Semiconductor Dielectric Etching Equipment Market

Semiconductor Dielectric Etching Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703166 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Semiconductor Dielectric Etching Equipment Market Size

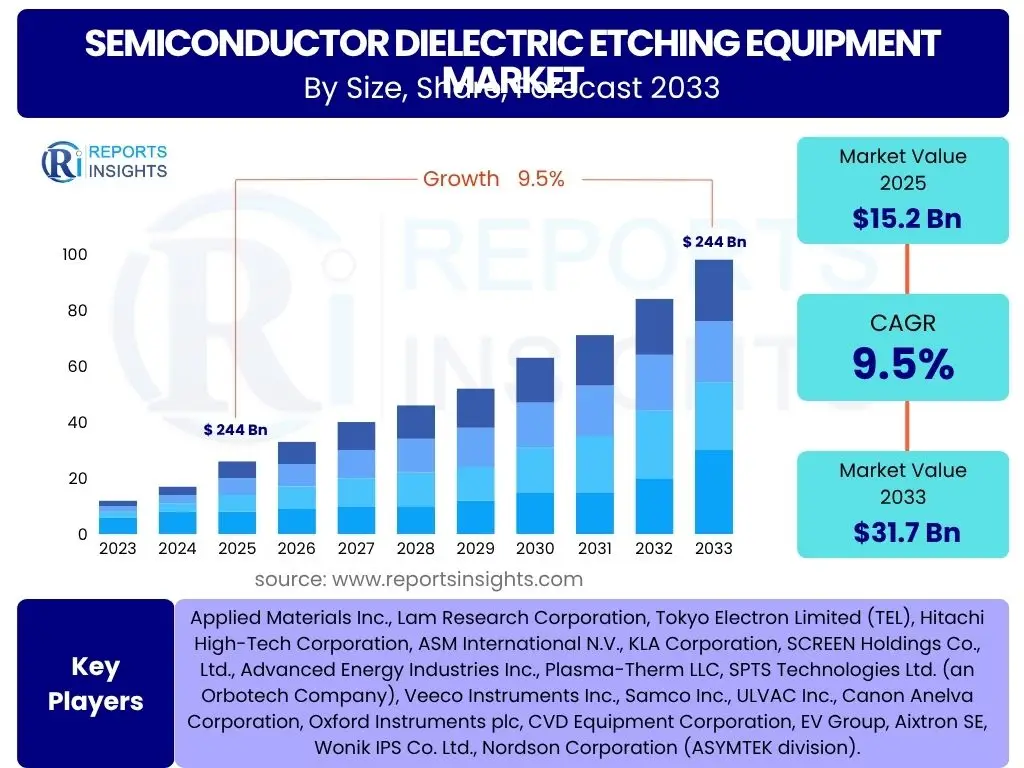

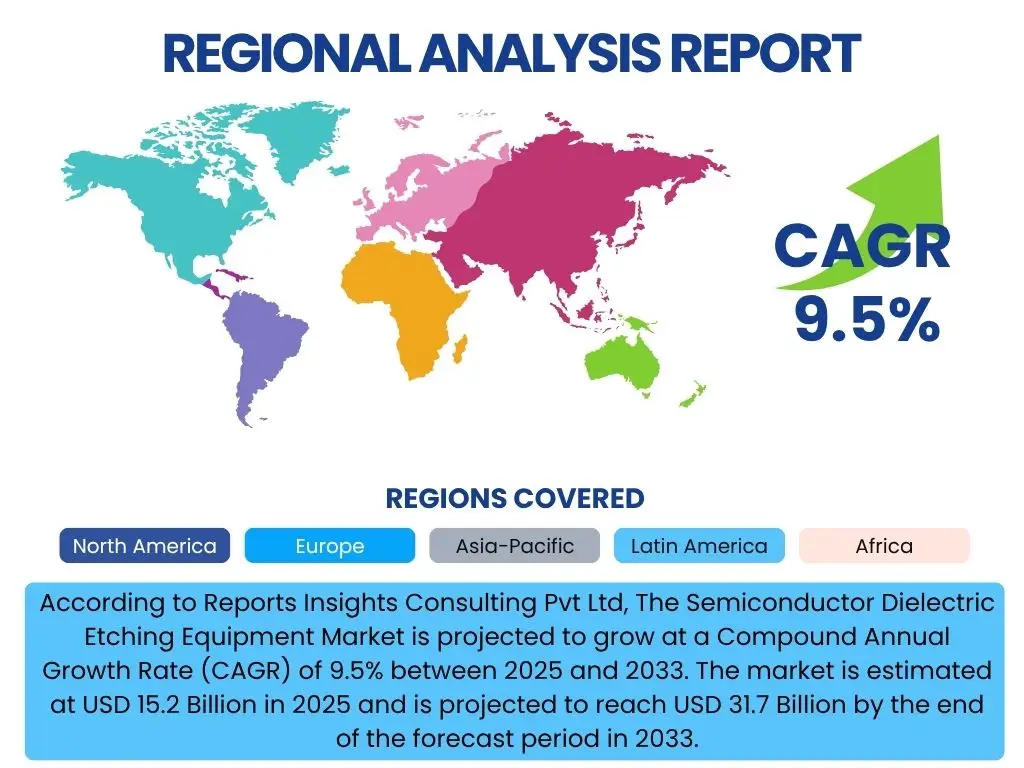

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Dielectric Etching Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 31.7 Billion by the end of the forecast period in 2033.

Key Semiconductor Dielectric Etching Equipment Market Trends & Insights

The semiconductor dielectric etching equipment market is currently undergoing significant transformation, driven by an escalating demand for advanced electronic devices and the continuous pursuit of miniaturization in chip manufacturing. A prominent trend involves the adoption of atomic layer etching (ALE) and plasma etching technologies, which offer superior precision and control over material removal at the nanoscale. These advancements are crucial for producing integrated circuits with increasingly smaller feature sizes and higher transistor densities, meeting the stringent requirements of next-generation applications.

Another key insight is the growing emphasis on advanced packaging solutions, such as 3D ICs and fan-out wafer-level packaging (FOWLP), which necessitate more complex and precise dielectric etching processes. This pushes equipment manufacturers to innovate in areas like anisotropic etching, high-aspect-ratio etching, and selective etching to handle diverse dielectric materials with high fidelity. Furthermore, sustainability considerations are influencing equipment design, with a focus on reducing energy consumption and minimizing the use of hazardous chemicals, aligning with global environmental regulations and corporate social responsibility initiatives.

The market also reflects a strategic shift towards integrated process solutions, where etching steps are seamlessly combined with deposition and cleaning processes to enhance overall manufacturing efficiency and yield. This integration reduces process variability and optimizes throughput, addressing the complex demands of advanced semiconductor fabrication. The rapid expansion of emerging technologies like artificial intelligence, 5G, and the Internet of Things is directly fueling the demand for high-performance chips, thereby accelerating the innovation cycle in dielectric etching equipment.

- Miniaturization and increasing transistor density in chip design

- Adoption of advanced etching techniques such as Atomic Layer Etching (ALE)

- Growth in advanced packaging technologies like 3D ICs and FOWLP

- Emphasis on high aspect ratio etching (HARC) for complex structures

- Integration of etching processes with deposition and cleaning for improved yield

- Increasing demand for semiconductor devices in AI, 5G, and IoT applications

- Focus on energy efficiency and sustainable manufacturing practices

AI Impact Analysis on Semiconductor Dielectric Etching Equipment

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is profoundly impacting the semiconductor dielectric etching equipment market by enhancing operational efficiency, process control, and predictive capabilities. Users frequently inquire about how AI can optimize etching parameters, reduce process variability, and improve overall wafer yield. AI algorithms can analyze vast datasets from manufacturing processes, identifying subtle correlations and anomalies that human operators might miss, leading to more precise adjustments and reduced material waste.

Common user concerns revolve around the implementation complexity, data security, and the need for specialized AI expertise within fabrication plants. However, the expectations are high for AI to enable smarter etching tools capable of real-time fault detection, predictive maintenance, and self-correction, thereby minimizing downtime and maximizing equipment utilization. AI-powered diagnostic systems are particularly sought after for their ability to anticipate equipment failures, schedule maintenance proactively, and maintain consistent process quality over extended periods.

Furthermore, AI is expected to accelerate the development of new etching recipes and processes for novel materials and complex chip architectures. By simulating and optimizing etching conditions virtually, AI can significantly reduce the need for costly and time-consuming physical experiments. This not only speeds up the research and development cycle but also ensures that new equipment designs are inherently more intelligent and adaptable to future technological shifts, addressing the industry's rapid innovation pace.

- Enhanced process control and optimization through real-time data analysis

- Predictive maintenance for reduced downtime and increased equipment lifespan

- Automated anomaly detection and self-correction capabilities in etching tools

- Accelerated development of new etching recipes and material processing techniques

- Improved yield management and reduction in wafer scrap rates

- Increased precision and uniformity in etching processes

- Optimization of energy consumption and operational costs

Key Takeaways Semiconductor Dielectric Etching Equipment Market Size & Forecast

The semiconductor dielectric etching equipment market is poised for robust growth, primarily driven by the relentless demand for higher performance, smaller, and more complex integrated circuits. The projected Compound Annual Growth Rate (CAGR) underscores a significant expansion over the forecast period, reflecting investments in advanced fabrication technologies and the global push for digital transformation. This growth is heavily influenced by the proliferation of AI, 5G, IoT, and automotive electronics, all of which require sophisticated semiconductor components.

A crucial takeaway is the increasing expenditure on research and development by equipment manufacturers to keep pace with the evolving technological landscape. Innovations in etching precision, selectivity, and throughput are essential for addressing the challenges of sub-10nm node fabrication and advanced packaging. Furthermore, the market's trajectory indicates a shift towards more sustainable and efficient etching solutions, driven by both regulatory pressures and corporate environmental initiatives, impacting equipment design and operational paradigms.

Geographically, the Asia Pacific region is expected to maintain its dominance due to the presence of major semiconductor foundries and increased government support for local manufacturing. However, North America and Europe are also witnessing significant investments in new fabs and R&D, positioning them as key contributors to market growth. The market's resilience is tied to the fundamental role of semiconductors in modern technology, ensuring sustained demand for advanced dielectric etching capabilities despite potential economic fluctuations.

- Significant market expansion driven by global semiconductor demand

- Technological advancements in etching precision are critical for future growth

- Asia Pacific region maintains strong market leadership

- Increased R&D investment by equipment manufacturers for next-gen technologies

- Growing importance of sustainable and energy-efficient etching solutions

- Direct correlation with the expansion of AI, 5G, IoT, and automotive sectors

- Emphasis on yield improvement and process control in fabrication

Semiconductor Dielectric Etching Equipment Market Drivers Analysis

The semiconductor dielectric etching equipment market is propelled by several robust drivers, primarily the escalating global demand for advanced electronic devices across diverse sectors. The continuous miniaturization of semiconductor components, driven by Moore's Law, necessitates increasingly precise and sophisticated etching equipment capable of handling intricate patterns at nanoscale dimensions. This pursuit of higher transistor density and improved performance per chip is a fundamental catalyst for innovation and investment in dielectric etching technologies.

Furthermore, the rapid expansion of emerging technologies such as Artificial Intelligence (AI), 5G connectivity, Internet of Things (IoT), and high-performance computing (HPC) significantly contributes to market growth. These applications demand higher volumes of complex, high-performance integrated circuits, which in turn require advanced dielectric etching processes for their fabrication. The automotive industry's increasing adoption of sophisticated electronics for autonomous driving and infotainment systems also acts as a strong driver, fueling demand for specialized and robust semiconductor components.

Investment in new fabrication plants (fabs) and the expansion of existing ones worldwide also provide a substantial impetus to the market. Governments and private entities are injecting considerable capital into semiconductor manufacturing infrastructure to enhance domestic production capabilities and reduce reliance on global supply chains. This surge in capital expenditure directly translates into increased procurement of advanced etching equipment, ensuring market buoyancy over the forecast period.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization of Semiconductor Devices | +2.5% | Global, particularly Asia Pacific (Taiwan, South Korea) | Short to Medium Term (2025-2029) |

| Increasing Demand for Advanced Electronics (AI, 5G, IoT) | +2.0% | Global, especially North America, Asia Pacific, Europe | Medium to Long Term (2026-2033) |

| Growth in Foundry and OSAT Investments | +1.8% | Asia Pacific (China, Taiwan), North America, Europe | Medium Term (2025-2030) |

| Technological Advancements in Material Science | +1.5% | Global | Long Term (2028-2033) |

Semiconductor Dielectric Etching Equipment Market Restraints Analysis

Despite robust growth drivers, the semiconductor dielectric etching equipment market faces several significant restraints that could impede its expansion. One primary restraint is the exceptionally high capital expenditure required for designing, manufacturing, and installing advanced etching equipment. The sophisticated nature of these machines, coupled with the need for ultra-precision and highly controlled environments, makes them incredibly expensive, creating a substantial barrier to entry for new players and potentially slowing down capacity expansion for existing ones, especially for smaller manufacturers.

Another significant challenge is the inherent complexity and rapid evolution of semiconductor manufacturing processes. Dielectric etching requires highly specialized technical expertise for operation, maintenance, and troubleshooting. The shortage of skilled professionals, including engineers and technicians with expertise in plasma physics, materials science, and advanced process control, can constrain market growth. This talent gap can lead to operational inefficiencies, slower adoption of new technologies, and increased operational costs for semiconductor manufacturers.

Furthermore, geopolitical tensions and trade disputes pose a considerable restraint, particularly impacting global supply chains for critical components and materials required for etching equipment. Export controls, tariffs, and restrictions on technology transfer can disrupt the flow of essential parts and intellectual property, leading to delays in equipment delivery, increased costs, and uncertainty for market participants. The highly cyclical nature of the semiconductor industry, characterized by periods of boom and bust, can also lead to unpredictable demand patterns, making long-term investment planning challenging for equipment manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Equipment | -1.5% | Global | Short to Medium Term (2025-2029) |

| Technological Complexity and Skilled Labor Shortage | -1.2% | Global, particularly developed economies | Medium to Long Term (2026-2033) |

| Geopolitical Tensions and Supply Chain Disruptions | -1.0% | Global, especially regions involved in trade disputes | Short to Medium Term (2025-2028) |

Semiconductor Dielectric Etching Equipment Market Opportunities Analysis

The semiconductor dielectric etching equipment market presents numerous growth opportunities driven by continuous technological advancements and expanding application areas. One significant opportunity lies in the development and commercialization of next-generation etching technologies, such as advanced plasma etching systems incorporating AI and machine learning for enhanced precision and process control. These innovations can address the evolving requirements of sub-3nm node fabrication and the complexities associated with novel materials like high-k dielectrics and 2D materials, opening new revenue streams for equipment manufacturers.

The increasing focus on advanced packaging solutions, including 3D-ICs, chiplets, and wafer-level packaging, offers another substantial opportunity. These packaging methods require highly specialized dielectric etching processes to create intricate interconnections and maintain signal integrity. Equipment providers capable of delivering solutions for Through-Silicon Vias (TSVs) and advanced redistribution layers (RDLs) will find significant demand. The trend towards heterogenous integration also drives the need for etching equipment that can handle different materials and device types on a single platform.

Furthermore, the emergence of new market segments like quantum computing, neuromorphic computing, and advanced photonics creates niche but high-value opportunities for specialized dielectric etching equipment. These nascent technologies often demand unique etching capabilities for fabricating their foundational components, pushing the boundaries of existing equipment performance. Investment in these areas could yield long-term benefits for companies that proactively develop tailored solutions. Additionally, the drive for enhanced energy efficiency and sustainable manufacturing practices within the semiconductor industry provides an opportunity for equipment manufacturers to innovate with greener etching chemistries and lower power consumption designs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Sub-3nm Node Fabrication | +1.8% | Global, particularly Asia Pacific | Medium to Long Term (2027-2033) |

| Growth in Advanced Packaging Technologies | +1.5% | Global | Medium Term (2025-2030) |

| Emergence of New Computing Paradigms (Quantum, Neuromorphic) | +1.0% | North America, Europe, select Asia Pacific regions | Long Term (2029-2033) |

| Demand for Energy-Efficient and Sustainable Etching Solutions | +0.8% | Global | Medium Term (2026-2031) |

Semiconductor Dielectric Etching Equipment Market Challenges Impact Analysis

The semiconductor dielectric etching equipment market faces several formidable challenges that necessitate continuous innovation and strategic adaptation from market participants. One significant challenge is the escalating cost of research and development required to keep pace with the rapid technological advancements in semiconductor manufacturing. As feature sizes shrink and new materials are introduced, developing etching equipment that can deliver the necessary precision, selectivity, and process control becomes increasingly complex and expensive, potentially straining profit margins and extending product development cycles.

Another major hurdle is the stringent requirement for process control and yield optimization. Dielectric etching is a critical step in semiconductor fabrication, and any deviations in the process can lead to significant yield losses, directly impacting manufacturers' profitability. Achieving uniform etching across large wafers, especially with increasing wafer sizes (e.g., 300mm to 450mm), and managing the variability of plasma conditions or chemical reactions present ongoing technical difficulties. Ensuring high throughput while maintaining superior quality remains a balancing act.

Furthermore, the market is subject to intense competition among a limited number of dominant players, leading to pressure on pricing and innovation. This competitive landscape, coupled with the cyclical nature of the semiconductor industry, introduces volatility in demand and revenue streams. Adapting to evolving customer needs, which include demands for faster cycle times, lower power consumption, and greater automation, while navigating intellectual property complexities and maintaining robust supply chains, poses continuous operational and strategic challenges for equipment manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High R&D Costs and Long Development Cycles | -1.3% | Global | Short to Medium Term (2025-2029) |

| Maintaining Process Control and Yield Optimization at Advanced Nodes | -1.1% | Global | Medium Term (2026-2031) |

| Intense Competition and Cyclical Industry Nature | -0.9% | Global | Short to Medium Term (2025-2028) |

Semiconductor Dielectric Etching Equipment Market - Updated Report Scope

This market research report offers a comprehensive analysis of the Semiconductor Dielectric Etching Equipment Market, encompassing historical data, current market dynamics, and future projections. It provides in-depth insights into market size, growth trends, key drivers, restraints, opportunities, and challenges influencing the industry landscape. The scope includes a detailed segmentation analysis, regional breakdowns, and profiles of leading market players, offering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 31.7 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials Inc., Lam Research Corporation, Tokyo Electron Limited (TEL), Hitachi High-Tech Corporation, ASM International N.V., KLA Corporation, SCREEN Holdings Co., Ltd., Advanced Energy Industries Inc., Plasma-Therm LLC, SPTS Technologies Ltd. (an Orbotech Company), Veeco Instruments Inc., Samco Inc., ULVAC Inc., Canon Anelva Corporation, Oxford Instruments plc, CVD Equipment Corporation, EV Group, Aixtron SE, Wonik IPS Co. Ltd., Nordson Corporation (ASYMTEK division). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Dielectric Etching Equipment Market is comprehensively segmented to provide granular insights into its various facets, enabling a detailed understanding of market dynamics and growth opportunities across different categories. This segmentation helps stakeholders identify specific growth areas, competitive landscapes, and technological advancements within each sub-segment. The market is primarily analyzed based on equipment type, application areas, wafer size, and end-user industries, reflecting the diverse requirements of semiconductor manufacturing.

The segmentation by equipment type distinguishes between various etching methodologies, such as plasma (dry) etching, wet etching, and the emerging atomic layer etching (ALE). Plasma etching, known for its precision and anisotropy, is further categorized by plasma source and gas chemistries. Wet etching, while offering high selectivity, is primarily used for bulk material removal. ALE represents a cutting-edge approach, providing ultimate control at the atomic level, crucial for future nodes. Each type caters to specific process requirements and material properties in chip fabrication.

Applications include broad categories like logic and memory etching, which represent the largest segments, alongside specialized areas such as power device etching, MEMS (Micro-Electro-Mechanical Systems) etching, and advanced packaging etching. These application-specific demands drive innovation in etching tool capabilities. Furthermore, segmentation by wafer size (e.g., 200mm, 300mm, and future 450mm) highlights the ongoing transition to larger wafer formats for increased productivity. End-user segmentation encompasses foundries, Integrated Device Manufacturers (IDMs), OSAT providers, and research institutions, each with distinct needs and procurement patterns for etching equipment.

- By Type:

- Plasma Etching Equipment (Dry Etching)

- Wet Etching Equipment

- Atomic Layer Etching (ALE) Equipment

- By Application:

- Logic & Memory Etching

- Power Device Etching

- MEMS Etching

- Advanced Packaging Etching

- By Wafer Size:

- 200mm

- 300mm

- Other (e.g., 450mm, Specialty Wafer Sizes)

- By End-User:

- Foundries

- Integrated Device Manufacturers (IDMs)

- OSAT (Outsourced Semiconductor Assembly and Test)

- Research & Development Institutes

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to the presence of major semiconductor manufacturing hubs in Taiwan, South Korea, China, and Japan. High investments in new fabs and advanced technology nodes drive significant demand. Strong government support and a robust electronics manufacturing ecosystem contribute to its leading position.

- North America: A significant market driven by technological innovation, substantial R&D investments, and the presence of leading semiconductor companies. Focus on advanced computing, AI, and defense applications fuels demand for high-performance chips, thereby boosting the etching equipment market.

- Europe: Exhibits steady growth, propelled by investments in automotive electronics, industrial IoT, and specialized semiconductor applications. Governments are promoting localized semiconductor production, leading to new fab initiatives and increased equipment procurement.

- Latin America: A developing market with nascent semiconductor manufacturing capabilities. Growth is primarily driven by increasing digitalization and consumer electronics demand, leading to gradual expansion in manufacturing infrastructure.

- Middle East and Africa (MEA): Currently a smaller market, but with emerging opportunities driven by diversification efforts into technology-intensive industries and increased adoption of digital infrastructure. Investments in data centers and communication technologies could spur future growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Dielectric Etching Equipment Market.- Applied Materials Inc.

- Lam Research Corporation

- Tokyo Electron Limited (TEL)

- Hitachi High-Tech Corporation

- ASM International N.V.

- KLA Corporation

- SCREEN Holdings Co., Ltd.

- Advanced Energy Industries Inc.

- Plasma-Therm LLC

- SPTS Technologies Ltd. (an Orbotech Company)

- Veeco Instruments Inc.

- Samco Inc.

- ULVAC Inc.

- Canon Anelva Corporation

- Oxford Instruments plc

- CVD Equipment Corporation

- EV Group

- Aixtron SE

- Wonik IPS Co. Ltd.

- Nordson Corporation (ASYMTEK division)

Frequently Asked Questions

Analyze common user questions about the Semiconductor Dielectric Etching Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is semiconductor dielectric etching equipment?

Semiconductor dielectric etching equipment is specialized machinery used in the fabrication of integrated circuits to precisely remove layers of dielectric (insulating) materials from a semiconductor wafer. This process creates patterns and structures essential for the functionality of transistors and interconnections on a chip.

How is AI impacting dielectric etching processes?

AI is transforming dielectric etching by enabling real-time process optimization, predictive maintenance of equipment, automated fault detection, and faster development of new etching recipes. It enhances precision, improves yield, and reduces operational costs by analyzing complex data patterns.

What are the primary drivers of the dielectric etching equipment market?

Key drivers include the continuous miniaturization of semiconductor devices, increasing global demand for advanced electronics (e.g., AI, 5G, IoT), significant investments in new fabrication plants (fabs), and the growth of advanced packaging technologies.

Which regions are leading the market for dielectric etching equipment?

The Asia Pacific region, particularly Taiwan, South Korea, China, and Japan, leads the market due to the concentration of major semiconductor foundries and extensive manufacturing investments. North America and Europe are also significant contributors with robust R&D and advanced manufacturing capabilities.

What are the main types of dielectric etching equipment?

The main types include plasma etching (dry etching) equipment, known for its precision and anisotropy; wet etching equipment, primarily used for bulk material removal; and Atomic Layer Etching (ALE) equipment, offering atomic-level control for highly critical applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted