ATM Machine Market

ATM Machine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706267 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

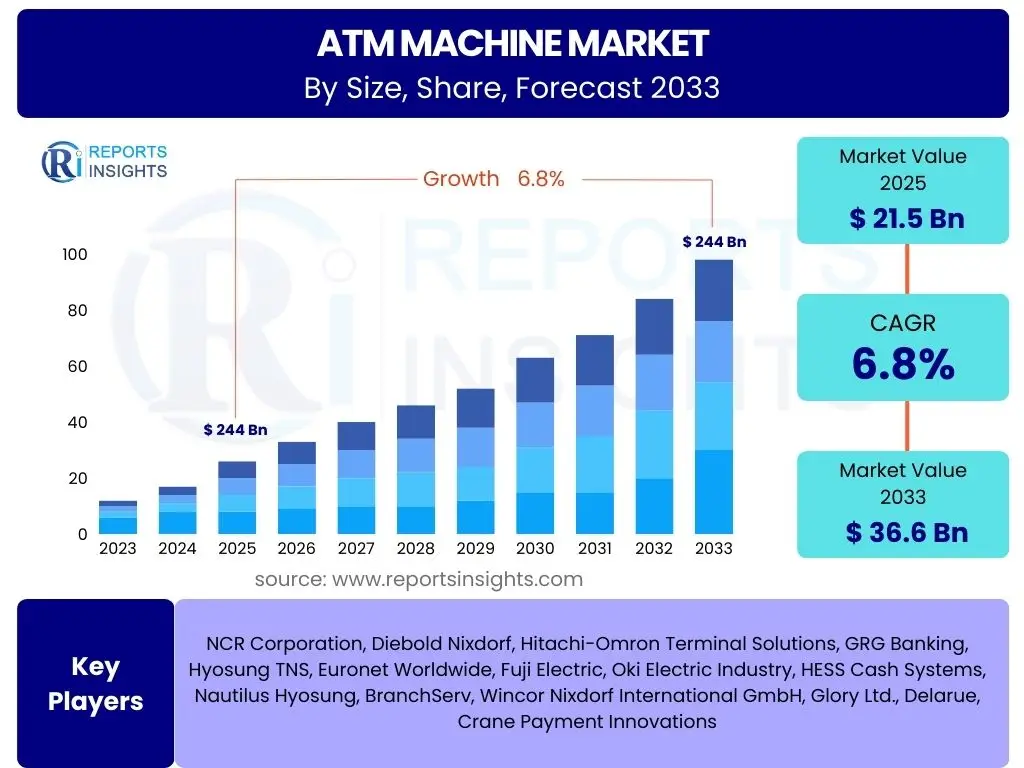

ATM Machine Market Size

According to Reports Insights Consulting Pvt Ltd, The ATM Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 21.5 billion in 2025 and is projected to reach USD 36.6 billion by the end of the forecast period in 2033.

Key ATM Machine Market Trends & Insights

The ATM machine market is undergoing a significant transformation, driven by evolving consumer expectations and technological advancements. Users are increasingly interested in how ATMs are adapting to the digital age, seeking functionalities beyond simple cash dispensing. Key inquiries revolve around the integration of contactless technologies, biometric authentication, enhanced security features, and the role of ATMs as comprehensive self-service banking hubs. There is a clear trend towards smarter, more secure, and versatile machines that can complement or even augment traditional branch services, addressing concerns about their continued relevance in a cashless society.

Modern ATMs are becoming integral components of a hybrid banking ecosystem, offering a bridge between physical cash transactions and digital services. Financial institutions are leveraging these machines to provide a wider array of services, including bill payments, cardless withdrawals, instant account opening, and personalized customer support. This evolution is vital for maintaining the ATM's strategic importance, especially in regions where digital adoption is slower or where physical presence remains crucial for financial inclusion. The emphasis is shifting from merely transactional devices to intelligent service points.

- Integration of Contactless Technology: Enabling NFC-based transactions and cardless withdrawals.

- Biometric Authentication: Enhancing security and user convenience with fingerprint or facial recognition.

- Advanced Security Features: Implementing anti-skimming, anti-fraud, and enhanced surveillance systems.

- Multi-functional Capabilities: Expanding services beyond cash to include bill payments, mobile top-ups, and instant account services.

- Predictive Maintenance and Remote Monitoring: Utilizing IoT for proactive issue resolution and operational efficiency.

- Software-Defined ATMs: Greater flexibility and easier updates for new features and security patches.

- Hybrid Functionality: Combining traditional ATM services with interactive video tellers for remote assistance.

AI Impact Analysis on ATM Machine

User inquiries regarding the impact of Artificial Intelligence on ATM machines primarily focus on how AI can enhance operational efficiency, security, and the overall customer experience. Common themes include AI's potential to automate tasks, predict maintenance needs, detect fraud, and personalize user interactions. There is significant interest in whether AI will lead to the replacement of traditional ATM functions or merely augment them, with a general expectation that AI will make ATMs smarter, more responsive, and more secure, thereby extending their utility in the evolving banking landscape.

AI is set to revolutionize ATM operations by enabling predictive analytics for cash management, significantly reducing downtime and operational costs. Through AI-driven insights, financial institutions can optimize cash replenishment schedules, minimize idle inventory, and improve machine uptime. Furthermore, AI's capabilities in real-time fraud detection are paramount, allowing for the immediate identification and mitigation of suspicious activities, thus enhancing the security posture of ATM networks. The integration of AI also paves the way for a more personalized user experience, with ATMs capable of learning user preferences and offering tailored services and recommendations.

- Predictive Maintenance: AI algorithms analyze machine performance data to predict potential failures, enabling proactive repairs and minimizing downtime.

- Enhanced Fraud Detection: AI-powered systems can detect sophisticated fraud patterns in real-time, significantly improving security against skimming and cyberattacks.

- Optimized Cash Management: AI forecasts cash demand based on historical data and local events, optimizing cash replenishment and reducing operational costs.

- Personalized User Experience: AI can analyze transaction history to offer customized services, promotions, or language options, improving customer satisfaction.

- Voice and Chatbot Integration: AI-driven interfaces enable voice-activated commands and virtual assistance, making ATMs more accessible and user-friendly.

- Biometric Integration: AI enhances the accuracy and speed of biometric authentication methods for secure transactions.

- Operational Efficiency: AI automates routine tasks, reduces human intervention, and streamlines back-end processes, leading to significant cost savings.

Key Takeaways ATM Machine Market Size & Forecast

Common user questions about the ATM machine market size and forecast center on its resilience in the face of digital transformation, the primary drivers of its growth, and where future opportunities lie. Users seek to understand if the market is still viable for investment, what segments are expanding fastest, and the geographical areas promising the most growth. The insights sought typically confirm the market's continued relevance, albeit in an evolved form, and highlight the strategic importance of technological integration and expansion into new customer segments.

Despite the proliferation of digital payment methods, the ATM machine market is projected to demonstrate sustained growth, primarily driven by the ongoing need for cash access globally, particularly in developing economies where financial inclusion initiatives are paramount. The market's resilience stems from its adaptation through technology integration, transforming ATMs into versatile self-service banking platforms. Future growth will be significantly influenced by innovations that enhance security, operational efficiency, and expand functionality, positioning ATMs as complementary rather than competitive with digital channels. This strategic evolution ensures their continued role in the broader financial ecosystem.

- Market Resilience: The ATM market continues to grow, adapting to evolving financial landscapes rather than declining.

- Technological Evolution: Growth is largely propelled by the integration of advanced technologies like AI, biometrics, and contactless features.

- Emerging Market Dominance: Developing regions, especially Asia Pacific and Latin America, are key growth hubs due to financial inclusion drives.

- Service Expansion: Future ATMs will offer broader services beyond cash, becoming comprehensive self-service banking terminals.

- Operational Efficiency Focus: Emphasis on predictive maintenance and optimized cash management drives investment and market growth.

ATM Machine Market Drivers Analysis

The increasing global push for financial inclusion remains a primary driver, particularly in developing economies where access to traditional banking infrastructure is limited. ATMs provide essential cash access and basic banking services, bridging the gap for unbanked and underbanked populations. Urbanization and the growth of commercial centers also fuel demand for convenient cash access points, especially in areas with high foot traffic or limited bank branches. This fundamental need for accessible cash continues to underpin market expansion.

Continuous technological advancements and the need for upgraded infrastructure are significant drivers. Older ATM models are being replaced with newer, more efficient, and secure smart ATMs that offer a broader range of services, including contactless transactions, bill payments, and cardless withdrawals. The growing demand for self-service banking solutions, reducing the need for human tellers, further accelerates this trend, enhancing operational efficiency for financial institutions. Additionally, the proliferation of cross-border remittances in certain regions drives the demand for accessible cash withdrawal points, further supporting market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Financial Inclusion | +1.8% | Asia Pacific, Latin America, MEA | Long Term |

| Growing Demand for Self-Service Banking | +1.5% | Global | Medium Term |

| Technological Advancements & Upgrades | +1.2% | North America, Europe, APAC | Medium Term |

| Urbanization and Infrastructure Development | +1.0% | Emerging Economies | Long Term |

| Cross-Border Remittances | +0.8% | Specific Corridors, Developing Nations | Medium Term |

ATM Machine Market Restraints Analysis

The accelerating global shift towards digital payment methods, including mobile wallets, online banking, and contactless card payments, presents a significant restraint. In many developed markets, cash usage is steadily declining, directly impacting the demand for ATM transactions. This trend forces financial institutions to re-evaluate their ATM deployment strategies and consider alternative investment in digital channels, potentially leading to a reduction in new ATM installations in certain areas.

High operational and maintenance costs associated with ATM networks, including cash replenishment, security, software updates, and physical maintenance, pose a substantial burden on banks. These costs can erode profitability, especially for older or less frequently used machines. Furthermore, the persistent threat of cyberattacks, skimming, and other forms of ATM fraud necessitates continuous investment in security upgrades and compliance measures, adding to the cost burden and potentially deterring further investment in new machines or expansion into new locations due to perceived security risks.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rise of Digital Payments & Cashless Trends | -1.5% | North America, Europe | Long Term |

| High Operational & Maintenance Costs | -1.2% | Global | Continuous |

| Cybersecurity Threats & Fraud Risks | -1.0% | Global | Continuous |

| Branchless Banking Models | -0.8% | Developed Markets | Medium Term |

| Declining Cash Usage in Specific Sectors | -0.7% | Retail, Urban Centers | Medium Term |

ATM Machine Market Opportunities Analysis

The concept of "ATM as a Service" (AaaS) presents a significant opportunity, allowing financial institutions to outsource ATM operations to third-party providers, thereby reducing capital expenditure and operational complexities. This model enables wider deployment and more efficient management of ATM networks, particularly in new or underserved markets. Additionally, the integration of advanced functionalities, such as cryptocurrency dispensing, biometric authentication, and personalized advertising, transforms ATMs into versatile self-service banking kiosks, creating new revenue streams and enhancing user engagement.

Untapped markets in developing regions, where banking infrastructure is still evolving, offer substantial growth potential for ATM deployment to enhance financial inclusion. The emergence of brown-label and white-label ATMs, operated by non-bank entities, further expands the market reach and accessibility, catering to a broader consumer base. Moreover, the focus on smart ATMs equipped with IoT capabilities for remote monitoring and predictive maintenance represents an opportunity for improved uptime, reduced operational costs, and the delivery of more efficient and reliable services, making them attractive investments for various stakeholders.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| ATM as a Service (AaaS) Model Adoption | +1.0% | Global | Medium Term |

| Expansion into Underserved & Rural Areas | +0.9% | Asia Pacific, Africa, Latin America | Long Term |

| Integration of New Technologies (e.g., Crypto) | +0.8% | Developed Markets, Specific Niches | Medium Term |

| Smart & IoT-enabled ATMs | +0.7% | Global | Medium Term |

| White-Label & Brown-Label ATM Growth | +0.6% | India, Southeast Asia, Brazil | Long Term |

ATM Machine Market Challenges Impact Analysis

Cybersecurity threats and sophisticated fraud techniques represent a continuous challenge for the ATM market. Skimming devices, malware attacks, and logical attacks necessitate constant vigilance and investment in advanced security measures, imposing significant financial and reputational risks on financial institutions. Ensuring compliance with evolving regulatory standards, particularly regarding data privacy and anti-money laundering, adds another layer of complexity, demanding significant resources for adherence and audit.

The evolving preferences of consumers towards digital banking channels pose a fundamental challenge to the traditional ATM model, particularly in developed economies. Financial institutions must adapt their strategies to maintain the relevance of ATMs by offering differentiated services that complement digital offerings, rather than being standalone cash points. Additionally, infrastructure deficits in certain regions, such as reliable power supply, internet connectivity, and physical security, can hinder the effective deployment and operation of ATM networks, especially in remote or challenging geographical areas.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advanced Cybersecurity Threats | -1.2% | Global | Continuous |

| Evolving Consumer Preferences for Digital Banking | -1.0% | Developed Markets | Medium Term |

| Regulatory Compliance & Anti-Fraud Measures | -0.9% | Global | Continuous |

| Infrastructure Limitations (Power, Connectivity) | -0.7% | Developing Regions | Long Term |

| Competition from Fintech Solutions | -0.6% | Global | Medium Term |

ATM Machine Market - Updated Report Scope

This market research report offers an extensive and up-to-date analysis of the global ATM Machine market. It delves into current market dynamics, growth drivers, restraints, and emerging opportunities, providing a comprehensive understanding of the industry landscape. The report covers detailed market segmentation by type, application, technology, and functionality, alongside an in-depth regional analysis. It also highlights the competitive landscape by profiling key market players, offering strategic insights for stakeholders to navigate the market effectively.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.5 Billion |

| Market Forecast in 2033 | USD 36.6 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NCR Corporation, Diebold Nixdorf, Hitachi-Omron Terminal Solutions, GRG Banking, Hyosung TNS, Euronet Worldwide, Fuji Electric, Oki Electric Industry, HESS Cash Systems, Nautilus Hyosung, BranchServ, Wincor Nixdorf International GmbH, Glory Ltd., Delarue, Crane Payment Innovations |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ATM machine market is broadly segmented to provide a granular view of its diverse landscape, enabling a deeper understanding of specific market dynamics and growth opportunities within each category. This detailed segmentation helps in identifying key areas of investment, technological focus, and regional relevance, allowing stakeholders to tailor strategies for optimal market penetration and expansion. By analyzing each segment, a comprehensive picture of the market's current state and future potential emerges.

Each segment, whether by type, application, technology, or functionality, represents distinct customer needs and operational models. For instance, the shift from conventional to smart ATMs reflects the increasing demand for advanced features, while the growth of brown-label and white-label ATMs indicates a rising trend in outsourced or non-bank operated services. Understanding these distinctions is crucial for manufacturers, service providers, and financial institutions to innovate and adapt their offerings to specific market demands and regulatory environments across different geographies.

- By Type:

- Conventional ATM

- Smart ATM

- Brown Label ATM

- White Label ATM

- By Application:

- On-Premise

- Off-Premise

- Mobile ATM

- By Technology:

- Hardware

- Card Reader

- Dispenser

- Processor

- Touchscreen

- Others

- Software

- Operating Systems

- Security Software

- Application Software

- Services

- Deployment & Installation

- Maintenance & Repair

- Managed Services

- Hardware

- By Functionality:

- Cash Dispenser

- Cash Recycler

- Deposit

- Information Terminal

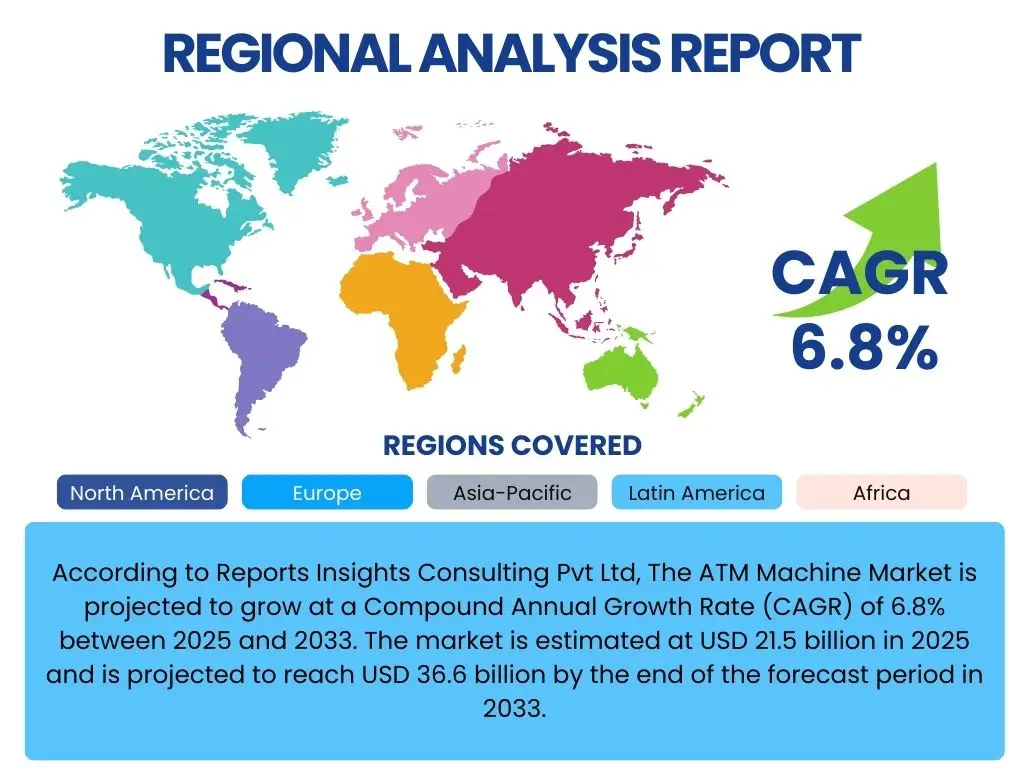

Regional Highlights

- North America: Characterized by early adoption of advanced ATM technologies, a strong focus on self-service banking, and a high rate of digital payment usage, leading to market evolution towards smart, multi-functional ATMs rather than sheer volume expansion.

- Europe: Exhibits a mature market with significant emphasis on security enhancements, regulatory compliance, and the integration of contactless and biometric features. Diverse regional trends exist, with some countries maintaining high cash usage while others rapidly transition to cashless societies.

- Asia Pacific (APAC): Represents the largest and fastest-growing market, driven by expanding financial inclusion initiatives, rapid urbanization, and a large unbanked population. Significant investments in new ATM deployments, especially brown-label and white-label, and the adoption of technologically advanced machines are prevalent.

- Latin America: Shows robust growth propelled by increasing financial literacy, urbanization, and a consistent demand for accessible banking services. The region is witnessing a rise in ATM installations in both urban and rural areas to serve underserved communities and facilitate remittances.

- Middle East and Africa (MEA): Emerging as a high-potential market due to ongoing economic diversification, government initiatives for financial inclusion, and a relatively untapped banking sector. Investments in secure and technologically updated ATM infrastructure are increasing to support growing economic activity and provide basic banking access.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the ATM Machine Market.- NCR Corporation

- Diebold Nixdorf

- Hitachi-Omron Terminal Solutions

- GRG Banking

- Hyosung TNS

- Euronet Worldwide

- Fuji Electric

- Oki Electric Industry

- HESS Cash Systems

- Nautilus Hyosung

- BranchServ

- Wincor Nixdorf International GmbH

- Glory Ltd.

- Delarue

- Crane Payment Innovations

Frequently Asked Questions

Are ATM machines still relevant in an increasingly cashless society?

Yes, ATM machines remain highly relevant. While digital payments are rising, ATMs are evolving into multi-functional self-service banking terminals that offer services beyond cash, such as bill payments, cardless withdrawals, and account inquiries. They also play a crucial role in financial inclusion, particularly in developing economies and rural areas where access to traditional banking services is limited, ensuring continued cash accessibility for a significant portion of the global population.

What are the latest technological advancements in ATM machines?

The latest advancements include contactless transaction capabilities (NFC), biometric authentication (fingerprint, facial recognition), AI-powered fraud detection, and predictive maintenance. Smart ATMs now incorporate IoT for remote monitoring and offer expanded functionalities like cryptocurrency dispensing and interactive video teller services, making them more secure, efficient, and versatile.

How do ATM machines contribute to financial inclusion?

ATMs significantly enhance financial inclusion by providing accessible banking services, especially for unbanked and underbanked populations in remote or underserved areas. They offer convenient cash access, deposit services, and often serve as the primary banking touchpoint where traditional bank branches are scarce, enabling broader participation in the formal economy.

What is the 'ATM as a Service' (AaaS) model?

ATM as a Service (AaaS) is a business model where financial institutions outsource their ATM operations, including hardware, software, maintenance, cash management, and security, to third-party providers. This model allows banks to reduce capital expenditure, streamline operations, and expand their ATM network without directly managing the infrastructure, leading to greater efficiency and market reach.

What are the primary security concerns for ATM machines?

Primary security concerns include physical attacks (skimming, cash trapping), logical attacks (malware, network intrusion), and cyber fraud. To counter these, the industry is increasingly adopting advanced security measures such as anti-skimming devices, end-to-end encryption, multi-factor authentication, AI-driven fraud detection, and advanced surveillance systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted