Geotechnical and Structural Monitoring Device Market

Geotechnical and Structural Monitoring Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709325 | Last Updated : December 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Geotechnical and Structural Monitoring Device Market Size

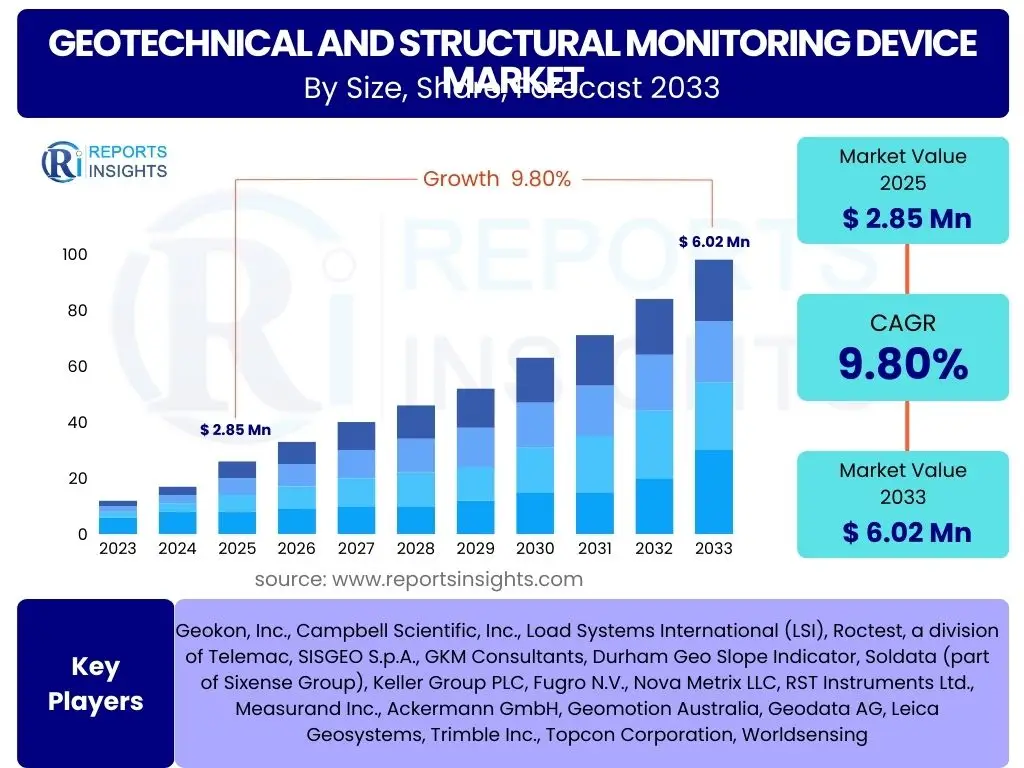

According to Reports Insights Consulting Pvt Ltd, The Geotechnical and Structural Monitoring Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 2.85 Billion in 2025 and is projected to reach USD 6.02 Billion by the end of the forecast period in 2033.

This growth trajectory is underpinned by an increasing global emphasis on infrastructure safety, predictive maintenance, and resilience against natural disasters. The demand for sophisticated monitoring solutions is expanding across various sectors, including civil engineering, mining, energy, and transportation, as stakeholders seek to mitigate risks and ensure the long-term integrity of critical assets. Advancements in sensor technology, data analytics, and communication protocols are also contributing significantly to the market's expansion.

Key Geotechnical and Structural Monitoring Device Market Trends & Insights

Common user questions regarding market trends highlight a strong interest in technological advancements, integration capabilities, and the move towards more proactive monitoring strategies. Users frequently inquire about the latest innovations in sensor technology, the role of data analytics in predictive maintenance, and the adoption of wireless and remote monitoring systems. There is also significant curiosity about how these devices are being applied in urban development, critical infrastructure projects, and environmental monitoring to address evolving safety and operational challenges.

The market is experiencing a significant shift towards smart, integrated monitoring solutions that offer real-time data and advanced analytical capabilities. The proliferation of IoT devices and cloud computing is enabling more comprehensive and accessible monitoring frameworks, moving beyond traditional manual inspections. This evolution is driven by the need for enhanced safety protocols, cost efficiency, and improved decision-making processes in construction and operational phases of large-scale projects. Furthermore, the push for sustainable and resilient infrastructure is creating a demand for monitoring solutions that can provide early warnings and inform adaptive strategies.

- Shift towards Wireless and IoT-enabled Monitoring Systems for enhanced connectivity and data transmission.

- Increasing adoption of Real-time Data Analytics and AI for predictive maintenance and early warning systems.

- Growing demand for Integrated Monitoring Solutions combining geotechnical, structural, and environmental parameters.

- Miniaturization of Sensors and Drones for more accessible and versatile deployment in hard-to-reach areas.

- Emphasis on Data Visualization and User-Friendly Interfaces for improved operational insights and decision-making.

- Expansion of Fiber Optic Sensing Technology for distributed and long-range monitoring applications.

- Development of Resilient Infrastructure Monitoring to withstand climate change impacts and natural hazards.

AI Impact Analysis on Geotechnical and Structural Monitoring Device

User inquiries about AI's impact consistently revolve around its potential to revolutionize data interpretation, predictive modeling, and autonomous operations within geotechnical and structural monitoring. Key themes include the ability of AI to process vast datasets from multiple sensors, identify subtle anomalies indicative of potential failures, and automate routine monitoring tasks, thereby reducing human error and operational costs. Concerns often touch upon the accuracy of AI models, the need for robust data governance, and the integration challenges with existing legacy systems, while expectations are high for enhanced safety, efficiency, and the proactive management of infrastructure assets.

Artificial intelligence is profoundly transforming the geotechnical and structural monitoring landscape by enabling sophisticated data analysis and predictive capabilities. AI algorithms can process immense volumes of sensor data, including strain, displacement, tilt, and vibration, to detect patterns and anomalies that might be imperceptible to human analysis. This allows for the development of highly accurate predictive models that forecast potential structural fatigue, material degradation, or instability, thereby facilitating proactive maintenance and preventing catastrophic failures. The integration of machine learning into monitoring systems is leading to more intelligent, self-optimizing solutions that can adapt to changing environmental conditions and operational demands, significantly enhancing the reliability and lifespan of critical infrastructure.

- Automated Data Interpretation: AI algorithms process complex sensor data to identify patterns and anomalies faster than manual analysis.

- Predictive Maintenance: Machine learning models forecast potential structural failures, enabling proactive intervention and reducing downtime.

- Enhanced Anomaly Detection: AI improves the accuracy of detecting subtle changes that indicate early signs of distress in structures or ground conditions.

- Optimized Sensor Placement: AI can analyze historical data to recommend optimal placement of sensors for maximum data efficacy.

- Reduced False Positives/Negatives: Sophisticated AI models can minimize erroneous alerts, improving the trustworthiness of monitoring systems.

- Autonomous Monitoring Systems: AI facilitates the development of self-regulating systems that can adjust parameters and flag critical events without constant human oversight.

Key Takeaways Geotechnical and Structural Monitoring Device Market Size & Forecast

Analysis of user questions regarding key takeaways from the market size and forecast consistently reveals a focus on the underlying growth drivers, the most promising technological advancements, and the critical factors influencing market expansion. Users are keenly interested in understanding which sectors will experience the most significant growth, the impact of regulatory frameworks on adoption rates, and the long-term sustainability of current market trends. There is also a strong desire to identify the primary challenges that might impede this growth and how these can be strategically addressed to maximize market potential and investment returns.

The Geotechnical and Structural Monitoring Device Market is poised for substantial and sustained growth, driven by a confluence of factors including increasing global infrastructure development, stringent safety regulations, and rapid technological innovations. The market's upward trajectory is indicative of a broader industry shift towards preventative and predictive maintenance strategies, recognizing the economic and safety benefits of early detection of potential issues. While significant opportunities lie in emerging economies and the continuous integration of advanced analytics, addressing challenges related to data security, initial investment costs, and the need for skilled personnel will be crucial for unlocking the market's full potential and ensuring its robust expansion throughout the forecast period.

- Robust Growth: The market is projected to nearly double in value by 2033, reflecting strong demand for enhanced safety and operational efficiency.

- Technology-Driven Expansion: Innovation in IoT, AI, and advanced sensor technologies is a primary catalyst for market growth and competitive differentiation.

- Infrastructure Focus: Significant investments in civil infrastructure, mining, and energy sectors are key demand generators.

- Regulatory Compliance: Strict safety standards and environmental regulations are compelling greater adoption of monitoring solutions globally.

- Emerging Market Potential: Developing economies, particularly in Asia Pacific, present substantial untapped opportunities for market players.

- Shift to Predictive Maintenance: The industry is moving from reactive repairs to proactive, data-driven asset management facilitated by monitoring devices.

Geotechnical and Structural Monitoring Device Market Drivers Analysis

The global surge in infrastructure development projects, ranging from urban expansion and transportation networks to critical energy facilities, represents a fundamental driver for the Geotechnical and Structural Monitoring Device Market. As nations invest heavily in constructing new roads, bridges, tunnels, dams, and high-rise buildings, the imperative for ensuring their structural integrity and long-term safety from the design phase through to operational lifespan becomes paramount. Monitoring devices are indispensable in these projects for assessing ground conditions, managing construction risks, and verifying structural performance, thereby minimizing costly delays and potential failures. This sustained global construction boom provides a robust and continuously expanding demand base for advanced monitoring solutions.

Furthermore, the increasing awareness and enforcement of stringent safety regulations and environmental standards across industries significantly propel market growth. Governments and regulatory bodies worldwide are implementing stricter mandates for worker safety, public infrastructure resilience, and environmental protection, particularly in high-risk sectors like mining and oil & gas. Compliance with these regulations often necessitates the deployment of reliable geotechnical and structural monitoring devices to detect potential hazards, prevent environmental contamination, and ensure adherence to design specifications. This regulatory push not only creates a baseline demand but also encourages continuous innovation in monitoring technologies to meet evolving compliance requirements and industry best practices.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Infrastructure Development | +3.5% | Global, particularly Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Growing Awareness of Structural Safety | +2.8% | Global | Medium to Long-term |

| Stringent Safety Regulations and Standards | +2.3% | North America, Europe, Asia Pacific | Medium to Long-term |

| Technological Advancements in Sensing & Data Analytics | +2.0% | Global | Short to Long-term |

| Rise in Mining and Construction Activities | +1.5% | Asia Pacific, Latin America, Africa | Medium-term |

Geotechnical and Structural Monitoring Device Market Restraints Analysis

One of the primary restraints impeding the broader adoption of geotechnical and structural monitoring devices is the high initial investment cost associated with advanced systems. These comprehensive solutions often involve expensive sensors, specialized installation, sophisticated data acquisition units, and complex software platforms for analysis and visualization. For many small to medium-sized enterprises (SMEs) or projects with limited budgets, the upfront capital expenditure can be prohibitive, despite the long-term benefits of risk mitigation and cost savings from preventative maintenance. This financial barrier limits market penetration, particularly in regions where economic constraints are more pronounced or where the perceived return on investment is not immediately evident.

Another significant challenge is the lack of skilled professionals capable of effectively deploying, maintaining, and interpreting data from these advanced monitoring systems. The operation of modern geotechnical and structural monitoring solutions requires a blend of civil engineering knowledge, expertise in sensor technology, and proficiency in data science and analytics. A shortage of such multidisciplinary talent can lead to improper installation, inaccurate data collection, or misinterpretation of results, undermining the effectiveness and reliability of the monitoring efforts. This skills gap not only increases operational costs due to the need for specialized training or external consultants but also acts as a bottleneck for wider market adoption and efficient utilization of these critical technologies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs | -2.0% | Global, particularly developing regions | Medium to Long-term |

| Lack of Skilled Workforce | -1.8% | Global | Long-term |

| Complexity of Data Management & Integration | -1.5% | Global | Medium-term |

| Perceived Lack of Standardization | -1.2% | Europe, North America | Medium-term |

| Harsh Environmental Conditions Affecting Sensor Longevity | -1.0% | Mining, Remote Infrastructure | Long-term |

Geotechnical and Structural Monitoring Device Market Opportunities Analysis

The rapid urbanization and industrialization occurring in emerging economies across Asia Pacific, Latin America, and Africa present significant untapped opportunities for the geotechnical and structural monitoring device market. As these regions undergo massive infrastructure transformations, including the construction of smart cities, extensive transportation networks, and large-scale industrial facilities, the demand for robust monitoring solutions to ensure safety and efficiency is escalating. Many of these regions are also prone to seismic activity or challenging ground conditions, further emphasizing the need for reliable monitoring. Market players can strategically expand their presence in these areas by offering scalable and cost-effective solutions tailored to local requirements, thereby capitalizing on a burgeoning market with immense growth potential.

Another substantial opportunity lies in the integration of monitoring devices with advanced technologies such as the Internet of Things (IoT), 5G connectivity, and sophisticated data analytics platforms. The convergence of these technologies enables real-time, remote, and highly accurate data collection and analysis, transforming traditional monitoring into predictive intelligence. This allows for the development of smart infrastructure systems that can self-diagnose and communicate potential issues, moving beyond simple data logging to truly intelligent asset management. Companies that can seamlessly integrate these technologies to offer comprehensive, cloud-based monitoring as a service (MaaS) solutions will gain a significant competitive edge, meeting the increasing demand for end-to-end digital solutions in the construction and asset management sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Economies (Asia Pacific, Latin America) | +3.0% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Integration with IoT, AI, and 5G Technologies | +2.5% | Global | Short to Long-term |

| Growth in Renewable Energy Infrastructure Monitoring | +2.0% | Europe, North America, Asia Pacific | Medium to Long-term |

| Increased Adoption in Predictive Maintenance Strategies | +1.8% | Global | Medium to Long-term |

| Development of Public-Private Partnerships for Large Projects | +1.5% | Global | Long-term |

Geotechnical and Structural Monitoring Device Market Challenges Impact Analysis

One of the persistent challenges in the geotechnical and structural monitoring device market is ensuring the long-term reliability and robustness of sensors and data acquisition systems in harsh environmental conditions. Devices deployed in remote mining sites, offshore platforms, or extreme weather zones are exposed to corrosive elements, vibrations, extreme temperatures, and moisture, which can degrade performance or lead to premature failure. Maintaining accuracy and functionality over extended periods in such challenging environments requires specialized materials, advanced packaging, and rigorous testing, which can add to the cost and complexity of the solutions. Overcoming these environmental vulnerabilities is crucial for building trust and ensuring the sustained adoption of monitoring technologies in critical applications.

Another significant hurdle involves the interoperability and standardization of data from disparate monitoring systems and sensors from various manufacturers. In many large-scale projects, multiple types of sensors and devices from different vendors may be deployed, each generating data in proprietary formats. This lack of universal standards for data collection, transmission, and interpretation creates significant integration challenges, making it difficult to consolidate, analyze, and gain holistic insights from the vast amounts of generated data. Addressing this interoperability gap through industry-wide standards and open-platform solutions is essential for facilitating seamless data exchange, improving data analytics capabilities, and ultimately enhancing the overall value proposition of integrated monitoring systems.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Sensor Reliability in Harsh Environments | -1.5% | Mining, Marine, Extreme Climates | Long-term |

| Data Security and Privacy Concerns | -1.2% | Global | Medium to Long-term |

| Interoperability and Standardization Issues | -1.0% | Global | Medium-term |

| Regulatory Complexities Across Different Jurisdictions | -0.8% | Global | Long-term |

| Balancing Cost-Effectiveness with Advanced Functionality | -0.7% | Global, particularly price-sensitive markets | Short to Medium-term |

Geotechnical and Structural Monitoring Device Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Geotechnical and Structural Monitoring Device Market, covering historical data from 2019 to 2023, with detailed market forecasts extending from 2025 to 2033. The study meticulously examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographic regions. It further includes a thorough impact analysis of emerging technologies like AI and IoT, competitive landscape assessment, and profiles of leading market players to offer actionable insights for stakeholders. The report aims to equip industry participants with a holistic understanding of market dynamics to inform strategic decision-making and identify future growth avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 6.02 Billion |

| Growth Rate | 9.8% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Geokon, Inc., Campbell Scientific, Inc., Load Systems International (LSI), Roctest, a division of Telemac, SISGEO S.p.A., GKM Consultants, Durham Geo Slope Indicator, Soldata (part of Sixense Group), Keller Group PLC, Fugro N.V., Nova Metrix LLC, RST Instruments Ltd., Measurand Inc., Ackermann GmbH, Geomotion Australia, Geodata AG, Leica Geosystems, Trimble Inc., Topcon Corporation, Worldsensing |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Geotechnical and Structural Monitoring Device Market is meticulously segmented to provide a granular understanding of its diverse applications and technological offerings. This segmentation allows for a detailed analysis of market dynamics within specific product categories, technological approaches, and end-user industries, highlighting areas of high growth and emerging demand. By understanding how different segments interact and evolve, stakeholders can better tailor their strategies, develop specialized products, and target specific market niches for optimal returns.

The market's intricate structure reflects the varied requirements of civil engineering, mining, and critical infrastructure projects, where specific device types and technologies are often mandated by project scale, environmental conditions, and regulatory compliance. Analyzing these segments individually and in conjunction provides crucial insights into the current market landscape and future growth trajectories, enabling businesses to identify areas for investment, innovation, and strategic partnerships. This detailed breakdown ensures a comprehensive market overview, supporting informed decision-making across the value chain.

- By Device Type: This segment includes devices such as Extensometers, Inclinometers, Piezometers, Settlement Systems, Strain Gauges, Load Cells, Tiltmeters, Vibration Monitors, Pressure Cells, Total Stations/GNSS, and other specialized meters like Crack Meters and Thermometers. Each device serves a specific purpose in measuring various geotechnical and structural parameters.

- By Technology: Encompasses the different methods of data acquisition and transmission, including Wired Monitoring, Wireless Monitoring (increasingly IoT-enabled for real-time data), Fiber Optic Sensing for distributed measurements, Robotic Total Stations for automated surveying, and Satellite-based Monitoring (InSAR) for large-area deformation analysis.

- By End-User Industry: Covers the primary sectors utilizing these devices, such as Building & Construction (spanning residential, commercial, and industrial projects), Mining (both open-pit and underground operations), Civil Infrastructure (including bridges, dams, tunnels, roads, and railways), Energy (oil & gas, power generation, and renewable energy facilities), Environmental Monitoring, and niche applications in Aerospace & Defense, and Research.

- By Component: Segregates the market into Hardware (comprising sensors, dataloggers, cables, and gateways), Software (for data management, advanced analysis, and visualization platforms), and Services (including installation, calibration, maintenance, and expert consulting).

Regional Highlights

- North America: Expected to maintain a significant market share due to substantial investments in aging infrastructure modernization, stringent safety regulations, and the rapid adoption of advanced monitoring technologies. The presence of key market players and a robust R&D ecosystem further fuels growth.

- Europe: A mature market driven by high-value civil engineering projects, a strong focus on sustainable infrastructure, and advanced regulatory frameworks. Countries like Germany, the UK, and France are leading the adoption of sophisticated monitoring solutions for tunnels, bridges, and critical industrial sites.

- Asia Pacific (APAC): Projected to be the fastest-growing region, propelled by massive infrastructure development projects in countries like China, India, Japan, and Southeast Asian nations. Rapid urbanization, increasing mining activities, and the growing adoption of smart city initiatives contribute to escalating demand.

- Latin America: Demonstrates steady growth, primarily driven by investments in mining, oil and gas, and public infrastructure projects. Countries such as Brazil, Mexico, and Chile are witnessing increased deployment of monitoring devices to ensure project safety and efficiency.

- Middle East and Africa (MEA): Emerging as a high-potential market due to large-scale construction projects, particularly in the GCC countries, and growing investments in energy and transportation infrastructure. The need for resilient structures in harsh climates also drives demand for robust monitoring solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Geotechnical and Structural Monitoring Device Market.- Geokon, Inc.

- Campbell Scientific, Inc.

- Load Systems International (LSI)

- Roctest, a division of Telemac

- SISGEO S.p.A.

- GKM Consultants

- Durham Geo Slope Indicator

- Soldata (part of Sixense Group)

- Keller Group PLC

- Fugro N.V.

- Nova Metrix LLC

- RST Instruments Ltd.

- Measurand Inc.

- Ackermann GmbH

- Geomotion Australia

- Geodata AG

- Leica Geosystems

- Trimble Inc.

- Topcon Corporation

- Worldsensing

Frequently Asked Questions

Analyze common user questions about the Geotechnical and Structural Monitoring Device market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a geotechnical and structural monitoring device?

Geotechnical and structural monitoring devices are specialized instruments used to measure and analyze the behavior of ground conditions, earthworks, and structures. They collect data on parameters like deformation, strain, load, tilt, and pressure to assess stability, predict failures, and ensure the safety and longevity of infrastructure projects and natural formations. These devices are critical for risk management in construction, mining, and civil engineering.

Why is geotechnical and structural monitoring important?

Geotechnical and structural monitoring is crucial for ensuring public safety, protecting assets, and optimizing maintenance strategies for critical infrastructure. By providing real-time data and early warning systems, it helps prevent catastrophic failures, reduce operational costs, and ensure compliance with safety regulations. It supports informed decision-making throughout the lifespan of structures and projects, from construction to decommissioning.

What are the key technologies driving innovation in this market?

Key technologies driving innovation include the Internet of Things (IoT) for wireless and real-time data transmission, Artificial Intelligence (AI) and Machine Learning for advanced data analysis and predictive modeling, Fiber Optic Sensing for distributed measurements, and drone-based inspections. These advancements enhance accuracy, efficiency, and the overall intelligence of monitoring systems, enabling more proactive asset management.

Which industries are the primary end-users of these monitoring devices?

The primary end-user industries include Building & Construction (for residential, commercial, and industrial structures), Mining (for slope stability and ground control), Civil Infrastructure (bridges, dams, tunnels, roads, railways), and Energy (oil & gas, power generation, renewable energy facilities). Environmental monitoring and specialized applications in aerospace also represent significant segments.

What are the main challenges faced by the Geotechnical and Structural Monitoring Device Market?

The main challenges include high initial investment costs for advanced systems, the lack of a skilled workforce to operate and interpret data from these technologies, issues related to data security and privacy, and the need for greater interoperability and standardization among various monitoring solutions. Additionally, ensuring sensor reliability in harsh environmental conditions remains a significant technical hurdle.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted