SMT Placement Equipment Market

SMT Placement Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703925 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

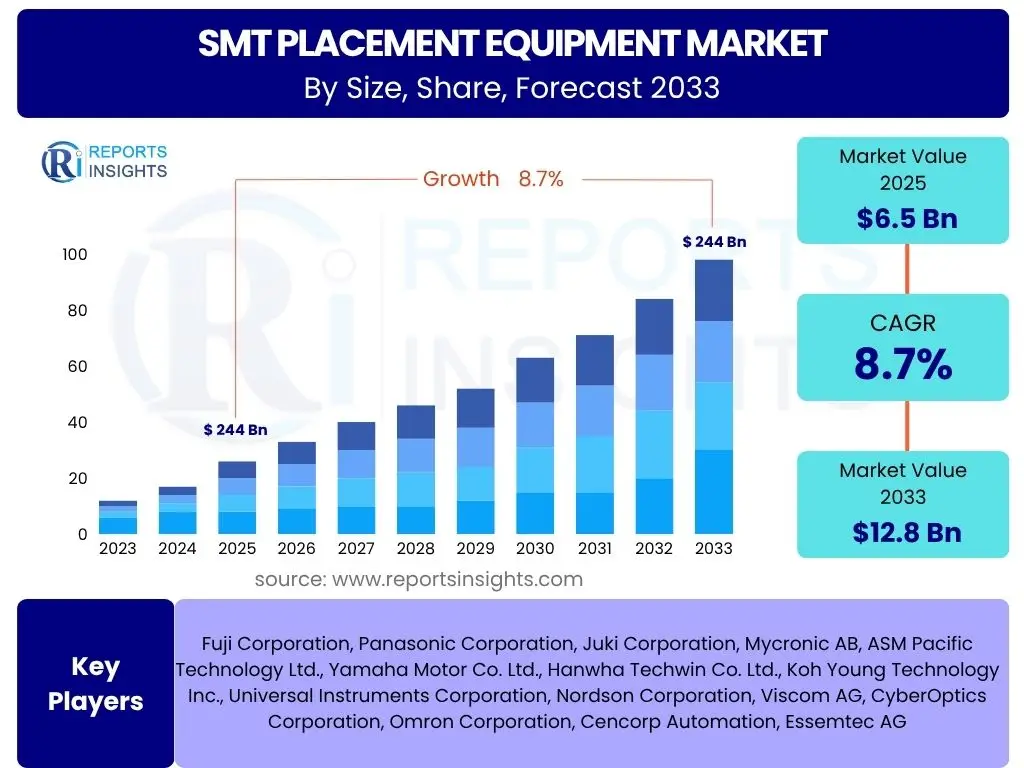

SMT Placement Equipment Market Size

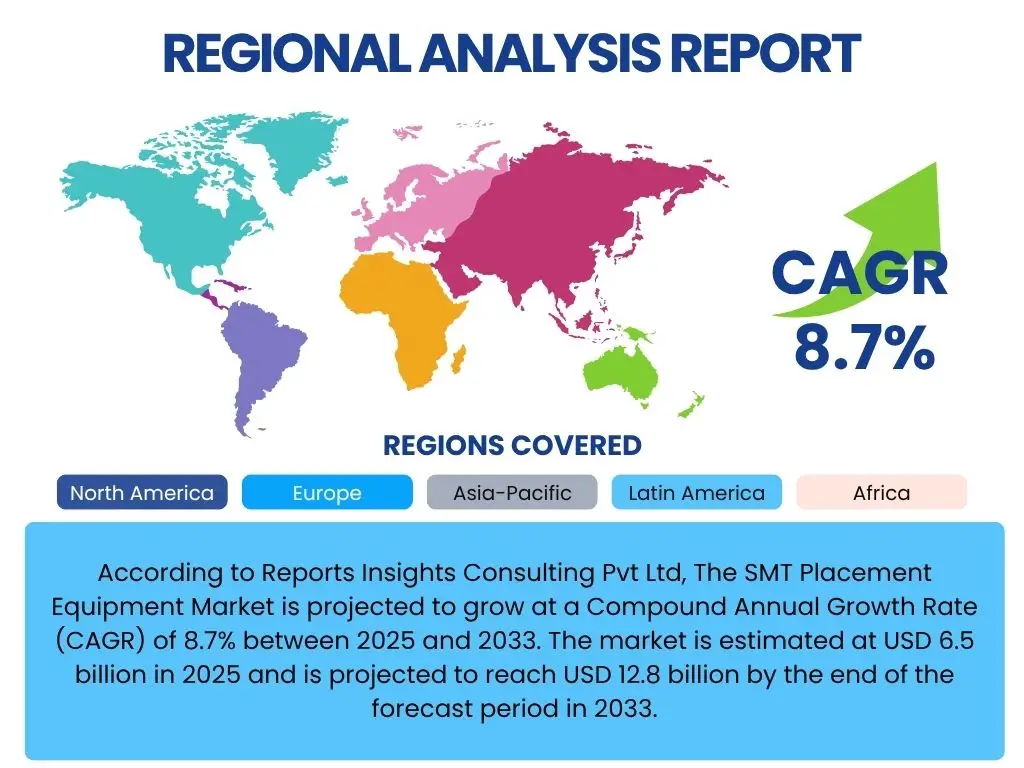

According to Reports Insights Consulting Pvt Ltd, The SMT Placement Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 6.5 billion in 2025 and is projected to reach USD 12.8 billion by the end of the forecast period in 2033.

Key SMT Placement Equipment Market Trends & Insights

The SMT Placement Equipment market is undergoing significant transformation driven by the escalating demand for advanced electronic devices and the continuous push towards miniaturization. Current user inquiries frequently revolve around the adoption of high-speed and high-precision placement technologies, as manufacturers seek to enhance production efficiency and yield. There is also a notable interest in modular and flexible SMT lines that can quickly adapt to diverse product specifications and production volumes, reflecting the dynamic nature of the electronics manufacturing landscape. Furthermore, questions related to the integration of Industry 4.0 principles, such as predictive maintenance, real-time monitoring, and data analytics, are becoming more prevalent as companies aim for smarter factory operations.

Another key area of user interest centers on sustainability and energy efficiency in SMT processes. Manufacturers are increasingly looking for equipment that not only offers high performance but also minimizes energy consumption and waste, aligning with global environmental regulations and corporate responsibility initiatives. The trend towards specialized placement solutions for emerging technologies like advanced packaging (e.g., System-in-Package, Chip-on-Board) and flexible electronics also garners attention, indicating a shift towards more complex and customized manufacturing capabilities. This collectively points to a market evolving towards greater automation, intelligence, and adaptability.

- Increased demand for high-speed and high-precision placement solutions.

- Growing adoption of modular and flexible SMT lines for diverse production needs.

- Integration of Industry 4.0 technologies, including IoT, AI, and Big Data analytics.

- Emphasis on energy efficiency and sustainable manufacturing processes.

- Development of specialized equipment for advanced packaging and flexible electronics.

- Expansion of automation and robotic solutions within SMT lines.

AI Impact Analysis on SMT Placement Equipment

User queries regarding the impact of Artificial Intelligence (AI) on SMT Placement Equipment predominantly focus on how AI can enhance operational efficiency, reduce errors, and optimize production workflows. A significant theme is the application of AI in predictive maintenance, where algorithms analyze sensor data from machines to anticipate potential failures, thereby minimizing downtime and extending equipment lifespan. Users are keen to understand how AI-driven vision systems can improve component recognition and placement accuracy, particularly for ultra-small or complex components, which directly translates to higher yield rates and reduced rework.

Furthermore, there is considerable interest in AI's role in optimizing production scheduling and line balancing. By processing vast amounts of production data, AI can suggest optimal component feeder arrangements, placement sequences, and machine configurations to maximize throughput and minimize bottlenecks. The concept of "self-optimizing" SMT lines, where AI continuously learns and adapts to changing production parameters, is also a key area of discussion. This extends to quality control, with AI-powered inspection systems offering more precise and faster defect detection than traditional methods, leading to superior product quality and reduced manufacturing costs.

- Enhanced predictive maintenance and fault diagnosis.

- Improved vision system accuracy for component recognition and placement.

- Optimization of production scheduling and line balancing.

- Real-time quality control and defect detection through AI-powered inspection.

- Adaptive learning for self-optimizing SMT lines.

- Automated programming and setup for quicker changeovers.

Key Takeaways SMT Placement Equipment Market Size & Forecast

The SMT Placement Equipment market is poised for robust growth, driven primarily by the relentless expansion of the electronics industry and the increasing complexity of electronic assemblies. A key takeaway from the market size and forecast is the significant investment in advanced manufacturing technologies, particularly those that offer higher precision, speed, and automation. Users frequently inquire about the segments expected to exhibit the highest growth, with consumer electronics, automotive electronics, and telecommunications identified as major contributors due to their continuous innovation cycles and demand for compact, high-performance devices. The shift towards miniaturization across various applications is a foundational element fueling this market's expansion, requiring sophisticated placement solutions.

Moreover, the forecast highlights a strong regional divergence in growth trajectories, with the Asia Pacific region maintaining its dominance as a manufacturing hub, while North America and Europe focus on high-value, niche applications and technological innovation. The increasing adoption of Industry 4.0 principles and the integration of artificial intelligence are not just trends but critical enablers that will shape the market's trajectory, leading to more efficient and resilient production lines. The competitive landscape is characterized by continuous R&D, with manufacturers striving to offer more versatile and intelligent equipment to meet evolving industry demands and secure market share. These factors collectively indicate a dynamic market with sustained growth potential driven by technological advancements and global electronics demand.

- Consistent growth propelled by global electronics demand and miniaturization trends.

- Strong investment in high-precision, high-speed, and automated placement solutions.

- Consumer electronics, automotive, and telecom sectors as primary growth drivers.

- Asia Pacific retains market leadership; North America and Europe focus on innovation.

- Industry 4.0 and AI integration are pivotal for future market development.

- Competitive landscape emphasizes R&D for versatile and intelligent equipment.

SMT Placement Equipment Market Drivers Analysis

The SMT Placement Equipment market is significantly propelled by the burgeoning demand for electronic devices across various sectors, coupled with the persistent trend towards miniaturization and higher functionality. The proliferation of smartphones, wearables, and advanced computing devices necessitates compact and densely packed circuit boards, driving the need for increasingly precise and efficient SMT placement machinery. Furthermore, the rapid expansion of the Internet of Things (IoT) ecosystem, encompassing smart home devices, industrial sensors, and connected vehicles, creates substantial demand for large-volume production of complex electronic modules, thereby stimulating investment in high-throughput SMT lines. The continuous evolution of consumer electronics, characterized by shorter product lifecycles and accelerated innovation, also compels manufacturers to adopt state-of-the-art SMT equipment capable of rapid changeovers and versatile production.

Another critical driver is the automotive industry's accelerating transition towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS), which are heavily reliant on sophisticated electronic control units (ECUs) and sensors. The stringent reliability and performance requirements of automotive electronics demand highly accurate and robust SMT placement processes. Similarly, the global rollout of 5G infrastructure is fueling the demand for new telecommunications equipment, including base stations and network devices, which require high-density component placement. The convergence of these factors underscores a robust and sustained demand for advanced SMT placement technologies, driving market expansion globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization and High-Density Packaging | +1.8% | Global, particularly APAC (China, Korea), North America | 2025-2033 |

| Growth of IoT and Connected Devices | +1.5% | Global | 2025-2033 |

| Expansion of Automotive Electronics (EVs, ADAS) | +1.2% | Europe, North America, APAC (Japan, China, South Korea) | 2025-2033 |

| 5G Infrastructure Rollout | +1.0% | APAC, North America, Europe | 2025-2030 |

| Industry 4.0 Adoption and Smart Factory Initiatives | +0.9% | Global, particularly developed economies | 2026-2033 |

SMT Placement Equipment Market Restraints Analysis

Despite the strong growth drivers, the SMT Placement Equipment market faces several notable restraints that can impede its expansion. One significant challenge is the high initial capital expenditure required for acquiring advanced SMT machines. These sophisticated systems, especially those offering high speed, precision, and automation, represent a substantial investment for manufacturers, particularly small and medium-sized enterprises (SMEs). This high cost can deter new entrants and limit the pace of technology upgrades for existing players, especially in regions with tighter financial constraints or less developed manufacturing infrastructures. The complexity of operating and maintaining these machines also necessitates highly skilled labor, which can be a bottleneck in regions facing a shortage of trained technicians and engineers, adding to operational costs and potential downtime.

Furthermore, geopolitical uncertainties and trade tensions can disrupt global supply chains, affecting the availability of critical components and materials required for SMT equipment manufacturing. This can lead to increased production costs, extended lead times, and reduced profit margins for equipment vendors. Economic slowdowns and fluctuating consumer spending patterns can also dampen the demand for electronic products, thereby reducing the need for new SMT placement equipment. The intense competition within the market, characterized by rapid technological advancements and price pressures, further challenges manufacturers to continuously innovate while maintaining competitive pricing, potentially impacting profitability and market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -1.5% | Global, more pronounced in emerging markets | 2025-2033 |

| Shortage of Skilled Labor | -1.0% | Global, particularly North America, Europe, parts of APAC | 2025-2033 |

| Global Economic Volatility and Supply Chain Disruptions | -0.8% | Global | 2025-2028 |

| Intense Market Competition and Price Pressures | -0.7% | Global | 2025-2033 |

SMT Placement Equipment Market Opportunities Analysis

The SMT Placement Equipment market is rich with opportunities driven by technological advancements and evolving industry needs. One significant opportunity lies in the burgeoning demand for specialized SMT equipment tailored for advanced packaging technologies, such as System-in-Package (SiP), Chip-on-Board (COB), and fan-out wafer-level packaging (FOWLP). As electronics continue to miniaturize and integrate more functionalities, the need for precision placement of complex and sensitive components within tight spaces creates a niche for highly specialized and accurate SMT machines. The expansion into new and emerging markets, particularly in Southeast Asia, Latin America, and parts of Africa, offers untapped potential as these regions develop their manufacturing capabilities and increase local electronics production. These markets often seek cost-effective yet reliable solutions, presenting opportunities for both new and refurbished equipment providers.

Another promising area is the development of SMT solutions specifically designed for flexible and wearable electronics. The unique substrates and form factors of these devices require adapted placement techniques and equipment that can handle non-rigid materials without compromising accuracy or speed. Furthermore, the growing focus on sustainability and energy efficiency within manufacturing presents an opportunity for equipment manufacturers to innovate and offer greener SMT solutions. This includes developing machines with lower power consumption, reduced material waste, and capabilities for rework or recycling, aligning with global environmental regulations and corporate sustainability goals. The increasing adoption of automation and robotics in general manufacturing also offers a synergistic opportunity for SMT equipment providers to integrate their systems more deeply into fully automated production lines, offering end-to-end solutions that enhance overall factory efficiency and reduce manual intervention.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Demand for Advanced Packaging Solutions | +1.4% | Global, particularly North America, APAC (Taiwan, Korea) | 2026-2033 |

| Growth in Emerging Manufacturing Hubs | +1.1% | Southeast Asia, India, Latin America | 2025-2033 |

| Flexible and Wearable Electronics Manufacturing | +0.9% | Global, particularly North America, Europe, APAC | 2027-2033 |

| Focus on Energy Efficiency and Sustainable Production | +0.8% | Europe, North America, Japan | 2026-2033 |

| Integration with Fully Automated Production Lines | +0.7% | Global | 2025-2033 |

SMT Placement Equipment Market Challenges Impact Analysis

The SMT Placement Equipment market faces several significant challenges that necessitate strategic responses from manufacturers. One primary challenge is the rapid pace of technological obsolescence. As electronic components become smaller and more complex, and new manufacturing techniques emerge, existing SMT equipment can quickly become outdated, requiring frequent and costly upgrades or replacements. This continuous need for innovation and adaptation puts immense pressure on R&D budgets and can strain manufacturers' financial resources. Another critical challenge is maintaining high levels of precision and reliability amidst increasing production speeds and miniaturization. The margin for error is shrinking, and any deviation in placement accuracy can lead to significant yield losses and increased rework, demanding sophisticated machine vision systems and robust control algorithms.

Furthermore, managing complex global supply chains for components and raw materials remains a persistent challenge, susceptible to geopolitical tensions, natural disasters, and pandemics, leading to potential delays and cost escalations. The intense competitive landscape, characterized by numerous global and regional players, also poses a significant challenge, driving down profit margins and necessitating continuous differentiation through innovation and superior customer service. Ensuring compliance with evolving international regulations, particularly concerning environmental standards, data privacy (for connected machines), and labor safety, adds another layer of complexity for SMT equipment manufacturers operating globally. Overcoming these challenges requires agile development, robust quality control, and strategic partnerships across the value chain.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -1.2% | Global | 2025-2033 |

| Maintaining Precision with High Throughput | -1.0% | Global | 2025-2033 |

| Supply Chain Vulnerability | -0.9% | Global | 2025-2028 |

| Intensifying Competition and Price Sensitivity | -0.8% | Global | 2025-2033 |

| Evolving Regulatory Compliance | -0.6% | Europe, North America, Asia | 2025-2033 |

SMT Placement Equipment Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the SMT Placement Equipment market, offering an exhaustive analysis of market size, growth trends, and future projections. It provides an in-depth understanding of the key drivers, restraints, opportunities, and challenges shaping the industry, alongside a detailed segmentation analysis. The report's scope extends to cover the impact of emerging technologies such as Artificial Intelligence and Industry 4.0 on market evolution, offering strategic insights for stakeholders. It also includes a thorough competitive landscape analysis, profiling leading companies and their strategic initiatives to provide a holistic view of the market's structure and potential for growth.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.5 billion |

| Market Forecast in 2033 | USD 12.8 billion |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Fuji Corporation, Panasonic Corporation, Juki Corporation, Mycronic AB, ASM Pacific Technology Ltd., Yamaha Motor Co. Ltd., Hanwha Techwin Co. Ltd., Koh Young Technology Inc., Universal Instruments Corporation, Nordson Corporation, Viscom AG, CyberOptics Corporation, Omron Corporation, Cencorp Automation, Essemtec AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The SMT Placement Equipment market is comprehensively segmented to provide a nuanced understanding of its various facets and their respective contributions to the overall market landscape. These segmentations are critical for identifying specific growth pockets, understanding regional preferences, and analyzing competitive strategies tailored to different product types, technologies, and applications. The segmentation by type reflects the diverse range of machines available, each optimized for specific component sizes, placement speeds, and production volumes, from high-throughput chip shooters to versatile multi-functional placers. The distinction by technology highlights the advancements in pick-and-place mechanisms, incorporating robotics and integrated inspection systems to enhance accuracy and efficiency. Furthermore, the market is differentiated by application, categorizing the demand from various end-use industries, which are the primary drivers of innovation and adoption in this sector. This detailed breakdown enables a precise assessment of market opportunities and challenges across the spectrum of SMT manufacturing.

- By Type: Chip Shooters, Multi-functional Placers, Flexible Placers, High-speed Placers, Others

- By Head Type: Single-head, Dual-head, Multi-head

- By Technology: Pick and Place (PnP), Robotic Placement, Automated Optical Inspection (AOI) Integrated

- By Mounting Type: Surface Mount Technology (SMT), Through-Hole Technology (THT)

- By Application: Consumer Electronics, Automotive Electronics, Telecommunications, Medical Devices, Industrial Electronics, Aerospace & Defense, Others

- By End-Use Industry: Original Equipment Manufacturers (OEMs), Electronic Manufacturing Services (EMS) Providers

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to its robust electronics manufacturing base, presence of major EMS providers, and high demand from consumer electronics and automotive sectors. Countries like China, South Korea, Japan, and Taiwan are key contributors to both production and consumption. The region benefits from lower manufacturing costs and government initiatives supporting electronics production.

- North America: Characterized by significant R&D investments and adoption of advanced SMT technologies, particularly for high-value applications in aerospace, defense, medical devices, and high-performance computing. The region focuses on innovation, automation, and the development of specialized solutions for complex assemblies.

- Europe: Exhibits strong growth driven by the automotive industry, industrial electronics, and the push towards Industry 4.0. Germany, France, and the UK are key markets, emphasizing precision engineering, automation, and sustainable manufacturing practices in SMT processes.

- Latin America: An emerging market for SMT equipment, witnessing increased investment in local electronics manufacturing, particularly in Brazil and Mexico, driven by growing consumer demand and foreign investments. The focus is on expanding production capabilities and adopting more efficient manufacturing processes.

- Middle East and Africa (MEA): Represents a nascent but growing market, with increasing government initiatives to diversify economies and establish local manufacturing bases. Investments in telecommunications infrastructure and domestic consumer electronics assembly are driving gradual adoption of SMT equipment in select countries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the SMT Placement Equipment Market.- Fuji Corporation

- Panasonic Corporation

- Juki Corporation

- Mycronic AB

- ASM Pacific Technology Ltd.

- Yamaha Motor Co. Ltd.

- Hanwha Techwin Co. Ltd.

- Koh Young Technology Inc.

- Universal Instruments Corporation

- Nordson Corporation

- Viscom AG

- CyberOptics Corporation

- Omron Corporation

- Cencorp Automation

- Essemtec AG

Frequently Asked Questions

Analyze common user questions about the SMT Placement Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is SMT Placement Equipment?

SMT Placement Equipment refers to machinery used in Surface Mount Technology (SMT) to accurately place electronic components onto printed circuit boards (PCBs). These machines are critical for automated electronics manufacturing, handling components ranging from microchips to resistors at high speeds and precision.

What are the primary drivers of growth for the SMT Placement Equipment market?

Key growth drivers include the increasing demand for miniaturized electronic devices, the expansion of IoT and connected devices, the rapid growth of automotive electronics (EVs, ADAS), and the global rollout of 5G infrastructure, all requiring advanced component placement solutions.

How is Artificial Intelligence impacting SMT Placement Equipment?

AI is significantly impacting SMT equipment by enabling predictive maintenance, improving vision system accuracy for component recognition, optimizing production scheduling, and enhancing real-time quality control and defect detection, leading to more intelligent and efficient manufacturing.

Which regions are leading in the SMT Placement Equipment market?

The Asia Pacific region, particularly countries like China, South Korea, and Japan, currently dominates the SMT Placement Equipment market due to its extensive electronics manufacturing base and high production volumes. North America and Europe are also key markets, focusing on technological innovation and high-value applications.

What are the main challenges facing the SMT Placement Equipment market?

Major challenges include the high initial capital investment for advanced machinery, a shortage of skilled labor, vulnerability to global supply chain disruptions, intense market competition leading to price pressures, and the rapid pace of technological obsolescence.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted