorithms, and data ecosystems. Cross-industry collaborations, involving technology firms, automotive OEMs, urban planners, and telecommunications providers, are crucial for building a comprehensive L4 ecosystem and unlocking new business models. Emerging economies, particularly in Asia Pacific, represent a vast untapped market where L4 autonomous solutions could address unique transportation challenges and rapidly develop smart infrastructure, offering immense long-term growth potential once initial deployment hurdles are overcome and regulatory frameworks mature.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Commercial Mobility (Robotaxis, Logistics) | +6.0% | Global, especially urban centers and logistics hubs | Short to Mid-term (2025-2030) |

| Development of Software Platforms & AI Solutions | +5.5% | Global, particularly tech innovation hubs (US, China, Europe) | Ongoing |

| Creation of New Business Models (MaaS, Data Services) | +5.0% | Global | Mid-term (2027-2032) |

| Addressing Transportation Gaps in Emerging Markets | +4.0% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2029-2033) |

| Synergies with Smart City and IoT Ecosystems | +3.5% | Global | Mid to Long-term (2028-2033) |

L4 Autonomou Driving Market Challenges Impact Analysis

The L4 autonomous driving market faces formidable challenges that demand innovative solutions and persistent effort from all stakeholders. A critical challenge is achieving absolute reliability and safety in all conceivable operational design domains (ODDs), including adverse weather conditions, complex urban environments, and handling unpredictable human behavior. The immense complexity of verifying and validating autonomous systems, particularly for rare but critical edge cases, requires billions of miles of testing, much of which must be done in simulation, posing a significant technological and computational hurdle. Another major concern is the ethical dilemma and legal liability in the event of an accident involving an autonomous vehicle. Determining responsibility among the vehicle manufacturer, software provider, sensor supplier, and even the vehicle owner remains a complex issue that requires clear legislative frameworks.

Furthermore, securing L4 systems against cyber threats is paramount. As these vehicles become highly connected and rely on sophisticated software, they present attractive targets for malicious actors, necessitating continuous investment in robust cybersecurity measures to prevent hacking and data breaches. Building and maintaining public trust and acceptance is an ongoing challenge, influenced by media portrayal, accident narratives, and perceived risks. Overcoming skepticism and fostering confidence will require transparent communication, proven safety records, and effective public education campaigns. Finally, the development of comprehensive, high-definition digital maps for everywhere L4 vehicles might operate, along with the necessary physical infrastructure adjustments (e.g., smart roads, dedicated lanes), represents a vast and expensive undertaking, particularly for widespread deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Absolute Safety and Reliability (Edge Cases) | -6.0% | Global | Ongoing |

| Ethical Dilemmas and Legal Liability Frameworks | -5.5% | Global, particularly legal jurisdictions | Mid to Long-term (2027-2033) |

| Cybersecurity Threats and Data Privacy Protection | -5.0% | Global | Ongoing |

| Building and Maintaining Public Trust and Acceptance | -4.5% | Global | Mid to Long-term (2026-2033) |

| Development of Comprehensive HD Mapping and Infrastructure | -4.0% | Global, varies by region's development status | Long-term (2028-2033) |

L4 Autonomou Driving Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the L4 Autonomous Driving market, covering key market dynamics, segmentation, regional trends, and competitive landscape. The report delivers actionable insights into market size, growth drivers, restraints, opportunities, and challenges affecting the industry from 2019 to 2033. It highlights the impact of emerging technologies, such as advanced AI and V2X communication, on market evolution and projects future market valuations based on current and anticipated trends. The study also features profiles of leading market participants, offering a holistic view of the competitive environment and strategic initiatives undertaken by key players to maintain market position and foster innovation.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.2 Billion |

| Market Forecast in 2033 | USD 149.5 Billion |

| Growth Rate | 28.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Waymo, Cruise, Mobileye, Baidu, Pony.ai, Aurora, Nuro, Aptiv, Bosch, Continental AG, ZF Friedrichshafen AG, Valeo, Nvidia, Qualcomm, Intel, Hyundai Mobis, Magna International, Daimler Truck AG, Volvo Group, Toyota |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The L4 autonomous driving market is meticulously segmented to provide a granular understanding of its diverse components, vehicle applications, and end-use sectors. This comprehensive segmentation allows for a detailed analysis of market dynamics within each category, identifying specific growth opportunities and competitive landscapes. The component segment highlights the critical hardware and software technologies underpinning L4 systems, ranging from advanced sensors to sophisticated AI algorithms. The vehicle type segmentation differentiates between passenger cars, various commercial vehicles like trucks and buses, and specialized autonomous platforms such as robotaxis and shuttles, each with unique market trajectories and deployment challenges.

Furthermore, the market is segmented by application, which provides insight into the primary commercial and operational uses of L4 technology. This includes ride-hailing services, which are proving to be a key early commercialization pathway, as well as logistics and last-mile delivery, where autonomous solutions promise significant efficiency gains. Public transportation and personal mobility also represent significant application areas that are expected to evolve with the increasing maturity of L4 technology. This multi-faceted segmentation ensures that stakeholders can pinpoint specific areas of growth, understand value chain dynamics, and tailor their strategies to target the most promising market niches within the rapidly expanding L4 autonomous driving ecosystem.

- By Component:

- Hardware: Lidar, Radar, Camera, Ultrasonic Sensors, GPS/GNSS, Inertial Measurement Units (IMU)

- Software: Perception, Localization, Path Planning, Control Systems, Operating Systems

- Services: Mapping, Connectivity, Over-the-Air (OTA) Updates, Maintenance, Data Management

- By Vehicle Type:

- Passenger Cars

- Commercial Vehicles: Trucks, Buses

- Robo-taxis

- Shuttles

- By Application:

- Ride-Hailing

- Logistics and Last-Mile Delivery

- Public Transportation

- Personal Mobility

- Others (e.g., Agriculture, Mining, Specialized Industrial Vehicles)

Regional Highlights

- North America: Positioned as a leading market for L4 autonomous driving due to significant investments in R&D, supportive regulatory sandboxes, a robust tech ecosystem, and the presence of major autonomous vehicle companies. The region is characterized by extensive testing and early commercial deployment of robotaxi services in cities like Phoenix and San Francisco.

- Europe: Demonstrating strong progress with initiatives focused on smart infrastructure, cross-border autonomous driving corridors, and high standards for vehicle safety and cybersecurity. Countries like Germany, France, and the UK are actively developing legislation and conducting trials, emphasizing passenger safety and data privacy.

- Asia Pacific (APAC): Expected to be the fastest-growing market, driven by substantial government support, rapid urbanization, massive investments in smart city projects, and a large consumer base. China is a prominent leader with ambitious national strategies and numerous companies aggressively developing and deploying L4 autonomous fleets, particularly in ride-hailing and logistics. Japan and South Korea are also making significant strides in technology development and infrastructure readiness.

- Latin America: An emerging market with growing interest in autonomous transportation solutions to address urban mobility challenges. While currently lagging in widespread L4 deployment, increasing foreign investment and local pilot programs are paving the way for future growth, particularly in select urban centers.

- Middle East and Africa (MEA): Gradually adopting L4 autonomous driving technologies, particularly in countries with smart city visions like the UAE and Saudi Arabia. These regions are investing in innovative transportation solutions to diversify their economies and enhance urban living, though widespread adoption faces challenges related to infrastructure and regulatory development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the L4 Autonomou Driving Market.- Waymo

- Cruise

- Mobileye

- Baidu

- Pony.ai

- Aurora

- Nuro

- Aptiv

- Bosch

- Continental AG

- ZF Friedrichshafen AG

- Valeo

- Nvidia

- Qualcomm

- Intel

- Hyundai Mobis

- Magna International

- Daimler Truck AG

- Volvo Group

- Toyota

Frequently Asked Questions

Analyze common user questions about the L4 Autonomou Driving market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is L4 Autonomous Driving?

L4 autonomous driving, or Level 4 autonomy, refers to a vehicle's ability to perform all driving tasks and monitor the driving environment independently under specific conditions, known as its operational design domain (ODD). Within this ODD, the vehicle requires no human intervention for driving, meaning a human driver is not expected to take control. If the vehicle exits its ODD, it will perform a minimal risk maneuver, such as safely pulling over.

What are the primary benefits of L4 autonomous driving?

The key benefits of L4 autonomous driving include significantly enhanced road safety by reducing human error, increased traffic efficiency through optimized flow and reduced congestion, and improved accessibility for individuals unable to drive. Additionally, it offers potential for substantial cost savings in commercial applications like logistics and ride-hailing due to reduced labor costs and optimized fleet utilization.

What are the main challenges to widespread L4 adoption?

Key challenges for widespread L4 adoption include the high costs of development and deployment, the complexities of ensuring absolute safety and reliability in all scenarios, the lack of a uniform global regulatory framework, and significant public trust issues. Cybersecurity risks and the need for extensive, high-definition digital mapping also pose substantial hurdles.

When is L4 autonomous driving expected to be widely available?

While L4 autonomous vehicles are currently operating in limited commercial capacities (e.g., robotaxi services in select cities), widespread availability for personal ownership is anticipated to be a more gradual process. Commercial applications in geofenced areas, such as logistics and public shuttles, are expected to scale more rapidly within the next 5-10 years, with broader consumer adoption extending into the 2030s as technology matures and regulatory environments evolve.

How does AI contribute to L4 autonomous driving?

Artificial intelligence is fundamental to L4 autonomous driving, enabling vehicles to perceive their environment, make complex decisions, and control vehicle movements. AI algorithms power sensor fusion for accurate object detection, predictive analytics for anticipating traffic behavior, and path planning for safe navigation. Advanced AI models, including deep learning, allow the vehicle to learn from vast datasets and adapt to diverse driving conditions, significantly enhancing the system's robustness and intelligence.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted