Renewable Fuel Market

Renewable Fuel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701176 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Renewable Fuel Market Size

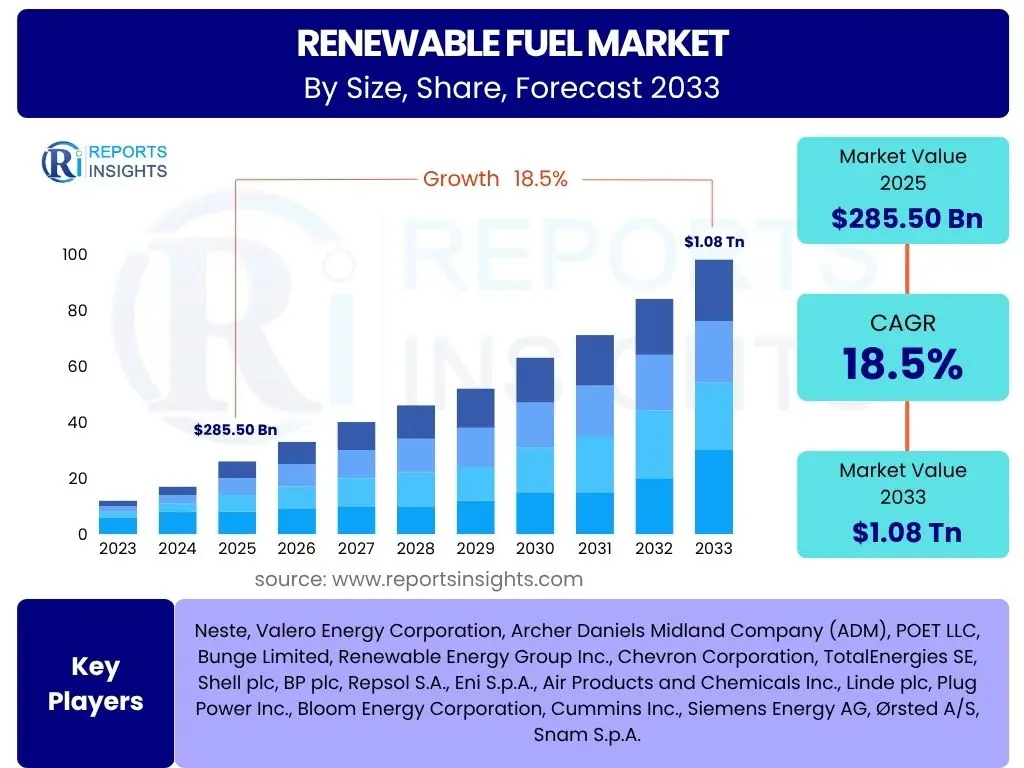

According to Reports Insights Consulting Pvt Ltd, The Renewable Fuel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. This substantial growth is indicative of a global shift towards sustainable energy solutions and a concerted effort to reduce carbon emissions across various sectors. The market's expansion is underpinned by increasing governmental support through mandates and incentives, coupled with advancements in production technologies that enhance efficiency and lower costs.

The market is estimated at USD 285.50 Billion in 2025 and is projected to reach USD 1.08 Trillion by the end of the forecast period in 2033. This significant valuation increase highlights the escalating investment and commercialization of diverse renewable fuel types, including advanced biofuels, green hydrogen, and sustainable aviation fuels. The trajectory signifies a maturing industry capable of delivering significant contributions to global energy needs while addressing environmental imperatives.

Key Renewable Fuel Market Trends & Insights

The renewable fuel market is undergoing a dynamic transformation, driven by a confluence of technological innovation, evolving regulatory frameworks, and increasing sustainability demands from consumers and industries. Key trends revolve around the diversification of feedstocks, the emergence of novel fuel types like green hydrogen and sustainable aviation fuels (SAF), and the integration of artificial intelligence for operational optimization. Stakeholders are particularly interested in how these trends will influence investment opportunities, supply chain resilience, and the overall pace of decarbonization across transport and industrial sectors.

Furthermore, there is a pronounced trend towards circular economy principles, with a focus on utilizing waste streams, agricultural residues, and non-food crops for biofuel production, thereby mitigating concerns related to land use and food security. The emphasis on developing advanced technologies for carbon capture and utilization in conjunction with renewable fuel production also represents a significant area of interest, promising to further enhance the environmental credentials of these energy sources. These developments collectively point towards a future where renewable fuels play an increasingly central role in the global energy mix, fostering energy independence and climate resilience.

- Diversification of Feedstocks: Expanding beyond traditional crops to include waste, algae, and cellulosic materials.

- Growth of Green Hydrogen: Increasing investment and development in hydrogen produced via electrolysis using renewable electricity.

- Sustainable Aviation Fuel (SAF) Adoption: Rising demand and production of fuels capable of significantly reducing aviation emissions.

- Integration with Carbon Capture: Pairing renewable fuel production with carbon capture, utilization, and storage technologies for enhanced climate benefits.

- Advanced Biofuel Technologies: Development of next-generation biofuels with higher energy density and lower environmental impact.

- Policy Support and Mandates: Strong governmental backing through incentives, blending mandates, and emission reduction targets.

AI Impact Analysis on Renewable Fuel

Artificial intelligence is poised to revolutionize the renewable fuel sector by optimizing various stages of the value chain, from feedstock sourcing and processing to distribution and end-use. Users frequently inquire about AI's role in enhancing production efficiency, predicting supply chain disruptions, and managing complex energy systems. AI algorithms can analyze vast datasets to identify optimal conditions for biofuel fermentation, hydrogen production, or biorefinery operations, thereby minimizing waste and maximizing yield. This predictive capability extends to forecasting feedstock availability and pricing, enabling more robust supply chain management and reducing operational risks.

Beyond production, AI's influence extends to critical infrastructure management and market dynamics. AI-powered systems can facilitate smarter grid integration for renewable electricity, ensuring a stable and efficient supply for green hydrogen production. Furthermore, AI contributes to predictive maintenance for renewable fuel production facilities, reducing downtime and operational costs. The application of machine learning in discovering novel catalysts and optimizing biochemical processes in research and development further accelerates innovation within the renewable fuel landscape, leading to more efficient and cost-effective solutions for sustainable energy generation.

- Enhanced Production Optimization: AI algorithms optimize biorefinery processes, fermentation, and hydrogen electrolysis for maximum yield and efficiency.

- Predictive Maintenance: AI identifies potential equipment failures in production facilities, reducing downtime and maintenance costs.

- Supply Chain Management: AI improves feedstock sourcing, logistics, and inventory management, ensuring stable supply.

- Research and Development Acceleration: AI speeds up the discovery of new catalysts and biological pathways for advanced fuel production.

- Resource Efficiency: AI monitors and manages energy and water consumption within production cycles, leading to more sustainable operations.

- Market Forecasting and Trading: AI models predict renewable fuel demand and pricing, aiding strategic decision-making and market participation.

Key Takeaways Renewable Fuel Market Size & Forecast

The overarching takeaway from the renewable fuel market size and forecast analysis is its undeniable trajectory of robust growth, fueled by global decarbonization imperatives and strong policy support. Users are keenly interested in understanding the magnitude of this growth, the primary drivers underpinning it, and the potential for long-term investment. The market's projected expansion to over a trillion dollars by 2033 underscores its critical role in the future energy landscape, presenting significant opportunities for innovation and economic development. The shift from nascent technologies to commercially viable solutions is a pivotal insight, indicating a maturing industry.

Furthermore, a key insight is the increasing diversity within the renewable fuel portfolio, moving beyond traditional biofuels to embrace green hydrogen, sustainable aviation fuels, and renewable natural gas. This diversification enhances market resilience and addresses a broader spectrum of energy demands across various sectors. The forecast also implicitly highlights the imperative for continued policy incentives, technological breakthroughs, and infrastructure development to sustain this growth momentum and overcome inherent challenges, ensuring renewable fuels contribute significantly to global climate goals.

- Significant Market Expansion: Projected to exceed USD 1 Trillion by 2033, driven by global energy transition.

- Policy-Driven Growth: Government mandates, incentives, and carbon pricing mechanisms are primary accelerators.

- Technological Advancements: Ongoing innovation in production processes and feedstock diversification enhances viability.

- Diversified Fuel Portfolio: Increasing prominence of green hydrogen and SAF alongside advanced biofuels.

- Decarbonization Imperative: Essential for achieving global net-zero emission targets across transportation and industrial sectors.

- Investment Hotbed: Presents substantial opportunities for R&D, infrastructure development, and commercial scaling.

Renewable Fuel Market Drivers Analysis

The renewable fuel market is propelled by a multitude of factors, each contributing significantly to its accelerated growth and widespread adoption. Foremost among these drivers is the escalating global concern over climate change and the urgent need to reduce greenhouse gas emissions. This environmental imperative has spurred governments worldwide to implement stringent regulations, carbon pricing mechanisms, and blending mandates, thereby creating a robust demand for cleaner energy alternatives in sectors traditionally reliant on fossil fuels, such as transportation and industrial processes. The alignment of corporate sustainability goals with national climate targets further amplifies this demand, as companies seek to reduce their carbon footprint and enhance their ESG credentials.

Technological advancements also play a crucial role, continuously improving the efficiency and cost-effectiveness of renewable fuel production. Innovations in feedstock conversion technologies, catalytic processes, and biorefinery designs are making a wider range of biomass and waste materials viable for fuel production, reducing reliance on food crops and addressing sustainability concerns. Additionally, the quest for enhanced energy security and reduced dependence on volatile fossil fuel markets drives investment in domestic renewable fuel production, particularly in regions keen on diversifying their energy portfolios. The falling costs of renewable electricity, essential for green hydrogen production, further bolsters the economic competitiveness of certain renewable fuel pathways.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Goals & Policies | +5.5% | Global, particularly EU, North America, China | Short to Long-term (2025-2033) |

| Technological Advancements & Cost Reductions | +4.8% | Global, particularly R&D hubs in North America, Europe, Japan | Medium to Long-term (2027-2033) |

| Increasing Energy Security Concerns | +3.2% | Europe, Asia Pacific, North America | Short to Medium-term (2025-2030) |

| Growing Corporate Sustainability Initiatives | +2.5% | Global, particularly Multinational Corporations | Medium to Long-term (2026-2033) |

| Rising Demand for Sustainable Aviation Fuel (SAF) | +2.0% | Global Aviation Industry, Major Hubs (EU, US) | Medium to Long-term (2027-2033) |

Renewable Fuel Market Restraints Analysis

Despite the robust growth prospects, the renewable fuel market faces several significant restraints that could temper its expansion if not adequately addressed. One primary challenge is the relatively high production cost of some advanced renewable fuels compared to conventional fossil fuels, particularly without substantial government subsidies or carbon pricing mechanisms. This cost disparity can hinder widespread adoption, especially in price-sensitive markets. Additionally, the existing infrastructure for transportation, storage, and distribution of renewable fuels, particularly for emerging types like green hydrogen, is often underdeveloped or requires substantial investment for conversion, creating a significant barrier to market penetration.

Another critical restraint pertains to feedstock availability and sustainability. While the industry is moving towards non-food feedstocks and waste materials, concerns persist regarding the scalability of these sources without impacting other vital sectors like agriculture or land use. The logistical complexities and costs associated with collecting, transporting, and processing diverse and often geographically dispersed feedstocks also pose operational challenges. Furthermore, regulatory uncertainty and inconsistency across different regions can create an unpredictable investment climate, deterring potential investors from committing to large-scale renewable fuel projects. These factors necessitate concerted efforts in policy harmonization, technological innovation, and infrastructure development to mitigate their impact on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs & Price Competitiveness | -3.0% | Global, particularly developing economies | Short to Medium-term (2025-2030) |

| Inadequate Infrastructure for Distribution | -2.5% | Global, particularly for Green Hydrogen & SAF | Short to Medium-term (2025-2030) |

| Feedstock Availability & Sustainability Concerns | -1.8% | Global, particularly regions with high agricultural land use | Medium to Long-term (2026-2033) |

| Regulatory Uncertainty & Policy Inconsistencies | -1.5% | Regional specific, e.g., US, Europe, Asia | Short to Medium-term (2025-2030) |

Renewable Fuel Market Opportunities Analysis

The renewable fuel market is brimming with opportunities driven by an accelerating global transition to low-carbon economies and technological breakthroughs. A significant opportunity lies in the burgeoning demand for sustainable aviation fuel (SAF) and marine biofuels, as these sectors face immense pressure to decarbonize but have limited alternative energy options. The development of specialized production pathways for these fuels, alongside supportive regulatory frameworks, presents a vast untapped market. Additionally, the circular economy model offers a compelling opportunity by leveraging diverse waste streams, including municipal solid waste, agricultural residues, and industrial by-products, as sustainable feedstocks for advanced biofuels and renewable natural gas, thereby addressing both energy needs and waste management challenges.

Another key opportunity is the rapid scale-up of green hydrogen production, fueled by declining renewable electricity costs and advancements in electrolysis technology. Green hydrogen is not only a clean fuel in itself but also a critical component for producing synthetic renewable fuels (e-fuels) and for decarbonizing hard-to-abate industrial sectors. Furthermore, advancements in biotechnology and synthetic biology are opening new avenues for developing novel fuel pathways and highly efficient microorganisms for biofuel production, promising even greater cost reductions and feedstock flexibility in the future. The increasing adoption of carbon capture and utilization (CCU) technologies in conjunction with bioenergy further amplifies the decarbonization potential, creating opportunities for negative emissions fuels.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Sustainable Aviation Fuel (SAF) & Marine Biofuels | +4.5% | Global Aviation & Shipping Hubs (North America, Europe, Asia) | Medium to Long-term (2026-2033) |

| Expansion of Green Hydrogen Production | +4.0% | Global, particularly regions with abundant renewable energy resources | Medium to Long-term (2027-2033) |

| Utilization of Diverse Waste Feedstocks | +3.0% | Global, particularly urban areas & agricultural regions | Short to Medium-term (2025-2030) |

| Advancements in Biotechnological Conversion Pathways | +2.5% | Global R&D Hubs, Biotech-focused regions | Medium to Long-term (2027-2033) |

Renewable Fuel Market Challenges Impact Analysis

The renewable fuel market, while promising, grapples with several formidable challenges that require concerted efforts for resolution. One significant hurdle is scaling up production to meet projected demand, which often necessitates substantial capital investment in new facilities and complex supply chains. This scalability challenge is particularly acute for emerging technologies like advanced biofuels and green hydrogen, where production processes are still maturing and require significant engineering and financial resources. Another persistent challenge is ensuring the long-term sustainability of feedstocks, particularly preventing competition with food crops or exacerbating deforestation, which can undermine the environmental credibility of renewable fuels and attract public scrutiny.

Furthermore, maintaining cost competitiveness with established fossil fuels, especially during periods of low oil prices, remains a critical challenge without stable policy support or carbon pricing mechanisms. The intermittency of renewable electricity sources, which is crucial for green hydrogen production, adds complexity to ensuring a consistent and cost-effective supply. Moreover, public perception and acceptance, often influenced by historical debates around land use or fuel performance, can pose barriers to wider adoption. Addressing these challenges will necessitate robust policy frameworks, continuous technological innovation, strategic infrastructure development, and effective stakeholder engagement to ensure the sustainable and widespread deployment of renewable fuels.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scaling Up Production & Capital Intensity | -2.8% | Global, particularly for new project development | Short to Medium-term (2025-2030) |

| Ensuring Feedstock Sustainability & Availability | -2.2% | Global, particularly in biomass-rich regions | Medium to Long-term (2026-2033) |

| Cost Competitiveness Against Fossil Fuels | -1.7% | Global, particularly in absence of strong carbon pricing | Short to Medium-term (2025-2030) |

| Infrastructure Development & Interoperability | -1.3% | Global, particularly for Hydrogen & SAF distribution | Medium to Long-term (2027-2033) |

Renewable Fuel Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Renewable Fuel Market, examining its current state, historical performance, and future growth trajectories. The scope encompasses detailed market sizing, segmentation by fuel type, feedstock, and application, alongside a thorough regional breakdown. It integrates insights on market dynamics, including drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. The report also highlights the impact of emerging technologies like Artificial Intelligence and the evolving regulatory landscape on market progression, offering a robust framework for understanding market potential and investment avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 285.50 Billion |

| Market Forecast in 2033 | USD 1.08 Trillion |

| Growth Rate | 18.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Neste, Valero Energy Corporation, Archer Daniels Midland Company (ADM), POET LLC, Bunge Limited, Renewable Energy Group Inc., Chevron Corporation, TotalEnergies SE, Shell plc, BP plc, Repsol S.A., Eni S.p.A., Air Products and Chemicals Inc., Linde plc, Plug Power Inc., Bloom Energy Corporation, Cummins Inc., Siemens Energy AG, Ørsted A/S, Snam S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The renewable fuel market is broadly segmented across several critical dimensions to provide a granular understanding of its diverse components and evolving dynamics. These segmentations by fuel type, feedstock, and application enable a detailed analysis of market growth drivers and opportunities within specific niches. The 'By Fuel Type' segmentation distinguishes between established biofuels like ethanol and biodiesel, and rapidly growing segments such as green hydrogen, renewable natural gas (RNG), and sustainable aviation fuel (SAF), each possessing unique production pathways, end-uses, and market trajectories.

The 'By Feedstock' segmentation highlights the shift from traditional food crops to more sustainable and abundant sources like waste materials, agricultural residues, and cellulosic biomass, which are crucial for minimizing land-use conflicts and enhancing the environmental profile of renewable fuels. Lastly, the 'By Application' segment delineates the primary end-use sectors, with transportation (road, aviation, marine) being a dominant consumer, followed by power generation, and industrial and residential heating, underscoring the versatility of renewable fuels in decarbonizing a wide array of economic activities. This multi-faceted segmentation allows for targeted strategic planning and investment decisions across the value chain.

- By Fuel Type:

- Biofuels (Ethanol, Biodiesel, Biojet Fuel, Biogas, Renewable Diesel (HVO))

- Green Hydrogen

- Renewable Natural Gas (RNG)

- Sustainable Aviation Fuel (SAF)

- Other Renewable Fuels (e.g., bio-methanol, cellulosic ethanol)

- By Feedstock:

- Corn

- Sugarcane

- Algae

- Waste (Municipal Solid Waste, Agricultural Residues, Industrial Waste)

- Animal Fats & Used Cooking Oil (UCO)

- Cellulosic Biomass

- Renewable Electricity (for Green Hydrogen production)

- Other Feedstocks

- By Application:

- Transportation (Road, Aviation, Marine, Rail)

- Power Generation

- Industrial Heating & Power

- Residential & Commercial Heating

- Other Applications (e.g., chemical production)

Regional Highlights

The global renewable fuel market exhibits significant regional variations in growth, policy support, and technological adoption. North America, particularly the United States, remains a dominant market, largely driven by established ethanol and biodiesel industries, robust federal and state-level renewable fuel standards, and increasing investments in sustainable aviation fuel (SAF) production. Canada also contributes with growing biofuel mandates and clean fuel regulations. Europe is a frontrunner in decarbonization efforts, with ambitious targets for renewable energy integration and strong support for advanced biofuels, green hydrogen, and renewable natural gas, notably in countries like Germany, France, and the Nordic nations, propelled by the Renewable Energy Directive (RED II).

Asia Pacific is emerging as a critical growth region, characterized by rapidly industrializing economies like China and India, which are heavily investing in renewable energy to address burgeoning energy demand and severe air pollution. China is making significant strides in green hydrogen production and electric vehicle adoption, while India is promoting ethanol blending programs. Japan and South Korea are focusing on hydrogen and e-fuels for their industrial sectors and transportation. Latin America, led by Brazil's long-standing leadership in sugarcane ethanol, continues to be a key player in biofuels, with other countries exploring their biomass potential. The Middle East and Africa are witnessing growing interest in green hydrogen projects, leveraging their abundant solar and wind resources for electrolysis, signaling nascent but high-potential markets for future renewable fuel development.

- North America: Dominant market with strong biofuel industries, increasing SAF mandates in the US, and growing clean fuel regulations in Canada.

- Europe: Leading in policy implementation (RED II), advanced biofuels, green hydrogen development (Germany, France, Netherlands), and renewable natural gas.

- Asia Pacific (APAC): Rapidly growing market driven by energy demand and decarbonization goals, with significant investments in green hydrogen (China, Japan, South Korea) and biofuels (China, India).

- Latin America: Strong biofuel production capabilities, particularly Brazil's sugarcane ethanol industry, and increasing focus on sustainable energy.

- Middle East and Africa (MEA): Emerging hub for green hydrogen production, leveraging abundant renewable energy resources (e.g., Saudi Arabia, UAE, South Africa).

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Renewable Fuel Market.- Neste

- Valero Energy Corporation

- Archer Daniels Midland Company (ADM)

- POET LLC

- Bunge Limited

- Renewable Energy Group Inc.

- Chevron Corporation

- TotalEnergies SE

- Shell plc

- BP plc

- Repsol S.A.

- Eni S.p.A.

- Air Products and Chemicals Inc.

- Linde plc

- Plug Power Inc.

- Bloom Energy Corporation

- Cummins Inc.

- Siemens Energy AG

- Ørsted A/S

- Snam S.p.A.

Frequently Asked Questions

What are renewable fuels?

Renewable fuels are energy sources derived from natural, replenishable resources that can be continuously regenerated, unlike fossil fuels. These fuels significantly reduce greenhouse gas emissions and environmental impact when compared to traditional petroleum-based fuels. They are integral to achieving global decarbonization targets and enhancing energy security across various sectors.

The category encompasses a diverse range of energy carriers, including biofuels produced from biomass (e.g., plants, algae, waste), green hydrogen generated through water electrolysis using renewable electricity, and renewable natural gas derived from organic waste. Their production pathways are designed to be sustainable, emphasizing circular economy principles and efficient resource utilization, making them a cornerstone of future sustainable energy systems.

What are the main types of renewable fuels?

The main types of renewable fuels broadly include biofuels, green hydrogen, and renewable natural gas (RNG). Biofuels, such as ethanol and biodiesel, are derived from organic matter like crops, agricultural waste, or animal fats. Biojet fuel and renewable diesel (HVO) are advanced biofuels used in aviation and heavy transport, respectively, offering significant emission reductions.

Green hydrogen is produced by splitting water using electricity generated from renewable sources like solar or wind power, resulting in zero carbon emissions at the point of production. Renewable natural gas, or biomethane, is captured from the anaerobic digestion of organic waste (e.g., landfills, wastewater treatment plants, agricultural waste) and can be used interchangeably with conventional natural gas. Sustainable Aviation Fuel (SAF) represents a rapidly growing subset, synthesized from various sustainable feedstocks for use in commercial aircraft.

How do renewable fuels contribute to sustainability?

Renewable fuels contribute significantly to sustainability by offering a lower-carbon alternative to fossil fuels, directly addressing climate change and air pollution. By utilizing renewable resources like biomass, waste, or sustainable electricity, they help reduce greenhouse gas emissions across their lifecycle, from production to combustion. This leads to improved air quality and a reduction in respiratory illnesses in urban areas.

Furthermore, many renewable fuel pathways promote circular economy principles by valorizing waste streams, turning discarded materials into valuable energy products. This reduces landfill burden and the need for new resource extraction. By diversifying the energy mix and reducing reliance on finite fossil fuel reserves, renewable fuels also enhance energy security and promote economic stability, fostering a more resilient and environmentally responsible global energy system.

What are the challenges for renewable fuels?

The renewable fuel sector faces several key challenges, including high production costs and achieving price competitiveness against established fossil fuels, especially without robust policy support. Scaling up production to meet increasing demand requires significant capital investment and complex technological advancements, which can be a barrier for new projects.

Another major challenge is ensuring the sustainable sourcing and adequate availability of feedstocks, preventing competition with food production or adverse land-use changes. Infrastructure limitations for storage, transportation, and distribution, particularly for emerging fuels like green hydrogen and SAF, also pose significant hurdles. Regulatory inconsistencies and uncertainty across different regions can further complicate investment decisions and market development, necessitating harmonized global policies.

What is the future outlook for renewable fuels?

The future outlook for renewable fuels is exceptionally positive, characterized by strong growth and increasing diversification. Driven by global decarbonization targets, escalating climate concerns, and supportive government policies, the market is poised for significant expansion, particularly in advanced biofuels, sustainable aviation fuels (SAF), and green hydrogen. Continuous technological innovation is expected to further reduce production costs and enhance efficiency, making renewable fuels increasingly competitive.

The focus will intensify on utilizing diverse, non-food feedstocks and waste streams to ensure sustainability and scalability. Strategic investments in infrastructure development, such as hydrogen pipelines and SAF distribution networks, will facilitate broader adoption. Renewable fuels are set to play an indispensable role in decarbonizing hard-to-abate sectors like aviation, shipping, and heavy industry, cementing their position as a cornerstone of the future clean energy economy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted