Solar Panel Adhesive Market

Solar Panel Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702167 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

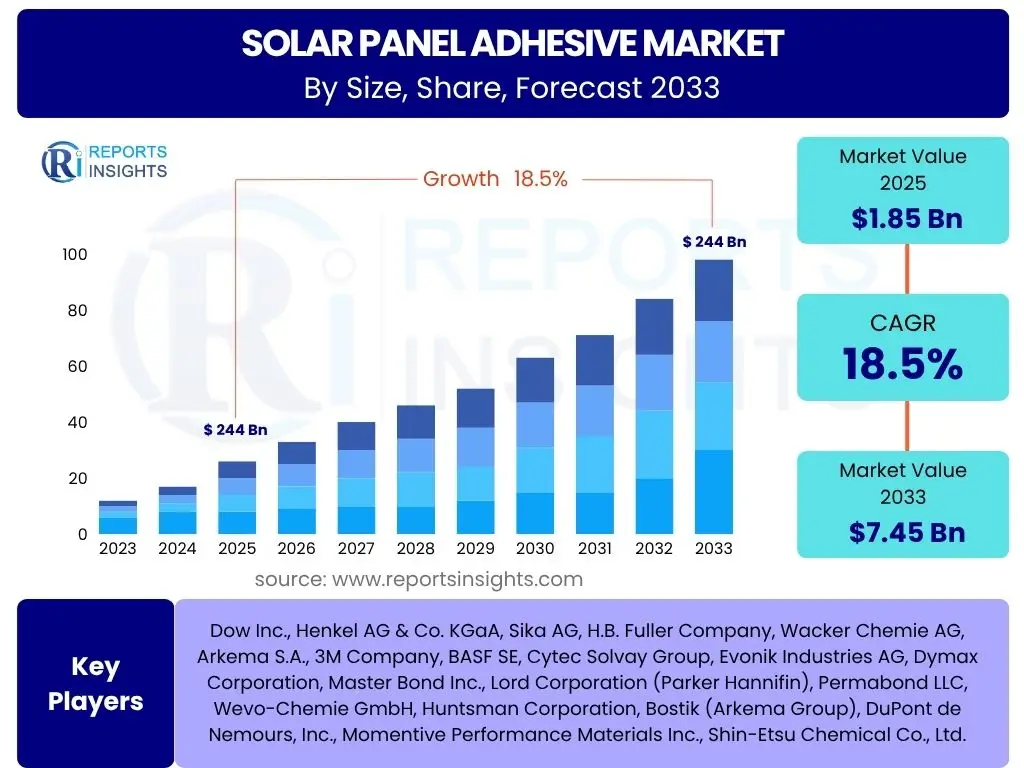

Solar Panel Adhesive Market Size

According to Reports Insights Consulting Pvt Ltd, The Solar Panel Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 1.85 billion in 2025 and is projected to reach USD 7.45 billion by the end of the forecast period in 2033. This significant growth trajectory is primarily driven by the escalating global demand for renewable energy sources and the continuous advancements in solar panel technology, which necessitate high-performance and durable adhesive solutions for enhanced longevity and efficiency of photovoltaic modules.

Key Solar Panel Adhesive Market Trends & Insights

User queries regarding the solar panel adhesive market frequently center on advancements in material science, the adoption of sustainable practices, and innovations in application technologies. A prominent trend involves the development of bio-based and environmentally friendly adhesives, driven by stringent environmental regulations and a growing industry commitment to sustainability. Manufacturers are increasingly investing in research and development to produce adhesives with reduced volatile organic compound (VOC) emissions and improved recyclability, aligning with the broader green energy transition. This shift addresses not only ecological concerns but also enhances worker safety during manufacturing and installation processes.

Another significant trend is the increasing demand for high-performance adhesives capable of withstanding extreme environmental conditions, including wide temperature fluctuations, high humidity, and prolonged UV exposure. This is crucial for ensuring the long-term durability and reliability of solar panels, particularly in diverse geographical regions from arid deserts to coastal areas. Furthermore, the integration of smart functionalities into adhesives, such as self-healing properties or real-time performance monitoring capabilities, represents an emerging area of interest. These innovations aim to extend the operational life of solar panels and minimize maintenance requirements, offering substantial cost savings over their lifecycle.

The market is also witnessing a trend towards specialized adhesives tailored for different solar panel technologies, including crystalline silicon, thin-film, and emerging perovskite solar cells. This customization ensures optimal bonding, thermal management, and electrical insulation properties specific to each panel type, thereby maximizing energy conversion efficiency. The focus on automation in solar panel manufacturing is simultaneously driving demand for adhesives that are compatible with high-speed, robotic application systems, leading to increased production efficiency and reduced labor costs. This move towards industrial-scale application methods is transforming the production landscape for solar modules globally.

- Emphasis on bio-based and low-VOC adhesive formulations.

- Development of high-performance adhesives for extreme weather conditions.

- Integration of smart features like self-healing and performance monitoring.

- Specialized adhesives for diverse solar panel technologies (e.g., crystalline, thin-film).

- Adoption of automation-compatible adhesives for high-speed manufacturing.

AI Impact Analysis on Solar Panel Adhesive

Common user questions regarding AI's influence on the solar panel adhesive sector primarily focus on its potential to optimize material composition, enhance quality control processes, and streamline manufacturing efficiency. Artificial intelligence, particularly machine learning algorithms, offers unparalleled capabilities in analyzing vast datasets related to material properties, environmental stress factors, and adhesive performance. This enables researchers to predict optimal adhesive formulations for specific applications, accelerating the discovery and development of new, more durable, and efficient adhesive solutions. AI-driven simulations can test various chemical combinations and bonding scenarios virtually, significantly reducing the time and cost associated with traditional physical experimentation.

In terms of manufacturing, AI is poised to revolutionize quality assurance and production line optimization. Computer vision systems powered by AI can detect microscopic defects in adhesive application or curing processes with far greater precision and speed than human inspection, ensuring consistent quality across large-scale production runs. Predictive maintenance models, leveraging AI, can analyze sensor data from adhesive dispensing equipment to anticipate potential failures or inconsistencies, allowing for proactive adjustments and minimizing downtime. This operational intelligence contributes to higher throughput and reduced material waste, which are critical for cost-effective solar panel manufacturing.

Beyond material science and manufacturing, AI also impacts supply chain management for solar panel adhesives. AI-driven predictive analytics can forecast demand fluctuations for various adhesive types, optimize inventory levels, and identify potential disruptions in raw material supply. This improves supply chain resilience and ensures timely availability of critical components, directly supporting the rapid expansion of solar energy projects worldwide. The integration of AI tools across the value chain, from R&D to deployment, is transforming the adhesive industry into a more agile, responsive, and innovative sector, driving continuous improvement in solar panel reliability and performance.

- AI-driven optimization of adhesive material composition and formulation.

- Enhanced quality control and defect detection using AI-powered computer vision.

- Predictive maintenance for adhesive manufacturing equipment.

- Supply chain optimization and demand forecasting for adhesive raw materials.

- Acceleration of R&D cycles for novel adhesive technologies.

Key Takeaways Solar Panel Adhesive Market Size & Forecast

User inquiries about key takeaways from the solar panel adhesive market size and forecast consistently highlight the robust growth prospects, the critical role of technological innovation, and the increasing strategic importance of adhesive solutions in the renewable energy ecosystem. A primary insight is the market's substantial Compound Annual Growth Rate, driven by global commitments to decarbonization and the burgeoning installation of photovoltaic systems across residential, commercial, and utility-scale projects. This growth underscores the essential nature of adhesives in ensuring the structural integrity, electrical insulation, and environmental sealing of solar panels, directly impacting their long-term performance and energy yield.

Another crucial takeaway is the pervasive influence of advanced material science and engineering on market expansion. The demand for adhesives that offer superior thermal stability, UV resistance, moisture barriers, and electrical properties is continuously rising as solar panel designs become more sophisticated and operate in increasingly diverse climatic conditions. Innovations in curing mechanisms, such as UV-curable or dual-cure adhesives, are also instrumental in improving manufacturing efficiency and reducing production cycle times, making the assembly of solar modules faster and more cost-effective. These technological advancements are not merely incremental but represent foundational shifts that enable next-generation solar technologies.

Furthermore, the market forecast reflects a growing awareness among solar panel manufacturers of the long-term value provided by high-quality adhesives. While initial cost might be a consideration, the emphasis has shifted towards total cost of ownership, where durable adhesives significantly reduce maintenance needs and extend the lifespan of panels, thereby enhancing return on investment for end-users. This perspective change positions adhesives not just as a component but as a strategic enabler of reliability and efficiency in the solar energy sector. Regional growth disparities are also a key takeaway, with Asia Pacific expected to remain a dominant force, supported by aggressive solar capacity expansion targets and supportive government policies.

- Strong market growth driven by global solar energy expansion.

- Technological advancements in adhesives are critical for panel performance.

- Focus on long-term durability and efficiency over initial material cost.

- Adhesives are key enablers for next-generation solar panel designs.

- Asia Pacific maintains significant market dominance and growth potential.

Solar Panel Adhesive Market Drivers Analysis

The solar panel adhesive market is propelled by several robust drivers, fundamentally rooted in the global energy transition and technological innovation within the photovoltaic sector. A primary driver is the accelerating deployment of solar energy capacity worldwide, spurred by climate change concerns, government incentives, and decreasing solar power generation costs. As more solar farms and rooftop installations are commissioned, the demand for reliable and high-performance adhesives, essential for the structural integrity and sealing of modules, naturally increases. This expansion is evident across all scales, from utility-scale projects requiring thousands of modules to residential and commercial installations, each demanding precision-engineered adhesive solutions.

Another significant driver is the continuous advancement in solar panel technology itself, leading to higher efficiency modules and new form factors such as flexible, transparent, and building-integrated photovoltaics (BIPV). These innovations often require specialized adhesive solutions that can bond diverse materials, withstand varied stresses, and maintain performance under challenging conditions. For instance, flexible solar panels necessitate highly elastic and durable adhesives, while BIPV applications demand strong adhesion to construction materials and aesthetic integration. The drive for higher power output from smaller module footprints also puts increased thermal and mechanical stress on components, elevating the need for advanced adhesive materials.

Moreover, supportive government policies and regulatory frameworks globally are fostering a conducive environment for market growth. These include feed-in tariffs, tax credits, renewable energy mandates, and subsidies for solar installations, which directly stimulate demand for solar panels and, consequently, for their adhesive components. The growing emphasis on environmental sustainability and the push for "green" manufacturing processes also favor adhesives with lower VOC content and improved recyclability, prompting manufacturers to innovate. This combination of policy support, technological evolution, and environmental consciousness creates a strong positive feedback loop for the solar panel adhesive market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Solar Panel Installations | +2.1% | Global, particularly Asia Pacific, North America, Europe | Short to Long-Term (2025-2033) |

| Advancements in PV Technology & Module Design | +1.8% | Global, with innovation hubs in China, Germany, USA | Mid to Long-Term (2026-2033) |

| Favorable Government Policies & Incentives for Renewables | +1.5% | Europe, USA, India, China | Short to Mid-Term (2025-2030) |

| Growing Demand for High-Efficiency & Durable Panels | +1.3% | Global, especially high-end segments | Mid to Long-Term (2027-2033) |

| Focus on Sustainable & Environmentally Friendly Adhesives | +0.9% | Europe, North America, Japan | Mid to Long-Term (2028-2033) |

Solar Panel Adhesive Market Restraints Analysis

Despite robust growth prospects, the solar panel adhesive market faces several notable restraints that could temper its expansion. One significant challenge is the volatility in raw material prices, particularly for petrochemical-derived components that form the base of many high-performance adhesives. Fluctuations in crude oil prices, coupled with supply chain disruptions exacerbated by geopolitical events or natural disasters, can directly impact the manufacturing costs of adhesives. This instability can lead to increased production expenses for adhesive manufacturers, which are then often passed on to solar panel manufacturers, potentially affecting the overall cost-competitiveness of solar energy. Such price unpredictability can hinder long-term planning and investment within the adhesive supply chain.

Another restraint is the relatively high initial cost associated with advanced, specialized adhesives compared to conventional bonding methods or lower-grade alternatives. While these high-performance adhesives offer superior durability, efficiency, and longevity for solar panels, the upfront investment can be a deterrent for some manufacturers, particularly in cost-sensitive markets or for projects with tighter budget constraints. There is often a trade-off between the immediate cost of materials and the long-term benefits in terms of panel performance and reduced maintenance. Educating the market on the total cost of ownership and the long-term value proposition of premium adhesives remains a critical challenge for market penetration.

Furthermore, the lack of standardized testing protocols and performance benchmarks for solar panel adhesives across different regions can create market inefficiencies. Variability in regulatory requirements and certification processes can complicate product development and market entry for global adhesive manufacturers, necessitating costly and time-consuming adaptations for different markets. This fragmentation can slow down the adoption of innovative adhesive solutions, as manufacturers may opt for universally accepted, albeit less optimized, materials to avoid compliance hurdles. Additionally, the limited awareness among some solar panel manufacturers about the critical role of advanced adhesives in overall panel performance and lifespan can also act as a restraint, leading to underinvestment in high-quality bonding solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -0.8% | Global | Short-Term (2025-2027) |

| High Initial Cost of Advanced Adhesives | -0.6% | Emerging Markets, Cost-sensitive regions | Mid-Term (2025-2030) |

| Lack of Standardized Testing & Regulations | -0.4% | Global, specifically developing markets | Mid to Long-Term (2027-2033) |

| Competition from Traditional Fastening Methods | -0.3% | Global, particularly in established markets | Short to Mid-Term (2025-2029) |

| Awareness & Education Gap in Market | -0.2% | Developing Economies | Long-Term (2029-2033) |

Solar Panel Adhesive Market Opportunities Analysis

The solar panel adhesive market presents significant opportunities for growth, driven by evolving solar technologies, expanding geographical markets, and the increasing emphasis on sustainable solutions. A key opportunity lies in the burgeoning market for Building Integrated Photovoltaics (BIPV) and Building Applied Photovoltaics (BAPV). As architectural designs increasingly incorporate solar energy generation, there is a rising demand for adhesives that offer strong structural bonding, weather sealing, and aesthetic integration, allowing solar modules to blend seamlessly with building facades, roofs, and windows. This segment requires specialized adhesive properties such as transparency, flexibility, and long-term durability in varied environmental conditions, opening new avenues for product innovation and market penetration beyond traditional framed panels.

Another substantial opportunity stems from the rapid expansion of solar energy markets in emerging economies, particularly in Asia Pacific, Latin America, and Africa. These regions are actively investing in renewable energy infrastructure to address growing energy demands and improve energy access, often with significant government support. The scale of planned solar projects in countries like India, Vietnam, and various African nations translates into massive demand for solar components, including adhesives. Companies that can offer cost-effective, high-performance adhesive solutions tailored to the specific climatic and economic conditions of these regions stand to gain substantial market share. Furthermore, the increasing adoption of off-grid and mini-grid solar solutions in remote areas also creates demand for robust, easy-to-apply adhesives.

Finally, the growing trend towards developing bio-based, recyclable, and environmentally friendly adhesives represents a strong opportunity for innovation and market differentiation. As environmental regulations tighten and corporate sustainability goals become more ambitious, there is a clear preference for adhesive solutions that minimize environmental impact throughout their lifecycle. Manufacturers investing in green chemistry and sustainable sourcing will find a receptive market, not only due to compliance requirements but also due to enhanced brand reputation and consumer preference. The development of smart adhesives with advanced functionalities, such as self-healing or integrated sensors for performance monitoring, also offers a premium market segment for specialized products, enhancing the long-term value proposition for solar panel manufacturers and asset owners.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Building Integrated Photovoltaics (BIPV) | +1.6% | Europe, North America, Japan, parts of Asia Pacific | Mid to Long-Term (2026-2033) |

| Emerging Markets Expansion (Asia, LatAm, Africa) | +1.4% | India, Southeast Asia, Brazil, South Africa | Short to Long-Term (2025-2033) |

| Development of Bio-based & Eco-friendly Adhesives | +1.2% | Europe, North America, Global sustainable markets | Mid to Long-Term (2027-2033) |

| Demand for Flexible & Lightweight Solar Panels | +1.0% | Global, specific niche applications | Long-Term (2028-2033) |

| Aftermarket & Repair Services for Existing Installations | +0.8% | Mature Solar Markets (Germany, Japan, USA) | Mid to Long-Term (2027-2033) |

Solar Panel Adhesive Market Challenges Impact Analysis

The solar panel adhesive market, while promising, contends with several critical challenges that demand strategic navigation. One primary challenge is ensuring long-term durability and performance in harsh environmental conditions. Solar panels are exposed to extreme temperatures, high humidity, UV radiation, and mechanical stresses for decades, and adhesives must maintain their integrity without degradation. Achieving this sustained performance requires advanced material science and rigorous testing, as adhesive failures can lead to delamination, moisture ingress, and significant power loss in solar modules. The development of adhesives that can reliably withstand these varied and prolonged stresses over a 25-year panel lifespan remains a continuous research and development hurdle.

Another significant challenge is the intense competition from alternative bonding and sealing methods, such as mechanical fasteners or traditional sealants. While adhesives offer advantages in terms of uniform stress distribution, aesthetic appeal, and streamlined manufacturing processes, some manufacturers may still opt for conventional methods due to established practices, lower perceived initial costs, or lack of awareness about the benefits of advanced adhesives. Overcoming this inertia requires effective market education and demonstration of the superior total cost of ownership that high-performance adhesives provide through enhanced panel longevity and reduced maintenance needs. Demonstrating clear return on investment is crucial for broader adoption.

Furthermore, managing the complexity of global supply chains for specialized chemical raw materials poses a substantial challenge. The production of advanced adhesives often relies on a diverse range of chemicals sourced from various parts of the world, making the supply chain vulnerable to geopolitical tensions, trade disputes, and logistics disruptions. Any interruption can lead to material shortages, increased lead times, and significant cost escalations for adhesive manufacturers, directly impacting their ability to meet demand from the rapidly growing solar industry. Ensuring a resilient and diversified supply chain, potentially through regional sourcing or strategic partnerships, is essential to mitigate these risks and maintain stable production and pricing.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Long-Term Durability in Harsh Climates | -0.7% | Global, particularly extreme climate zones | Long-Term (2028-2033) |

| Competition from Alternative Bonding Methods | -0.5% | Global, particularly established markets | Short to Mid-Term (2025-2029) |

| Supply Chain Disruptions for Raw Materials | -0.4% | Global | Short-Term (2025-2027) |

| Disposal & Recycling Challenges of End-of-Life Panels | -0.3% | Europe, Japan, evolving global regulations | Long-Term (2030-2033) |

| Compliance with Evolving Environmental Regulations | -0.2% | Europe, North America, developed economies | Mid to Long-Term (2027-2033) |

Solar Panel Adhesive Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global solar panel adhesive market, offering a detailed segmentation, regional insights, competitive landscape, and future growth projections. It encapsulates market sizing, key trends, drivers, restraints, opportunities, and challenges, along with the transformative impact of artificial intelligence. The report aims to equip stakeholders with actionable intelligence for strategic decision-making in this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 7.45 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Dow Inc., Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, Wacker Chemie AG, Arkema S.A., 3M Company, BASF SE, Cytec Solvay Group, Evonik Industries AG, Dymax Corporation, Master Bond Inc., Lord Corporation (Parker Hannifin), Permabond LLC, Wevo-Chemie GmbH, Huntsman Corporation, Bostik (Arkema Group), DuPont de Nemours, Inc., Momentive Performance Materials Inc., Shin-Etsu Chemical Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The solar panel adhesive market is comprehensively segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for precise analysis of market dynamics, growth drivers, and opportunities across various adhesive types, applications, module technologies, end-use industries, and forms. Understanding these segments is crucial for manufacturers to tailor their product offerings, for investors to identify high-growth areas, and for policymakers to formulate supportive strategies for the solar energy ecosystem.

- By Resin Type: This segment includes different chemical compositions of adhesives.

- Silicone: Known for excellent weatherability, UV resistance, and flexibility.

- Epoxy: Offers strong adhesion, chemical resistance, and rigidity.

- Polyurethane: Valued for flexibility, adhesion to various substrates, and toughness.

- Acrylic: Provides good adhesion, UV resistance, and quick curing.

- Others: Includes hybrid formulations and emerging adhesive chemistries.

- By Application: Focuses on where the adhesive is used within the solar panel.

- Junction Box Bonding: Securing the electrical enclosure to the module backsheet.

- Frame Bonding: Adhering the frame to the glass and backsheet.

- Encapsulation: Protecting sensitive components from moisture and environmental damage.

- Rail Bonding: Attaching mounting rails or brackets to the module.

- Edge Sealing: Sealing the perimeter of the panel for moisture and dust protection.

- Others: Miscellaneous applications like structural bonding in BIPV.

- By Module Type: Categorizes adhesives based on the type of photovoltaic module.

- Crystalline Silicon: Adhesives for traditional monocrystalline and polycrystalline panels.

- Thin Film: Specialized adhesives for flexible, transparent, or lightweight thin-film modules.

- Perovskite: Adhesives engineered for emerging, high-efficiency perovskite solar cells.

- Others: Includes multi-junction cells and other niche module types.

- By End-Use Industry: Identifies the primary market where solar panels are deployed.

- Residential: Rooftop installations on homes.

- Commercial: Solar systems for businesses, offices, and retail spaces.

- Industrial: Large-scale installations for industrial facilities and warehouses.

- Utility-Scale: Massive solar farms generating power for grids.

- Automotive: Solar integration in vehicles (e.g., solar car roofs).

- Others: Includes aerospace, marine, and portable power applications.

- By Form: Describes the physical state in which the adhesive is applied.

- Liquid: Flowable adhesives applied by dispensing.

- Paste: Viscous adhesives, often dispensed or screen-printed.

- Film: Pre-formed adhesive layers, typically heat-activated.

- Tape: Adhesive in tape form for easy application.

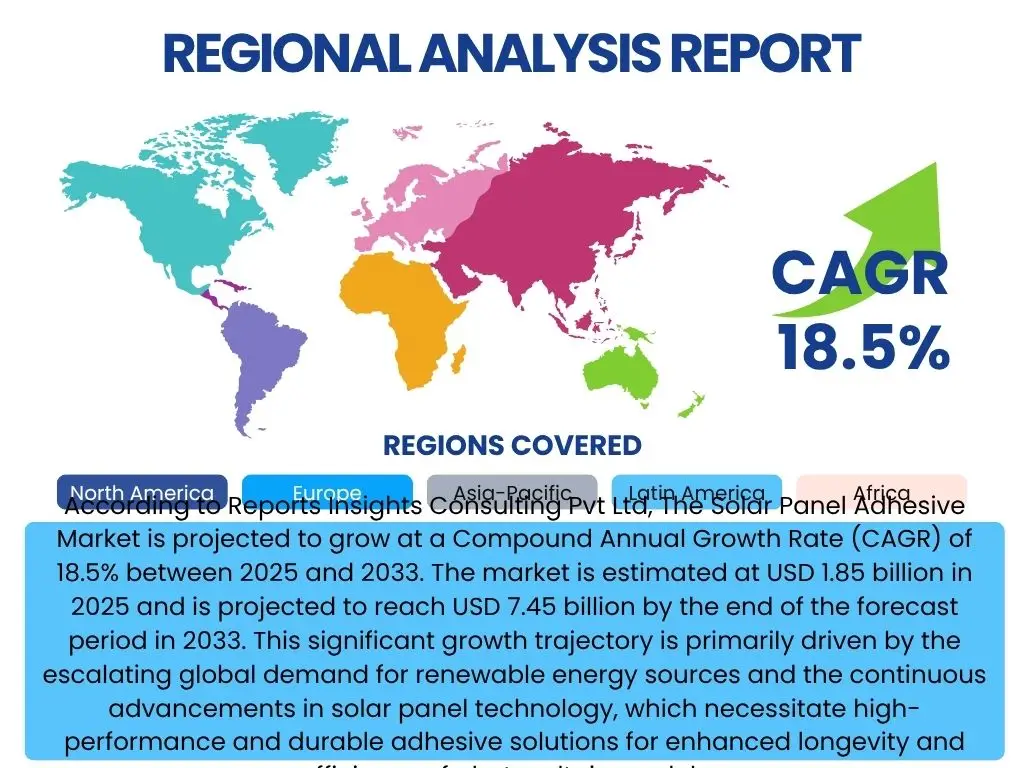

Regional Highlights

- Asia Pacific (APAC): Dominates the global solar panel adhesive market due to its robust solar panel manufacturing base, particularly in China, which is the world's largest producer and installer of solar energy. Countries like India, Vietnam, and South Korea are also rapidly expanding their solar capacities, driving immense demand for adhesives. Government incentives and ambitious renewable energy targets further accelerate market growth in this region.

- Europe: A mature market for solar energy, characterized by stringent environmental regulations and a strong focus on sustainable and eco-friendly adhesive solutions. Germany, Spain, and France are leading the transition towards cleaner energy, with significant investments in both traditional and innovative solar applications, including BIPV, creating demand for high-performance, compliant adhesives.

- North America: Driven by increasing solar installations in the United States, propelled by federal tax credits and state-level renewable energy mandates. The demand for durable and high-quality adhesives is high, especially for utility-scale projects and for ensuring longevity in diverse climates. Canada is also steadily growing its solar energy infrastructure.

- Latin America: Emerging as a significant growth region, with countries like Brazil, Mexico, and Chile investing heavily in solar power to meet rising energy demands and diversify their energy mix. The market here is characterized by a growing need for cost-effective yet reliable adhesive solutions for large-scale solar farms.

- Middle East and Africa (MEA): Poised for substantial growth, particularly in countries like UAE, Saudi Arabia, and South Africa, which are leveraging their abundant solar resources. Large-scale government projects and a push for economic diversification are driving solar adoption, necessitating adhesives that can withstand extreme desert climates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Solar Panel Adhesive Market.- Dow Inc.

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Wacker Chemie AG

- Arkema S.A.

- 3M Company

- BASF SE

- Cytec Solvay Group

- Evonik Industries AG

- Dymax Corporation

- Master Bond Inc.

- Lord Corporation (Parker Hannifin)

- Permabond LLC

- Wevo-Chemie GmbH

- Huntsman Corporation

- Bostik (Arkema Group)

- DuPont de Nemours, Inc.

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

Frequently Asked Questions

What is the projected growth rate of the Solar Panel Adhesive Market?

The Solar Panel Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033, driven by increasing global solar energy adoption and advancements in photovoltaic technology.

What are the primary drivers for the Solar Panel Adhesive Market?

Key drivers include the escalating global installation of solar panels, continuous technological advancements in PV modules, and supportive government policies promoting renewable energy investments worldwide.

How does AI impact the Solar Panel Adhesive Market?

AI influences the market by optimizing adhesive material composition, enhancing quality control through computer vision, streamlining manufacturing processes, and improving supply chain efficiency through predictive analytics.

Which regions are leading the demand for solar panel adhesives?

Asia Pacific currently dominates the market due to its extensive manufacturing base and rapid solar energy expansion, with Europe and North America also showing significant demand due to high adoption rates and regulatory support.

What are the key segments within the Solar Panel Adhesive Market?

The market is segmented by resin type (e.g., silicone, epoxy), application (e.g., junction box bonding, encapsulation), module type (e.g., crystalline silicon, thin film), end-use industry (e.g., residential, utility-scale), and form (e.g., liquid, paste).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted