Fuel Cell Electric Vehicle Market

Fuel Cell Electric Vehicle Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702883 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Fuel Cell Electric Vehicle Market Size

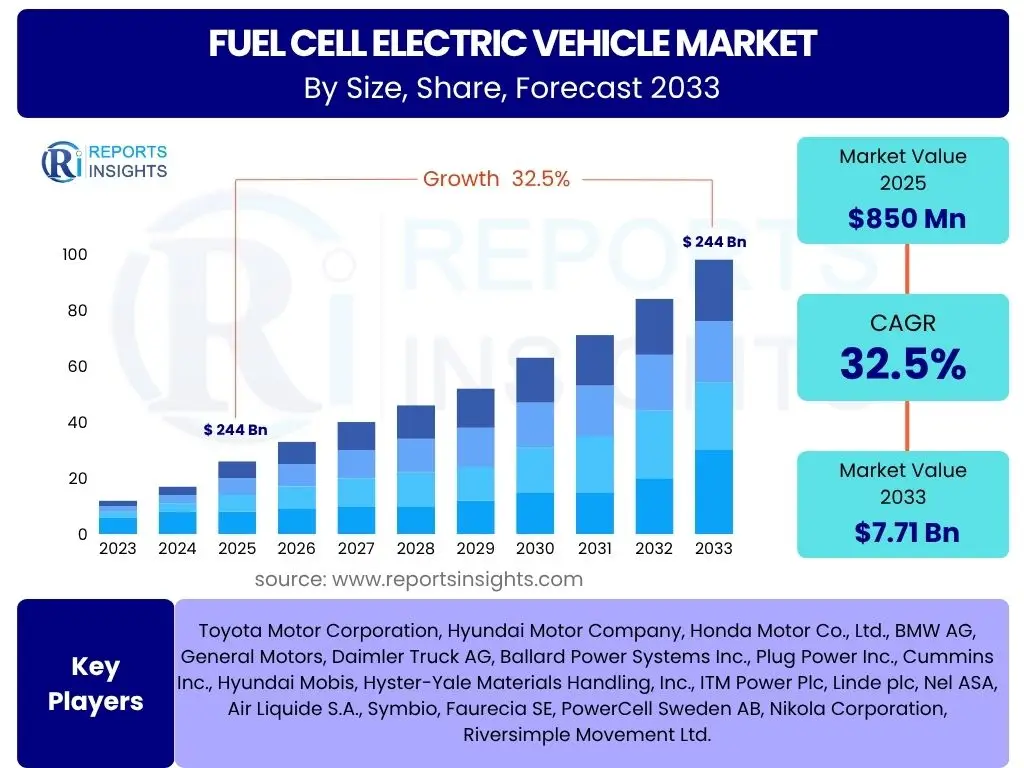

According to Reports Insights Consulting Pvt Ltd, The Fuel Cell Electric Vehicle Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 32.5% between 2025 and 2033. The market is estimated at USD 850 million in 2025 and is projected to reach USD 7.71 billion by the end of the forecast period in 2033.

Key Fuel Cell Electric Vehicle Market Trends & Insights

Market trends in the Fuel Cell Electric Vehicle (FCEV) sector indicate a significant shift towards sustainable transportation solutions driven by growing environmental concerns and supportive government initiatives. Users frequently inquire about the progression of hydrogen infrastructure, the comparative advantages of FCEVs over battery electric vehicles (BEVs), and the technological advancements making FCEVs more viable. Key insights highlight the increasing investments in hydrogen production and distribution, the expansion of FCEV models beyond passenger cars into heavy-duty commercial vehicles, and continuous improvements in fuel cell efficiency and durability, positioning FCEVs as a crucial part of the future mobility landscape.

The market is witnessing a diversification in FCEV applications, moving beyond initial passenger car deployments to include buses, trucks, trains, and even marine vessels. This expansion is supported by collaborative efforts between automotive manufacturers, energy companies, and governments to build out a comprehensive hydrogen ecosystem. Furthermore, technological breakthroughs in fuel cell stack design, hydrogen storage solutions, and overall system integration are addressing previous limitations, making FCEVs more competitive in terms of range, refueling time, and operational costs. The focus on green hydrogen production is also a critical trend, aiming to ensure the entire FCEV lifecycle is environmentally sustainable.

- Expansion of hydrogen refueling infrastructure globally.

- Increasing adoption of FCEVs in commercial and heavy-duty transport.

- Technological advancements in fuel cell efficiency and durability.

- Growing investment in green hydrogen production.

- Strategic partnerships among automotive, energy, and technology companies.

AI Impact Analysis on Fuel Cell Electric Vehicle

User queries regarding the impact of Artificial Intelligence (AI) on Fuel Cell Electric Vehicles often revolve around optimizing performance, enhancing safety, and improving manufacturing processes. AI is increasingly vital for predictive maintenance of fuel cell systems, managing hydrogen consumption for optimal efficiency, and enabling advanced driver-assistance systems (ADAS) or autonomous driving capabilities in FCEVs. The integration of AI algorithms allows for real-time monitoring of fuel cell health, anomaly detection, and optimization of power delivery, significantly improving vehicle reliability and reducing operational costs. This leads to a more intelligent and responsive FCEV ecosystem.

Beyond vehicle operation, AI also plays a transformative role in the manufacturing and design phases of FCEVs. Machine learning algorithms can accelerate the discovery of new catalyst materials, optimize the design of fuel cell stacks for maximum efficiency and longevity, and streamline production lines through automation and quality control. For the end-user, AI enhances the driving experience through personalized vehicle settings, intelligent navigation that accounts for refueling stations, and predictive analytics that inform maintenance schedules. As FCEV technology matures, the symbiotic relationship with AI will become even more pronounced, driving innovation and widespread adoption.

- Predictive maintenance and diagnostics for fuel cell systems.

- Optimization of hydrogen consumption and energy management.

- Enhancement of autonomous driving and ADAS features.

- AI-driven material discovery and fuel cell stack design optimization.

- Intelligent manufacturing and quality control in FCEV production.

Key Takeaways Fuel Cell Electric Vehicle Market Size & Forecast

Common user questions about the key takeaways from the Fuel Cell Electric Vehicle market forecast often focus on identifying the most lucrative growth areas, the primary catalysts for market expansion, and the enduring challenges that need to be addressed. The market's significant projected Compound Annual Growth Rate (CAGR) underscores a robust future for FCEVs, driven by increasing environmental regulations and the critical need for long-range, fast-refueling zero-emission vehicles, particularly in commercial applications. A key takeaway is the escalating investment in hydrogen infrastructure, which is foundational for enabling widespread FCEV adoption and overcoming historical limitations related to refueling accessibility.

Furthermore, the market's trajectory indicates a shift towards a more diversified FCEV portfolio, with heavy-duty trucks and buses emerging as strong growth segments due to their demanding operational profiles that benefit immensely from FCEV attributes like extended range and rapid refueling. Government incentives and corporate sustainability goals are pivotal in accelerating this adoption. While cost parity with conventional vehicles and the initial investment in hydrogen infrastructure remain hurdles, the long-term operational benefits and environmental imperatives are strong drivers for continued market expansion, making FCEVs a critical component of global decarbonization strategies.

- Significant growth anticipated, primarily driven by commercial vehicle electrification.

- Infrastructure development remains crucial for mass market adoption.

- Policy support and incentives are accelerating FCEV deployment.

- Technological advancements are continuously improving FCEV performance and cost-effectiveness.

- Hydrogen production, especially green hydrogen, is a key focus for sustainable growth.

Fuel Cell Electric Vehicle Market Drivers Analysis

The Fuel Cell Electric Vehicle (FCEV) market is significantly propelled by a confluence of factors including stringent global emission regulations, growing corporate sustainability commitments, and advancements in hydrogen production and infrastructure. Governments worldwide are implementing stricter mandates for vehicle emissions, pushing manufacturers and fleet operators towards zero-emission alternatives. FCEVs, with their only emission being water vapor, perfectly align with these environmental objectives, particularly for heavy-duty applications where battery electric solutions may face range or payload constraints.

Moreover, the increasing focus on energy independence and diversification of energy sources also acts as a strong driver. Hydrogen, being a versatile energy carrier, can be produced from various sources, including renewables, offering a pathway to reduced reliance on fossil fuels. Corporate sustainability initiatives also play a pivotal role, with major logistics and transportation companies committing to decarbonize their fleets, creating a robust demand for FCEVs. These drivers collectively contribute to the market's accelerated growth trajectory, fostering innovation and investment across the entire hydrogen value chain.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations & Zero-Emission Mandates | +8.2% | Europe, North America, Asia Pacific (China, Japan) | 2025-2033 (Long-term) |

| Advancements in Hydrogen Production & Infrastructure Development | +7.5% | Global, especially Japan, South Korea, Germany, California (US) | 2025-2033 (Mid to Long-term) |

| Increasing Demand for Heavy-Duty Zero-Emission Vehicles | +6.8% | Global Commercial Fleets, Logistics Sector | 2025-2033 (Mid to Long-term) |

| Government Incentives & Subsidies for FCEV Adoption | +5.1% | China, South Korea, Germany, US | 2025-2030 (Short to Mid-term) |

| Energy Security & Diversification of Fuel Sources | +4.9% | Europe, Asia Pacific | 2025-2033 (Long-term) |

Fuel Cell Electric Vehicle Market Restraints Analysis

Despite the promising outlook for Fuel Cell Electric Vehicles (FCEVs), several significant restraints could impede their widespread adoption and market growth. The primary challenge remains the underdeveloped hydrogen refueling infrastructure. The limited number of publicly accessible hydrogen stations, particularly outside of pioneering regions, creates range anxiety and inconvenience for potential FCEV owners and operators. This lack of infrastructure makes FCEVs a less practical choice compared to conventional gasoline vehicles or even battery electric vehicles (BEVs) which benefit from a rapidly expanding charging network.

Another considerable restraint is the high initial cost of FCEVs compared to their internal combustion engine (ICE) counterparts and even many BEVs. The complex manufacturing processes for fuel cells, the specialized materials required, and the relatively low production volumes contribute to higher purchase prices. Furthermore, the cost of hydrogen fuel itself, while potentially decreasing with scale, can still be a barrier in certain markets, especially if green hydrogen production is not yet economically competitive. Public perception and awareness also play a role; a lack of understanding about hydrogen safety and FCEV technology can deter consumers, requiring substantial educational efforts to overcome misconceptions and build trust.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Limited Hydrogen Refueling Infrastructure | -4.5% | Global, particularly emerging markets | 2025-2030 (Mid-term) |

| High Initial Cost of FCEVs & Hydrogen Fuel | -3.8% | Global, particularly price-sensitive markets | 2025-2029 (Short to Mid-term) |

| Competition from Battery Electric Vehicles (BEVs) | -2.7% | Global Passenger Vehicle Market | 2025-2033 (Long-term) |

| Public Perception & Safety Concerns Regarding Hydrogen | -1.5% | General Public, Less Informed Regions | 2025-2028 (Short-term) |

| Challenges in Large-Scale Green Hydrogen Production | -1.0% | Global, particularly industrial sectors | 2025-2033 (Long-term) |

Fuel Cell Electric Vehicle Market Opportunities Analysis

The Fuel Cell Electric Vehicle (FCEV) market presents significant opportunities driven by the unique advantages of hydrogen-powered mobility and evolving energy landscapes. One of the most prominent opportunities lies in the heavy-duty commercial vehicle segment, including long-haul trucks, buses, and trains. These applications greatly benefit from FCEVs' rapid refueling times and extended range capabilities, which are crucial for maintaining operational efficiency and minimizing downtime, aspects where battery electric vehicles often face limitations. As companies prioritize fleet decarbonization, the demand for FCEVs in this sector is poised for substantial growth.

Furthermore, the increasing global focus on developing a robust hydrogen economy, spurred by national strategies and international collaborations, creates vast opportunities for FCEV expansion. Investments in large-scale green hydrogen production, distribution networks, and the integration of hydrogen into existing energy systems are paving the way for more affordable and accessible hydrogen fuel. The development of advanced materials and manufacturing techniques for fuel cells and hydrogen storage also presents opportunities for cost reduction and performance enhancement. Niche applications such as material handling equipment (e.g., forklifts), marine vessels, and aviation also represent emerging high-growth segments for FCEV technology, diversifying the market beyond conventional road transport.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand in Heavy-Duty & Commercial Vehicles | +7.8% | Global Commercial Fleets, Logistics Sector | 2025-2033 (Long-term) |

| Development of Global Hydrogen Economy & Green Hydrogen Production | +6.5% | Europe, Asia Pacific, North America, Middle East | 2025-2033 (Mid to Long-term) |

| Technological Advancements in Fuel Cell Efficiency & Cost Reduction | +5.2% | Global R&D Hubs, Manufacturing Centers | 2025-2030 (Mid-term) |

| Expansion into Niche Applications (Marine, Rail, Aviation, Material Handling) | +4.7% | Specific Industrial & Transport Sectors Globally | 2027-2033 (Long-term) |

| Cross-Industry Collaborations for Integrated Solutions | +3.9% | Global, particularly among energy, automotive, & tech firms | 2025-2033 (Long-term) |

Fuel Cell Electric Vehicle Market Challenges Impact Analysis

The Fuel Cell Electric Vehicle (FCEV) market faces several critical challenges that demand strategic attention to ensure sustained growth and widespread adoption. One significant challenge is the ongoing "chicken-and-egg" dilemma concerning hydrogen infrastructure. Vehicle manufacturers are hesitant to produce FCEVs at scale without sufficient refueling stations, while energy companies are reluctant to invest heavily in infrastructure without a critical mass of FCEVs on the road. This symbiotic relationship creates a hurdle that requires coordinated efforts from both public and private sectors to overcome.

Another major challenge revolves around the current cost of hydrogen production, transportation, and storage. While green hydrogen offers a sustainable solution, its production is currently more expensive than hydrogen derived from fossil fuels, impacting the overall cost-effectiveness of FCEVs. The energy intensity of hydrogen production, even with electrolysis, adds to the complexity. Furthermore, competition from Battery Electric Vehicles (BEVs) is a persistent challenge, especially in the passenger car segment where BEVs have gained significant traction due to expanding charging networks, lower initial costs for many models, and broader public acceptance. Overcoming these challenges will require continuous innovation, policy support, and substantial infrastructure investment to unlock the full potential of the FCEV market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Comprehensive Hydrogen Refueling Network | -5.0% | Global, particularly nascent markets | 2025-2030 (Mid-term) |

| High Cost of Green Hydrogen Production & Distribution | -4.2% | Global, especially industrial consumers | 2025-2033 (Long-term) |

| Intense Competition from Established BEV Market | -3.5% | Global Passenger Vehicle Market | 2025-2033 (Long-term) |

| Limited Public Awareness and Perceived Safety Risks | -2.0% | General Public, Regions with Lower Exposure | 2025-2028 (Short-term) |

| Regulatory Hurdles and Standardization Issues | -1.2% | Cross-border markets, diverse regulatory environments | 2025-2029 (Mid-term) |

Fuel Cell Electric Vehicle Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Fuel Cell Electric Vehicle (FCEV) market, providing an in-depth analysis of market size, growth trends, key drivers, restraints, opportunities, and challenges from 2025 to 2033. It offers a detailed segmentation analysis across various vehicle types, components, applications, power outputs, and end-use sectors, ensuring a granular understanding of market behavior. The report also highlights regional market performances and profiles key industry players, providing strategic insights for stakeholders to navigate the evolving FCEV landscape and capitalize on emerging opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 850 million |

| Market Forecast in 2033 | USD 7.71 billion |

| Growth Rate | 32.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Toyota Motor Corporation, Hyundai Motor Company, Honda Motor Co., Ltd., BMW AG, General Motors, Daimler Truck AG, Ballard Power Systems Inc., Plug Power Inc., Cummins Inc., Hyundai Mobis, Hyster-Yale Materials Handling, Inc., ITM Power Plc, Linde plc, Nel ASA, Air Liquide S.A., Symbio, Faurecia SE, PowerCell Sweden AB, Nikola Corporation, Riversimple Movement Ltd. |

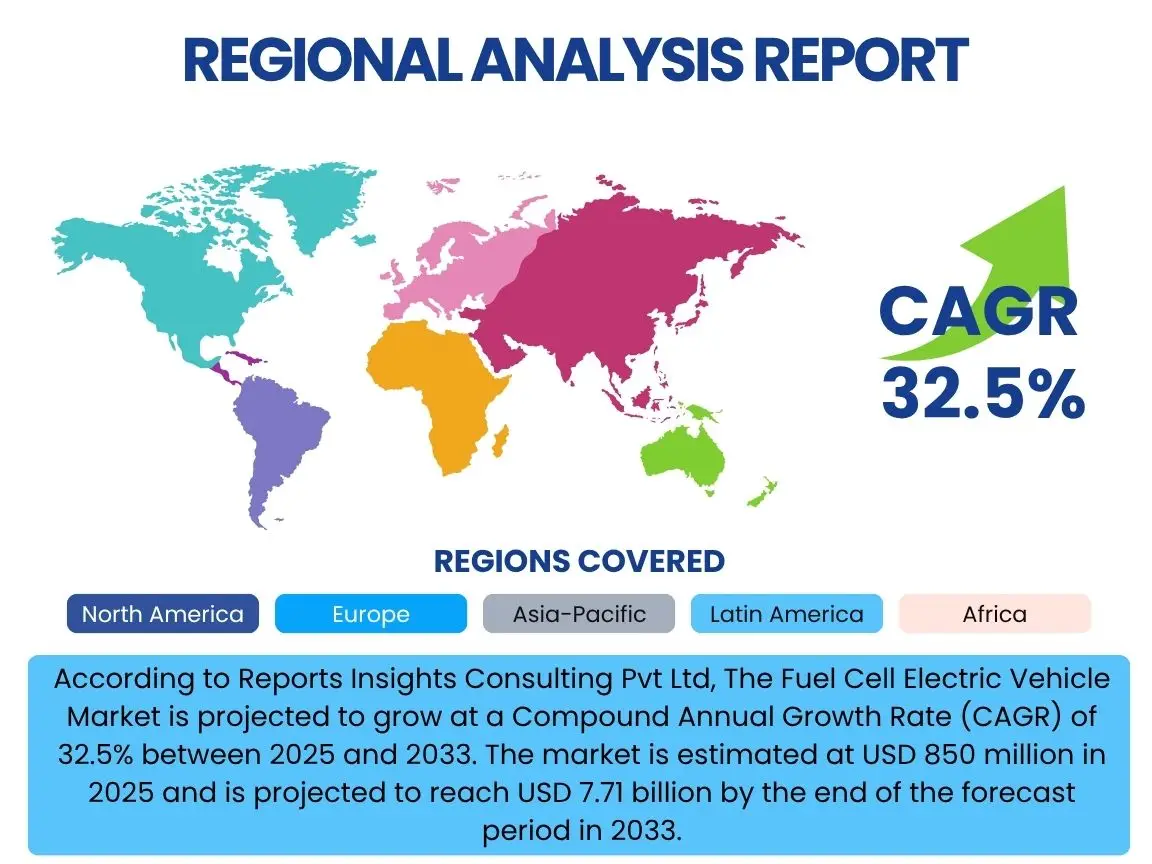

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fuel Cell Electric Vehicle market is meticulously segmented to provide a comprehensive understanding of its diverse landscape and to identify key areas of growth and opportunity. This segmentation allows for targeted analysis of market dynamics across different vehicle types, the critical components that form the core of FCEV technology, and various applications ranging from personal mobility to heavy industrial usage. By examining these distinct segments, stakeholders can discern specific market needs, technological requirements, and regulatory impacts, enabling more precise strategic planning and investment decisions.

Each segment, whether by vehicle type such as passenger cars or commercial trucks, or by component like fuel cell stacks and hydrogen storage systems, contributes uniquely to the overall market trajectory. The report further dissects the market by power output, catering to varying performance requirements, and by end-use, distinguishing between fleet operators, private consumers, and industrial clients. This granular approach not only highlights the evolving preferences and demands within the FCEV ecosystem but also underscores the multifaceted nature of hydrogen as a clean energy carrier for a wide array of transportation solutions.

- By Vehicle Type (Passenger Cars, Commercial Vehicles, Material Handling, Trains, Marine, Others)

- By Component (Fuel Cell Stack, Hydrogen Storage System, Balance of Plant, Power Control Unit, Electric Motor, Battery)

- By Application (Commercial Transport, Public Transport, Industrial & Logistics, Personal Mobility, Specialty Vehicles)

- By Power Output (Less than 50 kW, 50 kW - 150 kW, More than 150 kW)

- By End Use (Fleet Operators, Private Consumers, Government & Public Sector, Industrial Users)

Regional Highlights

- North America: The North American FCEV market is demonstrating steady growth, driven by environmental regulations in states like California and increasing corporate commitments to decarbonize logistics fleets. The region benefits from ongoing investments in hydrogen production and an expanding, albeit nascent, refueling infrastructure, particularly in commercial hubs. Government incentives and research initiatives also play a significant role in fostering market development, with a focus on heavy-duty applications.

- Europe: Europe is a frontrunner in FCEV adoption, largely due to ambitious decarbonization targets set by the European Union and strong national hydrogen strategies in countries like Germany, France, and the Netherlands. The region is witnessing robust growth in fuel cell buses and trucks, supported by a dense network of hydrogen corridors and cross-border collaborations aimed at establishing a comprehensive hydrogen economy. Significant public and private funding is being channeled into both FCEV deployment and green hydrogen infrastructure.

- Asia Pacific (APAC): The APAC region, led by Japan, South Korea, and China, dominates the global FCEV market. These countries have national hydrogen strategies, substantial government backing, and leading FCEV manufacturers. Japan and South Korea are pioneers in both FCEV technology and hydrogen infrastructure, while China is rapidly scaling up its FCEV fleet, especially for buses and heavy-duty trucks, leveraging its vast manufacturing capabilities and proactive policy support. The region's large population and growing demand for clean transportation make it a critical market.

- Latin America: The FCEV market in Latin America is in its nascent stages but holds considerable potential. Interest is growing, particularly in countries with abundant renewable energy resources suitable for green hydrogen production, such as Chile and Brazil. Pilot projects involving fuel cell buses and trucks are emerging, signaling a future trajectory towards adoption, though significant investment in infrastructure and policy frameworks will be essential for widespread market penetration.

- Middle East and Africa (MEA): The MEA region is emerging as a significant player in the global hydrogen economy, driven by its vast solar and wind energy potential for green hydrogen production. While FCEV adoption is currently limited, countries like Saudi Arabia and the UAE are investing heavily in hydrogen production and export capabilities, which could eventually support domestic FCEV markets. The focus is primarily on industrial and heavy transport applications, with potential for future expansion into public transport as infrastructure develops.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fuel Cell Electric Vehicle Market.- Toyota Motor Corporation

- Hyundai Motor Company

- Honda Motor Co., Ltd.

- BMW AG

- General Motors

- Daimler Truck AG

- Ballard Power Systems Inc.

- Plug Power Inc.

- Cummins Inc.

- Hyundai Mobis

- Hyster-Yale Materials Handling, Inc.

- ITM Power Plc

- Linde plc

- Nel ASA

- Air Liquide S.A.

- Symbio

- Faurecia SE

- PowerCell Sweden AB

- Nikola Corporation

- Riversimple Movement Ltd.

Frequently Asked Questions

How do Fuel Cell Electric Vehicles (FCEVs) work?

FCEVs generate electricity using a fuel cell that combines hydrogen and oxygen from the air, producing only water vapor as a byproduct. This electricity powers an electric motor to drive the wheels. Unlike battery electric vehicles, FCEVs create their own electricity onboard, allowing for longer driving ranges and quick refueling times, similar to conventional gasoline vehicles.

What are the main advantages of Fuel Cell Electric Vehicles over Battery Electric Vehicles (BEVs)?

FCEVs offer significant advantages such as rapid refueling (typically 3-5 minutes), extended driving ranges comparable to gasoline vehicles, and consistent performance in various climates. They are particularly well-suited for heavy-duty applications like trucks, buses, and trains where battery weight and charging times can be prohibitive, providing a more efficient solution for continuous operations.

What is the current status of hydrogen refueling infrastructure for FCEVs?

The global hydrogen refueling infrastructure is still in its developmental stages but is rapidly expanding, particularly in pioneering regions such as Japan, South Korea, parts of Europe (e.g., Germany), and California in the U.S. While the network is not yet as widespread as gasoline stations or EV charging points, significant investments are being made by governments and private entities to establish more robust and accessible refueling networks to support FCEV adoption.

Are Fuel Cell Electric Vehicles safe?

Yes, FCEVs are designed with stringent safety standards for hydrogen storage and handling, undergoing rigorous testing and certification. Hydrogen is stored in highly durable, crash-resistant tanks, and safety systems are in place to prevent leaks and manage potential incidents. Independent safety assessments and real-world performance have demonstrated their high safety record, similar to conventional vehicles.

What are the primary challenges hindering widespread FCEV adoption?

The main challenges include the limited availability of hydrogen refueling infrastructure, the high initial purchase cost of FCEVs compared to traditional vehicles and some BEVs, and the cost of producing green hydrogen. Additionally, overcoming public misconceptions about hydrogen safety and competing with the more established battery electric vehicle market are significant hurdles that the FCEV industry is actively addressing through innovation, policy support, and increased investment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted