Packaging Adhesive Market

Packaging Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703291 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

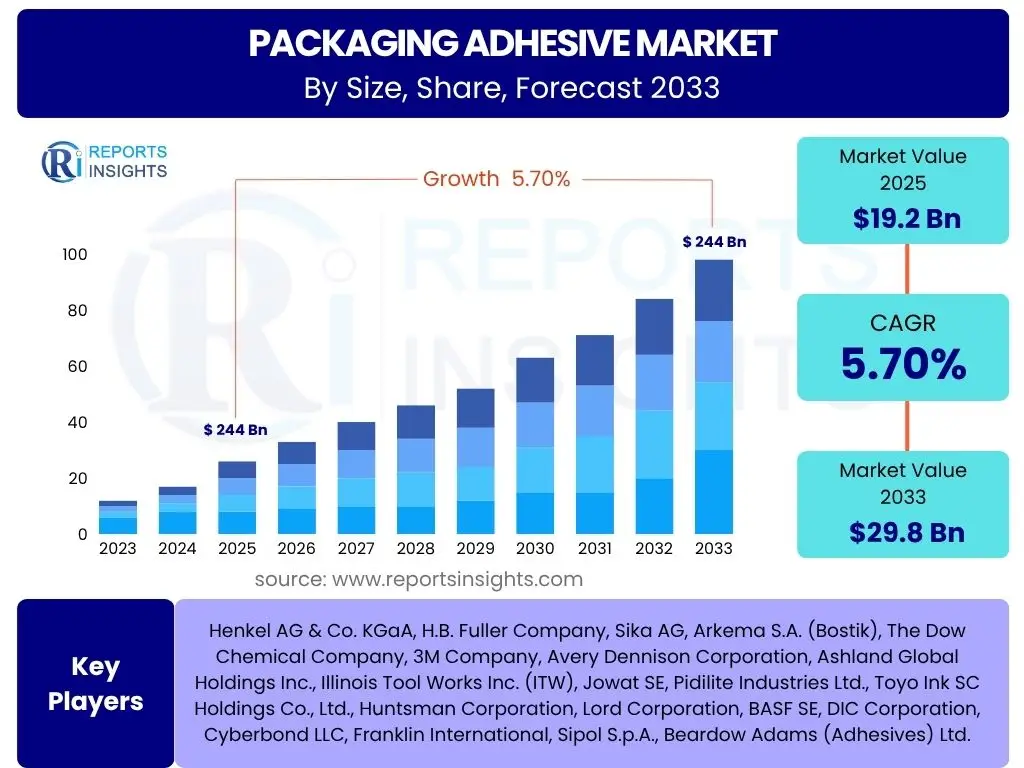

Packaging Adhesive Market Size

According to Reports Insights Consulting Pvt Ltd, The Packaging Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% between 2025 and 2033. The market is estimated at USD 19.2 Billion in 2025 and is projected to reach USD 29.8 Billion by the end of the forecast period in 2033.

Key Packaging Adhesive Market Trends & Insights

User queries frequently highlight sustainability, e-commerce impact, and technological advancements as primary areas of interest within the packaging adhesive market. Consumers and industries are increasingly seeking environmentally benign solutions, driving innovation in bio-based, water-based, and solvent-free adhesive formulations. The rapid expansion of e-commerce, particularly accelerated by global shifts in consumer purchasing habits, mandates robust and efficient packaging solutions, directly impacting the demand for high-performance adhesives capable of withstanding complex logistics and providing tamper-evident features.

Beyond eco-friendliness and e-commerce, the market is witnessing significant shifts due to evolving packaging designs and automation. The rise of flexible packaging, lightweight materials, and diverse substrates requires adhesives with enhanced bonding capabilities and versatility. Furthermore, increasing automation in packaging lines across various industries necessitates adhesives that offer faster setting times, improved machine runnability, and consistent performance, thereby contributing to higher production efficiencies and reduced operational costs. These trends collectively shape the current landscape and future trajectory of the packaging adhesive industry.

- Sustainable Formulations: Growing demand for bio-based, water-based, and solvent-free adhesives to reduce environmental footprint and volatile organic compound (VOC) emissions.

- E-commerce Packaging Growth: Increased need for durable, fast-setting, and secure adhesives for corrugated boxes, flexible mailers, and protective packaging due to the booming online retail sector.

- Flexible Packaging Evolution: Development of specialized adhesives for multi-layer films, stand-up pouches, and other flexible formats requiring strong bond strength, barrier properties, and heat resistance.

- Automation in Packaging Lines: Rising adoption of high-speed automated packaging machinery driving demand for adhesives with rapid cure times, excellent machine runnability, and consistent performance.

- Food Safety and Regulations: Strict global regulations for food contact materials pushing for low-migration, taint-free, and odorless adhesives, ensuring product safety and integrity.

AI Impact Analysis on Packaging Adhesive

Common user questions regarding AI's impact on packaging adhesives often center around its potential to revolutionize product development, manufacturing efficiency, and supply chain management. AI and machine learning algorithms are increasingly being leveraged in research and development to accelerate the discovery of novel adhesive formulations. By analyzing vast datasets of chemical properties, material interactions, and performance characteristics, AI can predict optimal compositions, simulate adhesion behavior under various conditions, and streamline the iterative process of material selection and testing, leading to faster time-to-market for new adhesive solutions.

In manufacturing, AI-driven solutions are enhancing operational efficiency and quality control. Predictive maintenance systems, powered by AI, can monitor adhesive application equipment in real-time, anticipate potential failures, and optimize production schedules, thereby minimizing downtime and waste. Furthermore, AI-enabled vision systems are being deployed for automated quality inspection, ensuring consistent adhesive bead application, bond integrity, and overall package quality at high speeds. This integration of AI not only improves product reliability but also contributes to significant cost savings and increased throughput in the adhesive production and application processes, transforming traditional manufacturing paradigms.

- Accelerated R&D: AI algorithms used for predicting adhesive properties, optimizing formulations, and simulating material interactions, leading to faster development of new products.

- Optimized Manufacturing Processes: AI-driven predictive maintenance for adhesive application equipment, real-time process control, and anomaly detection to enhance efficiency and reduce downtime.

- Enhanced Quality Control: AI-powered vision systems for automated inspection of adhesive application, ensuring consistent bond strength and detecting defects at high production speeds.

- Supply Chain Optimization: AI for demand forecasting, inventory management, and logistics optimization for raw materials and finished adhesive products, improving supply chain resilience.

- Smart Packaging Integration: Potential for AI to inform adhesive choices for smart packaging, facilitating embedding of sensors and RFID tags that require precise bonding.

Key Takeaways Packaging Adhesive Market Size & Forecast

Analysis of user questions concerning the packaging adhesive market size and forecast reveals a consistent interest in understanding the primary growth drivers, the influence of evolving consumer trends, and the geographical distribution of market opportunities. The market's projected growth is largely underpinned by the sustained expansion of packaged goods consumption, particularly in emerging economies, alongside significant shifts towards sustainable and high-performance packaging solutions globally. The increasing penetration of e-commerce continues to be a pivotal factor, demanding adhesives that offer speed, durability, and reliability for diverse packaging formats.

Furthermore, the forecast highlights the critical role of innovation in material science and adhesive chemistry. As industries adopt more complex substrates and pursue lighter, more efficient packaging designs, the demand for specialized, high-performance adhesives with advanced properties (e.g., improved temperature resistance, enhanced adhesion to difficult surfaces, or faster cure times) is intensifying. Regional dynamics indicate Asia Pacific as a significant growth hub due to industrial expansion and population growth, while stringent regulations in North America and Europe drive innovation towards safer and more eco-friendly products, collectively shaping a dynamic and growing market landscape.

- Robust Market Expansion: The packaging adhesive market is set for substantial growth, driven by increasing demand for packaged goods and the global rise of e-commerce.

- Sustainability as a Core Driver: Eco-friendly and bio-based adhesive solutions are gaining significant traction, influencing product development and consumer preference.

- Innovation in Performance: Continuous development of high-performance adhesives tailored for challenging substrates, diverse packaging formats, and automated application processes is crucial.

- Asia Pacific Dominance: The Asia Pacific region is expected to lead market growth due to rapid industrialization, increasing manufacturing activities, and a large consumer base.

- Regulatory Influence: Evolving regulatory landscapes concerning environmental impact and food safety are compelling manufacturers to innovate and comply, shaping market offerings.

Packaging Adhesive Market Drivers Analysis

The packaging adhesive market is experiencing robust growth driven by several key factors. The global proliferation of e-commerce has significantly boosted demand for reliable and efficient packaging solutions, necessitating high-performance adhesives that can ensure package integrity throughout complex supply chains. This trend, coupled with the rising consumption of packaged food, beverages, and consumer goods, particularly in developing economies, continues to fuel the need for various adhesive types to bond diverse packaging materials.

Furthermore, the accelerating adoption of flexible packaging formats due to their convenience, cost-effectiveness, and reduced material usage is a major driver. These innovative packaging designs often require specialized adhesives that can maintain strong bonds on multi-layered films and withstand various environmental conditions. Simultaneously, advancements in packaging machinery and the push for greater automation in manufacturing lines are creating demand for adhesives with rapid setting times and superior machine runnability, thereby enhancing overall production efficiency and throughput across the industry.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth of E-commerce | +1.5% to +2.0% | Global, particularly North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

| Increasing Demand for Flexible Packaging | +1.0% to +1.5% | Asia Pacific, Latin America, Europe | Medium to Long Term (2027-2033) |

| Rising Consumption of Packaged Goods | +0.8% to +1.2% | Emerging Economies (China, India, Brazil, Southeast Asia) | Short to Long Term (2025-2033) |

| Technological Advancements in Packaging Machinery | +0.5% to +0.8% | North America, Europe, Developed Asia Pacific | Medium Term (2026-2030) |

| Focus on Sustainable Packaging Solutions | +0.7% to +1.0% | Global, especially Europe and North America | Medium to Long Term (2027-2033) |

Packaging Adhesive Market Restraints Analysis

Despite significant growth prospects, the packaging adhesive market faces several notable restraints. Volatility in the prices of raw materials, largely derived from petrochemicals, poses a continuous challenge to manufacturers. Fluctuations in crude oil prices and the supply of key chemical intermediates can directly impact production costs, leading to margin pressures and pricing instability for adhesive products. This economic sensitivity can hinder long-term planning and investment within the industry.

Moreover, increasingly stringent environmental regulations, particularly concerning volatile organic compound (VOC) emissions and the disposal of hazardous chemicals, present a significant hurdle. Compliance with these regulations often necessitates investment in new formulations, production processes, and abatement technologies, which can increase operational expenses and product development timelines. The inherent complexity of developing adhesives that meet both high-performance requirements and strict environmental standards can slow down innovation and market entry for certain product categories, particularly in highly regulated regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.8% to -1.2% | Global | Short to Medium Term (2025-2029) |

| Stringent Environmental Regulations | -0.6% to -1.0% | Europe, North America, parts of Asia Pacific (e.g., China) | Medium to Long Term (2027-2033) |

| Competition from Alternative Bonding Methods | -0.3% to -0.5% | Specific Niche Applications, Developed Markets | Short to Medium Term (2025-2029) |

| Supply Chain Disruptions | -0.4% to -0.7% | Global, Intermittent | Short Term (2025-2026) |

| High Research and Development Costs | -0.2% to -0.4% | Global, particularly for specialized formulations | Long Term (2030-2033) |

Packaging Adhesive Market Opportunities Analysis

Significant opportunities exist within the packaging adhesive market, particularly driven by the growing emphasis on sustainability and the evolving landscape of packaging materials. The increasing consumer and regulatory preference for eco-friendly packaging solutions creates a strong demand for bio-based, biodegradable, and recyclable adhesives. Developing innovative adhesive systems that facilitate the recyclability or compostability of packaging materials presents a substantial avenue for market expansion and differentiation.

Furthermore, the expansion into emerging markets, especially in Asia Pacific and Latin America, offers considerable growth prospects. These regions are experiencing rapid industrialization, urbanization, and an increasing disposable income, leading to higher consumption of packaged goods and consequently, greater demand for packaging adhesives. Additionally, the continuous innovation in packaging designs, including lightweighting, smart packaging, and sophisticated barrier films, creates specific requirements for advanced adhesive technologies. This necessitates ongoing research and development into specialized adhesives capable of bonding diverse and challenging substrates, thereby opening up new product categories and application areas for market players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based & Sustainable Adhesives | +1.0% to +1.5% | Global, particularly Europe and North America | Medium to Long Term (2027-2033) |

| Expansion in Emerging Economies | +0.8% to +1.2% | Asia Pacific, Latin America, Middle East & Africa | Short to Long Term (2025-2033) |

| Innovation in Smart and Functional Packaging | +0.6% to +0.9% | North America, Europe, Developed Asia Pacific | Medium to Long Term (2028-2033) |

| Adoption of Recyclable and Reusable Packaging | +0.7% to +1.0% | Global, driven by regulatory and consumer pressure | Medium Term (2026-2030) |

| Growing Demand for Specialized Adhesives for Diverse Substrates | +0.5% to +0.8% | Global, across various industries | Short to Medium Term (2025-2029) |

Packaging Adhesive Market Challenges Impact Analysis

The packaging adhesive market faces several complex challenges that necessitate strategic responses from industry participants. One significant challenge is the increasing diversity and complexity of packaging substrates. Manufacturers are increasingly using multi-material laminates, recycled content, and specialized coatings to meet sustainability goals and performance requirements. Developing adhesives that can consistently bond these varied and often challenging surfaces while maintaining durability, barrier properties, and process efficiency is a continuous technical hurdle.

Another prominent challenge involves navigating the intricate and evolving regulatory landscape globally. Adhesives used in food packaging, for instance, must comply with stringent regulations concerning food contact materials, migration limits, and ingredient approvals across different jurisdictions (e.g., FDA, EU regulations). This fragmented regulatory environment adds complexity to product development, testing, and market entry, particularly for international players. Furthermore, the pressure to develop cost-effective sustainable solutions without compromising performance or increasing production costs presents a significant balancing act for adhesive manufacturers, driving the need for innovative and economically viable green technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adhering to Diverse and Challenging Substrates | -0.7% to -1.0% | Global, pervasive across applications | Short to Medium Term (2025-2029) |

| Complex and Evolving Regulatory Landscape | -0.5% to -0.8% | Europe, North America, Key Asian Markets | Medium to Long Term (2027-2033) |

| Developing Cost-Effective Sustainable Solutions | -0.4% to -0.6% | Global, particularly for mass-market adoption | Medium Term (2026-2030) |

| Performance Under Extreme Conditions (Temperature, Moisture) | -0.3% to -0.5% | Specific End-use Applications (e.g., frozen food, industrial) | Short to Medium Term (2025-2029) |

| Intense Competition and Price Pressure | -0.2% to -0.4% | Global, across all market segments | Short to Long Term (2025-2033) |

Packaging Adhesive Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Packaging Adhesive Market, covering historical data, current market dynamics, and future projections. The report offers detailed insights into market size, growth drivers, restraints, opportunities, and challenges, segmented across various parameters to provide a holistic view of the industry landscape. It also includes a competitive analysis featuring profiles of key market players and their strategies, alongside regional market trends and outlooks, enabling stakeholders to make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.2 Billion |

| Market Forecast in 2033 | USD 29.8 Billion |

| Growth Rate | 5.7% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema S.A. (Bostik), The Dow Chemical Company, 3M Company, Avery Dennison Corporation, Ashland Global Holdings Inc., Illinois Tool Works Inc. (ITW), Jowat SE, Pidilite Industries Ltd., Toyo Ink SC Holdings Co., Ltd., Huntsman Corporation, Lord Corporation, BASF SE, DIC Corporation, Cyberbond LLC, Franklin International, Sipol S.p.A., Beardow Adams (Adhesives) Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The packaging adhesive market is segmented across several critical dimensions, allowing for a granular understanding of its dynamics and growth pockets. Segmentation by chemistry encompasses widely used categories such as water-based, solvent-based, hot-melt, and reactive adhesives, each offering distinct performance characteristics and application benefits suitable for various packaging needs. Technology segmentation often overlaps with chemistry but focuses on the application and curing mechanisms, differentiating between water-borne, solvent-borne, hot melt, and reactive systems, which dictates their suitability for specific manufacturing processes.

Further segmentation by application highlights the diverse uses of adhesives in the packaging industry, including flexible packaging (pouches, films), rigid packaging (cartons, boxes), labels, tapes, and industrial assembly tasks for packaging components. Finally, the end-use industry segmentation provides insight into demand drivers from sectors such as food & beverage, personal care & cosmetics, healthcare, and general consumer goods, each with unique regulatory and performance requirements for their packaging adhesives. This multi-faceted segmentation helps to identify key market trends, competitive landscapes, and future growth opportunities within specific verticals.

- By Chemistry:

- Water-based: Emulsion, dispersion adhesives.

- Solvent-based: Based on synthetic or natural polymers dissolved in organic solvents.

- Hot-melt: Thermoplastic adhesives applied in molten state, solidifying upon cooling.

- Reactive & Others: Including Polyurethane (PU), Epoxy, Cyanoacrylate, UV-curable, Pressure-sensitive adhesives (PSA).

- By Technology:

- Water-borne

- Solvent-borne

- Hot Melt

- Reactive

- By Application:

- Flexible Packaging: Pouches, bags, films, laminations.

- Rigid Packaging: Cartons, cases, boxes, containers.

- Labels: Pressure-sensitive labels, wet glue labels.

- Tapes: Packaging tapes, specialty tapes.

- Industrial & Assembly: Palletizing, tray forming, specialty packaging.

- By End-use Industry:

- Food & Beverage: Dairy, bakery, confectionary, processed foods, beverages.

- Personal Care & Cosmetics: Toiletries, beauty products, hygiene products.

- Healthcare: Pharmaceutical packaging, medical devices.

- Industrial Packaging: Chemical, automotive, durable goods packaging.

- Consumer Goods: Electronics, apparel, home care products.

- Others: Specialty applications, niche markets.

Regional Highlights

The global packaging adhesive market exhibits distinct regional dynamics, with Asia Pacific emerging as the dominant and fastest-growing region. This growth is primarily fueled by rapid industrialization, increasing manufacturing activities, expanding consumer base, and rising disposable incomes in countries like China, India, Japan, and Southeast Asian nations. The burgeoning e-commerce sector and the expanding food and beverage industry in this region are significant contributors to the escalating demand for packaging adhesives across diverse applications.

North America and Europe represent mature markets characterized by stringent regulatory environments and a strong emphasis on sustainable and high-performance solutions. In these regions, the demand is driven by innovation in packaging design, the adoption of automation in packaging lines, and a shift towards eco-friendly adhesive formulations. Latin America and the Middle East & Africa are poised for steady growth, driven by urbanization, infrastructure development, and increasing consumption of packaged goods, presenting emerging opportunities for adhesive manufacturers to expand their market presence and cater to evolving local demands.

- Asia Pacific: Holds the largest market share and is projected to be the fastest-growing region due to booming manufacturing, rising disposable incomes, and increasing e-commerce penetration in countries such as China, India, Japan, South Korea, and Southeast Asian nations.

- North America: Characterized by technological advancements, strong emphasis on sustainable packaging solutions, and high demand from food & beverage, healthcare, and e-commerce sectors, particularly in the United States and Canada.

- Europe: A mature market with stringent environmental regulations driving innovation towards bio-based and low-VOC adhesives; significant demand from food & beverage, personal care, and industrial sectors across Germany, France, the UK, and Italy.

- Latin America: Expected to witness steady growth due to increasing industrialization, urbanization, and rising consumption of packaged goods, with Brazil and Mexico being key markets.

- Middle East & Africa (MEA): Emerging market with growth driven by infrastructure development, rising population, and increasing foreign investments in manufacturing and packaging industries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Packaging Adhesive Market.- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Arkema S.A. (Bostik)

- The Dow Chemical Company

- 3M Company

- Avery Dennison Corporation

- Ashland Global Holdings Inc.

- Illinois Tool Works Inc. (ITW)

- Jowat SE

- Pidilite Industries Ltd.

- Toyo Ink SC Holdings Co., Ltd.

- Huntsman Corporation

- Lord Corporation

- BASF SE

- DIC Corporation

- Cyberbond LLC

- Franklin International

- Sipol S.p.A.

- Beardow Adams (Adhesives) Ltd.

Frequently Asked Questions

Analyze common user questions about the Packaging Adhesive market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the primary growth driver for the Packaging Adhesive Market?

The primary growth driver for the packaging adhesive market is the rapid global expansion of the e-commerce sector, which necessitates robust and efficient packaging solutions, coupled with the increasing consumption of packaged goods worldwide.

What are the major types of adhesives used in packaging?

The major types of adhesives used in packaging include hot-melt adhesives, water-based adhesives, solvent-based adhesives, and reactive adhesives (such as polyurethanes), each suited for different substrates and application requirements.

How is sustainability impacting the Packaging Adhesive Market?

Sustainability is profoundly impacting the market by driving demand for eco-friendly solutions, including bio-based, water-based, and solvent-free adhesives, as well as formulations that facilitate packaging recyclability and compostability.

Which region holds the largest market share in Packaging Adhesives?

The Asia Pacific region currently holds the largest market share in the packaging adhesive market, primarily due to significant industrial growth, increasing manufacturing activities, and a large consumer base.

What are the key challenges faced by the Packaging Adhesive industry?

Key challenges for the packaging adhesive industry include navigating volatile raw material prices, complying with stringent and evolving environmental regulations, and developing adhesives for increasingly diverse and challenging packaging substrates.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted