Terminal Tractor Market

Terminal Tractor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708679 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Terminal Tractor Market Size

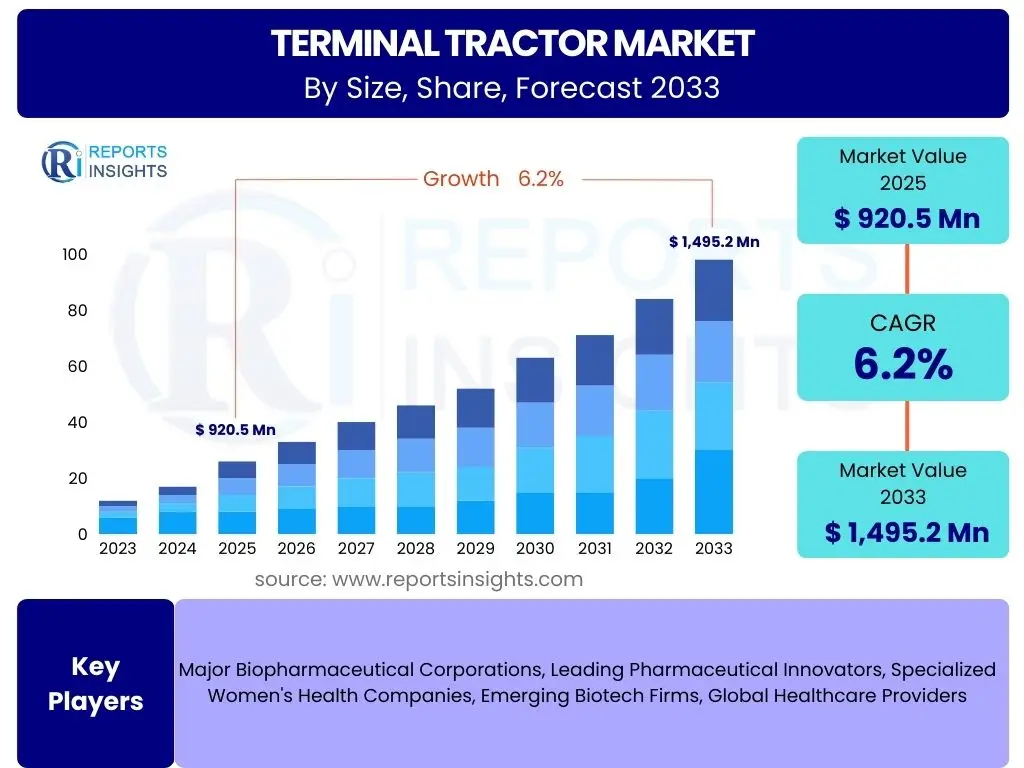

According to Reports Insights Consulting Pvt Ltd, The Terminal Tractor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 920.5 million in 2025 and is projected to reach USD 1,495.2 million by the end of the forecast period in 2033.

Key Terminal Tractor Market Trends & Insights

The Terminal Tractor market is currently undergoing significant transformation, driven by a confluence of technological advancements, evolving logistical demands, and stringent environmental regulations. A predominant trend involves the increasing adoption of electric and autonomous terminal tractors, aiming to enhance operational efficiency, reduce labor costs, and lower carbon emissions. This shift is particularly evident in port terminals and large distribution centers where repetitive tasks and predictable routes make automation highly viable.

Another critical insight is the growing emphasis on connectivity and data analytics within the terminal tractor ecosystem. Integrated telematics systems, GPS tracking, and fleet management software are becoming standard features, enabling real-time monitoring, predictive maintenance, and optimized route planning. These tools provide operators with actionable data, significantly improving asset utilization and overall supply chain visibility. The market is also witnessing a surge in demand for robust, high-performance vehicles capable of operating in diverse and often harsh environmental conditions, reinforcing the need for durable and reliable machinery.

Furthermore, the expansion of e-commerce and the associated boom in warehousing and logistics infrastructure worldwide are creating substantial demand for terminal tractors. As goods movement intensifies, the need for efficient and rapid yard management solutions becomes paramount, positioning terminal tractors as indispensable assets in the modern supply chain. Customization and modular designs are also emerging trends, allowing operators to configure vehicles for specific operational requirements, ranging from intermodal transport to factory floor logistics.

- Electrification and automation are key drivers for efficiency and sustainability.

- Integration of telematics and data analytics for optimized fleet management.

- Increased demand fueled by e-commerce expansion and logistics infrastructure growth.

- Focus on enhanced durability and performance for demanding operational environments.

- Emergence of customized and modular terminal tractor designs.

AI Impact Analysis on Terminal Tractor

The integration of Artificial Intelligence (AI) is poised to revolutionize the Terminal Tractor market, transforming traditional yard operations into highly intelligent and autonomous systems. Users frequently inquire about the practical applications of AI, specifically concerning how it can enhance efficiency, safety, and reduce operational costs. AI's primary impact will be seen in enabling advanced autonomy, allowing terminal tractors to navigate complex environments, perform precise coupling and uncoupling tasks, and dynamically respond to real-time changes in yard conditions without human intervention. This capability is expected to significantly reduce human error and optimize throughput in busy logistics hubs.

Beyond full autonomy, AI is crucial for predictive maintenance, a widely discussed benefit among stakeholders. By analyzing operational data from sensors on components like engines, transmissions, and tires, AI algorithms can predict potential failures before they occur. This proactive approach minimizes unexpected downtime, extends asset lifespan, and reduces maintenance costs, addressing a major concern for fleet operators. Furthermore, AI-powered route optimization systems will utilize real-time traffic, weather, and operational data to plan the most efficient paths for terminal tractors, cutting fuel consumption and improving turnaround times, which directly impacts profitability.

Safety is another critical area where AI will have a profound impact. AI-driven sensor fusion, object detection, and collision avoidance systems will enhance situational awareness for both autonomous and human-operated terminal tractors, mitigating risks in congested yards. Users are also keen on understanding AI's role in workforce management, such as allocating tasks to both human and robotic assets, and providing intelligent insights for training and performance improvement. The overall expectation is that AI will usher in an era of hyper-efficient, safer, and more sustainable terminal operations.

- Enables advanced autonomous operation and navigation in complex yard environments.

- Facilitates predictive maintenance, reducing downtime and operational costs.

- Optimizes routes and task scheduling for enhanced efficiency and fuel economy.

- Improves safety through AI-powered object detection and collision avoidance systems.

- Supports intelligent workforce management and operational analytics.

Key Takeaways Terminal Tractor Market Size & Forecast

The Terminal Tractor market is on a robust growth trajectory, driven primarily by the escalating demands of global logistics and the ongoing digital transformation within the supply chain sector. A key takeaway is the increasing investment in advanced technologies, particularly electrification and automation, which are not just incremental improvements but foundational shifts reshaping the market landscape. These technological advancements are critical for meeting the twin objectives of operational efficiency and environmental sustainability, which are now top priorities for operators worldwide. The forecast indicates sustained expansion, fueled by burgeoning e-commerce volumes and the strategic modernization of port and distribution center infrastructures.

Another significant insight from the market forecast is the pronounced regional disparities in adoption and growth. While mature markets in North America and Europe are leading in the integration of electric and autonomous solutions, emerging economies in Asia Pacific and Latin America are experiencing rapid growth in basic terminal tractor deployments as their logistics networks mature. This creates diverse opportunities for market players, requiring tailored strategies for different geographical contexts. The competitive landscape is also evolving, with traditional manufacturers investing heavily in R&D to incorporate cutting-edge features and new entrants specializing in electric or autonomous solutions.

Ultimately, the market's future is defined by its ability to adapt to dynamic operational requirements and technological innovation. The forecast underscores the essential role terminal tractors play in optimizing the final leg of the supply chain, a role that will only intensify with global trade expansion. Understanding the interplay between technological push, market pull from logistics growth, and regulatory pressures is crucial for navigating this evolving market successfully. The shift towards more sustainable and intelligent solutions is irreversible and will define market leadership in the coming decade.

- Market demonstrates strong growth, driven by global logistics and digital transformation.

- Electrification and automation are fundamental drivers of market evolution and sustainability.

- Regional growth varies, with mature markets leading tech adoption and emerging markets focusing on infrastructure build-out.

- Competitive landscape is dynamic, with strong R&D focus on advanced features.

- Sustainable and intelligent solutions are pivotal for future market leadership and operational efficiency.

Terminal Tractor Market Drivers Analysis

The Terminal Tractor market is significantly propelled by several powerful macroeconomic and technological forces. A primary driver is the exponential growth of the e-commerce sector, which necessitates highly efficient and rapid goods movement within warehouses, distribution centers, and port terminals. As online retail continues its expansion, the volume of packages and containers processed daily escalates, directly increasing the demand for specialized vehicles like terminal tractors that can quickly and safely shuffle trailers and containers.

Concurrently, the global expansion and modernization of port infrastructure and intermodal freight transportation systems act as a crucial catalyst. Ports worldwide are investing heavily in automation and expanding their capacities to handle larger vessels and increased cargo throughput. Terminal tractors are indispensable in these environments for efficiently moving containers between berths, stacking areas, and rail/road interfaces, thereby streamlining port logistics and reducing turnaround times. The increasing global trade volumes further underscore the necessity for robust and high-capacity terminal operations.

Furthermore, the persistent challenges posed by labor shortages, particularly for skilled drivers in logistics and trucking, are driving the adoption of automated and semi-autonomous terminal tractors. Companies are increasingly turning to technology to mitigate workforce limitations and reduce operational costs associated with manual labor. This push towards automation, coupled with rising fuel efficiency demands and regulatory pressures for reduced emissions, specifically encourages the uptake of electric and hybrid terminal tractors, aligning with broader sustainability goals across the industry.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| E-commerce Growth & Logistics Expansion | +1.8% | Global, particularly North America, APAC, Europe | Short to Mid-Term (2025-2030) |

| Port Modernization & Intermodal Traffic | +1.5% | Asia Pacific, Europe, North America | Mid to Long-Term (2027-2033) |

| Labor Shortages & Automation Adoption | +1.2% | North America, Europe | Mid-Term (2026-2031) |

| Demand for Fuel Efficiency & Emission Reduction | +0.8% | Europe, North America, China | Mid to Long-Term (2027-2033) |

Terminal Tractor Market Restraints Analysis

Despite the positive growth trajectory, the Terminal Tractor market faces several significant restraints that could impede its expansion. One primary restraint is the substantial initial capital investment required for purchasing terminal tractors, especially for advanced electric or autonomous models. Small to medium-sized logistics operators and businesses with limited capital budgets may find these costs prohibitive, opting for older, less efficient models or delaying fleet modernization. This high upfront cost can create a barrier to entry and slow the adoption rate of cutting-edge technologies.

Another critical restraint is the complexity and cost associated with establishing and maintaining the necessary infrastructure for electric and autonomous terminal tractors. Electric models require extensive charging infrastructure, including charging stations and grid upgrades, which entail significant planning and investment. Autonomous vehicles, on the other hand, demand sophisticated sensor arrays, high-definition mapping, and robust communication networks, along with the technical expertise to manage these systems. The lack of standardized infrastructure and the high costs involved can deter potential adopters.

Furthermore, regulatory hurdles and safety concerns, particularly regarding autonomous operations, represent a significant restraint. The legal frameworks for operating self-driving vehicles on private properties and especially in mixed traffic environments are still evolving and vary widely by region. Public perception and concerns about safety in shared operational spaces, along with the need for rigorous testing and certification, add layers of complexity and can slow down the widespread deployment of fully autonomous terminal tractors. Supply chain disruptions, often impacting component availability and manufacturing lead times, also pose ongoing challenges to market stability and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.1% | Global, particularly SMEs | Short to Mid-Term (2025-2030) |

| Infrastructure Requirements for EVs/Autonomous | -0.9% | Global | Mid-Term (2026-2031) |

| Regulatory Hurdles & Safety Concerns for Autonomy | -0.7% | North America, Europe | Mid to Long-Term (2027-2033) |

| Supply Chain Disruptions & Component Shortages | -0.5% | Global | Short-Term (2025-2027) |

Terminal Tractor Market Opportunities Analysis

The Terminal Tractor market is ripe with opportunities driven by technological advancements and evolving industry needs. A significant area of opportunity lies in the continued innovation and expansion of electric and hydrogen fuel cell terminal tractors. As global mandates for decarbonization intensify and corporate sustainability goals become more stringent, the demand for zero-emission yard vehicles is set to skyrocket. This presents substantial opportunities for manufacturers to develop and market advanced electric powertrains, longer-range batteries, and efficient charging solutions that cater to diverse operational requirements, offering a clear competitive edge.

Another major opportunity emerges from the rapid progress in autonomous driving technology. While full autonomy still faces regulatory and infrastructure challenges, the development and deployment of semi-autonomous and driver-assist features offer immediate market potential. Features such as automated hitching, precision maneuvering, and obstacle detection can significantly enhance operational safety and efficiency in controlled environments like private yards. Manufacturers focusing on modular autonomy solutions that can be progressively upgraded will be well-positioned to capitalize on this evolving market segment.

Furthermore, the untapped potential in emerging markets, particularly in Asia Pacific, Latin America, and Africa, presents substantial growth opportunities. As these regions experience rapid industrialization, infrastructure development, and growth in logistics and e-commerce, the demand for efficient terminal handling equipment is increasing. Companies that can offer cost-effective, durable, and regionally adapted terminal tractor solutions, alongside robust after-sales support and flexible financing options, stand to gain significant market share in these burgeoning economies. Diversification into specialized applications, such as cold chain logistics or heavy-duty industrial environments, also provides avenues for market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Electrification & Hydrogen Fuel Cell Adoption | +1.5% | Global, particularly Europe, North America, China | Mid to Long-Term (2027-2033) |

| Expansion of Autonomous & Semi-Autonomous Solutions | +1.3% | North America, Europe, select APAC countries | Mid-Term (2026-2031) |

| Growth in Emerging Markets (APAC, LATAM, MEA) | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Short to Mid-Term (2025-2030) |

| Development of Rental & Leasing Models | +0.7% | Global | Short to Mid-Term (2025-2030) |

Terminal Tractor Market Challenges Impact Analysis

The Terminal Tractor market, while promising, is not without its significant challenges that could hinder innovation and adoption. One major challenge is the complex integration of new technologies, particularly for autonomous and electric solutions, into existing logistical ecosystems. Many legacy systems and operational workflows are not designed to accommodate these advanced vehicles, requiring substantial investment in system upgrades, software integration, and workforce retraining. The interoperability between different brands of equipment and varying operational protocols presents a formidable hurdle for seamless fleet modernization.

Another critical challenge revolves around the skilled labor gap, specifically for operating and maintaining advanced terminal tractors. While automation aims to reduce the need for drivers, it creates a new demand for technicians skilled in robotics, AI, electrical systems, and complex software diagnostics. The shortage of such specialized personnel can significantly slow down the deployment and effective utilization of high-tech terminal tractors, impacting operational continuity and return on investment. Training programs and educational initiatives are essential but require considerable time and resources to develop and implement.

Furthermore, economic volatility and geopolitical uncertainties pose ongoing challenges, affecting investment decisions and supply chain stability. Fluctuations in raw material prices, currency exchange rates, and global trade policies can impact manufacturing costs and market demand. Intense competition within the market, coupled with continuous pressure to reduce total cost of ownership (TCO) for customers, compels manufacturers to innovate while simultaneously managing price points. Addressing these multifarious challenges requires strategic foresight, robust supply chain management, and a strong commitment to both technological advancement and workforce development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Integration with Legacy Systems | -1.0% | Global | Short to Mid-Term (2025-2030) |

| Skilled Labor Shortage for New Technologies | -0.8% | North America, Europe, Asia Pacific | Mid-Term (2026-2031) |

| Economic Volatility & Geopolitical Risks | -0.6% | Global | Short-Term (2025-2027) |

| Cybersecurity Risks for Connected & Autonomous Systems | -0.4% | Global | Mid to Long-Term (2027-2033) |

Terminal Tractor Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Terminal Tractor market, offering critical insights into market dynamics, segmentation, regional landscapes, and competitive strategies. It covers the historical performance, current market status, and future projections, aiming to equip stakeholders with actionable intelligence for strategic decision-making in this evolving industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 920.5 Million |

| Market Forecast in 2033 | USD 1,495.2 Million |

| Growth Rate | 6.2% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Kalmar (Cargotec Corporation), Terberg Benschop B.V., Capacity Trucks (REV Group), TICO Tractors, Autocar Terminal Tractors, Konecranes, Volvo Penta, Orange EV, BYD Company Ltd., Hyster-Yale Materials Handling, Lonking Holdings Limited, Ottawa (DOLL Fahrzeugbau GmbH), MAFI Transport-Systeme GmbH, Taylor Machine Works Inc., Battle Motors, Nikola Corporation, Sany Heavy Industry Co., Ltd., Anhui Heli Co., Ltd., Linde Material Handling, EP Equipment |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Terminal Tractor market is comprehensively segmented across various dimensions to provide granular insights into its multifaceted landscape. These segmentations are crucial for understanding distinct market behaviors, technological preferences, and operational requirements across different industries and applications. The primary breakdowns include distinctions by fuel type, reflecting the industry's shift towards sustainability, and by propulsion system, highlighting the adoption of advanced power technologies. Furthermore, segmentation by type examines the spectrum from manual to fully autonomous vehicles, showcasing the evolving levels of automation in yard operations. Tonnage capacity and application areas delineate the varied operational needs, from light-duty warehouse tasks to heavy-duty port container handling, providing a clear picture of specialized demand.

End-use industry segmentation offers insights into the specific requirements of sectors such as logistics, e-commerce, and manufacturing, while ownership patterns shed light on acquisition strategies, differentiating between new sales and the growing trend of rental or leasing options. This detailed categorization enables a thorough analysis of market dynamics, competitive positioning, and growth opportunities within each specific niche. Understanding these segments is vital for manufacturers to tailor their product offerings, for service providers to customize their solutions, and for investors to identify high-growth areas.

- By Fuel Type: This segment includes Diesel, Electric, Hybrid, CNG/LPG, and Hydrogen Fuel Cell, indicating the shift towards sustainable and diversified energy sources.

- By Propulsion: Covers Conventional internal combustion engines, Electric (Battery Electric and Fuel Cell Electric), and Hybrid systems, reflecting the innovation in powertrain technologies.

- By Type: Categorized into Manual (driver-operated), Semi-Autonomous (driver-assisted with some automated functions), and Fully-Autonomous (self-operating), illustrating the progression of automation.

- By Tonnage Capacity: Segments include Up to 30 Tons, 30-50 Tons, and Above 50 Tons, addressing the diverse range of load handling requirements.

- By Application: Encompasses Ports & Harbors, Airports, Logistics & Warehousing, Manufacturing Facilities, Railway Yards, and Intermodal Facilities, highlighting the primary operational environments.

- By End-use Industry: Features Logistics & Transportation, Retail & E-commerce, Automotive, Food & Beverage, Manufacturing, and Marine, demonstrating industry-specific demand patterns.

- By Ownership: Differentiated into New Sales, Rental/Leasing, and Aftermarket services, outlining various acquisition and service models.

Regional Highlights

The Terminal Tractor market exhibits distinct regional dynamics, influenced by varying levels of industrialization, infrastructure development, regulatory environments, and technological adoption rates. North America stands as a dominant region, driven by its robust logistics infrastructure, rapid expansion of e-commerce, and high labor costs that accelerate the adoption of automation and electrification. The presence of major ports, extensive warehousing networks, and a strong push towards reducing emissions are key factors contributing to the region's market leadership. Investment in smart port technologies and autonomous yard operations is particularly strong here, creating a significant market for advanced terminal tractors.

Europe also represents a significant market, characterized by stringent environmental regulations, a strong focus on sustainability, and a mature logistics sector. Countries like Germany, the Netherlands, and the UK are at the forefront of adopting electric and hybrid terminal tractors to meet ambitious decarbonization targets. The region's emphasis on intermodal transport and efficient supply chain management further fuels demand. European manufacturers are also key innovators in developing advanced, energy-efficient terminal tractor solutions. The push for autonomous solutions is also gaining traction, particularly within confined private terminals and distribution centers.

The Asia Pacific (APAC) region is projected to be the fastest-growing market, primarily due to rapid economic development, increasing trade volumes, and extensive investments in port expansion and logistics infrastructure, especially in countries like China, India, and Southeast Asian nations. While diesel models still dominate a significant portion of the market, there is a growing interest and investment in electric terminal tractors, particularly in China, driven by government incentives and strong domestic manufacturing capabilities. Latin America and the Middle East & Africa (MEA) are also experiencing steady growth, albeit from a smaller base, as their logistics capabilities mature and industrial activities expand, creating demand for efficient terminal handling equipment.

- North America: Market leader due to e-commerce growth, advanced logistics, high labor costs, and early adoption of automation and electrification. Key countries include the United States and Canada.

- Europe: Strong market driven by stringent environmental regulations, sustainability focus, mature logistics, and high adoption of electric/hybrid solutions. Key countries include Germany, UK, France, Netherlands.

- Asia Pacific (APAC): Fastest-growing market, propelled by rapid industrialization, increasing trade volumes, port expansion, and emerging demand for electrification. Key countries include China, India, Japan, Australia, South Korea.

- Latin America: Emerging market with steady growth, fueled by developing logistics infrastructure and increasing regional trade. Key countries include Brazil, Mexico, Argentina.

- Middle East & Africa (MEA): Growth driven by infrastructure development, expanding logistics hubs, and strategic investments in port and intermodal facilities. Key countries include UAE, Saudi Arabia, South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Terminal Tractor Market.- Kalmar (Cargotec Corporation)

- Terberg Benschop B.V.

- Capacity Trucks (REV Group)

- TICO Tractors

- Autocar Terminal Tractors

- Konecranes

- Volvo Penta

- Orange EV

- BYD Company Ltd.

- Hyster-Yale Materials Handling

- Lonking Holdings Limited

- Ottawa (DOLL Fahrzeugbau GmbH)

- MAFI Transport-Systeme GmbH

- Taylor Machine Works Inc.

- Battle Motors

- Nikola Corporation

- Sany Heavy Industry Co., Ltd.

- Anhui Heli Co., Ltd.

- Linde Material Handling

- EP Equipment

Frequently Asked Questions

Analyze common user questions about the Terminal Tractor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a terminal tractor and what is its primary function?

A terminal tractor, also known as a yard tractor, yard dog, or shunt truck, is a specialized semi-tractor designed to move semi-trailers within a confined area, such as a shipping yard, warehouse, or port, without operating on public roads. Its primary function is to quickly and efficiently shuttle trailers between loading docks, parking spots, and other designated areas, optimizing logistics operations.

What are the key advantages of using electric terminal tractors?

Electric terminal tractors offer several key advantages, including zero tailpipe emissions, significantly lower operating costs due to reduced fuel and maintenance expenses, quieter operation, and eligibility for various environmental incentives. These benefits contribute to enhanced sustainability and a more efficient work environment.

How is automation impacting the terminal tractor market?

Automation is significantly impacting the terminal tractor market by introducing semi-autonomous and fully-autonomous models, which enhance operational efficiency, reduce labor costs, and improve safety by minimizing human error. These systems utilize AI and advanced sensors for route optimization, predictive maintenance, and collision avoidance.

What factors are driving the growth of the terminal tractor market?

The growth of the terminal tractor market is primarily driven by the rapid expansion of e-commerce, increasing global trade volumes, modernization of port and logistics infrastructure, persistent labor shortages in the logistics sector, and the growing demand for sustainable and efficient yard operations.

What are the main challenges faced by the terminal tractor market?

The main challenges facing the terminal tractor market include high initial capital investment for advanced models, the complexity and cost of developing charging and autonomous infrastructure, evolving regulatory frameworks for autonomous vehicles, and the shortage of skilled technicians for new technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted