Semiconductor Wafer Used Electrostatic Chuck Market

Semiconductor Wafer Used Electrostatic Chuck Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704952 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Semiconductor Wafer Used Electrostatic Chuck Market Size

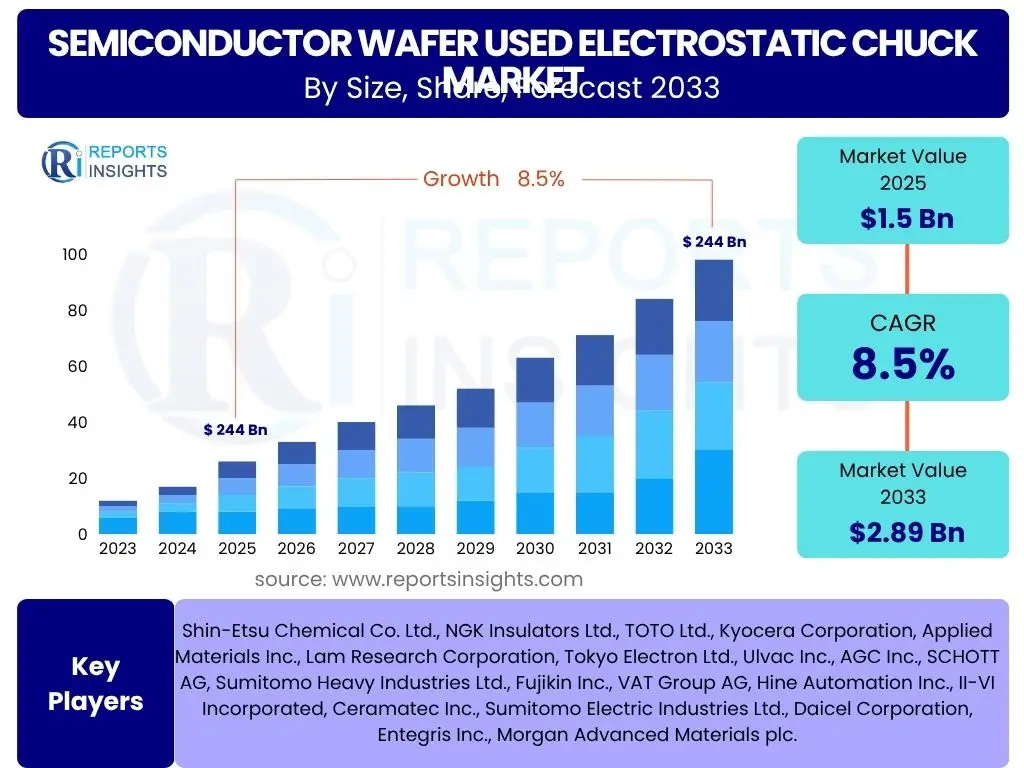

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Wafer Used Electrostatic Chuck Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 1.5 Billion in 2025 and is projected to reach USD 2.89 Billion by the end of the forecast period in 2033.

Key Semiconductor Wafer Used Electrostatic Chuck Market Trends & Insights

The Semiconductor Wafer Used Electrostatic Chuck (ESC) market is undergoing significant transformation driven by advancements in semiconductor manufacturing and increasing demand for higher performance and smaller devices. Common user questions often revolve around the technologies enabling next-generation chips, the impact of wafer size changes, and the shift towards more complex fabrication processes. These inquiries highlight a collective interest in how ESC technology is evolving to meet the stringent demands of advanced lithography, etching, and deposition processes, which require unprecedented precision and control.

Furthermore, users frequently inquire about the integration of new materials in ESCs, the development of more efficient cooling systems, and the ability of ESCs to handle extremely thin and fragile wafers. The growing adoption of advanced packaging technologies, such as 3D ICs and fan-out wafer-level packaging (FOWLP), also piques user interest, as these methods necessitate specialized chuck designs capable of managing diverse substrate types and complex architectures. The emphasis is increasingly on solutions that offer enhanced temperature uniformity, superior clamping force, and reduced particle contamination to improve manufacturing yields and overall device performance.

- Miniaturization and advanced node adoption driving demand for high-precision ESCs.

- Shift towards larger wafer sizes (300mm and beyond) necessitating robust ESC designs.

- Development of hybrid and multi-functional ESCs for varied process applications.

- Increased focus on temperature control and uniformity across the wafer surface.

- Integration of smart features for real-time monitoring and predictive maintenance.

- Growing adoption of ceramic and advanced material ESCs for superior performance.

AI Impact Analysis on Semiconductor Wafer Used Electrostatic Chuck

Common user questions related to the impact of Artificial Intelligence (AI) on Semiconductor Wafer Used Electrostatic Chucks (ESCs) often center on how AI can enhance manufacturing efficiency, optimize process parameters, and improve predictive capabilities. Users are keen to understand how AI-driven analytics can translate into better yield rates, reduced downtime, and more precise control over the complex etching, deposition, and lithography processes where ESCs are critical. The core interest lies in AI's potential to move beyond traditional process control towards intelligent, self-optimizing fabrication environments.

Another significant area of user inquiry concerns AI's role in predictive maintenance for ESCs, anticipating failures before they occur, and optimizing maintenance schedules to minimize operational disruptions. Users also explore how AI can be leveraged for real-time data analysis from ESC sensors to detect anomalies, fine-tune clamping forces, and ensure optimal temperature distribution across the wafer. The integration of AI aims to foster a more adaptive and resilient manufacturing ecosystem, allowing ESCs to perform at peak efficiency while reducing human intervention and the risk of errors, ultimately contributing to higher quality semiconductor devices.

- AI-driven process optimization for enhanced temperature uniformity and clamping force.

- Predictive maintenance algorithms for ESCs to reduce unplanned downtime.

- Real-time data analytics from ESC sensors for immediate anomaly detection and process correction.

- Improved yield management through AI-powered insights on wafer defects related to chuck performance.

- Automated calibration and self-correction mechanisms for ESCs using machine learning.

- Enhanced material characterization and selection for ESC components using AI models.

Key Takeaways Semiconductor Wafer Used Electrostatic Chuck Market Size & Forecast

Analyzing common user questions about the Semiconductor Wafer Used Electrostatic Chuck (ESC) market size and forecast reveals a strong interest in understanding the core drivers of growth, the segments offering the most promising opportunities, and the overall trajectory of the market. Users are particularly keen on identifying the critical technological advancements and industry shifts that will shape the market's expansion over the forecast period. The insights sought often include how the escalating demand for advanced electronic devices directly translates into growth within the ESC segment, which is a foundational component in chip manufacturing.

Furthermore, inquiries frequently touch upon the resilience of the market against potential macroeconomic headwinds, the impact of global supply chain dynamics, and the competitive landscape among key manufacturers. Users want to discern whether the market is primarily driven by volume increases in wafer production or by the rising complexity and value of individual ESC units. The emphasis is on gaining a clear, concise understanding of the market's future potential, identifying strategic entry points, and assessing long-term investment viability within the semiconductor equipment ecosystem.

- Strong growth projected, driven by increasing semiconductor demand and advanced manufacturing needs.

- Technological innovations in ESC design are crucial for market expansion.

- Asia Pacific is expected to remain the dominant region due to robust chip manufacturing infrastructure.

- Focus on precision and contamination control will dictate future product development.

- Opportunities exist in specialized ESCs for emerging applications like quantum computing and AI accelerators.

- Market resilience linked to sustained global investment in foundry capacity expansion.

Semiconductor Wafer Used Electrostatic Chuck Market Drivers Analysis

The Semiconductor Wafer Used Electrostatic Chuck (ESC) market is significantly propelled by the relentless demand for smaller, more powerful, and energy-efficient electronic devices. This demand directly translates into increased semiconductor manufacturing, requiring advanced fabrication processes that rely heavily on high-performance ESCs. As chip designers push the boundaries of Moore's Law, the need for precise wafer handling, superior temperature control, and minimized particle contamination becomes paramount, directly boosting the demand for sophisticated ESC solutions.

Another major driver is the global expansion of semiconductor fabrication capacities, particularly in Asia Pacific, coupled with substantial investments in new foundries and upgrades to existing ones. Governments worldwide are also fostering domestic chip production capabilities, further stimulating market growth. Additionally, the proliferation of emerging technologies such as Artificial Intelligence, 5G, IoT, and high-performance computing creates a continuous need for advanced semiconductors, thereby sustaining and accelerating the demand for the intricate and reliable wafer clamping provided by electrostatic chucks.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Semiconductor Device Demand | +1.5% | Global, particularly Asia Pacific, North America | Long-term (5-8 years) |

| Technological Advancements in Wafer Fabrication | +1.2% | Global, focused on leading-edge foundries | Mid-term (3-5 years) |

| Expansion of Foundry Capacities | +1.0% | Asia Pacific (Taiwan, South Korea, China), North America (US) | Short-term to Mid-term (1-5 years) |

| Growing Adoption of Advanced Packaging Technologies | +0.8% | Global | Mid-term (3-5 years) |

| Government Initiatives and Subsidies for Chip Manufacturing | +0.7% | North America, Europe, China | Long-term (5-8 years) |

Semiconductor Wafer Used Electrostatic Chuck Market Restraints Analysis

Despite robust growth drivers, the Semiconductor Wafer Used Electrostatic Chuck (ESC) market faces several notable restraints. A primary concern is the high cost associated with manufacturing and implementing advanced ESCs. These chucks often incorporate sophisticated materials and precise fabrication techniques, leading to significant capital expenditure for semiconductor manufacturers. This elevated cost can particularly affect smaller fabrication plants or those with limited budgets, potentially slowing down the adoption of the latest ESC technologies and impacting market expansion.

Another significant restraint is the technical complexity involved in ESC design and maintenance. Achieving uniform clamping, precise temperature control, and extended lifespan requires highly specialized expertise, and any failure can lead to substantial production losses. Furthermore, strict quality control standards and the need for zero contamination in semiconductor environments pose continuous challenges, driving up research and development costs and potentially limiting the speed of innovation. Geopolitical tensions and trade restrictions, particularly concerning technology exports, can also disrupt supply chains and hinder market growth in specific regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing and Implementation Costs | -0.8% | Global, impacting smaller fabs | Long-term (5-8 years) |

| Technical Complexity and Maintenance Challenges | -0.6% | Global, affecting operational efficiency | Mid-term (3-5 years) |

| Stringent Purity and Contamination Control Requirements | -0.5% | Global, especially leading-edge manufacturing | Continuous |

| Supply Chain Vulnerabilities and Geopolitical Tensions | -0.4% | Global, particularly between key trade blocs | Short-term (1-3 years) |

Semiconductor Wafer Used Electrostatic Chuck Market Opportunities Analysis

The Semiconductor Wafer Used Electrostatic Chuck (ESC) market is presented with significant opportunities stemming from the continuous evolution of semiconductor technology and the emergence of new application areas. The increasing demand for advanced materials in chip manufacturing, such as Gallium Nitride (GaN) and Silicon Carbide (SiC) for power electronics and RF devices, opens avenues for specialized ESCs designed to handle these unique material properties and process requirements. This diversification creates a need for chucks capable of operating under more extreme temperatures or with different electrical properties.

Moreover, the advent of next-generation computing paradigms like quantum computing and neuromorphic computing, while nascent, signifies long-term growth opportunities for highly specialized and ultra-precise ESCs. The integration of artificial intelligence and machine learning into semiconductor fabrication processes offers a chance to develop "smart" ESCs that can self-optimize and provide real-time feedback, further enhancing efficiency and yield. Additionally, the push towards sustainability and energy efficiency in manufacturing encourages the development of more energy-efficient ESC designs and materials, appealing to environmentally conscious manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of ESCs for Advanced Materials (GaN, SiC) | +0.9% | Global, focused on power electronics and RF | Mid-term to Long-term (3-8 years) |

| Integration of AI and Machine Learning for Smart ESCs | +0.8% | Global, impacting high-volume manufacturing | Mid-term (3-5 years) |

| Growth in Emerging Computing Technologies (Quantum, Neuromorphic) | +0.7% | Global, R&D focused regions | Long-term (5-8 years) |

| Focus on Sustainability and Energy-Efficient Manufacturing | +0.6% | Europe, North America, Japan | Mid-term (3-5 years) |

Semiconductor Wafer Used Electrostatic Chuck Market Challenges Impact Analysis

The Semiconductor Wafer Used Electrostatic Chuck (ESC) market faces several significant challenges that could impede its growth and innovation. One critical challenge is the escalating complexity of semiconductor processes, which demands increasingly sophisticated ESC designs capable of precise temperature uniformity, exceptionally tight flatness tolerances, and robust particle control across larger wafer sizes. Meeting these exacting technical specifications requires substantial investment in research and development, posing a barrier to entry for new players and adding pressure on established manufacturers.

Another major challenge is maintaining the integrity and long-term performance of ESCs in harsh manufacturing environments characterized by extreme temperatures, corrosive chemicals, and high-frequency plasma. The degradation of ESC materials over time, leading to reduced clamping force or surface damage, can result in significant yield losses and increased operational costs due to frequent replacement or maintenance. Furthermore, the rapid pace of technological obsolescence in the semiconductor industry means that ESC manufacturers must continuously innovate to keep pace with evolving process requirements, demanding agile development cycles and significant capital outlay. Supply chain disruptions, exacerbated by global events, also present a persistent challenge, affecting the availability and cost of raw materials and specialized components required for ESC production.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Technical Complexity of Wafer Processing | -0.7% | Global, impacting R&D and manufacturing | Continuous |

| Maintaining Performance in Harsh Manufacturing Environments | -0.6% | Global, affecting operational efficiency and lifespan | Long-term (5-8 years) |

| Rapid Technological Obsolescence and Need for Constant Innovation | -0.5% | Global, impacting market competitiveness | Short-term to Mid-term (1-5 years) |

| Supply Chain Disruptions and Raw Material Availability | -0.4% | Global, impacting production schedules | Short-term (1-3 years) |

Semiconductor Wafer Used Electrostatic Chuck Market - Updated Report Scope

This report offers a comprehensive analysis of the Semiconductor Wafer Used Electrostatic Chuck market, detailing its current size, historical performance, and future growth projections. It delves into the driving forces and restraining factors influencing market dynamics, identifies key opportunities, and addresses prevailing challenges. The scope encompasses detailed market segmentation, regional analyses, and profiles of leading industry players, providing a holistic view of the market landscape and critical insights for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.89 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Shin-Etsu Chemical Co. Ltd., NGK Insulators Ltd., TOTO Ltd., Kyocera Corporation, Applied Materials Inc., Lam Research Corporation, Tokyo Electron Ltd., Ulvac Inc., AGC Inc., SCHOTT AG, Sumitomo Heavy Industries Ltd., Fujikin Inc., VAT Group AG, Hine Automation Inc., II-VI Incorporated, Ceramatec Inc., Sumitomo Electric Industries Ltd., Daicel Corporation, Entegris Inc., Morgan Advanced Materials plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Wafer Used Electrostatic Chuck (ESC) market is comprehensively segmented to provide a granular understanding of its diverse components and their respective growth trajectories. This segmentation allows for a detailed analysis of market dynamics across various product types, operational mechanisms, and application areas within the semiconductor manufacturing ecosystem. Understanding these distinct segments is crucial for identifying specific market opportunities, tailoring product development, and devising effective market entry strategies.

The market is primarily categorized by the material composition of the chuck (Type), the configuration of the electrodes (Electrode Type), the specific fabrication processes they are used in (Application), and the type of semiconductor entity utilizing them (End-User). Each segment plays a vital role in the overall market, with specific technologies and operational demands driving their individual growth and evolution. This multi-dimensional segmentation ensures a precise and actionable market overview, addressing the nuances of the complex semiconductor industry.

- By Type:

- Ceramic Electrostatic Chucks: Widely used for their high temperature stability and excellent dielectric properties, crucial for advanced processes.

- Quartz Electrostatic Chucks: Preferred in certain applications requiring high purity and specific thermal characteristics.

- Other Materials: Including advanced composite materials and specialized polymers, catering to niche or emerging process demands.

- By Electrode Type:

- Monopolar: Simpler design, generally used for basic clamping.

- Bipolar: Offers enhanced clamping force and precise control, commonly used in more demanding processes.

- Multipole: Provides highly localized and precise clamping, vital for managing wafer distortion in critical applications.

- By Application:

- Etching: Dominant application, requiring high temperature uniformity and robust clamping.

- Physical Vapor Deposition (PVD): Used for thin film deposition processes.

- Chemical Vapor Deposition (CVD): Critical for uniform material deposition.

- Lithography: Demands extreme precision and flatness.

- Metrology: Used for highly accurate wafer measurement and inspection.

- Ion Implantation: Requires stable wafer positioning during ion bombardment.

- Other Applications: Including wafer testing, grinding, and specialized R&D processes.

- By End-User:

- Foundries: Independent manufacturers producing chips for fabless companies, representing a significant market share.

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and sell their own chips, utilizing ESCs in their internal fabrication lines.

- Outsourced Semiconductor Assembly and Test (OSAT): Companies providing post-fabrication services, increasingly adopting ESCs for advanced packaging steps.

Regional Highlights

- Asia Pacific (APAC): Dominates the Semiconductor Wafer Used Electrostatic Chuck market due to the concentration of major semiconductor manufacturing hubs in countries like Taiwan, South Korea, China, and Japan. The region benefits from massive investments in new fab construction and capacity expansion by leading foundries and IDMs, driven by global demand for consumer electronics, automotive chips, and AI processors. This robust ecosystem ensures continued demand for advanced ESCs.

- North America: A significant market driven by strong research and development activities, particularly in advanced node technology and high-performance computing. The presence of leading semiconductor equipment manufacturers and cutting-edge foundries, coupled with government initiatives to boost domestic chip production, fuels the demand for innovative and high-precision ESC solutions. The focus here is often on high-value, niche applications.

- Europe: Exhibits steady growth, propelled by robust automotive electronics, industrial IoT, and advanced research initiatives. Countries like Germany, France, and the Netherlands host key players in semiconductor equipment manufacturing and specialty chip production. The emphasis on smart factories and sustainable manufacturing practices also contributes to the adoption of advanced ESC technologies in the region.

- Latin America: Currently a smaller market, but with emerging potential as several countries explore opportunities in semiconductor assembly and testing. While not a primary manufacturing hub for wafers, increasing investment in supporting industries could drive incremental demand for specific ESC applications in the long term.

- Middle East and Africa (MEA): Represents a nascent market with limited direct semiconductor manufacturing. However, increasing technological adoption and diversification efforts in some economies, particularly in areas like data centers and digital infrastructure, could indirectly create future demand for semiconductor components, thus impacting the ESC market on a smaller scale over the forecast period.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Wafer Used Electrostatic Chuck Market.- Shin-Etsu Chemical Co. Ltd.

- NGK Insulators Ltd.

- TOTO Ltd.

- Kyocera Corporation

- Applied Materials Inc.

- Lam Research Corporation

- Tokyo Electron Ltd.

- Ulvac Inc.

- AGC Inc.

- SCHOTT AG

- Sumitomo Heavy Industries Ltd.

- Fujikin Inc.

- VAT Group AG

- Hine Automation Inc.

- II-VI Incorporated

- Ceramatec Inc.

- Sumitomo Electric Industries Ltd.

- Daicel Corporation

- Entegris Inc.

- Morgan Advanced Materials plc.

Frequently Asked Questions

Analyze common user questions about the Semiconductor Wafer Used Electrostatic Chuck market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is an Electrostatic Chuck (ESC) used for in semiconductor manufacturing?

An Electrostatic Chuck (ESC) is a critical component in semiconductor manufacturing equipment used to hold semiconductor wafers securely in place using electrostatic force during various processing steps, such as etching, deposition, lithography, and ion implantation, ensuring precise alignment and temperature control.

What are the primary factors driving the growth of the ESC market?

The primary factors driving ESC market growth include the increasing global demand for advanced semiconductor devices, continuous miniaturization and adoption of smaller process nodes, significant investments in new foundry capacities, and the rising complexity of wafer fabrication processes requiring superior precision and control.

How does AI impact the Semiconductor Wafer Used Electrostatic Chuck market?

AI impacts the ESC market by enabling advanced process optimization for enhanced temperature uniformity and clamping force, facilitating predictive maintenance to reduce downtime, and supporting real-time data analytics from ESC sensors for immediate anomaly detection and improved yield management.

Which regions are leading the market for Electrostatic Chucks?

The Asia Pacific region, particularly countries like Taiwan, South Korea, China, and Japan, leads the market for Electrostatic Chucks due to its dominant position in global semiconductor manufacturing and ongoing investments in new fabrication facilities. North America and Europe also hold significant market shares driven by advanced R&D and specialized chip production.

What are the key challenges faced by the ESC market?

Key challenges for the ESC market include the high manufacturing and implementation costs of advanced chucks, the technical complexity required for precise design and maintenance, stringent purity and contamination control standards, and the need for constant innovation to keep pace with rapidly evolving semiconductor technologies and harsh operating environments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted