High performance Adhesive Market

High performance Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703177 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

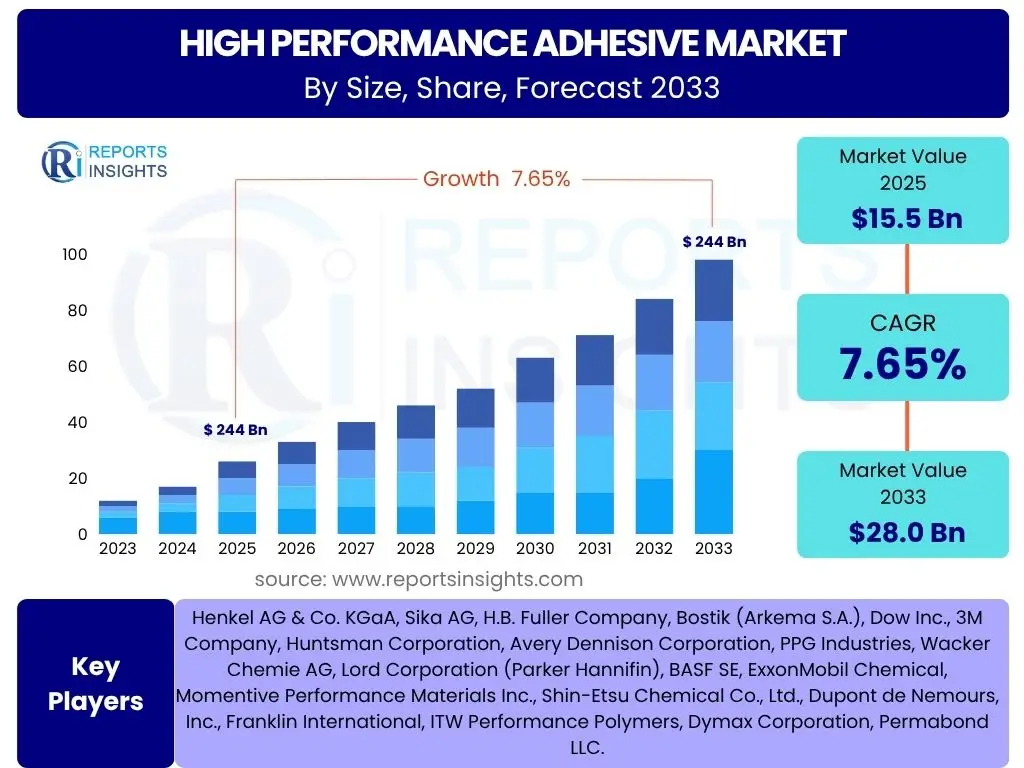

High performance Adhesive Market Size

According to Reports Insights Consulting Pvt Ltd, The High performance Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.65% between 2025 and 2033. The market is estimated at USD 15.5 billion in 2025 and is projected to reach USD 28.0 billion by the end of the forecast period in 2033.

Key High performance Adhesive Market Trends & Insights

The High performance Adhesive market is witnessing a transformative phase driven by evolving industrial demands and technological advancements. Key trends indicate a significant shift towards more sustainable, efficient, and application-specific adhesive solutions. Innovations in material science are enabling the development of adhesives with superior bonding strength, durability, and resistance to extreme conditions, directly addressing the needs of high-growth sectors such as automotive, electronics, and aerospace. Furthermore, the increasing complexity of manufacturing processes and the drive for lightweighting are compelling industries to adopt advanced adhesive formulations that can replace traditional fastening methods.

Consumer and industrial expectations for environmental responsibility are also shaping market trends, with a notable rise in the demand for bio-based and low-VOC (Volatile Organic Compound) adhesives. This aligns with global regulatory pressures and corporate sustainability initiatives, pushing manufacturers to invest in greener formulations. The integration of automation in adhesive application processes is another critical trend, enhancing precision, speed, and efficiency in manufacturing lines, thereby reducing labor costs and waste. These overarching trends highlight a market in constant evolution, prioritizing performance, sustainability, and intelligent application methods.

- Growing demand for lightweight materials in automotive and aerospace.

- Increasing adoption of sustainable and bio-based adhesive solutions.

- Miniaturization and complex designs driving demand in electronics.

- Shift towards advanced manufacturing techniques requiring specific adhesive properties.

- Rising demand for medical and healthcare applications requiring biocompatibility.

- Development of smart adhesives with sensing capabilities.

- Automation and robotic integration in adhesive dispensing.

AI Impact Analysis on High performance Adhesive

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is poised to revolutionize the High performance Adhesive market by enhancing various stages of the product lifecycle, from research and development to manufacturing and application. Users frequently inquire about AI's potential to accelerate new adhesive formulation, optimize production processes, and improve quality control. AI algorithms can analyze vast datasets of material properties, chemical reactions, and performance characteristics, significantly shortening the time required for discovering novel adhesive compounds and predicting their behavior under specific conditions. This capability helps overcome the traditional trial-and-error approach, leading to more efficient R&D and faster market entry for innovative products.

Beyond formulation, AI's influence extends to optimizing manufacturing parameters, predicting equipment maintenance needs, and ensuring consistent product quality. Predictive analytics powered by AI can monitor production lines in real-time, identifying anomalies and preventing defects, thereby reducing waste and improving overall operational efficiency. Furthermore, AI can assist in customizing adhesive solutions for niche applications by simulating performance and recommending optimal formulations, addressing specific user requirements with unprecedented precision. The primary concerns often revolve around the initial investment costs for AI infrastructure, data privacy, and the need for skilled personnel to implement and manage these advanced systems effectively.

- Accelerated discovery and formulation of new adhesive materials.

- Optimization of manufacturing processes for improved efficiency and yield.

- Predictive quality control, minimizing defects and ensuring consistency.

- Enhanced supply chain management and demand forecasting for raw materials.

- Intelligent robots for precise and automated adhesive application.

- Personalized adhesive solutions through advanced material simulation.

Key Takeaways High performance Adhesive Market Size & Forecast

The High performance Adhesive market is on a robust growth trajectory, primarily driven by increasing industrial application in demanding environments and the continuous pursuit of enhanced material performance. Key takeaways from market size and forecast analyses indicate sustained expansion across diverse end-use sectors, including automotive, electronics, and construction, where traditional joining methods are being increasingly replaced by advanced adhesive solutions. The market's upward momentum is further supported by innovations focused on strength, durability, and adaptability to complex substrates, making high-performance adhesives critical components in modern manufacturing and product design.

A significant aspect of this growth is the escalating demand for lightweight and sustainable solutions. Forecasts highlight that industries are prioritizing adhesives that contribute to energy efficiency and environmental responsibility, influencing product development and market adoption. Moreover, regional economic developments and infrastructure projects, particularly in emerging economies, are expected to fuel demand for high-performance construction and industrial adhesives. The market's resilience against economic fluctuations is also notable, as adhesives are integral to the production of essential goods and infrastructure, ensuring consistent demand even during challenging periods.

- Market projected for substantial growth through 2033, driven by industrial advancements.

- Automotive, electronics, and construction sectors are key growth engines.

- Sustainability and lightweighting trends are core to future product development.

- Increased adoption in medical and aerospace for critical applications.

- Emerging economies present significant untapped market potential.

- Continuous innovation in adhesive chemistries and application technologies.

High performance Adhesive Market Drivers Analysis

The High performance Adhesive market is propelled by several robust drivers stemming from evolving industrial requirements and technological advancements. A primary driver is the accelerating demand for lightweight materials, particularly in the automotive and aerospace sectors, where high-performance adhesives offer superior strength-to-weight ratios compared to traditional fasteners. This shift enables manufacturers to reduce vehicle weight, leading to improved fuel efficiency and reduced emissions, aligning with global environmental regulations and consumer preferences. Furthermore, the intricate designs and miniaturization trends in the electronics industry necessitate highly precise and reliable bonding solutions, which high-performance adhesives are uniquely positioned to provide, ensuring circuit integrity and device durability.

Another significant driver is the expanding application scope in emerging fields such as renewable energy, medical devices, and advanced composites. As industries push the boundaries of material science and product functionality, the need for adhesives that can withstand extreme temperatures, harsh chemicals, or biological environments becomes paramount. Additionally, the growing focus on automation and efficient manufacturing processes across industries drives the adoption of adhesives that offer faster curing times and easier application. These factors collectively create a strong foundation for sustained market growth by addressing critical performance and operational needs across a wide array of industrial applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweighting in Automotive & Aerospace | +1.5% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Miniaturization and Complexity in Electronics Manufacturing | +1.2% | Asia Pacific, North America, Europe | Short to Mid-term (2025-2030) |

| Growth in Medical Devices and Healthcare Sector | +0.8% | North America, Europe | Mid to Long-term (2027-2033) |

| Advancements in Construction and Infrastructure Projects | +0.7% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

| Emphasis on Sustainable and Eco-Friendly Adhesives | +0.6% | Europe, North America | Mid to Long-term (2028-2033) |

High performance Adhesive Market Restraints Analysis

Despite the robust growth drivers, the High performance Adhesive market faces several restraints that could potentially impede its expansion. One significant challenge is the volatility and increasing cost of raw materials, many of which are derived from petrochemicals. Fluctuations in crude oil prices directly impact the production costs of various adhesive components, leading to price instability and challenging profit margins for manufacturers. This unpredictability makes long-term planning and pricing strategies difficult, particularly for smaller market players. Additionally, the complex regulatory landscape surrounding chemical manufacturing and product safety poses a considerable hurdle. Strict environmental regulations regarding VOC emissions, hazardous substances, and waste disposal necessitate significant investment in R&D for compliant formulations, increasing operational costs and potentially slowing down new product introductions.

Another restraint involves the technical complexities and specialized application requirements of high-performance adhesives. Achieving optimal bonding performance often requires precise application conditions, specialized equipment, and skilled labor, which can be a barrier for industries not equipped with such capabilities. The slower curing times of some high-performance adhesive systems, compared to traditional fastening methods, can also impact production line speeds, thereby limiting their adoption in high-volume manufacturing environments. Furthermore, the intense competition within the market, coupled with the capital-intensive nature of adhesive manufacturing and R&D, can exert downward pressure on pricing, affecting overall profitability for market participants. These factors collectively present significant challenges that manufacturers must navigate to sustain growth and innovation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -1.0% | Global | Short-term (2025-2027) |

| Stringent Environmental Regulations and Compliance Costs | -0.8% | Europe, North America, Asia Pacific | Mid to Long-term (2026-2033) |

| High R&D Investment and Long Product Development Cycles | -0.5% | Global | Long-term (2028-2033) |

| Performance Limitations in Extreme Conditions for Certain Applications | -0.4% | Global | Short to Mid-term (2025-2030) |

| Lack of Awareness and Technical Expertise in Developing Regions | -0.3% | Latin America, Middle East & Africa | Long-term (2029-2033) |

High performance Adhesive Market Opportunities Analysis

The High performance Adhesive market is ripe with opportunities driven by evolving industrial needs and technological breakthroughs. A significant opportunity lies in the burgeoning demand for sustainable and bio-based adhesive solutions. As industries globally prioritize environmental responsibility, there is an increasing market pull for adhesives with reduced environmental footprints, offering a strong competitive edge for manufacturers investing in green chemistry. This includes the development of adhesives derived from renewable resources and those with lower VOC content, catering to stringent environmental regulations and corporate sustainability mandates. The expansion of 3D printing and additive manufacturing technologies also presents a novel opportunity, as these processes increasingly require specialized adhesives for bonding complex geometries and dissimilar materials, opening new avenues for customized adhesive formulations.

Furthermore, the rapid infrastructure development and urbanization in emerging economies, particularly in Asia Pacific and Latin America, are creating substantial demand for high-performance adhesives in the construction, automotive, and packaging sectors. These regions offer large, growing consumer bases and industrial capacities that are progressively adopting advanced manufacturing techniques. The medical and healthcare sectors also represent a high-growth opportunity, with increasing demand for biocompatible and sterile adhesives for medical devices, wearables, and surgical applications. Innovations in smart adhesives, capable of sensing environmental changes or structural integrity, further expand the market potential, promising new product categories and applications in intelligent systems and IoT devices. These diverse avenues underscore the dynamic and expansive nature of future growth in the high-performance adhesive sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based & Sustainable Adhesives | +1.3% | Europe, North America, Asia Pacific | Mid to Long-term (2027-2033) |

| Emerging Applications in 3D Printing and Additive Manufacturing | +1.0% | North America, Europe, Asia Pacific | Mid to Long-term (2028-2033) |

| Growth in Emerging Economies' Industrial and Construction Sectors | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Short to Mid-term (2025-2030) |

| Increasing Adoption in Electric Vehicles (EVs) and Battery Technologies | +0.7% | Asia Pacific, Europe, North America | Mid to Long-term (2027-2033) |

| Advancements in Smart Adhesives and Functional Coatings | +0.5% | North America, Europe | Long-term (2029-2033) |

High performance Adhesive Market Challenges Impact Analysis

The High performance Adhesive market faces several notable challenges that require strategic navigation from manufacturers and industry stakeholders. A primary challenge is the continuous need for innovation to meet increasingly specific and demanding application requirements. As industries like aerospace and electronics push the boundaries of materials and design, adhesives must evolve rapidly to bond advanced composites, dissimilar materials, and micro-components while withstanding extreme environmental conditions. This necessitates substantial and ongoing investment in research and development, which can be resource-intensive and carry high risks of failure. Furthermore, the inherent complexity of high-performance adhesive formulations often leads to high manufacturing costs, making it difficult for some solutions to compete with traditional joining methods on a purely cost-per-application basis, especially in price-sensitive markets.

Another significant challenge stems from the stringent regulatory frameworks governing the chemical industry, particularly concerning environmental health and safety. Compliance with varying global and regional regulations, such as REACH in Europe or EPA standards in North America, requires continuous reformulation efforts to eliminate or reduce hazardous substances, manage emissions, and ensure product safety throughout the supply chain. This regulatory burden not only adds to operational costs but can also delay market entry for new products. Additionally, the relatively longer curing times of some high-performance adhesives, compared to mechanical fasteners or other quick-set adhesives, can be a hurdle in high-speed production environments, limiting their widespread adoption in certain manufacturing processes that prioritize rapid throughput. Addressing these multifaceted challenges will be crucial for sustained growth and innovation in the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Need for Continuous R&D and Innovation to Meet Niche Demands | -0.9% | Global | Mid to Long-term (2026-2033) |

| High Initial Investment in Manufacturing and Application Equipment | -0.7% | Global | Short to Mid-term (2025-2029) |

| Competition from Traditional Fastening Methods and Alternative Materials | -0.6% | Global | Short to Mid-term (2025-2029) |

| Technical Expertise Required for Optimal Application and Performance | -0.5% | Developing Regions | Long-term (2028-2033) |

| Disposal and Recycling Challenges for Adhesive-Bonded Products | -0.4% | Europe, North America | Long-term (2029-2033) |

High performance Adhesive Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the High performance Adhesive market, covering its current status, historical trends, and future projections. The report offers detailed insights into market size, growth drivers, restraints, opportunities, and challenges, providing a holistic view for stakeholders. It encompasses thorough segmentation analysis by various factors such as resin type, technology, application, and end-use industry, alongside a detailed regional outlook. The study also profiles key market players, offering competitive intelligence and strategic recommendations for market entry and expansion.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.5 Billion |

| Market Forecast in 2033 | USD 28.0 Billion |

| Growth Rate | 7.65% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, Bostik (Arkema S.A.), Dow Inc., 3M Company, Huntsman Corporation, Avery Dennison Corporation, PPG Industries, Wacker Chemie AG, Lord Corporation (Parker Hannifin), BASF SE, ExxonMobil Chemical, Momentive Performance Materials Inc., Shin-Etsu Chemical Co., Ltd., Dupont de Nemours, Inc., Franklin International, ITW Performance Polymers, Dymax Corporation, Permabond LLC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The High performance Adhesive market is meticulously segmented to provide a granular understanding of its diverse components and their contributions to overall market dynamics. This segmentation is crucial for identifying specific growth pockets, understanding competitive landscapes within sub-sectors, and formulating targeted market strategies. The market is primarily categorized by resin type, technology, application, and end-use industry, each offering unique performance characteristics and catering to distinct industrial requirements. For instance, the choice of resin type often dictates the adhesive's strength, flexibility, and resistance to environmental factors, while the technology segment highlights the curing mechanisms and application methods.

The application and end-use industry segments provide insights into the functional roles of high-performance adhesives across various sectors. From bonding critical components in aerospace to providing structural integrity in construction or protecting sensitive electronics, each application demands specific adhesive properties. Understanding these segments enables manufacturers to tailor product development, sales, and marketing efforts more effectively, addressing the precise needs of each niche. This comprehensive segmentation framework allows for a detailed analysis of market trends, competitive positioning, and future opportunities across the entire high-performance adhesive value chain.

- By Resin Type:

- Epoxy: Known for high strength, chemical resistance, and excellent adhesion to various substrates.

- Acrylic: Offers fast curing, good adhesion to plastics, and flexibility.

- Polyurethane: Provides flexibility, impact resistance, and strong bonding to diverse materials.

- Silicone: Characterized by excellent temperature resistance, flexibility, and weatherability.

- Cyanoacrylate: Rapid-bonding, high-strength adhesive suitable for small area bonds.

- Others: Includes polyimide, rubber-based, and other specialized chemistries.

- By Technology:

- Water-based: Environmentally friendly, low VOC, used in packaging and construction.

- Solvent-based: Strong adhesion, fast drying, used where water resistance is critical.

- Hot Melt: Thermoplastic adhesives, fast setting, used in packaging and assembly.

- Reactive: Cured by chemical reaction (e.g., UV-cured, anaerobic, two-part epoxies), offering superior performance.

- Others: Includes pressure-sensitive adhesives (PSAs), film adhesives.

- By Application:

- Bonding: Primary application for joining materials.

- Sealing: Providing environmental protection and preventing leakage.

- Encapsulation: Protecting sensitive electronic components.

- Lamination: Bonding multiple layers of materials.

- Potting: Filling voids for insulation and protection.

- Others: Including gasketing, threadlocking, coating.

- By End-Use Industry:

- Automotive: Lightweighting, structural bonding, interior assembly.

- Electronics: Device assembly, component protection, thermal management.

- Construction: Structural glazing, flooring, roofing, panel bonding.

- Medical: Device assembly, disposable products, wound care.

- Packaging: Food and beverage packaging, flexible packaging.

- Aerospace: Fuselage assembly, interior components, lightweight structures.

- Industrial Assembly: Appliance manufacturing, machinery, tools.

- Footwear: Sole bonding, upper assembly.

- Others: Renewable energy (solar panels), marine, railway.

Regional Highlights

- North America: This region is a significant market for high-performance adhesives, driven by robust growth in the automotive, aerospace, and medical device sectors. The strong presence of research and development facilities, coupled with increasing demand for lightweight materials and advanced manufacturing technologies, contributes to market expansion. Strict environmental regulations also push demand for sustainable and low-VOC adhesive solutions.

- Europe: Europe represents a mature but highly innovative market, characterized by stringent environmental regulations and a strong focus on sustainability. The automotive, construction, and general industrial sectors are key consumers. The region leads in the development and adoption of bio-based and energy-efficient adhesive technologies, spurred by initiatives like the European Green Deal.

- Asia Pacific (APAC): APAC is the largest and fastest-growing market for high-performance adhesives, fueled by rapid industrialization, urbanization, and a booming manufacturing sector. Countries like China, India, Japan, and South Korea are major contributors, with high demand from electronics, automotive production, infrastructure development, and packaging industries. The region also serves as a global manufacturing hub, driving massive consumption.

- Latin America: This region is an emerging market for high-performance adhesives, with growth largely attributed to increasing investment in infrastructure projects, automotive manufacturing, and construction activities. Brazil and Mexico are key contributors, experiencing a growing adoption of advanced adhesive technologies to improve product quality and manufacturing efficiency.

- Middle East and Africa (MEA): The MEA region is experiencing steady growth in the high-performance adhesive market, primarily driven by substantial construction and infrastructure development projects, especially in the GCC countries. The diversification of economies away from oil and gas, coupled with investments in industrialization, is creating new opportunities for adhesive applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the High performance Adhesive Market.- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Bostik (Arkema S.A.)

- Dow Inc.

- 3M Company

- Huntsman Corporation

- Avery Dennison Corporation

- PPG Industries

- Wacker Chemie AG

- Lord Corporation (Parker Hannifin)

- BASF SE

- ExxonMobil Chemical

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- Dupont de Nemours, Inc.

- Franklin International

- ITW Performance Polymers

- Dymax Corporation

- Permabond LLC.

Frequently Asked Questions

What are High performance Adhesives?

High performance adhesives are advanced bonding agents designed to offer superior strength, durability, and resistance to extreme environmental conditions such as temperature fluctuations, moisture, chemicals, and stress. They are formulated using specialized chemistries to meet demanding industrial and critical application requirements where traditional adhesives may fail.

Which industries primarily use High performance Adhesives?

High performance adhesives are extensively utilized across various industries including automotive (for structural bonding and lightweighting), electronics (for component assembly and protection), aerospace (for aircraft structures), medical (for device assembly and biocompatible applications), construction (for structural glazing and flooring), and packaging.

What are the key drivers for the High performance Adhesive market growth?

The market is driven by increasing demand for lightweight and sustainable materials, miniaturization in electronics, advancements in manufacturing processes, and growing applications in medical devices and renewable energy. The replacement of traditional fasteners with adhesives for improved aesthetics and performance also contributes significantly.

What are the main challenges facing the High performance Adhesive market?

Key challenges include volatile raw material prices, stringent environmental regulations requiring reformulation, the need for continuous research and development to meet evolving application demands, and the technical expertise required for optimal adhesive application and performance.

What are the emerging trends in High performance Adhesives?

Emerging trends include the development of bio-based and sustainable adhesive solutions, the integration of smart functionalities (e.g., sensing capabilities), increasing adoption in 3D printing and additive manufacturing, and continued innovation to support electric vehicle production and battery technology.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted