Structural Adhesive Market

Structural Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708791 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

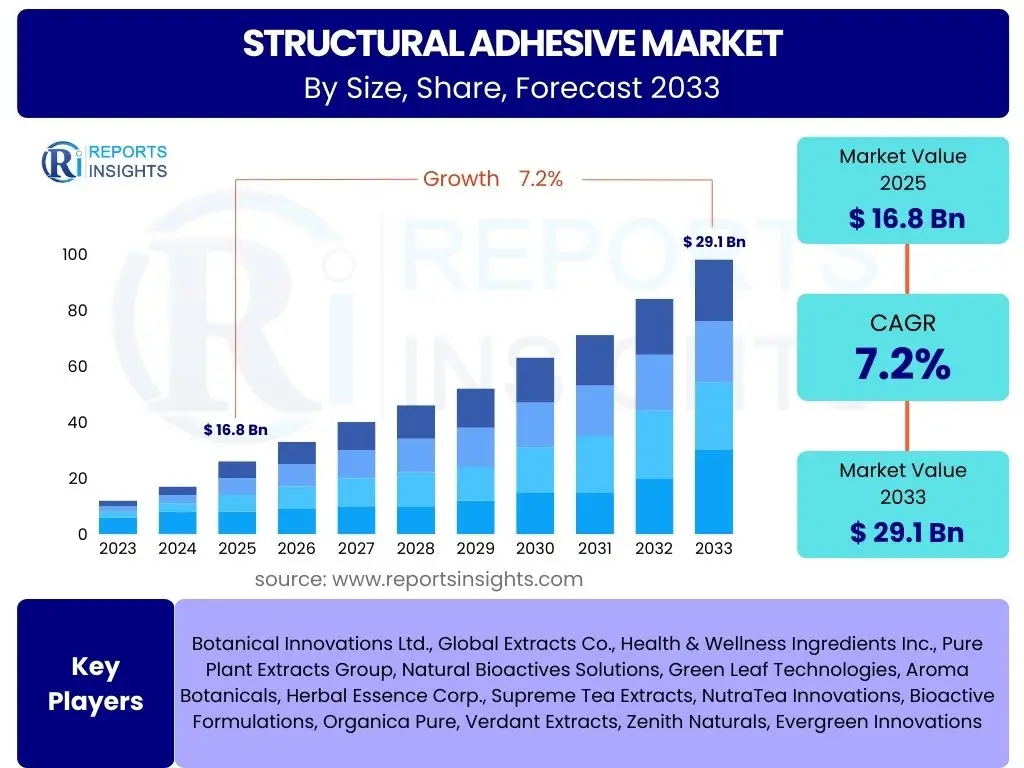

Structural Adhesive Market Size

According to Reports Insights Consulting Pvt Ltd, The Structural Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 16.8 Billion in 2025 and is projected to reach USD 29.1 Billion by the end of the forecast period in 2033.

Key Structural Adhesive Market Trends & Insights

The structural adhesive market is witnessing significant transformations driven by evolving industrial requirements and technological advancements. Key trends indicate a strong shift towards lightweighting in transportation sectors, an increasing demand for sustainable and bio-based adhesive solutions, and the integration of advanced manufacturing techniques. Furthermore, the market is characterized by innovation in adhesive chemistries to bond challenging substrates and withstand extreme environmental conditions, catering to the sophisticated needs of modern applications across diverse industries. The convergence of these factors is shaping a dynamic landscape, pushing manufacturers to develop high-performance, durable, and environmentally conscious products.

Another prominent insight revolves around the expanding application scope of structural adhesives. Originally dominant in aerospace and automotive, their utility has now permeated wind energy, electronics, construction, and marine sectors due to superior bonding strength, fatigue resistance, and aesthetic advantages over traditional fastening methods. This diversification is fueled by the desire for enhanced product performance, simplified assembly processes, and reduced overall manufacturing costs. The focus remains on developing adhesives that offer both structural integrity and process efficiency, ensuring their continued adoption in high-stress, critical applications.

- Increased adoption in automotive lightweighting initiatives.

- Growing demand for sustainable and bio-based adhesive formulations.

- Development of advanced adhesives for dissimilar material bonding.

- Rising application in renewable energy (e.g., wind turbine blades).

- Miniaturization and complex assembly in electronics driving demand.

- Focus on improved process efficiency and automation in application.

AI Impact Analysis on Structural Adhesive

Artificial Intelligence (AI) is set to significantly influence the structural adhesive market by optimizing various stages of the product lifecycle, from research and development to manufacturing and quality control. Users are keen to understand how AI can accelerate material discovery, predict adhesive performance more accurately, and streamline production processes. AI-driven simulations can drastically reduce the time and cost associated with developing new formulations, allowing chemists to explore a vast array of molecular structures and predict their bonding characteristics and durability under specific conditions before physical synthesis. This predictive capability promises to enhance innovation speed and bring novel, high-performance adhesives to market faster.

Moreover, AI's impact extends into operational efficiencies within adhesive manufacturing and application. Users anticipate AI to play a crucial role in predictive maintenance of adhesive dispensing equipment, optimizing curing processes through real-time data analysis, and ensuring consistent quality control. By leveraging machine learning algorithms, manufacturers can analyze vast datasets from production lines to identify anomalies, prevent defects, and fine-tune parameters for optimal output. This leads to reduced waste, improved product consistency, and significant cost savings. The integration of AI also supports the development of smart adhesive systems capable of self-monitoring or responding to environmental changes, opening new frontiers for application.

- Accelerated material discovery and formulation development through AI-driven simulations.

- Enhanced predictive modeling for adhesive performance and durability.

- Optimization of manufacturing processes, including curing and dispensing.

- Improved quality control and defect detection via machine vision and data analytics.

- Predictive maintenance for adhesive application equipment, reducing downtime.

- Development of smart adhesives with self-monitoring capabilities.

Key Takeaways Structural Adhesive Market Size & Forecast

The structural adhesive market is poised for robust growth, driven primarily by an escalating demand for high-performance bonding solutions across critical industrial sectors. A key takeaway is the sustained momentum from the automotive and aerospace industries, where the imperative for lightweighting and enhanced fuel efficiency continues to champion structural adhesives over traditional mechanical fasteners. This trend is expected to significantly contribute to the market's expansion, with manufacturers focusing on developing advanced adhesive systems that offer superior strength-to-weight ratios and improved fatigue resistance.

Furthermore, the market's resilience and future trajectory are heavily influenced by the increasing adoption of structural adhesives in emerging applications such as wind energy, electronics, and construction. The forecast indicates that regional growth will be particularly strong in Asia Pacific due to rapid industrialization and infrastructure development, while North America and Europe will continue to lead in technological innovation and high-value applications. Understanding these dynamics is crucial for stakeholders aiming to capitalize on the evolving landscape, with strategic investments in R&D and geographic expansion being paramount for competitive advantage.

- The market is projected for strong growth, driven by key end-use industries.

- Automotive and aerospace sectors remain primary growth engines due to lightweighting needs.

- Emerging applications in wind energy and electronics offer significant expansion opportunities.

- Asia Pacific is anticipated to be a high-growth region for structural adhesive consumption.

- Technological advancements in adhesive chemistry are crucial for market competitiveness.

Structural Adhesive Market Drivers Analysis

The structural adhesive market is experiencing significant tailwinds from several key industries, primarily driven by the overarching need for enhanced performance, efficiency, and sustainability in modern manufacturing. One of the most prominent drivers is the automotive industry's relentless pursuit of lightweighting strategies to meet stringent fuel efficiency and emissions regulations. Structural adhesives enable the bonding of dissimilar materials like aluminum, composites, and high-strength steels, which are difficult or impossible to join with traditional methods, thereby reducing vehicle weight and improving structural integrity. This shift away from mechanical fasteners for lighter, more efficient vehicles directly propels the demand for advanced structural adhesives that offer high strength, durability, and crashworthiness.

Another crucial driver is the rapid expansion of the aerospace and defense sectors, where structural adhesives are integral to the assembly of aircraft components, satellites, and drones. Their use contributes to reducing overall aircraft weight, which translates into lower fuel consumption and increased payload capacity. Moreover, these adhesives offer superior fatigue resistance, better stress distribution, and smoother aerodynamic surfaces compared to rivets or welds, enhancing the operational lifespan and safety of aerospace structures. The ongoing development of advanced composite materials in these industries further necessitates the use of specialized structural adhesives, as they are often the most effective joining solution for these complex materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Automotive Lightweighting | +2.1% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Growth in Aerospace & Defense Industry | +1.8% | North America, Europe, Asia Pacific | 2025-2033 |

| Increased Use of Composite Materials | +1.5% | Global | 2025-2033 |

| Expansion of Wind Energy Sector | +1.3% | Europe, Asia Pacific, North America | 2025-2033 |

| Miniaturization in Electronics | +0.8% | Asia Pacific, North America | 2025-2033 |

Structural Adhesive Market Restraints Analysis

Despite the robust growth, the structural adhesive market faces several restraints that could potentially impact its trajectory. One significant challenge is the volatility in raw material prices, particularly for petrochemical-derived components like epoxies, polyurethanes, and acrylics. Fluctuations in crude oil prices directly influence the cost of these key ingredients, leading to unstable production costs for adhesive manufacturers. This price unpredictability can squeeze profit margins, necessitate frequent price adjustments for end-users, and complicate long-term strategic planning, especially for smaller market players who may lack the purchasing power of larger corporations.

Another critical restraint involves stringent environmental regulations governing the use of certain chemicals and volatile organic compounds (VOCs) in adhesive formulations. Regulatory bodies worldwide are increasingly pushing for lower VOC emissions and the reduction of hazardous substances, forcing manufacturers to invest heavily in research and development to reformulate products. While this drive towards greener adhesives presents opportunities for innovation, it also incurs significant compliance costs, extends product development cycles, and may limit the performance characteristics of environmentally friendly alternatives compared to traditional, more potent formulations. Furthermore, the need for specialized application equipment and skilled labor for structural adhesives can sometimes deter their adoption, especially in industries accustomed to simpler, conventional fastening methods.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -1.2% | Global | Short to Medium Term (2025-2029) |

| Stringent Environmental Regulations | -1.0% | Europe, North America, Asia Pacific (developing) | Medium to Long Term (2025-2033) |

| Complexity of Application & Curing Processes | -0.7% | Global | Short to Medium Term (2025-2029) |

| Performance Limitations in Extreme Conditions | -0.5% | Specific High-Performance Applications | Long Term (2025-2033) |

Structural Adhesive Market Opportunities Analysis

The structural adhesive market is ripe with opportunities, primarily driven by the continuous quest for enhanced performance and sustainable solutions across various industries. A significant opportunity lies in the development and commercialization of bio-based and sustainable structural adhesives. With growing environmental consciousness and stricter regulations, there is an increasing demand for adhesive solutions derived from renewable resources, offering reduced carbon footprint and lower toxicity. Companies investing in green chemistry and developing high-performance bio-adhesives stand to gain a competitive edge and tap into a rapidly expanding market segment driven by corporate sustainability goals and consumer preferences.

Furthermore, the emergence of advanced manufacturing techniques such as 3D printing and the increasing adoption of multi-material designs in industries like automotive, aerospace, and electronics present unique opportunities for structural adhesives. As products become more complex and lightweight, the need for adhesives capable of bonding diverse substrates with varying thermal expansion coefficients becomes paramount. Innovations in adhesive technology to cater to these intricate bonding challenges, including those requiring rapid curing, high-temperature resistance, or specific electrical properties, will unlock new application areas and drive market expansion. The medical device industry, with its focus on miniaturization and biocompatibility, also offers a niche for specialized structural adhesives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based & Sustainable Adhesives | +1.6% | Europe, North America, Asia Pacific | Medium to Long Term (2027-2033) |

| Increasing Demand in Advanced Composites & Multi-Material Designs | +1.4% | Global | 2025-2033 |

| Growing Application in Medical Devices & Wearables | +1.1% | North America, Europe, Asia Pacific | 2025-2033 |

| Emerging Markets & Infrastructure Development | +0.9% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Integration with Additive Manufacturing (3D Printing) | +0.6% | Global, particularly R&D hubs | Long Term (2028-2033) |

Structural Adhesive Market Challenges Impact Analysis

The structural adhesive market faces several significant challenges that require strategic innovation and adaptation from manufacturers. One primary challenge is achieving consistent high-performance bonding across an increasingly diverse range of substrates, including new types of plastics, advanced composites, and coated metals. Developing universal adhesives that offer reliable long-term performance, adequate adhesion strength, and environmental resistance (e.g., to moisture, chemicals, and temperature fluctuations) for all these materials remains a complex technical hurdle. This complexity is amplified by the varying surface energies, cleanliness requirements, and curing mechanisms associated with different materials, often necessitating highly specialized and application-specific formulations, which can be costly and time-consuming to develop.

Another critical challenge is the competition from traditional fastening methods and the need for greater end-user education and training. While structural adhesives offer numerous advantages, many industries still prefer or are accustomed to mechanical fasteners due to perceived ease of application, reversibility, and established assembly lines. Overcoming this inertia requires not only demonstrating the clear technical and economic benefits of adhesives but also providing comprehensive support, including application guidelines, equipment recommendations, and training programs. Furthermore, managing the shelf life and storage conditions of reactive adhesive systems, ensuring proper mixing and curing, and addressing potential health and safety concerns during handling pose logistical and operational challenges that can impact adoption rates and overall market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Consistent Bonding Across Diverse Substrates | -0.9% | Global | 2025-2033 |

| Competition from Traditional Fasteners | -0.8% | Global | Short to Medium Term (2025-2029) |

| Need for Specialized Application Equipment & Training | -0.6% | Global | 2025-2033 |

| Managing Shelf Life & Storage Conditions | -0.4% | Global | Short Term (2025-2027) |

Structural Adhesive Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global structural adhesive market, covering historical data, current market dynamics, and future projections. It delves into the key drivers, restraints, opportunities, and challenges influencing market growth, offering a detailed segmentation by resin type, end-use industry, and application. Furthermore, the report presents a thorough regional analysis and profiles leading market players, equipping stakeholders with critical insights for strategic decision-making and competitive positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 16.8 Billion |

| Market Forecast in 2033 | USD 29.1 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, 3M Company, Arkema S.A., DOW Inc., Ashland Global Holdings Inc., Huntsman Corporation, Lord Corporation (Parker Hannifin), ITW Performance Polymers, Permabond LLC, Master Bond Inc., Bostik (Arkema Group), DuPont de Nemours, Inc., Momentive Performance Materials Inc., Wacker Chemie AG, BASF SE, Cytec Solvay Group, Scigrip (IPS Corporation), Jowat SE |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The structural adhesive market is comprehensively segmented to provide a granular view of its diverse applications and material compositions. This segmentation is crucial for understanding the specific dynamics, growth opportunities, and competitive landscape within each category. Analyzing the market across various dimensions allows for a more targeted strategic approach, enabling stakeholders to identify high-growth areas and tailor product offerings to specific industry needs.

- By Resin Type: This segment includes different chemical bases that determine the adhesive's properties and performance.

- Epoxy

- Polyurethane

- Acrylic

- Cyanoacrylate

- Silicone

- Others (e.g., SMP, Phenolic)

- By End-Use Industry: This categorizes the market based on the primary sector where structural adhesives are utilized, highlighting industry-specific demand drivers.

- Automotive

- Aerospace

- Construction

- Wind Energy

- Electronics

- Marine

- Others (e.g., Rail, Medical, Consumer Goods)

- By Application: This segment details the specific uses of structural adhesives within the end-use industries, showcasing functional requirements.

- Body-in-white (Automotive)

- Interior (Automotive)

- Exterior (Automotive)

- Engine & Powertrain (Automotive)

- Wing & Fuselage Assembly (Aerospace)

- Rotor Blades (Wind Energy)

- Composite Bonding (General)

- Battery Assembly (Electronics/Automotive EV)

- Others (e.g., Panel Lamination, Electronic Component Encapsulation)

Regional Highlights

- North America: This region stands as a significant market for structural adhesives, particularly driven by robust demand from the aerospace, automotive, and construction industries. The presence of major aircraft manufacturers and electric vehicle production facilities, coupled with stringent performance standards and ongoing technological advancements, fuels the adoption of high-performance bonding solutions.

- Europe: Europe represents a mature yet innovative market, characterized by stringent environmental regulations and a strong emphasis on sustainable adhesive solutions. Key drivers include the growing wind energy sector, advanced manufacturing in automotive, and substantial investments in construction and infrastructure projects, particularly in countries like Germany, France, and the UK.

- Asia Pacific (APAC): This region is projected to exhibit the highest growth rate in the structural adhesive market, primarily due to rapid industrialization, burgeoning manufacturing sectors, and increasing foreign direct investment. Countries like China, India, Japan, and South Korea are witnessing significant expansion in automotive production, electronics manufacturing, and infrastructure development, leading to a surge in demand for structural adhesives.

- Latin America: The structural adhesive market in Latin America is experiencing gradual growth, propelled by increasing investments in infrastructure development, expanding automotive manufacturing bases (especially in Mexico and Brazil), and a developing construction sector. While smaller than other regions, it offers emerging opportunities.

- Middle East and Africa (MEA): The MEA region presents nascent but growing opportunities, largely influenced by rising investments in construction and infrastructure projects, particularly in the GCC countries. The diversification of economies away from oil and gas and the development of new manufacturing capabilities are expected to drive future demand for structural adhesives.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Structural Adhesive Market.- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- 3M Company

- Arkema S.A.

- DOW Inc.

- Ashland Global Holdings Inc.

- Huntsman Corporation

- Lord Corporation (Parker Hannifin)

- ITW Performance Polymers

- Permabond LLC

- Master Bond Inc.

- Bostik (Arkema Group)

- DuPont de Nemours, Inc.

- Momentive Performance Materials Inc.

- Wacker Chemie AG

- BASF SE

- Cytec Solvay Group

- Scigrip (IPS Corporation)

- Jowat SE

Frequently Asked Questions

What are structural adhesives?

Structural adhesives are high-strength bonding agents capable of holding load-bearing joints together permanently, distributing stress evenly across the bonded area. They are designed to withstand significant shear, tensile, and peel forces, making them suitable for critical applications where strong, durable, and long-lasting bonds are required.

What are the primary advantages of using structural adhesives over traditional fasteners?

Structural adhesives offer several advantages, including superior stress distribution, reduced weight in assemblies, enhanced fatigue resistance, improved aesthetics due to invisible bonds, and the ability to join dissimilar materials. They also provide sealing properties, dampen vibrations, and can simplify manufacturing processes.

Which industries are the largest consumers of structural adhesives?

The largest consumers of structural adhesives include the automotive industry (for lightweighting and body-in-white assembly), aerospace (for aircraft structures and components), construction (for panel bonding and structural glazing), and wind energy (for rotor blade assembly).

What are the main types of structural adhesives?

The main types of structural adhesives are epoxy, polyurethane, acrylic, and cyanoacrylate. Each type offers distinct performance characteristics, such as different curing times, temperature resistances, and adhesion to specific substrates, tailored for various industrial applications.

What key trends are shaping the future of the structural adhesive market?

Key trends include the increasing demand for sustainable and bio-based adhesive solutions, continuous innovation for bonding advanced composite and dissimilar materials, growth in electric vehicle battery assembly, and the adoption of automation and AI in adhesive application and development processes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted