Wood Based Panel Market

Wood Based Panel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703306 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

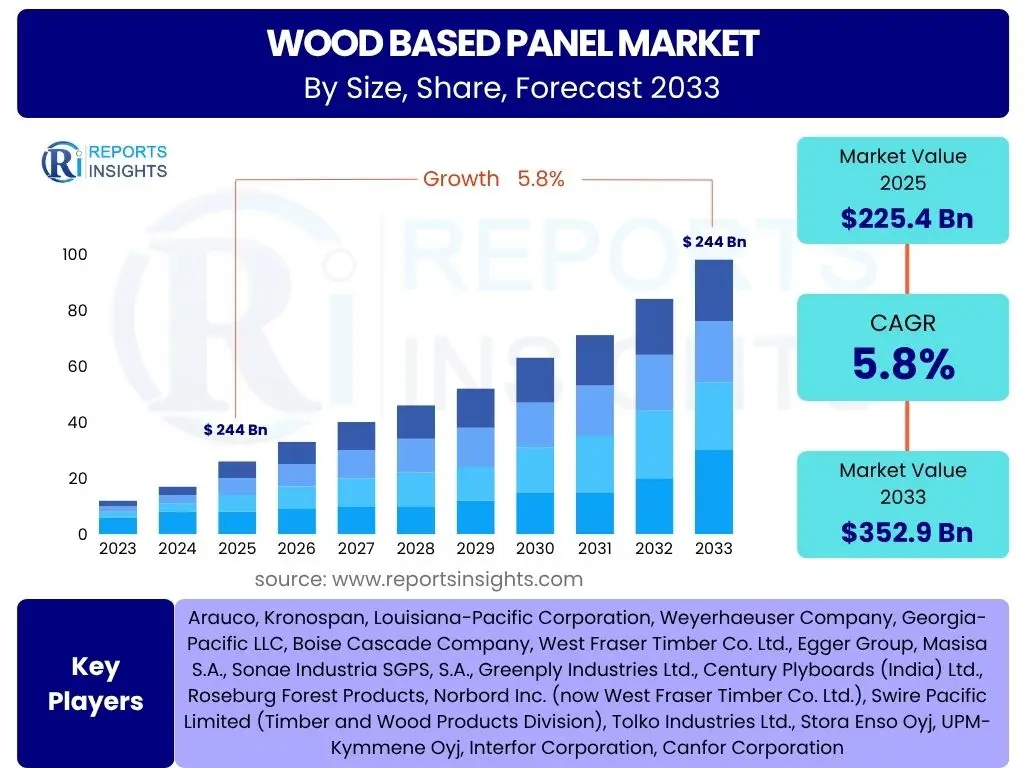

Wood Based Panel Market Size

According to Reports Insights Consulting Pvt Ltd, The Wood Based Panel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 225.4 billion in 2025 and is projected to reach USD 352.9 billion by the end of the forecast period in 2033.

Key Wood Based Panel Market Trends & Insights

User inquiries frequently revolve around the evolving landscape of the wood based panel market, particularly focusing on sustainability, technological advancements, and shifting consumer preferences. There is a clear interest in understanding how environmental concerns are driving product innovation, the impact of digitalization on manufacturing processes, and the increasing demand for customizable and aesthetically pleasing panel solutions. Furthermore, the integration of smart home technologies and the preference for healthier indoor environments are emerging as significant areas of interest, influencing material choices and product development within the industry.

The market is witnessing a strong push towards eco-friendly and sustainable products, with an increasing emphasis on sourcing from certified forests and utilizing recycled content. This trend is not merely a regulatory compliance issue but a core consumer demand influencing purchasing decisions. Simultaneously, advancements in manufacturing technologies are enabling the production of panels with enhanced properties, such as improved moisture resistance, fire retardancy, and durability, catering to a wider range of applications and performance requirements. These technological leaps are also contributing to greater efficiency and reduced waste in production, aligning with both economic and environmental objectives.

- Growing demand for sustainable and eco-friendly wood panels, driven by environmental awareness and certifications.

- Increasing adoption of engineered wood products due to their superior strength, stability, and resource efficiency.

- Rise of customized and aesthetically diverse panel solutions catering to modern interior design trends.

- Technological advancements in manufacturing processes leading to improved panel properties and production efficiency.

- Shift towards lightweight and high-performance panels for diverse applications in furniture, construction, and automotive industries.

- Integration of smart features and healthier material compositions for indoor air quality improvements.

AI Impact Analysis on Wood Based Panel

User questions related to the impact of AI on the wood based panel sector often explore its potential for optimizing production processes, enhancing quality control, and improving supply chain management. Stakeholders are keen to understand how AI algorithms can predict market demand, minimize raw material waste, and streamline logistics from forest to finished product. There is also significant curiosity regarding AI's role in predictive maintenance of machinery and its ability to identify defects in panels with greater accuracy than traditional methods.

AI's influence in the wood based panel industry is primarily manifested through advancements in operational efficiency and data-driven decision-making. Machine learning algorithms are being deployed to analyze vast datasets related to timber quality, production parameters, and customer preferences, enabling manufacturers to fine-tune their processes for optimal yield and product consistency. Predictive analytics, powered by AI, helps in forecasting equipment failures, thereby reducing downtime and maintenance costs. The ability of AI to process complex information rapidly allows for more agile responses to market shifts and supply chain disruptions, fostering a more resilient and responsive industry.

- Optimized resource utilization and waste reduction through AI-driven material sorting and cutting pattern optimization.

- Enhanced quality control with AI-powered visual inspection systems detecting defects with high precision.

- Predictive maintenance of machinery, reducing downtime and operational costs.

- Improved supply chain efficiency and logistics management through demand forecasting and route optimization.

- Development of new material compositions and panel designs aided by AI simulation and design tools.

- Real-time data analysis for agile decision-making in production and inventory management.

Key Takeaways Wood Based Panel Market Size & Forecast

Common user questions regarding key takeaways from the Wood Based Panel market size and forecast highlight a desire to understand the primary drivers of growth, the most promising market segments, and the overarching factors influencing future expansion. Users are looking for concise insights into where the market is headed, what opportunities lie ahead, and which regions are expected to contribute significantly to market value. The emphasis is on actionable intelligence that distills complex market data into clear, digestible conclusions.

The market is poised for steady growth, primarily fueled by robust construction activities, increasing urbanization, and a growing global preference for sustainable building materials. Engineered wood products, in particular, are expected to exhibit strong performance due to their versatility and environmental benefits. While North America and Europe remain mature markets, the Asia Pacific region is anticipated to be a significant growth engine, driven by rapid industrialization and residential development. Investment in research and development for innovative panel types and improved manufacturing efficiencies will be crucial for competitive advantage in this evolving landscape.

- Steady growth trajectory projected, driven by global construction and furniture industries.

- Significant expansion expected in engineered wood panels, including OSB, MDF, and plywood, due to their performance characteristics.

- Asia Pacific to emerge as a dominant growth region, propelled by urbanization and infrastructure development.

- Sustainability and eco-friendly sourcing are paramount factors influencing market adoption and product innovation.

- Technological advancements in production processes are enhancing panel quality and reducing manufacturing costs.

- Increased demand for customizable and versatile panel solutions in diverse end-use applications.

Wood Based Panel Market Drivers Analysis

The growth of the wood based panel market is significantly propelled by several interconnected factors, primarily rooted in global demographic shifts and evolving industrial demands. The rapid expansion of the construction sector, particularly in emerging economies, alongside an increasing preference for sustainable and prefabricated building solutions, drives substantial demand for various panel types. Furthermore, the burgeoning furniture industry, both residential and commercial, relies heavily on wood panels for cost-effective and versatile design solutions. These foundational demands create a strong undercurrent of growth for the market.

Beyond traditional applications, the increasing global population and continuous urbanization necessitate new housing and commercial spaces, directly translating into higher consumption of wood based panels. The inherent advantages of engineered wood products, such as consistency, strength, and reduced environmental impact compared to solid wood, make them highly attractive for modern construction practices. Moreover, advancements in panel manufacturing technologies have led to the development of panels with enhanced properties like improved moisture resistance, fire retardancy, and aesthetic appeal, broadening their application scope and reinforcing market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in residential and commercial construction activities | +1.5% | Asia Pacific, North America, Europe | Mid to Long-term (2025-2033) |

| Increasing demand for sustainable and eco-friendly building materials | +1.2% | Global, particularly Europe and North America | Mid to Long-term (2025-2033) |

| Expansion of the furniture manufacturing industry | +1.0% | Asia Pacific, Europe | Mid to Long-term (2025-2033) |

| Technological advancements in panel production and product innovation | +0.8% | Global | Short to Mid-term (2025-2029) |

| Urbanization and rising disposable incomes, boosting interior design and renovation | +0.7% | Emerging economies (India, China, Southeast Asia) | Mid to Long-term (2025-2033) |

Wood Based Panel Market Restraints Analysis

Despite robust growth drivers, the wood based panel market faces several significant restraints that could temper its expansion. One primary concern is the volatility of raw material prices, particularly timber, which is subject to seasonal variations, environmental regulations, and global supply chain disruptions. This fluctuation directly impacts production costs and profit margins for manufacturers, making long-term planning challenging. Additionally, stringent environmental regulations regarding deforestation, sustainable forestry practices, and emissions from panel manufacturing facilities can increase operational complexities and compliance costs, potentially slowing down market growth in certain regions.

Another major restraint comes from the increasing competition posed by alternative building materials and furniture components, such as plastics, metals, and composites. These substitutes often offer different properties or cost advantages for specific applications, drawing away market share from wood based panels. Economic slowdowns and recessionary pressures in key markets can also significantly dampen construction and furniture manufacturing activities, directly reducing demand for wood panels. Furthermore, issues such as illegal logging in some regions can negatively impact the market's reputation and hinder the adoption of certified, sustainable products, creating a perception challenge for the entire industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in raw material (timber) prices | -1.3% | Global, particularly regions with limited domestic timber supply | Short to Mid-term (2025-2029) |

| Stringent environmental regulations and compliance costs | -1.0% | Europe, North America | Long-term (2025-2033) |

| Competition from alternative materials (plastics, metals, composites) | -0.9% | Global, especially in industrial applications | Mid to Long-term (2025-2033) |

| Economic slowdowns and geopolitical uncertainties impacting construction | -0.7% | Global, with varying regional severity | Short-term (2025-2027) |

| Health concerns related to VOC emissions from certain panel types | -0.5% | Developed countries (Europe, North America) | Mid-term (2025-2030) |

Wood Based Panel Market Opportunities Analysis

The wood based panel market is rich with opportunities, particularly in expanding application areas and capitalizing on evolving consumer preferences. The growing global emphasis on green building initiatives and sustainable urban development presents a significant avenue for market players to innovate and offer certified eco-friendly products. As governments and construction firms increasingly prioritize materials with lower carbon footprints and higher recyclability, wood based panels, especially those derived from sustainable sources, become highly competitive. This shift creates demand for new product lines and enhanced marketing strategies focused on environmental benefits.

Furthermore, advancements in manufacturing technology and material science open doors for the development of high-performance panels tailored for specific needs, such as fire-resistant panels for commercial buildings or moisture-resistant panels for kitchens and bathrooms. The rise of modular construction and prefabrication techniques also offers a fertile ground for wood based panels, given their ease of handling, lightweight nature, and structural integrity. Penetration into emerging markets, where construction and furniture industries are experiencing rapid growth, coupled with the expansion of e-commerce platforms for building materials, provides additional avenues for market expansion and increased accessibility to a wider consumer base.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing adoption of green building practices and sustainable construction | +1.4% | Global, particularly developed economies and rapidly developing urban centers | Mid to Long-term (2025-2033) |

| Product innovation and development of high-performance panels (e.g., moisture-resistant, fire-retardant) | +1.1% | Global | Mid-term (2025-2030) |

| Expansion into new application areas such as automotive interiors and packaging | +0.9% | Global | Long-term (2028-2033) |

| Untapped potential in emerging economies with high infrastructure development | +0.8% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2025-2033) |

| Growth of modular and prefabricated construction methods | +0.6% | North America, Europe, parts of Asia Pacific | Mid to Long-term (2025-2033) |

Wood Based Panel Market Challenges Impact Analysis

The wood based panel market faces several inherent challenges that demand strategic responses from industry players. Supply chain disruptions, often triggered by natural disasters, geopolitical tensions, or health crises, can severely impact the availability and cost of raw timber and other necessary inputs. Such disruptions can lead to production delays, increased logistics costs, and ultimately, higher prices for end products, affecting market competitiveness. Furthermore, the industry is increasingly grappling with a shortage of skilled labor, particularly in manufacturing and forestry operations, which can constrain production capacity and hinder the adoption of advanced technologies requiring specialized expertise.

Another significant challenge involves navigating the complex and evolving landscape of environmental regulations and certifications. While sustainability presents an opportunity, the stringent requirements for forest management, formaldehyde emissions, and waste disposal can impose substantial compliance costs and necessitate significant investments in new technologies or processes. Differentiating products in a competitive market, especially against lower-cost alternatives or products from regions with less stringent regulations, also poses a continuous challenge. Moreover, the need to adapt to changing consumer preferences, such as the demand for VOC-free panels or specific aesthetic finishes, requires ongoing research and development investment, placing pressure on manufacturers to remain agile and innovative.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply chain disruptions and logistics complexities | -1.2% | Global | Short-term (2025-2027) |

| Shortage of skilled labor in manufacturing and forestry | -1.0% | North America, Europe | Mid to Long-term (2025-2033) |

| Intense competition and price pressure from regional and international players | -0.8% | Global, particularly Asia Pacific and competitive export markets | Mid to Long-term (2025-2033) |

| Compliance with evolving environmental and health regulations (e.g., formaldehyde emissions) | -0.7% | Europe, North America, emerging Asian markets adopting stricter standards | Long-term (2025-2033) |

| Need for continuous innovation to meet changing design trends and performance requirements | -0.6% | Global | Mid to Long-term (2025-2033) |

Wood Based Panel Market - Updated Report Scope

This report provides an in-depth analysis of the global wood based panel market, encompassing a comprehensive evaluation of market size, growth drivers, restraints, opportunities, and challenges across various product types, applications, and end-use sectors. It offers a detailed forecast from 2025 to 2033, highlighting regional market dynamics and the competitive landscape. The scope includes an examination of key market trends, the impact of emerging technologies such as AI, and a strategic overview of prominent industry players to provide a holistic understanding of market potential and strategic imperatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 225.4 billion |

| Market Forecast in 2033 | USD 352.9 billion |

| Growth Rate | 5.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Arauco, Kronospan, Louisiana-Pacific Corporation, Weyerhaeuser Company, Georgia-Pacific LLC, Boise Cascade Company, West Fraser Timber Co. Ltd., Egger Group, Masisa S.A., Sonae Industria SGPS, S.A., Greenply Industries Ltd., Century Plyboards (India) Ltd., Roseburg Forest Products, Norbord Inc. (now West Fraser Timber Co. Ltd.), Swire Pacific Limited (Timber and Wood Products Division), Tolko Industries Ltd., Stora Enso Oyj, UPM-Kymmene Oyj, Interfor Corporation, Canfor Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The wood based panel market is extensively segmented by product type, application, and end-use, allowing for a granular analysis of market dynamics and growth potential across diverse categories. Each segment exhibits unique characteristics and growth drivers, reflecting varying technological advancements, consumer preferences, and industry demands. Understanding these specific segments is crucial for identifying targeted growth opportunities and developing effective market entry strategies for manufacturers and suppliers.

Within product types, engineered wood products such as Medium Density Fiberboard (MDF), Oriented Strand Board (OSB), and plywood continue to dominate due to their versatile applications and improved performance attributes. The application segment highlights the critical role of these panels in key sectors like furniture manufacturing and construction, which collectively represent the largest consumption areas. Furthermore, the end-use segmentation differentiates between residential, commercial, and industrial demands, providing insights into the varying quality, aesthetic, and functional requirements across different consumer bases.

- By Product Type: This segment includes a wide array of panels, each with distinct properties and uses.

- Plywood: Known for its strength and stability, widely used in construction, furniture, and marine applications.

- Particleboard (Chipboard): Economical and versatile, commonly used in furniture, cabinetry, and internal partitioning.

- Medium Density Fiberboard (MDF): Valued for its smooth surface and consistent density, ideal for painting, laminating, and intricate designs in furniture and interior applications.

- Oriented Strand Board (OSB): A high-performance engineered wood panel, primarily used in structural applications like wall sheathing, flooring, and roof decking in construction.

- High Density Fiberboard (HDF): Denser and more durable than MDF, often used for flooring substrates and high-stress applications.

- Laminated Veneer Lumber (LVL): An engineered wood product created by bonding thin wood veneers with adhesives, primarily used for beams, headers, and rimboard in construction.

- Glued Laminated Timber (Glulam): Composed of multiple layers of lumber bonded with durable adhesives, used for structural beams and columns in large-span construction.

- Cross-Laminated Timber (CLT): A large-scale, prefabricated engineered wood product used for floors, walls, and roofs in mid-rise and high-rise timber buildings.

- Others: Includes composite panels, insulation boards, and specialized panel products.

- By Application: This segmentation focuses on the primary industries and uses for wood based panels.

- Furniture and Cabinets: The largest application segment, encompassing residential furniture, office furniture, kitchen cabinets, and modular storage solutions.

- Construction: Includes various structural and non-structural uses such as flooring, wall paneling, roofing, subflooring, and concrete formwork.

- Interior Decoration: Involves decorative panels, partitions, wall cladding, and ceiling applications in residential and commercial spaces.

- Packaging: Utilized for crates, pallets, and protective packaging solutions in industrial and commercial sectors.

- Automotive Interiors: Growing application in vehicle interior components, including door panels, dashboards, and boot liners, driven by lightweighting trends.

- Other Industrial Applications: Encompasses uses in shipbuilding, railway coaches, toys, and various manufacturing processes.

- By End-Use: This segment categorizes consumption based on the type of consumer or building project.

- Residential: Demand driven by new home construction, renovations, and furniture purchases for households.

- Commercial: Includes applications in offices, retail spaces, hotels, healthcare facilities, and educational institutions.

- Industrial: Covers manufacturing facilities, warehouses, and other industrial infrastructure, including packaging and specialized industrial uses.

Regional Highlights

The global wood based panel market demonstrates distinct dynamics across various regions, influenced by economic development, construction trends, regulatory environments, and raw material availability. Each geographic segment presents unique opportunities and challenges for market participants. Understanding these regional specificities is vital for developing effective market strategies and optimizing supply chains.

North America and Europe represent mature markets with established construction and furniture industries. In North America, the demand for OSB and plywood is robust, driven by extensive residential construction and renovation activities, particularly single-family homes. The region also shows increasing adoption of sustainable building practices and engineered wood products for their performance and environmental benefits. European markets, similarly, are characterized by a strong emphasis on sustainability, with stringent regulations promoting low-emission products and certified timber sources. MDF and particleboard are widely used in furniture manufacturing and interior design, reflecting a strong design-conscious consumer base. Innovation in engineered wood for prefabricated construction methods is also a key trend.

Asia Pacific is projected to be the fastest-growing region, primarily due to rapid urbanization, increasing disposable incomes, and significant investments in infrastructure and housing projects in countries like China, India, and Southeast Asian nations. This region is a major hub for furniture manufacturing and boasts a large construction sector, driving high demand for all types of wood panels. However, it also faces challenges related to raw material sourcing and environmental compliance. Latin America and the Middle East & Africa (MEA) are emerging markets with considerable growth potential. Latin America benefits from increasing residential and commercial construction, particularly in Brazil and Mexico. The MEA region, though smaller, is seeing growth driven by diversification efforts, infrastructure development, and a growing tourism sector, which fuels demand for interior fit-outs and furniture in new establishments. Resource availability and political stability can influence growth rates in these regions.

- North America: Dominant in structural panels like OSB and plywood; strong residential construction market; increasing focus on sustainable building and prefabricated housing; mature market with high per capita consumption.

- Europe: High demand for MDF and particleboard in furniture and interior design; stringent environmental regulations driving demand for low-emission and certified products; significant focus on renovation and sustainable forestry; growth in CLT and glulam for mass timber construction.

- Asia Pacific (APAC): Fastest-growing region driven by rapid urbanization, infrastructure development, and booming construction and furniture manufacturing industries in China, India, and Southeast Asia; large consumer base and increasing disposable incomes; growing adoption of engineered wood products.

- Latin America: Emerging market with potential growth stemming from urbanization and increasing investments in residential and commercial infrastructure, particularly in Brazil and Mexico; fluctuating economic conditions can impact market stability.

- Middle East and Africa (MEA): Growing market influenced by diversification efforts from oil-dependent economies, significant construction projects, and increasing tourism; reliance on imports for raw materials and finished products; varied regulatory landscapes.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wood Based Panel Market.- Arauco

- Kronospan

- Louisiana-Pacific Corporation

- Weyerhaeuser Company

- Georgia-Pacific LLC

- Boise Cascade Company

- West Fraser Timber Co. Ltd.

- Egger Group

- Masisa S.A.

- Sonae Industria SGPS, S.A.

- Greenply Industries Ltd.

- Century Plyboards (India) Ltd.

- Roseburg Forest Products

- Tolko Industries Ltd.

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Interfor Corporation

- Canfor Corporation

- Swire Pacific Limited (Timber and Wood Products Division)

Frequently Asked Questions

What is the projected growth rate for the Wood Based Panel Market?

The Wood Based Panel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, driven by increasing construction activities and demand for sustainable materials.

Which product types are expected to lead market growth?

Engineered wood products such as Oriented Strand Board (OSB), Medium Density Fiberboard (MDF), and plywood are anticipated to be key growth drivers due to their versatility, performance, and environmental benefits in construction and furniture applications.

How is sustainability impacting the wood based panel industry?

Sustainability is a major driver, leading to increased demand for eco-friendly panels sourced from certified forests, reduced VOC emissions, and panels made from recycled content, influencing product innovation and consumer preference.

What are the key regions contributing to market expansion?

Asia Pacific is expected to be the fastest-growing region due to rapid urbanization and significant infrastructure development, while North America and Europe will continue to be significant, mature markets with a focus on high-value and sustainable products.

What role does AI play in the Wood Based Panel Market?

AI is increasingly being utilized for optimizing production processes, enhancing quality control through defect detection, improving supply chain efficiency, and enabling predictive maintenance of machinery within the wood based panel industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted