Stationary Fuel Cell Market

Stationary Fuel Cell Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703561 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Stationary Fuel Cell Market Size

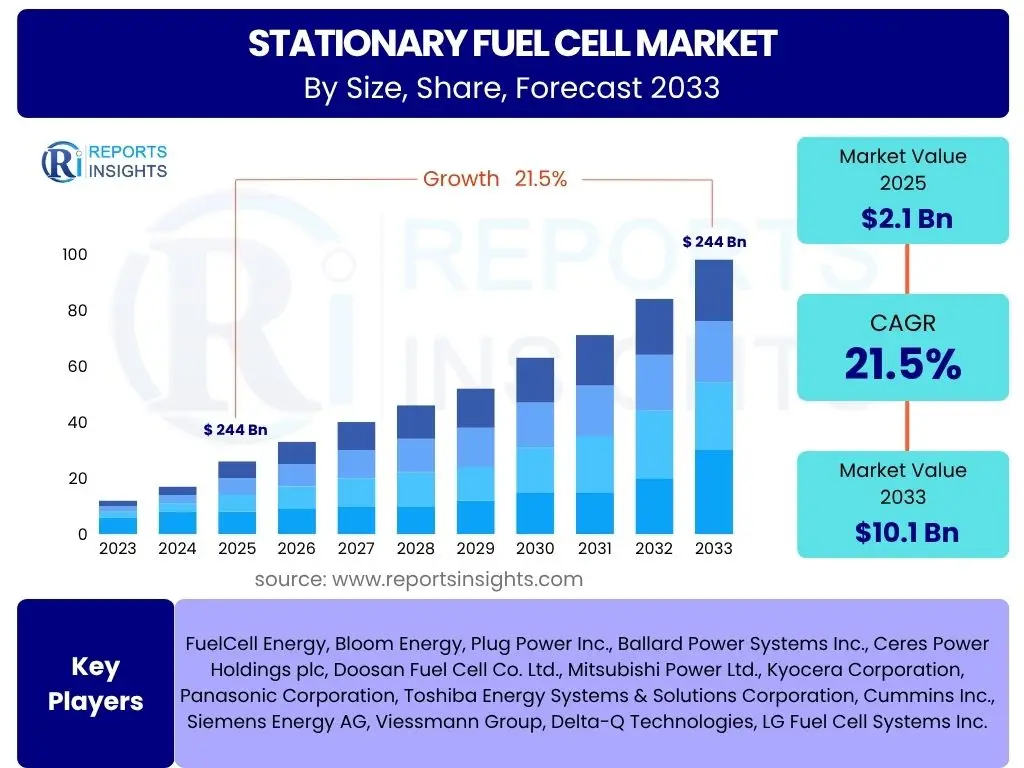

According to Reports Insights Consulting Pvt Ltd, The Stationary Fuel Cell Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 10.1 Billion by the end of the forecast period in 2033.

Key Stationary Fuel Cell Market Trends & Insights

The Stationary Fuel Cell market is witnessing significant transformative trends driven by increasing global focus on decarbonization and energy independence. Key developments include the rapid advancements in fuel cell technology leading to improved efficiency and durability, alongside a notable decrease in manufacturing costs. There is also a growing adoption of fuel cells in diverse applications, moving beyond traditional backup power to primary power generation for industrial, commercial, and residential sectors. Furthermore, the integration of fuel cells with renewable energy sources and smart grid technologies is emerging as a critical trend, enhancing grid stability and enabling more resilient energy systems.

Another prominent trend is the strong emphasis on hydrogen infrastructure development, which is crucial for the widespread deployment of hydrogen-based fuel cells. Governments globally are investing heavily in green hydrogen production and distribution networks, which directly supports the viability and expansion of the stationary fuel cell market. Additionally, the development of modular and scalable fuel cell systems allows for greater flexibility in deployment, catering to varying power needs from small-scale residential units to large-scale industrial applications. This modularity also facilitates easier installation and maintenance, further contributing to market growth.

- Technological advancements enhancing efficiency and lifespan.

- Decreasing manufacturing and operational costs.

- Integration with renewable energy and smart grid systems.

- Increased investment in hydrogen production and infrastructure.

- Growing adoption in critical infrastructure and data centers.

- Development of modular and scalable fuel cell solutions.

- Policy support and incentives for clean energy adoption.

- Focus on decentralized power generation for grid resilience.

AI Impact Analysis on Stationary Fuel Cell

Artificial Intelligence (AI) is set to revolutionize the Stationary Fuel Cell market by enhancing operational efficiency, predictive maintenance, and strategic decision-making. Users frequently inquire about AI's role in optimizing fuel cell performance, detecting anomalies before critical failures, and managing complex energy systems. AI algorithms can analyze vast datasets from fuel cell operations, including temperature, pressure, and power output, to identify patterns indicative of potential issues, thereby extending the lifespan of units and reducing downtime. This capability is crucial for ensuring the reliability and economic viability of fuel cell installations in mission-critical applications.

Moreover, AI is pivotal in optimizing energy management within systems that incorporate stationary fuel cells. It can forecast energy demand and supply fluctuations, manage hydrogen fuel consumption, and integrate fuel cells seamlessly with other distributed energy resources like solar and wind power. Users are keen to understand how AI can improve grid stability and reduce operational costs through intelligent load balancing and energy dispatch. AI also plays a role in the design and development phases, accelerating the discovery of new materials and refining fuel cell architectures through advanced simulation and machine learning techniques, addressing concerns about accelerating innovation and cost reduction.

- Predictive maintenance for increased uptime and longevity.

- Real-time performance optimization and fault detection.

- Enhanced energy management and grid integration.

- Optimized hydrogen supply and demand forecasting.

- Accelerated material discovery and fuel cell design.

- Improved manufacturing processes through AI-driven automation.

- Data analytics for operational insights and cost reduction.

Key Takeaways Stationary Fuel Cell Market Size & Forecast

The Stationary Fuel Cell market is poised for substantial growth over the next decade, driven by an accelerating global transition towards cleaner energy sources and the increasing demand for resilient and decentralized power solutions. Key takeaways from the market size and forecast analysis reveal a robust Compound Annual Growth Rate, indicating strong confidence in fuel cell technology as a viable alternative to conventional power generation. This growth is underpinned by continuous technological improvements, supportive government policies, and the urgent need for reliable energy infrastructure in various sectors, including data centers, telecom towers, and critical industrial facilities. Users frequently inquire about the primary factors fueling this expansion and the sectors that will experience the most significant adoption.

A significant insight is the market's trajectory towards becoming a cornerstone of sustainable energy grids, moving beyond niche applications to mainstream deployment. The forecast underscores the increasing economic competitiveness of stationary fuel cells as costs decline and efficiency improves, making them an attractive investment for both developed and emerging economies. Furthermore, the market's expansion is expected across all major regions, with specific growth hotspots influenced by local energy policies, availability of fuel infrastructure, and industrial demand for high-quality, uninterrupted power. The long-term outlook emphasizes the role of stationary fuel cells in achieving net-zero emissions targets and enhancing energy security.

- Significant CAGR indicates strong market expansion through 2033.

- Growing demand for clean, reliable, and decentralized power.

- Increasing adoption in critical infrastructure like data centers and healthcare.

- Technological advancements driving efficiency and cost-effectiveness.

- Supportive government policies and decarbonization mandates.

- Market shift towards widespread commercial and industrial applications.

Stationary Fuel Cell Market Drivers Analysis

The Stationary Fuel Cell market is primarily propelled by the global imperative to reduce carbon emissions and transition to sustainable energy sources. Increasing awareness regarding climate change and stringent environmental regulations are compelling industries and governments to invest in clean power generation technologies like fuel cells. This shift is also supported by the growing need for energy independence and grid resilience, especially in the face of aging infrastructure and increasing frequency of extreme weather events. Fuel cells offer a reliable, low-emission alternative for baseload and backup power, addressing these critical concerns.

Moreover, the continuous advancements in fuel cell technology, leading to improved efficiency, durability, and a reduction in manufacturing costs, significantly contribute to market expansion. As the cost per kilowatt-hour decreases, stationary fuel cells become more economically viable for a broader range of applications, including commercial, industrial, and residential sectors. Furthermore, government incentives, subsidies, and supportive policies promoting hydrogen economy development and renewable energy integration are creating a conducive environment for market growth, encouraging both research and development and commercial deployment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for clean energy solutions | +5.5% | Global | 2025-2033 |

| Increasing need for grid resilience and reliable power | +4.8% | North America, Europe, APAC | 2025-2033 |

| Supportive government policies and incentives | +4.2% | Europe, Japan, South Korea, US, China | 2025-2030 |

| Technological advancements and cost reduction | +4.0% | Global | 2028-2033 |

| Expansion of hydrogen infrastructure | +3.5% | Europe, Japan, South Korea, US | 2027-2033 |

| Rising adoption in data centers and telecom sectors | +3.0% | North America, Europe, APAC | 2025-2030 |

| Decentralized power generation trend | +2.5% | Global | 2025-2033 |

Stationary Fuel Cell Market Restraints Analysis

Despite significant growth potential, the Stationary Fuel Cell market faces several notable restraints that could temper its expansion. One of the primary barriers is the high initial capital cost associated with fuel cell systems, particularly compared to traditional power generation technologies. While operational costs are often lower, the upfront investment can be prohibitive for many potential adopters, especially smaller businesses or residential users. This cost factor necessitates long payback periods, making it less attractive without substantial subsidies or economic incentives.

Another significant restraint is the underdeveloped hydrogen infrastructure in many regions. The widespread adoption of hydrogen fuel cells relies heavily on the availability of readily accessible and affordable hydrogen supply. Currently, the production, storage, and distribution of hydrogen are still in nascent stages in numerous areas, leading to logistical challenges and higher fuel costs. Additionally, public perception concerns regarding hydrogen safety, though largely unfounded with modern technology, can also act as a psychological barrier to adoption. Competition from other established or rapidly developing renewable energy technologies, such as solar PV and battery storage, also presents a challenge, as these alternatives often have lower initial investment costs and more mature infrastructure.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment | -3.0% | Global | 2025-2028 |

| Lack of mature hydrogen infrastructure | -2.5% | Most Regions (excluding select few) | 2025-2029 |

| Competition from alternative energy sources | -2.0% | Global | 2025-2033 |

| Public perception and safety concerns | -1.5% | Certain Developing Markets | 2025-2027 |

| Complexity of system integration | -1.0% | New Adopters | 2025-2026 |

Stationary Fuel Cell Market Opportunities Analysis

The Stationary Fuel Cell market is presented with significant opportunities driven by evolving global energy landscapes and technological advancements. The increasing global push for decarbonization and the urgent need for reliable, off-grid power solutions in remote areas or during grid outages represent major growth avenues. Fuel cells offer a compelling solution for providing continuous, clean power to critical infrastructure such as data centers, hospitals, and telecommunication networks, where power continuity is paramount. The expansion of smart cities and the demand for distributed power generation further amplify these opportunities.

Furthermore, the rapid advancements in hydrogen production technologies, particularly green hydrogen derived from renewable sources, are creating a more sustainable and economically viable fuel supply for stationary fuel cells. This, coupled with the development of more efficient and durable fuel cell stacks, enhances the overall attractiveness of the technology. Emerging applications in niche industrial sectors requiring specific power characteristics, and the potential for fuel cells to act as balancing assets within renewable-heavy grids, also represent promising market opportunities. Collaboration between technology developers, energy providers, and policymakers is key to unlocking these potentials and accelerating market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for backup and primary power in critical infrastructure | +4.5% | North America, Europe, APAC | 2025-2033 |

| Advancements in green hydrogen production technologies | +4.0% | Europe, Japan, US, China | 2027-2033 |

| Expansion into new industrial and commercial applications | +3.5% | Global | 2026-2033 |

| Integration with renewable energy sources and microgrids | +3.0% | Global | 2025-2033 |

| Government focus on energy independence and security | +2.8% | Europe, Asia Pacific | 2025-2030 |

| Market potential in remote and off-grid locations | +2.2% | Africa, Latin America, South East Asia | 2025-2033 |

Stationary Fuel Cell Market Challenges Impact Analysis

The Stationary Fuel Cell market faces several significant challenges that could impede its growth trajectory. One of the primary challenges is achieving widespread cost competitiveness with conventional power sources and other established renewable technologies. While costs are declining, they have not yet reached parity in all applications without financial incentives. This makes it challenging to scale up adoption, especially in markets where electricity prices are low or where incumbent technologies are deeply entrenched. Overcoming this cost barrier requires further technological innovation, economies of scale in manufacturing, and sustained policy support.

Another major challenge revolves around the development and standardization of hydrogen supply chains. The current lack of a comprehensive and robust hydrogen infrastructure, from production to distribution and storage, creates significant logistical hurdles and drives up the cost of fuel for stationary fuel cells. Ensuring a reliable and affordable supply of hydrogen, particularly green hydrogen, is critical for the long-term viability and broad deployment of these systems. Additionally, the complexity of integrating fuel cell systems with existing grid infrastructure and managing regulatory frameworks across diverse regions poses considerable technical and administrative challenges, requiring substantial collaboration among stakeholders and clear, consistent policy direction.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving cost competitiveness at scale | -3.5% | Global | 2025-2029 |

| Establishing comprehensive hydrogen infrastructure | -3.0% | Global (excluding specific hubs) | 2025-2030 |

| Regulatory complexity and standardization issues | -2.5% | Diverse Regions | 2025-2028 |

| Supply chain vulnerabilities for key components | -2.0% | Global | 2025-2027 |

| Limited public awareness and education | -1.5% | Emerging Markets | 2025-2027 |

| Securing long-term stable funding for R&D and deployment | -1.0% | Global | 2025-2033 |

Stationary Fuel Cell Market - Updated Report Scope

This market insights report on Stationary Fuel Cells provides a comprehensive analysis of the current market landscape, growth drivers, restraints, opportunities, and challenges. It delves into segment-wise performance and regional dynamics, offering a forward-looking perspective on market evolution and strategic recommendations for stakeholders. The report aims to equip industry participants with actionable intelligence to navigate the complexities of the market and capitalize on emerging trends.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 10.1 Billion |

| Growth Rate | 21.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | FuelCell Energy, Bloom Energy, Plug Power Inc., Ballard Power Systems Inc., Ceres Power Holdings plc, Doosan Fuel Cell Co. Ltd., Mitsubishi Power Ltd., Kyocera Corporation, Panasonic Corporation, Toshiba Energy Systems & Solutions Corporation, Cummins Inc., Siemens Energy AG, Viessmann Group, Delta-Q Technologies, LG Fuel Cell Systems Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Stationary Fuel Cell market is comprehensively segmented by fuel cell type, application, and end-use, reflecting the diverse technological landscape and varied power generation needs across industries. This granular segmentation provides a detailed understanding of market dynamics, growth pockets, and key areas of investment. Each segment demonstrates unique characteristics concerning technological maturity, cost efficiency, and suitability for specific power requirements, driving differentiated adoption patterns globally.

By analyzing these segments, stakeholders can identify the most promising areas for product development and market penetration. For instance, Solid Oxide Fuel Cells (SOFCs) are gaining traction for their high efficiency in large-scale power generation and Combined Heat and Power (CHP) applications, while Polymer Electrolyte Membrane Fuel Cells (PEMFCs) are preferred for smaller, distributed power systems due to their quick startup and compact size. The end-use segmentation highlights critical sectors such as data centers and telecommunications, where reliable backup power is paramount, driving significant demand for fuel cell solutions. Understanding these specific segment contributions is vital for strategic planning and resource allocation within the market.

- By Type: Polymer Electrolyte Membrane Fuel Cell (PEMFC), Phosphoric Acid Fuel Cell (PAFC), Solid Oxide Fuel Cell (SOFC), Molten Carbonate Fuel Cell (MCFC), Others

- By Application: Combined Heat and Power (CHP), Primary Power, Backup Power

- By End-Use: Commercial, Industrial, Residential, Data Centers, Telecom Towers, Utilities, Healthcare Facilities, Military & Defense, Others

Regional Highlights

- North America: Expected to maintain a significant market share due to increasing investments in renewable energy, stringent emission regulations, and the growing demand for reliable backup power in critical infrastructure, particularly data centers and healthcare facilities. Government initiatives and incentives for clean energy adoption further bolster market growth.

- Europe: Driven by ambitious decarbonization targets set by the European Green Deal and significant investments in hydrogen strategies. Countries like Germany, France, and the UK are actively promoting the deployment of stationary fuel cells for decentralized power generation and grid stability, aiming for energy independence.

- Asia Pacific (APAC): Projected to be the fastest-growing region, owing to rapid industrialization, increasing energy demand, and governmental support for fuel cell technology in countries such as Japan, South Korea, and China. These nations are heavily investing in hydrogen production and fuel cell deployment across various sectors, including residential and commercial applications.

- Latin America: Showing nascent growth, primarily driven by the need for reliable power solutions in remote areas and increasing interest in sustainable energy alternatives. However, infrastructure development and investment remain key challenges that need to be addressed for accelerated adoption.

- Middle East and Africa (MEA): Witnessing gradual adoption, particularly in areas with underdeveloped grid infrastructure and a strong focus on diversifying energy sources away from fossil fuels. Opportunities exist in remote power generation for oil & gas operations, telecommunications, and off-grid communities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Stationary Fuel Cell Market.- FuelCell Energy

- Bloom Energy

- Plug Power Inc.

- Ballard Power Systems Inc.

- Ceres Power Holdings plc

- Doosan Fuel Cell Co. Ltd.

- Mitsubishi Power Ltd.

- Kyocera Corporation

- Panasonic Corporation

- Toshiba Energy Systems & Solutions Corporation

- Cummins Inc.

- Siemens Energy AG

- Viessmann Group

- Delta-Q Technologies

- LG Fuel Cell Systems Inc.

- Nedstack Fuel Cell Technology BV

- WATT Fuel Cell Corporation

- Intelligent Energy Limited

- Horizon Fuel Cell Technologies

- GenCell Ltd.

Frequently Asked Questions

Analyze common user questions about the Stationary Fuel Cell market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current market size and projected growth of Stationary Fuel Cells?

The Stationary Fuel Cell market is estimated at USD 2.1 Billion in 2025 and is projected to reach USD 10.1 Billion by 2033, growing at a CAGR of 21.5% during the forecast period.

What are the primary applications of Stationary Fuel Cells?

Stationary Fuel Cells are primarily used for Combined Heat and Power (CHP), primary power generation, and backup power in critical infrastructure like data centers, telecom towers, commercial buildings, and residential units.

What are the main drivers for the Stationary Fuel Cell market growth?

Key drivers include increasing demand for clean energy, supportive government policies and incentives, technological advancements reducing costs, and the growing need for resilient and decentralized power solutions.

What challenges does the Stationary Fuel Cell market face?

Major challenges include high initial capital costs, the nascent stage of hydrogen infrastructure development, intense competition from other energy sources, and regulatory complexities in various regions.

Which regions are leading in Stationary Fuel Cell adoption?

North America and Europe currently hold significant market shares due to strong environmental policies and infrastructure needs. Asia Pacific is projected to be the fastest-growing region, driven by governmental support and industrial expansion in countries like Japan, South Korea, and China.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted