GaN and SiC Power Semiconductor Market

GaN and SiC Power Semiconductor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705140 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

GaN and SiC Power Semiconductor Market Size

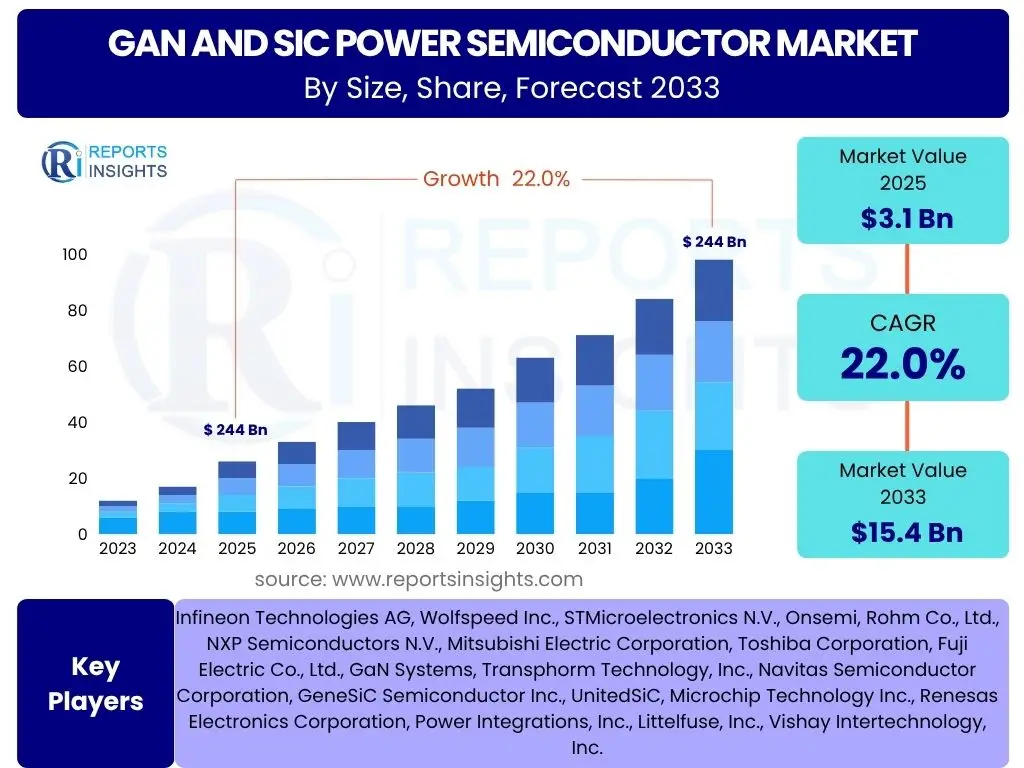

According to Reports Insights Consulting Pvt Ltd, The GaN and SiC Power Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.0% between 2025 and 2033. The market is estimated at USD 3.1 Billion in 2025 and is projected to reach USD 15.4 Billion by the end of the forecast period in 2033.

Key GaN and SiC Power Semiconductor Market Trends & Insights

User inquiries frequently highlight the rapid adoption of wide bandgap (WBG) semiconductors, particularly GaN and SiC, across a diverse range of high-power and high-frequency applications. There is considerable interest in how these materials are enabling significant advancements in energy efficiency and power density, which are critical for emerging technologies. Common questions revolve around the competitive advantages over traditional silicon, the speed of market penetration in specific sectors, and the ongoing developments in manufacturing processes that are driving down costs and improving performance. Insights point to a clear shift towards these next-generation materials as industries seek more robust and efficient power management solutions.

A notable trend is the escalating demand from the electric vehicle (EV) sector, where SiC is proving instrumental in improving the efficiency and range of on-board chargers, inverters, and DC-DC converters. Similarly, GaN is gaining traction in consumer electronics for fast chargers and compact power adapters, and in data centers for enhanced power supply units. The miniaturization capabilities and superior thermal performance of GaN and SiC are also key areas of focus. As research and development continue, the integration of advanced packaging technologies and improved reliability standards are further solidifying the market position of these innovative semiconductors.

- Accelerated adoption in Electric Vehicle (EV) powertrains for enhanced efficiency and extended range.

- Increased integration of GaN in consumer electronics, including ultra-fast chargers and compact power adapters.

- Growing demand from renewable energy systems, such as solar inverters and wind turbine converters.

- Significant advancements in manufacturing processes, leading to cost reduction and improved yield.

- Expansion into telecommunications infrastructure, particularly 5G base stations, requiring high power efficiency and compact designs.

AI Impact Analysis on GaN and SiC Power Semiconductor

User questions frequently probe the multifaceted impact of Artificial intelligence (AI) on the GaN and SiC power semiconductor market, focusing on how AI can both drive demand for these components and optimize their development and application. There is significant interest in AI's role in the design and simulation phases, predictive maintenance of power systems, and the overall energy efficiency requirements of AI data centers. Users are keen to understand if AI can accelerate the material discovery process or enhance manufacturing yields for these complex semiconductors, thereby reducing costs and improving performance. The prevailing expectation is that AI will be a dual-edged sword, acting as a catalyst for innovation within the WBG industry while simultaneously increasing the need for highly efficient power solutions.

The burgeoning field of AI necessitates increasingly powerful and energy-efficient computing infrastructure, directly fueling the demand for GaN and SiC power semiconductors in data centers and high-performance computing (HPC) environments. AI algorithms are also being deployed to optimize the design of GaN and SiC devices, leading to faster prototyping, improved performance metrics, and enhanced reliability. Furthermore, AI-driven predictive analytics can monitor the performance of power systems incorporating GaN and SiC, identifying potential failures before they occur and enabling proactive maintenance. This synergy between AI and WBG semiconductors is expected to drive further market expansion and technological advancement, pushing the boundaries of power conversion efficiency and system intelligence.

- AI-driven optimization of GaN and SiC device design and simulation, accelerating product development cycles.

- Increased demand for high-efficiency GaN and SiC power solutions in AI data centers and high-performance computing (HPC) infrastructure to manage escalating energy consumption.

- Application of AI in manufacturing processes for defect detection, yield optimization, and quality control in GaN and SiC wafer production.

- AI-enhanced predictive maintenance of power systems utilizing GaN and SiC, improving reliability and operational uptime.

- Facilitation of new material discovery and characterization for next-generation wide bandgap semiconductors through AI and machine learning algorithms.

Key Takeaways GaN and SiC Power Semiconductor Market Size & Forecast

User inquiries about key takeaways from the GaN and SiC Power Semiconductor market size and forecast consistently center on the high growth potential, the primary application drivers, and the strategic importance of investment in this sector. Stakeholders are keen to understand which segments will experience the most substantial growth, the factors sustaining the impressive CAGR, and the implications for both established players and new entrants. Insights indicate that the market is on a robust upward trajectory, primarily fueled by the global push for electrification and energy efficiency across multiple industries. The forecast suggests a transformative period where these advanced materials will increasingly displace traditional silicon in high-power and high-frequency applications, establishing a new paradigm in power electronics.

A crucial takeaway is the pervasive influence of environmental regulations and sustainability initiatives, which are compelling industries to adopt more energy-efficient solutions, thereby directly benefiting the GaN and SiC market. Furthermore, the continuous reduction in manufacturing costs, coupled with performance improvements, is expanding the addressable market for these semiconductors beyond niche applications to mass-market adoption. The competitive landscape is intensifying, with significant investments in research and development aimed at improving device reliability and scaling production capabilities. This dynamic environment promises sustained growth and opportunities for innovation throughout the forecast period, positioning GaN and SiC as foundational technologies for future power systems.

- The market is poised for significant expansion, driven by widespread adoption in Electric Vehicles and renewable energy systems.

- Continuous technological advancements and cost reductions are accelerating the displacement of silicon-based power semiconductors.

- Asia Pacific is anticipated to maintain its dominant position, fueled by robust manufacturing capabilities and high demand from key industries.

- Strategic partnerships and mergers and acquisitions are shaping the competitive landscape, fostering innovation and market consolidation.

- The long-term outlook remains highly positive due to increasing global emphasis on energy efficiency and power density across diverse applications.

GaN and SiC Power Semiconductor Market Drivers Analysis

The GaN and SiC power semiconductor market is experiencing significant growth propelled by several robust drivers. A primary catalyst is the global imperative for enhanced energy efficiency, as industries and consumers increasingly seek solutions that minimize power loss and reduce operational costs. This demand is particularly pronounced in sectors such as electric vehicles, where efficient power conversion directly translates to extended range and faster charging times. The inherent superior performance characteristics of GaN and SiC, including higher breakdown voltage, faster switching speeds, and lower on-resistance compared to traditional silicon, make them ideal for achieving these efficiency gains across a broad spectrum of applications.

Furthermore, the rapid expansion of high-power and high-frequency applications, such as 5G telecommunications infrastructure, data centers, and renewable energy systems, is creating substantial demand for these advanced semiconductors. These applications require power solutions that can handle extreme conditions while maintaining compact form factors and high reliability. The unique properties of GaN and SiC enable system miniaturization, reduce cooling requirements, and improve overall system performance, making them indispensable for next-generation electronic devices and power systems. Continuous innovation in manufacturing processes and material science is also playing a crucial role in lowering production costs and improving device reliability, further accelerating their market penetration and solidifying their position as key enablers for future technological advancements.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Adoption of Electric Vehicles (EVs) | +1.8% | Global, particularly Europe, North America, China | Medium-term to Long-term (3-8 years) |

| Growing Demand for Energy-Efficient Power Supplies | +1.5% | Global | Short-term to Long-term (1-8 years) |

| Expansion of 5G Infrastructure and Data Centers | +1.2% | Asia Pacific (APAC), North America, Europe | Medium-term (3-5 years) |

| Increasing Investment in Renewable Energy Systems | +1.0% | Global, particularly Europe, China, India | Medium-term to Long-term (3-8 years) |

GaN and SiC Power Semiconductor Market Restraints Analysis

Despite the robust growth trajectory, the GaN and SiC power semiconductor market faces several significant restraints that could temper its expansion. A primary challenge is the relatively higher manufacturing cost associated with these wide bandgap materials compared to traditional silicon. The specialized production processes, including epitaxy and substrate growth, require significant capital investment and technical expertise, leading to higher per-unit costs for GaN and SiC devices. This cost disparity can act as a barrier to widespread adoption, especially in price-sensitive applications where the performance advantages may not fully justify the increased expense for end-users.

Another crucial restraint pertains to the supply chain volatility and the limited availability of high-quality raw materials, particularly SiC substrates. The production of large-diameter SiC wafers is technically challenging and requires specialized facilities, leading to a concentrated supply base and potential bottlenecks. Furthermore, the complexity involved in designing and integrating GaN and SiC devices into existing power systems, coupled with a relative lack of standardized design tools and experienced engineers, can slow down adoption rates. Overcoming these technical and economic hurdles will be critical for the market to realize its full potential and achieve mass-market penetration across all target industries.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of WBG Materials | -0.8% | Global | Short-term to Medium-term (1-5 years) |

| Supply Chain Volatility and Material Availability | -0.7% | Global, especially China, Japan | Short-term (1-3 years) |

| Design and Integration Complexity | -0.5% | Global, particularly developing markets | Medium-term (3-5 years) |

| Limited Expertise and Talent Pool | -0.3% | Global | Short-term to Medium-term (1-5 years) |

GaN and SiC Power Semiconductor Market Opportunities Analysis

The GaN and SiC power semiconductor market is ripe with substantial opportunities, driven by ongoing technological shifts and evolving industrial requirements. One of the most prominent avenues for growth lies in the burgeoning electric vehicle (EV) market. As global automotive manufacturers accelerate their transition to electric powertrains, the demand for highly efficient SiC-based inverters and on-board chargers is soaring. The ability of SiC to reduce system weight, improve power density, and extend vehicle range presents a compelling value proposition that continues to drive its adoption in this high-growth sector, creating significant revenue streams for semiconductor manufacturers.

Beyond automotive, significant opportunities exist in the expansion of advanced power supply units for data centers and cloud infrastructure, where energy efficiency and thermal management are paramount. GaN devices are particularly well-suited for these applications due to their high switching speeds and compact form factors, enabling smaller, more efficient power converters. Furthermore, the push towards smart grid initiatives and the increasing penetration of renewable energy sources, such as solar power and wind energy, create vast opportunities for both GaN and SiC inverters. The industrial sector, with its diverse needs for motor drives, robotics, and automation systems, also represents a fertile ground for market penetration. The continuous development of novel applications, coupled with advancements in packaging and integration technologies, will unlock new market segments and sustain long-term growth for these transformative power semiconductors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Mass-Market Consumer Electronics | +1.0% | Asia Pacific (APAC), North America | Short-term to Medium-term (1-5 years) |

| Growth in High-Power Industrial Applications | +0.8% | Europe, North America, Asia Pacific (APAC) | Medium-term to Long-term (3-8 years) |

| Emergence of Smart Grid and Energy Storage Systems | +0.7% | Global | Medium-term (3-5 years) |

| Development of New Aerospace and Defense Applications | +0.5% | North America, Europe | Long-term (5-8 years) |

GaN and SiC Power Semiconductor Market Challenges Impact Analysis

The GaN and SiC power semiconductor market, while promising, faces a set of inherent challenges that necessitate strategic navigation for sustained growth. One significant challenge is the ongoing need for continuous improvement in device reliability and lifetime. While significant strides have been made, some applications, particularly those in extreme environments like automotive or aerospace, demand even higher levels of robustness and longevity. Ensuring consistent performance and mitigating potential failure mechanisms under varying operational conditions remains a critical area of focus for manufacturers and researchers. Addressing these reliability concerns is paramount to gaining broader industry acceptance and solidifying market trust in these advanced materials.

Another key challenge involves the intellectual property (IP) landscape and potential litigation. As the market expands and competition intensifies, the protection and enforcement of proprietary technologies become increasingly complex. Companies must navigate a dense web of patents and ensure their innovations are adequately protected while avoiding infringement. Furthermore, the absence of universally standardized design tools and comprehensive industry guidelines for GaN and SiC integration can complicate adoption for new entrants and smaller firms. Overcoming these challenges will require collaborative efforts across the industry, including continued investment in R&D, strategic IP management, and the development of industry-wide standards and educational initiatives to foster a more mature and accessible ecosystem for wide bandgap semiconductors.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Long-term Device Reliability and Lifetime | -0.6% | Global | Short-term to Medium-term (1-5 years) |

| Managing Complex Intellectual Property (IP) Landscape | -0.4% | Global | Medium-term (3-5 years) |

| Thermal Management and Packaging Constraints | -0.3% | Global | Short-term to Medium-term (1-5 years) |

| Competition from Advanced Silicon-Based Solutions | -0.2% | Global | Short-term (1-3 years) |

GaN and SiC Power Semiconductor Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the global GaN and SiC Power Semiconductor market, offering an in-depth analysis of its current landscape, historical performance, and future projections. The report provides a granular understanding of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It incorporates detailed industry insights, competitive benchmarking, and strategic recommendations to assist stakeholders in making informed business decisions. The scope of the report is designed to provide a holistic view of the market, addressing critical factors influencing its evolution and identifying key areas of investment and innovation.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.1 Billion |

| Market Forecast in 2033 | USD 15.4 Billion |

| Growth Rate | 22.0% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, Wolfspeed Inc., STMicroelectronics N.V., Onsemi, Rohm Co., Ltd., NXP Semiconductors N.V., Mitsubishi Electric Corporation, Toshiba Corporation, Fuji Electric Co., Ltd., GaN Systems, Transphorm Technology, Inc., Navitas Semiconductor Corporation, GeneSiC Semiconductor Inc., UnitedSiC, Microchip Technology Inc., Renesas Electronics Corporation, Power Integrations, Inc., Littelfuse, Inc., Vishay Intertechnology, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The GaN and SiC power semiconductor market is extensively segmented to provide a granular view of its diverse landscape and to identify specific growth areas. This segmentation allows for a detailed analysis of market dynamics based on the type of material, the specific application areas, and the various end-use industries that leverage these advanced semiconductors. Each segment presents unique growth drivers, technological requirements, and competitive landscapes, contributing distinctively to the overall market expansion. Understanding these segmentations is crucial for stakeholders to pinpoint opportunities and develop targeted strategies that align with market demands and technological advancements across different verticals.

The segmentation by material type clearly distinguishes between Gallium Nitride (GaN) and Silicon Carbide (SiC), each with its unique advantages and suitability for different applications due to their distinct electrical properties. Application-based segmentation highlights how these semiconductors are integrated into a wide range of devices, from power supplies and inverters to electric vehicle components and telecommunications infrastructure, underscoring their versatility. Furthermore, the end-use industry segmentation provides insights into the major sectors driving demand, such as automotive, consumer electronics, and renewable energy, illustrating the broad impact and adoption of GaN and SiC technologies across the global economy. This multi-dimensional segmentation facilitates a comprehensive understanding of the market's structure and its future growth potential.

- By Type:

- Gallium Nitride (GaN)

- Silicon Carbide (SiC)

- By Application:

- Power Supplies

- Inverters

- Converters

- Electric Vehicles (EVs)

- Consumer Electronics

- Industrial Motors

- Renewable Energy Systems

- Data Centers

- Telecommunications Infrastructure

- Aerospace & Defense

- By End-Use Industry:

- Automotive

- Consumer Electronics

- Industrial

- Energy & Power

- Telecommunications

- Aerospace & Defense

- Medical

- Computing

Regional Highlights

The global GaN and SiC power semiconductor market exhibits diverse growth patterns across various geographical regions, each contributing uniquely to the overall market expansion. Asia Pacific (APAC) stands out as the dominant region, primarily driven by its robust manufacturing capabilities, significant investments in electric vehicles and 5G infrastructure, and a large consumer electronics market, particularly in countries like China, Japan, South Korea, and Taiwan. The region benefits from a strong presence of leading semiconductor foundries and increasing government support for advanced material research and development.

North America and Europe also represent key markets, characterized by high adoption rates in automotive electrification, renewable energy integration, and data center expansion. North America's growth is fueled by technological innovation and the presence of major electric vehicle manufacturers and cloud service providers. Europe is strongly positioned due to stringent energy efficiency regulations, a strong automotive industry embracing EVs, and significant investments in green energy initiatives. Latin America, the Middle East, and Africa (MEA) are emerging markets, showing gradual growth as their industrial and infrastructure development progresses, increasingly adopting advanced power solutions in areas such as renewable energy and industrial applications.

- Asia Pacific (APAC): Dominates the market due to its robust electronics manufacturing base, rapid EV adoption rates, and extensive investment in 5G infrastructure, particularly in China, Japan, and South Korea.

- North America: Exhibits significant growth driven by increasing demand from the automotive sector (EVs), advanced data center development, and continuous technological innovation in power electronics.

- Europe: A strong market propelled by stringent energy efficiency regulations, aggressive electric vehicle targets, and substantial investments in renewable energy and smart grid initiatives.

- Latin America: Emerging market with increasing adoption in renewable energy projects and industrial applications, though starting from a smaller base.

- Middle East and Africa (MEA): Growing slowly but steadily, primarily driven by infrastructure development projects and increasing focus on diversifying energy sources through solar power.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the GaN and SiC Power Semiconductor Market.- Infineon Technologies AG

- Wolfspeed Inc.

- STMicroelectronics N.V.

- Onsemi

- Rohm Co., Ltd.

- NXP Semiconductors N.V.

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Fuji Electric Co., Ltd.

- GaN Systems

- Transphorm Technology, Inc.

- Navitas Semiconductor Corporation

- GeneSiC Semiconductor Inc.

- UnitedSiC

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Power Integrations, Inc.

- Littelfuse, Inc.

- Vishay Intertechnology, Inc.

Frequently Asked Questions

What are GaN and SiC power semiconductors?

GaN (Gallium Nitride) and SiC (Silicon Carbide) are wide bandgap (WBG) semiconductor materials that offer superior performance over traditional silicon in high-power and high-frequency applications. They can operate at higher temperatures, switch faster, and have lower energy losses, enabling more compact and efficient power electronic systems.

Why are GaN and SiC considered superior to silicon in certain applications?

GaN and SiC have higher electron mobility, breakdown voltage, and thermal conductivity than silicon. This allows devices made from these materials to achieve higher power density, better energy efficiency, and smaller form factors, making them ideal for demanding applications like electric vehicles, fast chargers, and renewable energy systems.

What are the primary applications driving the GaN and SiC power semiconductor market?

The main applications driving this market include electric vehicles (EVs) for their power inverters and on-board chargers, consumer electronics (especially fast-charging adapters), 5G telecommunications infrastructure, data centers needing highly efficient power supplies, and renewable energy systems like solar inverters.

What is the projected growth rate for the GaN and SiC power semiconductor market?

The GaN and SiC Power Semiconductor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.0% between 2025 and 2033, driven by increasing demand for energy-efficient and high-performance power solutions across various industries.

What challenges does the GaN and SiC power semiconductor market face?

Key challenges include the relatively higher manufacturing costs compared to silicon, complexities in device design and integration, potential supply chain volatility for raw materials, and the ongoing need to ensure long-term device reliability and manage complex intellectual property landscapes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted