Pressure Vacuum Breaker Market

Pressure Vacuum Breaker Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710187 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

Pressure Vacuum Breaker Market Size

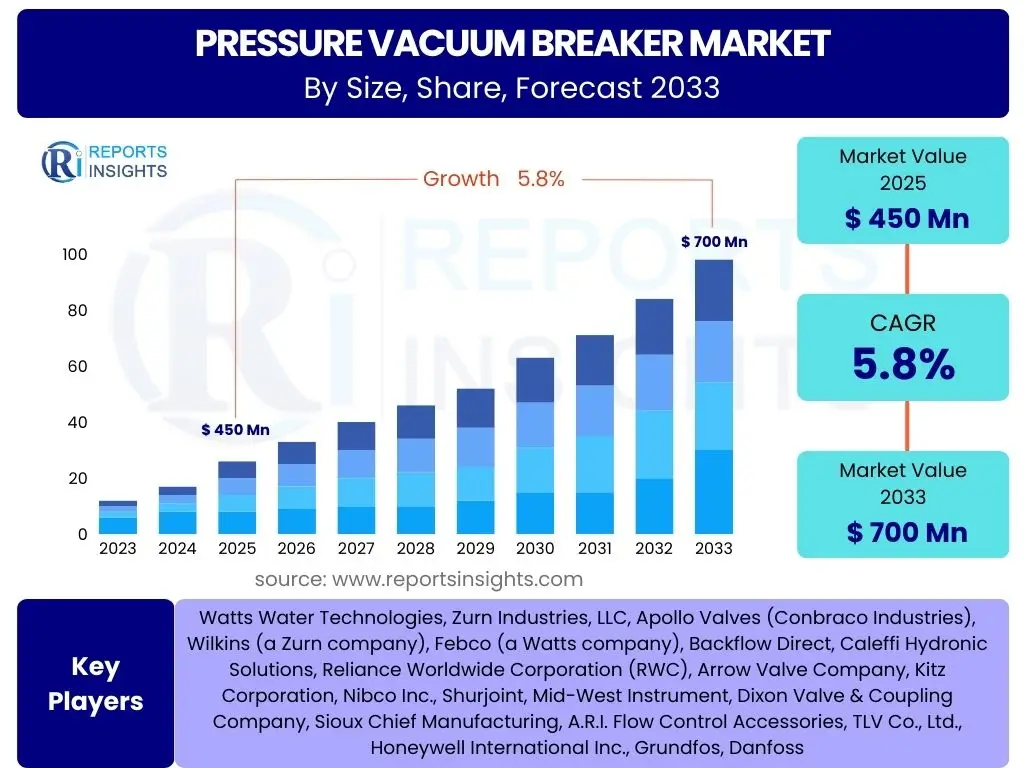

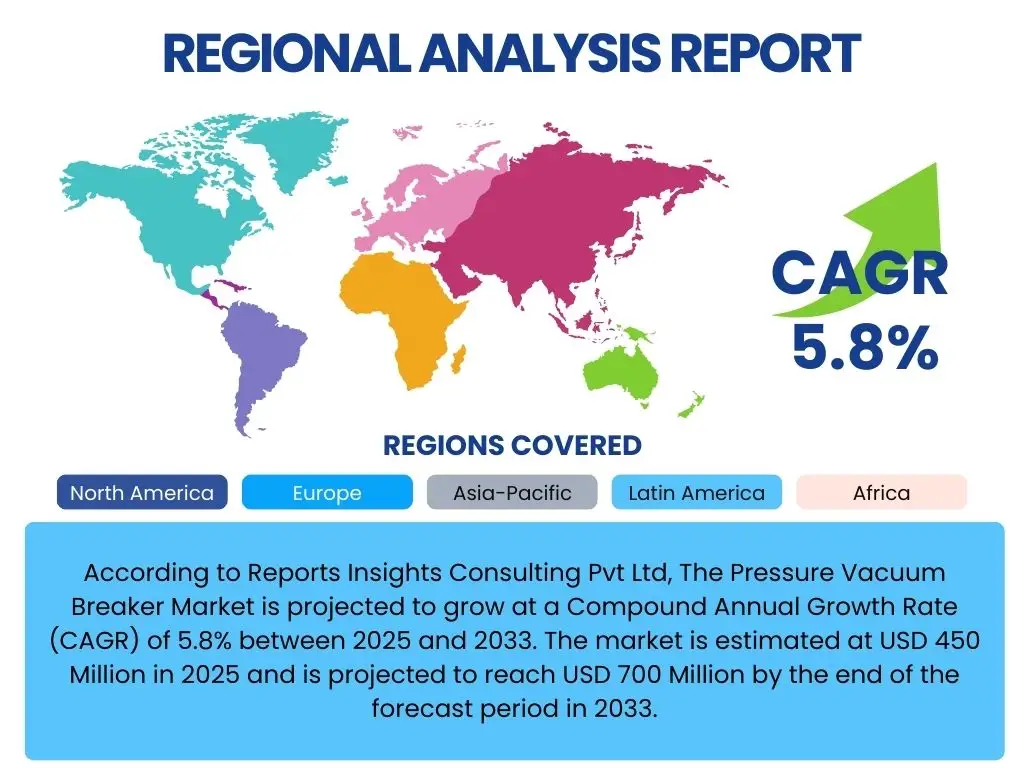

According to Reports Insights Consulting Pvt Ltd, The Pressure Vacuum Breaker Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 700 Million by the end of the forecast period in 2033.

Key Pressure Vacuum Breaker Market Trends & Insights

The Pressure Vacuum Breaker market is experiencing growth driven by an increasing emphasis on water safety and stringent regulatory compliance globally. Governments and municipal authorities are enacting stricter codes for backflow prevention in potable water systems, residential, commercial, and industrial applications. This regulatory push ensures the protection of public health by preventing contamination of the water supply, thereby creating a sustained demand for reliable pressure vacuum breaker devices.

Furthermore, the ongoing development of urban infrastructure, coupled with the modernization of existing water distribution networks, significantly contributes to market expansion. As smart city initiatives gain traction, the integration of advanced monitoring and control systems with backflow prevention devices is emerging as a key trend, enhancing efficiency and proactive maintenance. The demand for durable and low-maintenance solutions, capable of withstanding varying environmental conditions, also shapes product development and market dynamics.

- Increasing stringency of water safety regulations and codes globally.

- Growing investments in urban development and water infrastructure projects.

- Rising adoption of smart water management systems incorporating backflow prevention.

- Shift towards advanced materials for enhanced product durability and longevity.

- Heightened awareness among consumers and businesses regarding water contamination risks.

- Expansion of applications in non-potable water systems like irrigation and industrial processes.

AI Impact Analysis on Pressure Vacuum Breaker

Artificial Intelligence (AI) is transforming various industrial sectors, and while its direct impact on the mechanical function of pressure vacuum breakers (PVBs) is limited, its influence on the broader water management ecosystem in which PVBs operate is substantial. AI-driven analytics can optimize the performance and maintenance schedules of entire water distribution networks, identifying potential issues before they escalate and ensuring the sustained integrity of backflow prevention systems. This includes predictive maintenance for PVBs, where AI algorithms analyze sensor data to forecast equipment failures, thus extending their operational lifespan and reducing unexpected repair costs.

Moreover, AI contributes to enhanced compliance and operational efficiency within smart water infrastructure. By integrating PVB monitoring data with AI platforms, operators can gain real-time insights into system health, identify patterns indicative of backflow events, and automate reporting for regulatory bodies. This not only streamlines compliance processes but also improves the overall resilience and safety of water supplies, enabling more proactive management of critical water assets. The manufacturing processes for PVBs can also leverage AI for quality control and optimized production, ensuring higher product reliability.

- AI-driven predictive maintenance for pressure vacuum breakers and associated systems.

- Enhanced real-time monitoring and data analytics for compliance with water safety regulations.

- Integration of PVB performance data into smart water management platforms for optimized network operations.

- Automation of reporting and auditing for backflow prevention device status.

- Improved quality control and manufacturing efficiency through AI-powered production processes.

Key Takeaways Pressure Vacuum Breaker Market Size & Forecast

The Pressure Vacuum Breaker market is poised for steady and sustainable growth throughout the forecast period, primarily driven by an increasing global emphasis on public health and the critical need to protect potable water supplies from contamination. Regulatory bodies worldwide are continuously updating and enforcing stricter standards for backflow prevention, making the installation and regular maintenance of PVBs mandatory across a diverse range of applications. This regulatory environment creates a foundational demand that ensures the market's stability and consistent expansion.

Furthermore, significant investments in both new construction and the modernization of aging infrastructure are contributing substantially to market demand. As urban areas expand and existing water systems require upgrades, the necessity for robust and reliable backflow prevention devices becomes paramount. The market's resilience is also bolstered by ongoing technological advancements focused on improving product durability, ease of installation, and integration with advanced water management systems, indicating a future of innovation within this essential component of water safety.

- Consistent market expansion is anticipated, primarily fueled by stringent global water safety regulations.

- Infrastructure development and renovation projects are key drivers for increased PVB adoption.

- Growing awareness of waterborne contamination risks underscores the importance of backflow prevention.

- Technological advancements in materials and smart system integration will enhance product efficacy and market value.

- The market represents a critical component within the broader water and sanitation industry.

Pressure Vacuum Breaker Market Drivers Analysis

The Pressure Vacuum Breaker market is propelled by several robust drivers, fundamentally rooted in public health imperatives, infrastructure development, and regulatory frameworks. The increasing global awareness of waterborne diseases and the necessity of preventing cross-contamination in potable water systems mandates the installation of backflow prevention devices like PVBs. This heightened focus on water quality and safety serves as a primary impetus, driving demand across residential, commercial, and industrial sectors. Additionally, the continuous expansion of urban areas and the corresponding development of new water infrastructure, coupled with the need to modernize or replace aging systems, create consistent demand for these essential devices.

Regulatory mandates issued by governmental bodies and municipal water authorities are perhaps the most significant market driver. These regulations often specify the types of backflow prevention devices required for various applications and dictate regular inspection and maintenance schedules, ensuring a steady aftermarket for services and replacements. Furthermore, the growth in specific applications such as irrigation systems, fire protection, and industrial processing, where PVBs play a crucial role in protecting the main water supply, also contributes substantially to market expansion. The cumulative effect of these drivers creates a resilient and growing market landscape.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Regulatory Mandates for Water Safety | +1.5% | Global | Long-term |

| Growth in Construction Sector (Residential, Commercial, Industrial) | +1.2% | North America, Asia Pacific | Medium-term |

| Aging Water Infrastructure and Replacement Needs | +1.0% | Europe, North America | Long-term |

| Increasing Awareness of Water Contamination Risks | +0.8% | Global | Medium-term |

| Expansion of Irrigation Systems and Fire Protection Applications | +0.7% | Global | Medium-term |

Pressure Vacuum Breaker Market Restraints Analysis

Despite its critical role, the Pressure Vacuum Breaker market faces certain restraints that could temper its growth trajectory. One significant factor is the relatively high initial installation cost associated with these devices, particularly when integrating them into existing complex plumbing systems. This cost can be a deterrent for smaller businesses or residential property owners, especially in regions with less stringent enforcement of backflow prevention codes. The specialized nature of PVB installation and maintenance also requires certified professionals, adding to the overall expense and potentially limiting adoption where skilled labor is scarce or expensive.

Another restraint stems from the competitive landscape, where alternative backflow prevention devices, such as double check valve assemblies or reduced pressure zone assemblies, offer different cost-benefit profiles and application suitability. These alternatives can sometimes be preferred based on specific local codes, pressure requirements, or space constraints, creating market fragmentation. Furthermore, a lack of widespread awareness regarding the specific benefits and operational requirements of PVBs in certain developing regions can hinder market penetration, requiring ongoing educational efforts to overcome this barrier.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Installation and Maintenance Costs | -0.7% | Developing Regions, Cost-Sensitive Markets | Short-term |

| Availability of Alternative Backflow Prevention Devices | -0.6% | Global | Medium-term |

| Lack of Awareness and Enforcement in Certain Geographies | -0.5% | Middle East & Africa, Latin America | Long-term |

| Complexity of Installation and Requirement for Certified Professionals | -0.4% | Global | Short-term |

| Economic Downturns Affecting Construction Spending | -0.3% | Global | Short-term |

Pressure Vacuum Breaker Market Opportunities Analysis

The Pressure Vacuum Breaker market is rich with opportunities stemming from evolving technological landscapes, burgeoning infrastructure needs, and a heightened global consciousness towards environmental and public health concerns. A significant opportunity lies in the integration of PVBs into smart water management systems. As cities and industrial complexes increasingly adopt IoT-enabled infrastructure, there is a growing demand for backflow prevention devices that can offer real-time monitoring, remote diagnostics, and data analytics capabilities. This shift towards smart systems not only enhances efficiency and compliance but also creates new revenue streams for manufacturers offering advanced, connected solutions.

Furthermore, the expanding focus on sustainable water practices and resource management globally opens avenues for PVBs in non-traditional applications, such as graywater recycling systems and rainwater harvesting. These systems require robust backflow prevention to ensure that non-potable water sources do not contaminate the main supply, thereby driving demand in emerging green building and water conservation initiatives. Developing and offering products made from advanced, corrosion-resistant materials, or with modular designs that simplify maintenance, also presents a substantial opportunity to capture market share by addressing pain points of durability and serviceability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Smart Water Management and IoT Systems | +1.0% | North America, Europe, Asia Pacific | Long-term |

| Development of Advanced, Corrosion-Resistant Materials | +0.8% | Global | Medium-term |

| Expansion into Emerging Markets with Growing Infrastructure | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

| Retrofit and Renovation Projects for Aging Infrastructure | +0.7% | North America, Europe | Medium-term |

| Adoption in Green Building and Sustainable Water Practices (e.g., Graywater Systems) | +0.6% | Global | Long-term |

Pressure Vacuum Breaker Market Challenges Impact Analysis

The Pressure Vacuum Breaker market, while promising, contends with several significant challenges that necessitate strategic navigation by industry participants. One primary challenge involves the continuous evolution and increasing complexity of regulatory standards across different jurisdictions. Manufacturers and installers must remain constantly updated with varying local, national, and international codes, which can lead to compliance complexities and potential product redesigns or installation adjustments. This dynamic regulatory environment demands significant investment in research, testing, and certification to ensure product marketability and adherence to legal requirements.

Furthermore, intense price competition within the established segments of the market presents a considerable hurdle, particularly for new entrants or smaller players. The commoditization of standard PVB units can drive down profit margins, compelling companies to innovate with value-added features or focus on niche applications to differentiate their offerings. Supply chain disruptions, often exacerbated by global events or geopolitical tensions, also pose an ongoing challenge, affecting the availability of raw materials, manufacturing costs, and ultimately, product delivery timelines. Addressing these multifaceted challenges requires a blend of regulatory foresight, cost-efficiency, and supply chain resilience strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Compliance with Evolving and Varied Regulatory Standards | -0.5% | Global | Ongoing |

| Intense Price Competition and Market Commoditization | -0.6% | Global | Short-term |

| Skilled Labor Shortage for Installation and Maintenance | -0.4% | Global | Medium-term |

| Supply Chain Volatility and Raw Material Price Fluctuations | -0.3% | Global | Short-term |

| Educating End-Users and Regulators on Advanced Solutions | -0.2% | Developing Regions | Long-term |

Pressure Vacuum Breaker Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Pressure Vacuum Breaker Market, covering historical data, current market dynamics, and future projections. It delivers crucial insights into market size, growth drivers, restraints, opportunities, and challenges, offering a holistic view of the industry landscape. The report also includes detailed segmentation analysis by material, end-use industry, application, and pressure range, alongside a thorough regional assessment to pinpoint key growth areas and competitive strategies. Furthermore, the study profiles leading market players, analyzing their business strategies, product portfolios, and market positions to offer a complete competitive intelligence framework.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 700 Million |

| Growth Rate | 5.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Watts Water Technologies, Zurn Industries, LLC, Apollo Valves (Conbraco Industries), Wilkins (a Zurn company), Febco (a Watts company), Backflow Direct, Caleffi Hydronic Solutions, Reliance Worldwide Corporation (RWC), Arrow Valve Company, Kitz Corporation, Nibco Inc., Shurjoint, Mid-West Instrument, Dixon Valve & Coupling Company, Sioux Chief Manufacturing, A.R.I. Flow Control Accessories, TLV Co., Ltd., Honeywell International Inc., Grundfos, Danfoss |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Pressure Vacuum Breaker market is intricately segmented across various dimensions to provide a granular understanding of its structure and dynamics. These segments enable a detailed analysis of specific market niches, consumer preferences, and technological advancements tailored to particular requirements. Understanding these segmentations is crucial for manufacturers to optimize product development, for distributors to refine their sales strategies, and for end-users to select the most appropriate backflow prevention solutions for their applications. The primary segmentation categories include material type, end-use industry, application area, and pressure range, each presenting unique market characteristics and growth trajectories.

The material segment reflects advancements in engineering to enhance durability and performance, while the end-use industry and application segments highlight the diverse sectors reliant on PVBs for water safety and compliance. The pressure range classification caters to the technical specifications required for different hydraulic systems, ensuring that appropriate devices are matched to operating conditions. This multi-faceted segmentation allows for a comprehensive assessment of market opportunities and challenges within each specific sub-market, aiding in targeted strategic planning and investment decisions across the value chain.

- By Material: This segment examines the market based on the primary construction material, influencing durability, cost, and application suitability.

- Bronze: Traditional, durable, and corrosion-resistant, often used in larger commercial and industrial applications.

- PVC: Cost-effective and lightweight, popular in residential and irrigation systems.

- Stainless Steel: Offers superior corrosion resistance, suitable for harsh environments or specific industrial applications.

- Others (e.g., Engineered Plastics): Emerging materials offering specific benefits such as UV resistance or specialized chemical compatibility.

- By End-Use Industry: This segment categorizes demand based on the sector utilizing PVBs.

- Residential: Homes, apartments, and multi-family dwellings.

- Commercial: Office buildings, retail spaces, hotels, restaurants.

- Industrial: Manufacturing plants, processing facilities, power generation.

- Municipal: Public water systems, parks, government buildings.

- By Application: This segment focuses on the specific use cases for PVBs.

- Irrigation Systems: Protecting potable water from contamination by fertilizers and pesticides.

- Fire Protection Systems: Preventing backflow from fire sprinkler systems into the main water supply.

- Potable Water Systems: General residential and commercial connections where back-siphonage is a risk.

- Industrial Processes: Specific manufacturing or chemical processes requiring water supply protection.

- HVAC Systems: Preventing contamination from heating, ventilation, and air conditioning units.

- Others: Includes applications like laboratory equipment, car washes, and utility sinks.

- By Pressure Range: This segment differentiates devices based on their operational pressure limits.

- Low Pressure: Suitable for systems with lower static or operating pressures.

- Medium Pressure: Covers a broad range of common applications.

- High Pressure: Designed for robust systems with elevated pressure requirements.

Regional Highlights

The global Pressure Vacuum Breaker market exhibits distinct regional dynamics, influenced by varying regulatory landscapes, infrastructure development levels, and economic conditions. Each region presents a unique set of drivers and opportunities that shape market growth and competitive strategies. Understanding these regional nuances is essential for market players to effectively target their efforts and capitalize on localized demand. The key regions analyzed include North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa, each contributing significantly to the overall market trajectory.

North America and Europe, characterized by mature markets, stringent regulatory frameworks, and aging infrastructure, focus heavily on replacement and retrofit activities, alongside the adoption of advanced, smart solutions. In contrast, the Asia Pacific region is a high-growth market driven by rapid urbanization, extensive infrastructure development, and increasing awareness of water quality. Latin America and the Middle East and Africa represent emerging markets with substantial long-term growth potential, as these regions address burgeoning population needs and invest in modernizing their water and sanitation systems.

- North America: Dominates the market due to robust regulatory enforcement, high awareness of water safety, and significant investments in maintaining and upgrading aging water infrastructure. The region also leads in the adoption of smart water management technologies.

- Europe: Characterized by strong environmental protection laws and an emphasis on public health, driving consistent demand for backflow prevention. Renovation projects and a focus on sustainable water practices further contribute to market stability.

- Asia Pacific (APAC): Represents the fastest-growing region, fueled by rapid urbanization, industrialization, and massive infrastructure development projects. Increasing government initiatives for clean water supply and rising disposable incomes also propel market expansion.

- Latin America: An emerging market with growing investments in public utilities and residential construction. Rising awareness regarding water quality and the implementation of basic regulatory frameworks are driving demand.

- Middle East and Africa (MEA): This region is experiencing growth due to significant investments in new urban developments, particularly in the GCC countries, alongside efforts to address water scarcity challenges and improve water distribution networks.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pressure Vacuum Breaker Market.- Watts Water Technologies

- Zurn Industries, LLC

- Apollo Valves (Conbraco Industries)

- Wilkins (a Zurn company)

- Febco (a Watts company)

- Backflow Direct

- Caleffi Hydronic Solutions

- Reliance Worldwide Corporation (RWC)

- Arrow Valve Company

- Kitz Corporation

- Nibco Inc.

- Shurjoint

- Mid-West Instrument

- Dixon Valve & Coupling Company

- Sioux Chief Manufacturing

- A.R.I. Flow Control Accessories

- TLV Co., Ltd.

- Honeywell International Inc.

- Grundfos

- Danfoss

Frequently Asked Questions

What is a Pressure Vacuum Breaker (PVB)?

A Pressure Vacuum Breaker (PVB) is a type of backflow prevention device designed to protect potable water supplies from contamination caused by back-siphonage. It features a check valve to prevent backflow and an air inlet valve that opens when system pressure drops, introducing air to break the vacuum and prevent contaminated water from being drawn back into the main supply.

How does a Pressure Vacuum Breaker work?

A PVB operates by utilizing a spring-loaded check valve and an independently acting, spring-loaded air inlet valve. When water flows in the correct direction, the check valve opens. If system pressure drops (a back-siphonage condition), the check valve closes, and the air inlet valve opens, admitting atmospheric air into the system. This breaks the vacuum, preventing non-potable water from being siphoned back into the clean water supply.

Where are Pressure Vacuum Breakers commonly used?

Pressure Vacuum Breakers are most commonly used in applications where the potential for back-siphonage exists and the backflow preventer can be installed at least 12 inches above the highest point of water usage downstream. Typical applications include irrigation systems, lawn sprinklers, fire protection systems, and certain industrial or commercial potable water connections, especially those involving continuous pressure.

What are the key benefits of using a Pressure Vacuum Breaker?

The primary benefit of a PVB is its effective prevention of back-siphonage, thereby safeguarding public health by protecting potable water supplies from contamination. They are relatively simple in design, easier to maintain and test compared to some other backflow devices, and provide reliable protection for various applications where a continuous pressure hazard is present.

How often should a Pressure Vacuum Breaker be tested and maintained?

Most regulatory codes and manufacturers recommend that Pressure Vacuum Breakers be tested annually by a certified backflow prevention device tester. Regular testing ensures the device is functioning correctly and efficiently. Maintenance typically involves inspecting for leaks, checking valve components, and replacing worn parts as needed to ensure optimal performance and compliance with water safety standards.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted