Semiconductor Test Equipment Market

Semiconductor Test Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703350 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

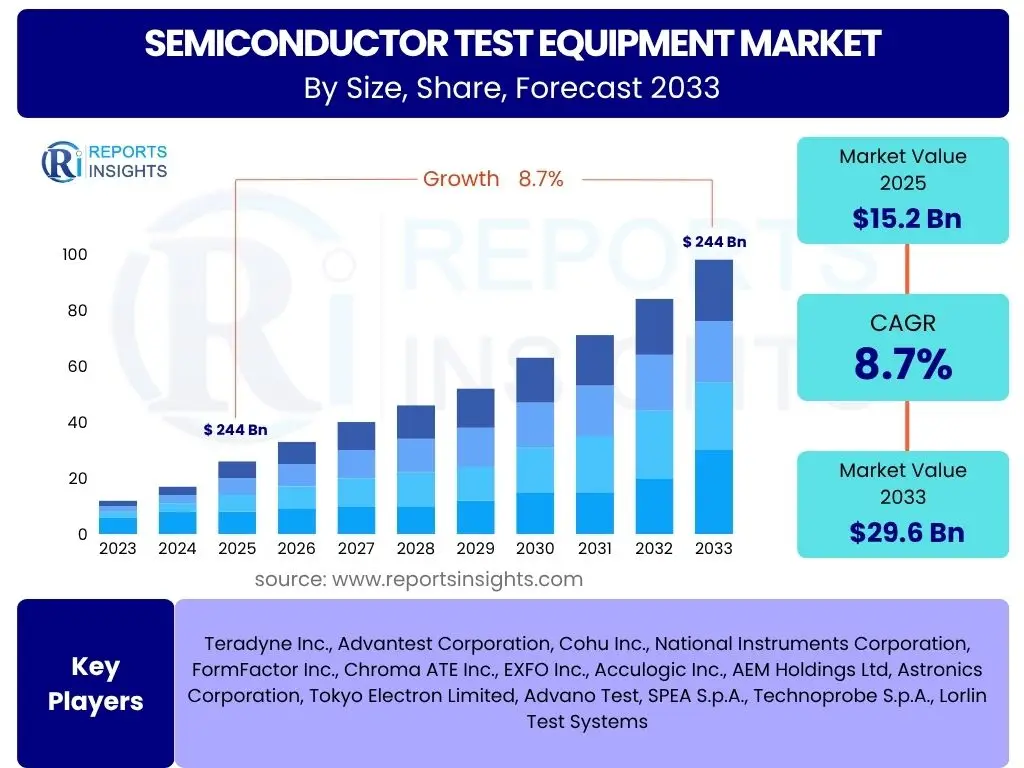

Semiconductor Test Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Test Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 29.6 Billion by the end of the forecast period in 2033.

Key Semiconductor Test Equipment Market Trends & Insights

User inquiries frequently highlight the rapid evolution of semiconductor technology and its direct impact on testing methodologies. A significant trend is the increasing complexity of chip designs, driven by advancements in Artificial Intelligence, 5G connectivity, and high-performance computing. This complexity necessitates more sophisticated and integrated test solutions capable of handling higher data rates, greater parallelism, and diverse functionalities within a single device. The industry is observing a shift towards parallel testing and multi-site testing to improve throughput and reduce costs, addressing the ever-growing demand for chips across various sectors.

Another prominent trend identified through user questions is the growing emphasis on silicon photonics and advanced packaging technologies like 3D ICs and chiplets. These innovations introduce new challenges for traditional testing, requiring novel optical testing capabilities and robust interconnect verification. Furthermore, the push for miniaturization and energy efficiency in electronic devices means that testing equipment must offer greater precision and sensitivity, capable of identifying subtle defects at microscopic levels. The integration of advanced analytics and machine learning into test processes is also gaining traction, enabling predictive maintenance, optimizing test flows, and improving overall yield management for semiconductor manufacturers.

- Escalating complexity of chip designs (e.g., AI/ML, 5G, HPC).

- Increased adoption of advanced packaging technologies (e.g., 3D ICs, chiplets).

- Growing demand for multi-site and parallel testing solutions.

- Emphasis on silicon photonics and integrated optical testing.

- Integration of data analytics and machine learning for test optimization.

- Focus on energy-efficient and highly precise testing.

AI Impact Analysis on Semiconductor Test Equipment

Common user questions regarding AI's influence on semiconductor test equipment center on its ability to enhance efficiency, reduce costs, and improve the accuracy of testing processes. Artificial intelligence is fundamentally transforming traditional testing paradigms by enabling smarter test pattern generation, optimizing test sequences, and performing advanced fault diagnosis. This leads to a significant reduction in test time and improved test coverage, which are crucial for managing the escalating cost of test and time-to-market pressures in the semiconductor industry. AI algorithms can analyze vast amounts of test data, identify correlations, and predict potential failures with greater precision than conventional methods, moving towards a more proactive and preventative testing approach.

Furthermore, AI facilitates predictive maintenance for test equipment itself, minimizing downtime and extending the lifespan of valuable assets. By analyzing operational data, AI can forecast component failures or performance degradation, allowing for timely interventions. The adoption of machine learning in anomaly detection helps in identifying subtle deviations from expected behavior during testing, which might indicate early signs of defects that human operators or traditional rule-based systems could miss. This enhanced diagnostic capability is particularly critical for high-reliability applications such as automotive and aerospace. While the initial investment in AI infrastructure can be substantial, the long-term benefits in terms of yield improvement, cost reduction, and faster product cycles are driving widespread adoption within the semiconductor test sector.

- Enhanced test pattern generation and optimization through machine learning.

- Improved fault diagnosis and root cause analysis.

- Reduced test time and increased throughput via AI-driven test sequence optimization.

- Predictive maintenance for semiconductor test equipment.

- Advanced anomaly detection for subtle defect identification.

- Potential for automated decision-making in test processes.

Key Takeaways Semiconductor Test Equipment Market Size & Forecast

Analysis of user inquiries concerning the semiconductor test equipment market size and forecast consistently reveals a strong interest in understanding the underlying drivers of growth and the long-term sustainability of the market. A key takeaway is the robust growth trajectory, primarily fueled by the insatiable global demand for semiconductors across diverse applications, including automotive, consumer electronics, data centers, and telecommunications. The market's resilience is further supported by the continuous technological advancements in chip design, which invariably demand more sophisticated and specialized test solutions. This creates a perpetual cycle of innovation and investment in testing infrastructure, ensuring consistent market expansion over the forecast period.

Another crucial insight is the increasing capital expenditure by chip manufacturers (IDMs, foundries, and OSATs) on advanced test equipment to maintain competitive edge and improve manufacturing yields. This investment is not only driven by volume but also by the complexity of advanced nodes and heterogeneous integration. The market forecast indicates a sustained upward trend, with significant opportunities emerging from new technologies like quantum computing, advanced sensing, and power electronics, each requiring unique testing paradigms. The integration of Industry 4.0 principles, including automation, IoT, and AI, within manufacturing and testing processes, further solidifies the market's growth outlook, ensuring that test equipment remains a critical enabler for the entire semiconductor ecosystem.

- Robust market growth driven by pervasive semiconductor demand.

- Continuous technological innovation in chip design necessitates advanced test solutions.

- Increased capital expenditure by semiconductor manufacturers on test infrastructure.

- Opportunities arising from emerging technologies (e.g., quantum computing, power electronics).

- Integration of Industry 4.0 technologies enhancing test efficiency.

- Strategic importance of test equipment for yield management and time-to-market.

Semiconductor Test Equipment Market Drivers Analysis

The semiconductor test equipment market is propelled by several robust drivers, primarily the escalating global demand for electronic devices across all sectors. This demand translates directly into increased semiconductor manufacturing, subsequently boosting the need for advanced testing solutions. The proliferation of next-generation technologies such as 5G, Artificial Intelligence (AI), the Internet of Things (IoT), and High-Performance Computing (HPC) mandates chips with higher performance, lower power consumption, and greater integration, each requiring rigorous and precise testing. The complexity of these new chip architectures and the shrinking geometries of transistors necessitate more sophisticated test equipment capable of validating intricate functionalities and ensuring reliability, thereby driving innovation and investment in this sector.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for advanced electronic devices (5G, AI, IoT, Automotive) | +2.5% | Global, particularly APAC (China, South Korea, Taiwan), North America | 2025-2033 (Long-term, Sustained) |

| Technological advancements and complexity of chip designs (e.g., FinFET, GAA, 3D ICs) | +2.0% | Global, particularly major semiconductor manufacturing hubs | 2025-2033 (Long-term, Progressive) |

| Rising capital expenditure by Foundries and OSATs | +1.8% | APAC (Taiwan, South Korea, China), North America | 2025-2030 (Mid-term, High) |

| Growing importance of yield management and quality control | +1.5% | Global | 2025-2033 (Ongoing) |

Semiconductor Test Equipment Market Restraints Analysis

Despite significant growth drivers, the semiconductor test equipment market faces several notable restraints. One primary challenge is the exceptionally high cost associated with developing and acquiring state-of-the-art test equipment. The increasing complexity of semiconductor devices translates directly into higher R&D expenses for test solution providers and significant capital expenditure for chip manufacturers, which can be a barrier for smaller players or in periods of economic uncertainty. The rapid obsolescence of technology also poses a restraint, as test equipment must be continually updated to keep pace with new chip generations, leading to shorter product lifecycles and accelerated depreciation for existing assets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High capital investment and R&D costs | -1.2% | Global | 2025-2033 (Ongoing) |

| Rapid technological obsolescence | -1.0% | Global | 2025-2033 (Ongoing) |

| Complexity in integrating new test methodologies | -0.8% | Global, particularly for smaller manufacturers | 2025-2030 (Mid-term) |

| Geopolitical tensions and trade barriers impacting supply chains | -0.7% | Global, particularly US-China, Europe | 2025-2028 (Short to Mid-term) |

Semiconductor Test Equipment Market Opportunities Analysis

The semiconductor test equipment market is ripe with numerous opportunities stemming from the evolving technological landscape and emerging application areas. A significant opportunity lies in the burgeoning market for advanced packaging technologies, such as 2.5D, 3D ICs, and chiplets. These innovative packaging methods require entirely new test approaches to verify interconnections and integrated functionalities, creating demand for specialized test equipment. The automotive industry's shift towards electric vehicles (EVs) and autonomous driving (AD) also presents a massive opportunity, as these applications demand extremely high reliability and safety standards, necessitating stringent and comprehensive testing throughout the chip lifecycle.

Furthermore, the increasing adoption of Artificial Intelligence (AI) and Machine Learning (ML) in test processes offers a transformative opportunity. AI/ML can optimize test flows, predict failures, and enhance data analysis, leading to significant improvements in efficiency and yield. The expansion of IoT devices and the widespread deployment of 5G infrastructure are continuously driving the need for new types of sensors, communication chips, and power management ICs, each requiring tailored test solutions. Miniaturization trends and the development of new materials in semiconductor manufacturing also create a demand for advanced metrology and inspection equipment, providing further avenues for market growth and innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in advanced packaging (2.5D/3D ICs, chiplets) | +1.5% | Global, especially APAC | 2025-2033 (Long-term) |

| Rising demand from automotive (EVs, ADAS) and industrial sectors | +1.3% | Europe, North America, APAC (China, Japan) | 2025-2033 (Long-term) |

| Integration of AI/ML for test optimization and predictive analytics | +1.0% | Global | 2025-2033 (Progressive) |

| Emergence of new technologies (e.g., quantum computing, silicon photonics) | +0.8% | North America, Europe, APAC (Japan) | 2028-2033 (Long-term, Emerging) |

Semiconductor Test Equipment Market Challenges Impact Analysis

The semiconductor test equipment market faces several significant challenges that can impede its growth and operational efficiency. One major challenge is the inherent complexity and increasing cost of testing advanced semiconductor devices. As chip designs become more intricate, incorporating billions of transistors and diverse functionalities, the development of comprehensive and efficient test programs becomes exceedingly difficult and resource-intensive. This complexity not only demands highly skilled engineers but also necessitates substantial investments in cutting-edge test methodologies and equipment, raising the barrier to entry and increasing operational expenses for manufacturers.

Furthermore, managing the rapid technological obsolescence of semiconductor devices poses a continuous challenge. Test equipment must constantly evolve to keep pace with new generations of chips, leading to shorter product cycles for test solutions and pressure on manufacturers to justify high capital expenditures for equipment that may quickly become outdated. Supply chain disruptions, often driven by geopolitical factors, raw material shortages, or global health crises, also present a significant challenge, impacting the timely delivery and cost-effectiveness of test equipment components. The increasing pressure for faster time-to-market for new electronic products further exacerbates these challenges, requiring test equipment providers to deliver innovative solutions under compressed development cycles while maintaining stringent quality and reliability standards.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing complexity and cost of testing advanced nodes | -1.5% | Global | 2025-2033 (Ongoing) |

| Short product lifecycles and rapid technological changes | -1.0% | Global | 2025-2033 (Ongoing) |

| Shortage of skilled workforce and talent in testing domain | -0.8% | Global, particularly developed regions | 2025-2030 (Mid-term) |

| Supply chain vulnerabilities and geopolitical uncertainties | -0.7% | Global | 2025-2028 (Short to Mid-term) |

Semiconductor Test Equipment Market - Updated Report Scope

This report provides an in-depth analysis of the Semiconductor Test Equipment Market, encompassing a thorough examination of market dynamics, key trends, drivers, restraints, opportunities, and challenges influencing its growth. It offers comprehensive market sizing and forecasts segmented by type, application, end-user, and region, providing a granular view of the industry landscape. The report also includes competitive intelligence, profiling major market players and assessing their strategic initiatives, product portfolios, and market positioning. Furthermore, it addresses the impact of emerging technologies, such as Artificial Intelligence and advanced packaging, on the testing ecosystem, offering actionable insights for stakeholders seeking to navigate the evolving market effectively.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 29.6 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Teradyne Inc., Advantest Corporation, Cohu Inc., National Instruments Corporation, FormFactor Inc., Chroma ATE Inc., EXFO Inc., Acculogic Inc., AEM Holdings Ltd, Astronics Corporation, Tokyo Electron Limited, Advano Test, SPEA S.p.A., Technoprobe S.p.A., Lorlin Test Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor test equipment market is meticulously segmented to provide a detailed understanding of its various facets and dynamics. This segmentation allows for a comprehensive analysis of demand drivers, technological preferences, and regional contributions across different product types, applications, and end-use industries. The market's diverse nature necessitates a granular breakdown to identify specific growth pockets and emerging areas of investment, aiding stakeholders in strategic decision-making and product development. Each segment plays a crucial role in shaping the overall market landscape, influenced by technological advancements, market demand, and competitive strategies.

- By Type:

- Wafer Probers: Equipment used for testing bare semiconductor wafers before dicing.

- Automated Test Equipment (ATE):

- Memory Test Systems: For testing various memory types (DRAM, NAND, SRAM).

- Mixed-Signal Test Systems: For testing devices with both analog and digital components.

- Digital Test Systems: Primarily for digital logic verification.

- RF Test Systems: For testing wireless communication components and modules.

- Analog Test Systems: For testing analog circuits and power management ICs.

- SOC Test Systems: For testing complex Systems-on-Chip that integrate multiple functionalities.

- Handlers: Robotic systems for automated loading, unloading, and sorting of devices during testing.

- Probes: Components that make electrical contact with the chip or wafer during testing.

- By Application:

- Foundry & Fabless: Testing services for integrated circuit manufacturing foundries and fabless semiconductor companies.

- IDM (Integrated Device Manufacturer): In-house testing for companies that design and manufacture their own chips.

- OSAT (Outsourced Semiconductor Assembly and Test): Testing services provided by third-party assembly and test providers.

- By End-use Industry:

- Consumer Electronics: Devices like smartphones, laptops, wearables, and home appliances.

- Automotive: Semiconductors for infotainment, ADAS, power management, and electric vehicles.

- Telecommunications: Components for 5G, networking equipment, and data centers.

- Industrial: Chips for industrial automation, robotics, and smart manufacturing.

- Medical: Semiconductors for medical imaging, diagnostics, and monitoring devices.

- Aerospace & Defense: High-reliability chips for avionics, radar, and communication systems.

- Others: Includes emerging applications like quantum computing and niche markets.

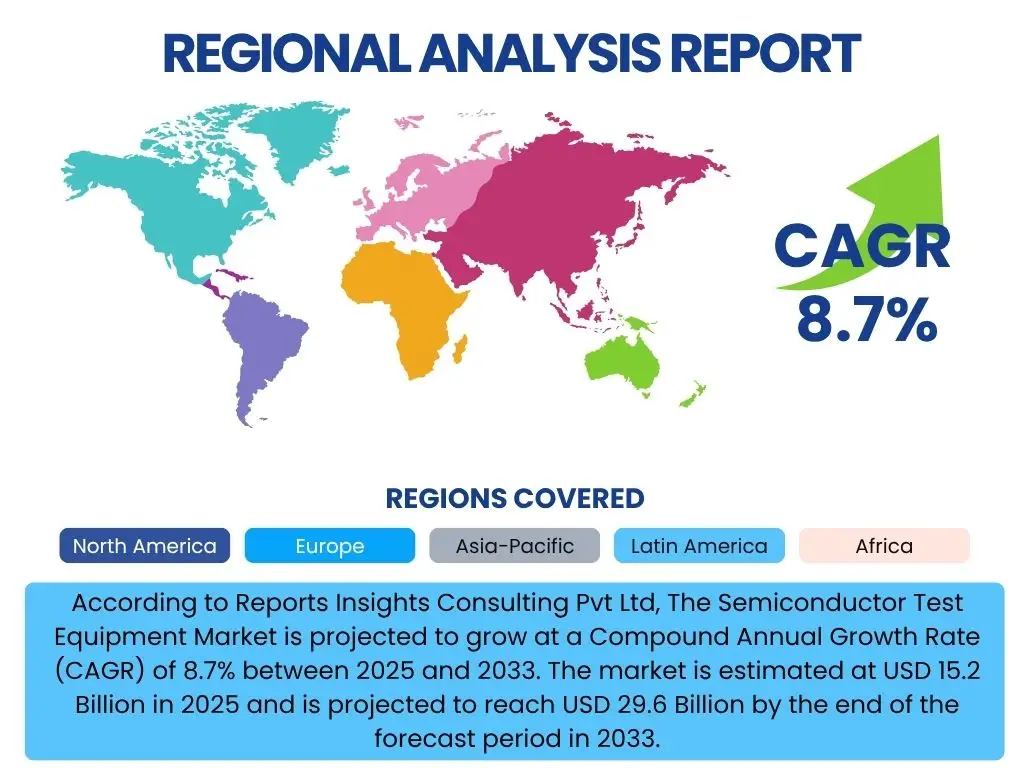

Regional Highlights

The Asia Pacific (APAC) region dominates the semiconductor test equipment market, driven by the presence of major semiconductor manufacturing hubs in countries like Taiwan, South Korea, China, and Japan. These countries host leading foundries, IDMs, and OSAT companies that are continually expanding their production capacities and investing in advanced testing infrastructure to meet global demand. Government initiatives supporting local semiconductor industries, coupled with a robust electronics manufacturing ecosystem, further propel the market in APAC. The region is at the forefront of adopting advanced packaging technologies and 5G deployment, which significantly boosts the demand for sophisticated test solutions.

North America and Europe represent mature markets with significant R&D capabilities and a strong focus on high-performance computing, automotive electronics, and specialized industrial applications. North America benefits from a strong base of fabless companies and leading-edge technology development, driving demand for advanced ATE. Europe is a key market for automotive semiconductors, power electronics, and industrial automation, leading to specialized testing requirements. Both regions are also active in developing AI chips and quantum computing, which are expected to create new avenues for test equipment innovation. Latin America and the Middle East & Africa (MEA) are emerging markets, showing gradual growth driven by increasing electronics consumption and developing local manufacturing capabilities, albeit at a slower pace compared to the established regions.

- Asia Pacific (APAC): Dominant market share due to large-scale semiconductor manufacturing, particularly in Taiwan, South Korea, China, and Japan. High investment in new fabs and advanced packaging.

- North America: Strong R&D, leadership in fabless design, and high-performance computing chips. Significant demand for advanced ATE and specialized test solutions.

- Europe: Key market for automotive semiconductors, power electronics, and industrial applications. Focus on high-reliability testing and innovation in emerging technologies.

- Latin America: Emerging market with growing electronics consumption and nascent manufacturing. Moderate growth expected.

- Middle East & Africa (MEA): Gradually increasing electronics demand and developing digital infrastructure. Limited but growing investment in semiconductor-related activities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Test Equipment Market.- Teradyne Inc.

- Advantest Corporation

- Cohu Inc.

- National Instruments Corporation

- FormFactor Inc.

- Chroma ATE Inc.

- EXFO Inc.

- Acculogic Inc.

- AEM Holdings Ltd

- Astronics Corporation

- Tokyo Electron Limited

- Advano Test

- SPEA S.p.A.

- Technoprobe S.p.A.

- Lorlin Test Systems

- NI (National Instruments)

- Keysight Technologies Inc.

- VIAVI Solutions Inc.

- Microtest S.p.A.

- Scorpion Technologies Ltd.

Frequently Asked Questions

What is Semiconductor Test Equipment?

Semiconductor test equipment refers to specialized machinery and systems used to verify the functionality, performance, and reliability of semiconductor devices, such as integrated circuits (ICs) and discrete components, throughout their manufacturing process, from wafer fabrication to final product assembly.

What are the primary drivers of the Semiconductor Test Equipment Market?

Key drivers include the surging global demand for electronic devices, the increasing complexity of chip designs (e.g., for AI, 5G, and HPC), continuous technological advancements in semiconductor manufacturing, and rising capital expenditure by chip foundries and Outsourced Semiconductor Assembly and Test (OSAT) companies.

How does AI impact the Semiconductor Test Equipment Market?

AI significantly impacts the market by enabling smarter test pattern generation, optimizing test sequences for efficiency, improving fault diagnosis and root cause analysis, facilitating predictive maintenance for equipment, and enhancing overall yield management through advanced data analytics.

What are the main challenges facing the Semiconductor Test Equipment Market?

Major challenges include the high cost of developing and acquiring advanced test equipment, rapid technological obsolescence of semiconductor devices, the increasing complexity of testing new chip architectures, and potential disruptions in the global supply chain for components and materials.

Which regions are key contributors to the Semiconductor Test Equipment Market?

The Asia Pacific (APAC) region is the largest contributor due to its extensive semiconductor manufacturing ecosystem. North America and Europe are significant mature markets driven by R&D and specialized applications, while Latin America and MEA are emerging regions with growing potential.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted