Semiconductor Market

Semiconductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704873 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Semiconductor Market Size

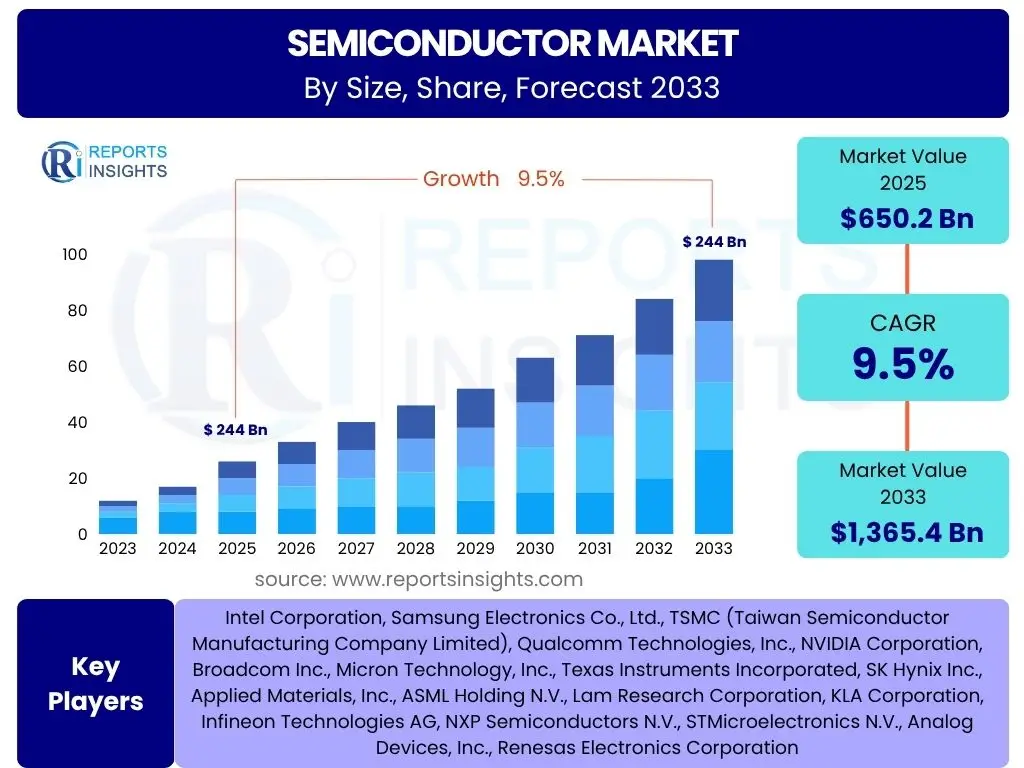

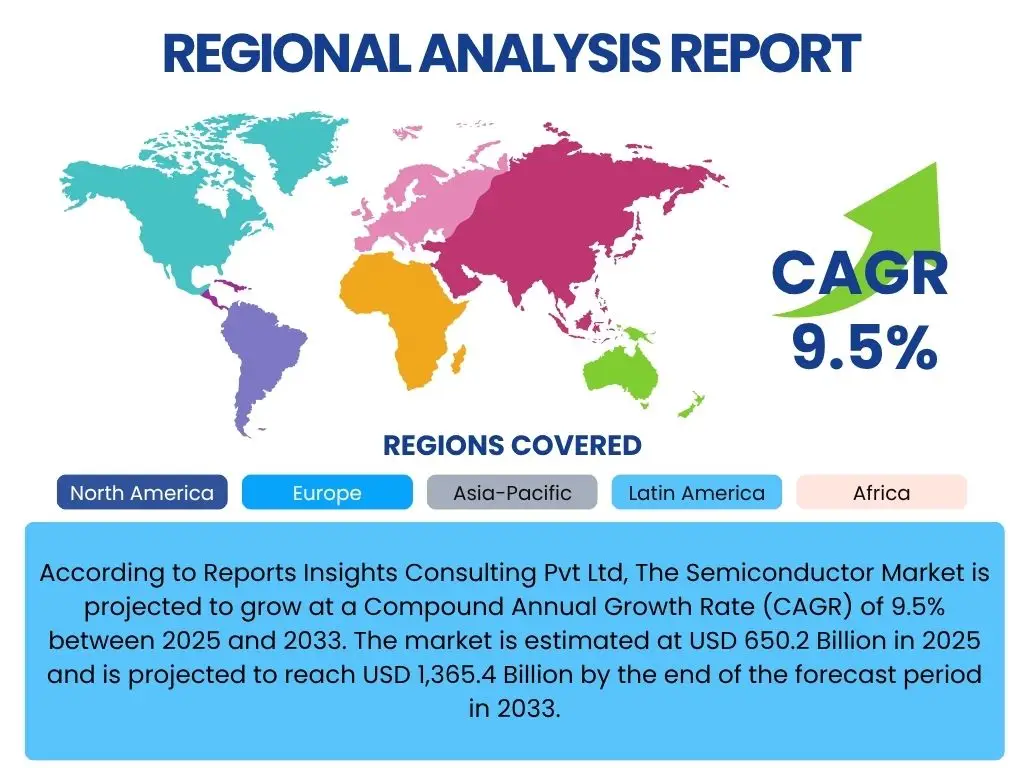

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 650.2 Billion in 2025 and is projected to reach USD 1,365.4 Billion by the end of the forecast period in 2033.

Key Semiconductor Market Trends & Insights

The semiconductor market is currently experiencing significant shifts driven by technological advancements and evolving global demands. Users frequently inquire about the trajectory of miniaturization, the impact of geopolitical factors on supply chains, and the proliferation of semiconductor applications beyond traditional computing. Key insights reveal a persistent drive towards smaller, more powerful, and energy-efficient chips, alongside an increasing emphasis on resilient and diversified supply chains to mitigate risks. Furthermore, the integration of semiconductors into an ever-expanding array of devices, from smart vehicles to advanced medical equipment, is redefining market dynamics and fostering new growth avenues. The interplay between innovation, geopolitical stability, and supply chain robustness remains a central theme shaping the industry's future.

Another crucial trend gaining prominence is the adoption of advanced packaging technologies, which allow for heterogeneous integration and improved performance without necessarily shrinking transistor sizes. This approach addresses the physical limitations of Moore's Law and enables higher levels of functionality and power efficiency in a smaller footprint. Additionally, the industry is witnessing a strong push towards sustainable manufacturing practices and the development of wide-bandgap (WBG) materials like SiC and GaN, which offer superior performance in power electronics, crucial for electric vehicles and renewable energy systems. These trends collectively underscore a dynamic and adaptable industry focused on both innovation and operational resilience.

- Miniaturization and advanced node development continuing but complemented by advanced packaging.

- Increased focus on supply chain resilience and regionalization amidst geopolitical shifts.

- Proliferation of semiconductors into new high-growth applications such as automotive and industrial IoT.

- Growing demand for specialized chips for Artificial Intelligence (AI) and Machine Learning (ML).

- Emergence of Wide Bandgap (WBG) materials (SiC, GaN) for power efficiency and high-performance applications.

- Integration of advanced sensor technologies across diverse sectors.

- Emphasis on sustainable manufacturing practices and energy-efficient chip designs.

AI Impact Analysis on Semiconductor

User queries regarding AI's influence on the semiconductor industry often center on its role as both a driver of demand for specialized chips and a transformative tool within the semiconductor manufacturing process itself. There is significant interest in understanding how AI will reshape chip architecture, lead to the development of new computational paradigms, and impact the competitive landscape. Expectations are high for AI to accelerate design cycles, optimize fabrication processes, and enhance chip performance for specific AI workloads. Concerns typically revolve around the immense power consumption of AI chips and the significant investment required for advanced AI-driven research and development.

The integration of Artificial Intelligence and Machine Learning is profoundly reshaping the semiconductor landscape, creating unprecedented demand for high-performance computing (HPC) and specialized AI accelerators. AI applications, from cloud-based inference to edge computing, require chips capable of handling massive parallel processing and complex neural network operations, driving innovation in GPU, ASIC, and FPGA designs. This demand not only boosts the revenue of chip manufacturers but also pushes the boundaries of chip architecture and materials science. Furthermore, AI is increasingly being applied within semiconductor design and manufacturing, optimizing everything from mask layout to yield management, leading to more efficient and cost-effective production processes.

- AI as a primary driver for demand in high-performance computing (HPC) chips and specialized accelerators (GPUs, ASICs).

- Acceleration of chip design and verification processes through AI-driven EDA tools.

- Optimization of semiconductor manufacturing, including predictive maintenance and yield enhancement, using AI algorithms.

- Development of new chip architectures and memory technologies specifically optimized for AI workloads.

- Increased focus on energy efficiency in AI chip design to mitigate power consumption challenges.

- Facilitation of edge AI processing requiring low-power, high-efficiency semiconductor solutions.

- Intensification of competition among semiconductor companies to lead in AI chip innovation.

Key Takeaways Semiconductor Market Size & Forecast

Common questions about the semiconductor market size and forecast reveal a strong user interest in understanding the primary growth catalysts, the segments poised for the most significant expansion, and the long-term investment outlook. Key insights indicate that sustained growth is primarily fueled by the pervasive digitalization across industries, the exponential rise of data, and the relentless pursuit of automation. The market forecast underscores a robust upward trajectory, highlighting the critical role semiconductors play as foundational technology for almost every modern industry. Investment opportunities are particularly strong in segments supporting AI, automotive electronics, and advanced connectivity solutions.

The analysis of the semiconductor market size and its projected growth reveals several critical takeaways for stakeholders. The market's resilience is evident in its ability to navigate global economic uncertainties, driven by fundamental long-term trends such as the digital transformation, the proliferation of the Internet of Things (IoT), and the burgeoning demand for cloud services. Future growth will be significantly shaped by advancements in fabrication processes, the development of novel materials, and the expansion into new application areas like quantum computing and advanced robotics. The forecast period anticipates a shift towards more specialized and integrated solutions, emphasizing the importance of strategic partnerships and vertical integration within the ecosystem.

- Digital transformation across all industries is a primary growth engine for semiconductor demand.

- Automotive electronics, AI, and data centers are key segments driving substantial market expansion.

- The market exhibits strong long-term growth prospects, despite short-term cyclical fluctuations.

- Investments are increasingly focused on advanced manufacturing capabilities and R&D for next-generation chips.

- Geopolitical factors and supply chain resilience remain critical considerations for future market stability.

- Emerging economies, particularly in Asia Pacific, are poised for significant contribution to market growth.

- Focus on energy efficiency and sustainable practices is becoming an increasingly important competitive differentiator.

Semiconductor Market Drivers Analysis

The semiconductor market's robust growth is primarily propelled by an accelerating global digital transformation, demanding ever-increasing computational power and connectivity. The proliferation of smart devices, the expansion of cloud computing infrastructure, and the roll-out of 5G networks are creating unprecedented demand for advanced chips. Furthermore, the automotive sector's shift towards electric vehicles and autonomous driving, coupled with the rapid adoption of Artificial Intelligence and the Internet of Things across various industries, are significantly broadening the application scope for semiconductors, cementing their foundational role in modern technological progress.

These drivers collectively contribute to a continuous need for innovation in chip design and manufacturing. The rising complexity of software and the demand for real-time processing necessitate more powerful and efficient semiconductor solutions. Government initiatives and investments in digital infrastructure, along with the growing consumer appetite for high-tech gadgets and smart home devices, further stimulate market expansion. The synergy between these factors ensures a sustained and dynamic growth trajectory for the semiconductor industry, pushing technological boundaries and opening new avenues for market penetration and development.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Consumer Electronics & Connectivity (5G) | +2.5% | Global, particularly Asia Pacific & North America | Short-term to Mid-term (2025-2030) |

| Rising Adoption of AI, IoT, and Cloud Computing | +3.0% | Global, especially North America, Europe, China | Mid-term to Long-term (2026-2033) |

| Growth in Automotive Electronics and Electric Vehicles (EVs) | +2.0% | Europe, North America, China, Japan | Mid-term to Long-term (2026-2033) |

| Government Support & Investment in Digital Infrastructure | +1.5% | United States, China, European Union, India | Short-term to Long-term (2025-2033) |

Semiconductor Market Restraints Analysis

Despite robust growth, the semiconductor market faces notable restraints that can impede its full potential. Geopolitical tensions and trade disputes, particularly between major economic powers, lead to uncertainty in supply chains and impose export restrictions, disrupting global market dynamics. The capital-intensive nature of semiconductor manufacturing, requiring billions of dollars for new fabs, creates high barriers to entry and limits the number of players capable of scaling production. Furthermore, the inherent cyclicality of the industry, characterized by periods of oversupply and undersupply, can lead to significant revenue volatility and challenges in long-term planning.

Another significant restraint is the shortage of skilled labor, particularly in advanced manufacturing and design roles, which can hinder innovation and production capacity. The increasing complexity of chip designs also extends development cycles and elevates research and development costs, putting pressure on profit margins. Environmental regulations and the need for sustainable manufacturing practices, while crucial for long-term viability, can also add to operational costs and complexity for semiconductor companies. Addressing these multifaceted restraints requires strategic planning, international collaboration, and significant investment in workforce development.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Tensions & Trade Restrictions | -1.8% | Global, particularly US, China, Europe | Short-term to Mid-term (2025-2030) |

| High Capital Expenditure & R&D Costs | -1.5% | Global, impacts new entrants disproportionately | Long-term (2025-2033) |

| Supply Chain Vulnerabilities & Disruptions | -1.2% | Global, especially reliant on specific regions (e.g., Taiwan, Korea) | Short-term to Mid-term (2025-2028) |

| Shortage of Skilled Workforce | -1.0% | North America, Europe, parts of Asia | Mid-term to Long-term (2026-2033) |

Semiconductor Market Opportunities Analysis

The semiconductor market is rich with opportunities driven by technological convergence and the expansion into untapped application areas. The burgeoning demand for specialized chips in emerging technologies like quantum computing, advanced materials, and silicon photonics presents significant avenues for growth and innovation. The development of advanced packaging techniques allows for heterogeneous integration, enabling higher performance and efficiency without relying solely on transistor scaling, thus extending the capabilities of existing semiconductor technologies. Furthermore, the increasing integration of semiconductors in industrial automation, medical devices, and space technology offers diverse new market segments.

The ongoing push towards sustainable and green technologies also opens opportunities for power semiconductors and energy-efficient chip designs, catering to the growing global focus on environmental responsibility. Smart infrastructure projects, smart cities, and the increasing adoption of edge computing further expand the addressable market for a wide range of semiconductor components, from sensors to microcontrollers. These opportunities require continuous investment in research and development, strategic partnerships, and a keen understanding of evolving market needs to capitalize on the next wave of technological innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Quantum Computing & Advanced Materials | +1.7% | Global, particularly North America, Europe, China | Long-term (2028-2033) |

| Growth in Advanced Packaging Technologies | +1.5% | Global, particularly Asia Pacific | Mid-term to Long-term (2026-2033) |

| Expansion into Industrial Automation & Robotics | +1.2% | Europe, North America, Japan, China | Mid-term (2025-2030) |

| Increased Demand for Medical Electronics | +1.0% | North America, Europe, parts of Asia | Short-term to Mid-term (2025-2030) |

Semiconductor Market Challenges Impact Analysis

The semiconductor market faces several inherent challenges that demand strategic foresight and adaptability. Rapid technological obsolescence is a constant pressure, requiring continuous investment in research and development to stay competitive and ensure product relevance. The capital-intensive nature of manufacturing and the extended timelines for constructing new fabrication plants (fabs) mean significant financial risk and a slow response to sudden shifts in demand. Moreover, the industry is highly susceptible to global economic downturns, which can swiftly impact consumer spending and corporate investments, leading to reduced demand for chips.

Furthermore, the complex global supply chain, often relying on a few key suppliers for critical materials and equipment, remains vulnerable to disruptions from natural disasters, geopolitical events, or pandemics. Intellectual property theft and cybersecurity threats pose significant risks, potentially leading to financial losses and erosion of competitive advantage. Navigating the intricate web of international trade policies and environmental regulations also adds layers of complexity, requiring companies to constantly adapt their operational strategies. Overcoming these challenges necessitates innovation, robust risk management, and strong international collaboration.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -1.0% | Global | Continuous |

| High Capital Intensity & Long Fab Construction Times | -0.8% | Global | Long-term (2025-2033) |

| Intensified Global Competition & Price Erosion | -0.7% | Global | Continuous |

| Environmental Compliance & Sustainability Pressures | -0.5% | Europe, North America, Japan | Mid-term to Long-term (2026-2033) |

Semiconductor Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Semiconductor Market, covering historical data from 2019 to 2023, base year 2024, and forecasts from 2025 to 2033. It offers a detailed breakdown of market size, growth drivers, restraints, opportunities, and challenges, along with extensive segmentation by components, applications, end-use industries, and regions. The report aims to deliver actionable insights for stakeholders, investors, and industry participants to navigate the complex market landscape and make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650.2 Billion |

| Market Forecast in 2033 | USD 1,365.4 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, Samsung Electronics Co., Ltd., TSMC (Taiwan Semiconductor Manufacturing Company Limited), Qualcomm Technologies, Inc., NVIDIA Corporation, Broadcom Inc., Micron Technology, Inc., Texas Instruments Incorporated, SK Hynix Inc., Applied Materials, Inc., ASML Holding N.V., Lam Research Corporation, KLA Corporation, Infineon Technologies AG, NXP Semiconductors N.V., STMicroelectronics N.V., Analog Devices, Inc., Renesas Electronics Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor market is extensively segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for precise analysis of growth areas, technological shifts, and competitive landscapes across various product categories and end-use industries. Understanding these segments is crucial for identifying specific market opportunities, tailoring product development strategies, and optimizing resource allocation. The comprehensive breakdown highlights the intricate interdependencies within the semiconductor ecosystem, from the foundational integrated circuits to specialized sensors and discrete power devices, each catering to distinct market needs and technological demands. Such detailed segmentation facilitates targeted marketing and strategic investment decisions for industry participants.

Further analysis within these segments reveals varying growth rates and levels of maturity. For instance, the demand for Memory ICs often experiences cyclical fluctuations, while Logic ICs are consistently driven by innovation in computing and AI. The Optoelectronics segment is seeing robust growth propelled by advancements in LED lighting and optical communication. Similarly, the Sensors market is expanding rapidly due to the proliferation of IoT devices and autonomous systems. By dissecting the market into these specific categories, stakeholders can gain clearer insights into the drivers and challenges unique to each segment, enabling more informed decision-making and strategic planning.

- By Component: Integrated Circuits (Analog IC, Logic IC, Memory IC, Microprocessor & Microcontroller, Digital IC, Mixed-Signal IC), Optoelectronics (LEDs, Lasers, Photodetectors), Sensors (Temperature Sensors, Pressure Sensors, Image Sensors, Motion Sensors, Chemical Sensors), Discrete Power Devices (Diodes, Transistors, Thyristors, MOSFETs, IGBTs)

- By Application: Data Processing (PCs, Laptops, Servers, Data Centers), Communication (Smartphones, Tablets, Network Equipment), Automotive (Infotainment, ADAS, Powertrain, Body Electronics), Industrial (Automation, Robotics, Power Management), Consumer Electronics (Wearables, Smart Home Devices, Gaming Consoles), Healthcare (Medical Imaging, Diagnostics, Patient Monitoring), Aerospace & Defense

- By End-Use Industry: Electronics & IT, Automotive, Industrial, Healthcare, Telecommunications, Aerospace & Defense, Others

- By Wafer Size: 200mm, 300mm, Others

- By Technology: FinFET, Planar, FD-SOI, Others

Regional Highlights

- Asia Pacific (APAC): Dominates the global semiconductor market, largely due to major manufacturing hubs in Taiwan, South Korea, Japan, and increasing R&D and consumption in China. The region benefits from a robust electronics manufacturing ecosystem, large consumer bases, and significant government investments in semiconductor capabilities. Countries like India and Southeast Asian nations are emerging as significant growth areas due to growing digitalization and manufacturing initiatives.

- North America: A leader in semiconductor design, research, and development, particularly for high-end processors, AI chips, and specialized semiconductors. The region boasts a strong ecosystem of fabless companies and significant investment in advanced manufacturing technologies, with recent policy efforts aiming to boost domestic production capabilities and supply chain resilience.

- Europe: Characterized by strong expertise in automotive semiconductors, industrial automation, and power management solutions. Countries like Germany, France, and the Netherlands are home to leading semiconductor companies and research institutions, focusing on specialized applications and collaborative innovation, often supported by regional initiatives to strengthen the semiconductor value chain.

- Latin America: An emerging market for semiconductor consumption, driven by increasing smartphone penetration, automotive production, and industrial digitalization. While manufacturing presence is smaller, the region represents a growing end-user market and a potential area for future assembly, test, and packaging (ATP) operations.

- Middle East and Africa (MEA): Primarily a consumption market, with growing demand for semiconductors driven by investments in smart city projects, data centers, and telecommunications infrastructure. Governments in the GCC countries are actively exploring diversification into high-tech manufacturing, potentially opening opportunities for semiconductor-related investments in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Market.- Intel Corporation

- Samsung Electronics Co., Ltd.

- TSMC (Taiwan Semiconductor Manufacturing Company Limited)

- Qualcomm Technologies, Inc.

- NVIDIA Corporation

- Broadcom Inc.

- Micron Technology, Inc.

- Texas Instruments Incorporated

- SK Hynix Inc.

- Applied Materials, Inc.

- ASML Holding N.V.

- Lam Research Corporation

- KLA Corporation

- Infineon Technologies AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Analog Devices, Inc.

- Renesas Electronics Corporation

Frequently Asked Questions

Analyze common user questions about the Semiconductor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Semiconductor Market?

The Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033, indicating robust expansion driven by increasing digitalization and technological advancements.

Which factors are primarily driving the growth of the Semiconductor Market?

Key drivers include the pervasive digitalization across industries, exponential rise of data, expanding adoption of AI and IoT, roll-out of 5G networks, and the rapid growth in automotive electronics, particularly electric vehicles.

How is Artificial Intelligence (AI) impacting the Semiconductor Industry?

AI is significantly impacting the semiconductor industry by driving demand for specialized high-performance chips, accelerating chip design processes, optimizing manufacturing efficiency, and fostering innovation in new chip architectures.

What are the main challenges faced by the Semiconductor Market?

Major challenges include rapid technological obsolescence, high capital expenditure requirements for manufacturing facilities, complex global supply chain vulnerabilities, geopolitical tensions, and the persistent shortage of skilled labor.

Which region is expected to dominate the Semiconductor Market?

Asia Pacific (APAC) is expected to continue dominating the global semiconductor market due to its established manufacturing hubs, large consumer base, and significant government investments in the semiconductor ecosystem across countries like Taiwan, South Korea, Japan, and China.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted